MFN clauses can feel like a “small line” in an early-round document. But that one line can quietly shape your next raise, your cap table, and how much control you keep.

In plain words, MFN usually means “Most Favored Nation.” In startup deals, it often shows up in notes or SAFEs and says something like: if you give someone else better terms later, I get those better terms too.

That sounds fair on paper. And sometimes it is. But in early rounds, MFN can either protect you or trap you, depending on how it is written and how you use it.

This article is going to explain MFN clauses in a way that is simple, real, and useful. No legal fluff. No “it depends” and then silence. Just the practical truth founders need before they sign anything.

And one quick note: Tran.vc works with deep tech and AI teams where IP is the core asset. Terms like MFN matter even more when your value is your inventions, your model, your robotics system, your data pipeline, your hardware design—things that take time and money to build. If you want help building an IP plan early (and getting patent work done as an in-kind investment up to $50,000), you can apply anytime here: https://www.tran.vc/apply-now-form/

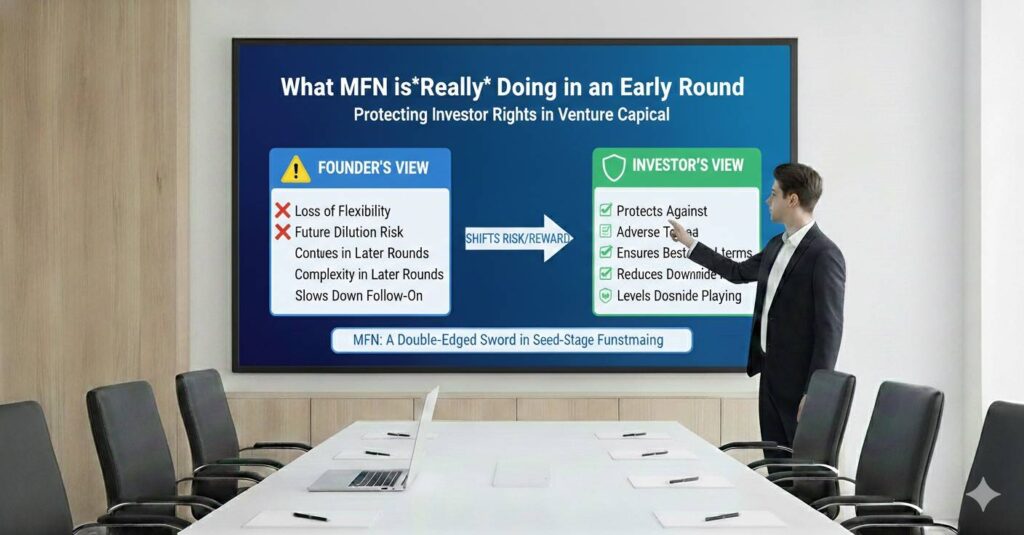

What MFN is really doing in an early round

At the earliest stage, most teams raise using a SAFE or convertible note. These tools exist because it is hard to price a company when you are still proving the product.

So instead of arguing about valuation, you raise now and convert later.

The big question becomes: convert into what terms later?

That is where MFN often enters.

An MFN clause is basically a promise:

If you sign a SAFE today, and then later you issue another SAFE that has better terms, the earlier investor can “upgrade” to those better terms.

That can mean better economics (like a higher discount), better protection (like a valuation cap when they did not have one), or extra rights (like pro rata or information rights). The exact meaning depends on the wording.

There is a common founder mistake here: they hear “MFN” and think it is one single thing, like a standard checkbox.

It is not.

MFN is more like a container. The container can hold small items or heavy objects. You need to know what is allowed inside.

Why early investors ask for MFN

In early rounds, investors feel one big fear: they invest before things are clear, and then someone else invests right after on sweeter terms.

They want to avoid being the “first check” that took the most risk but got the worst deal.

That is the emotional reason.

The business reason is simpler: early-stage deals move fast and are messy. MFN gives the investor comfort without making you negotiate every possible future case.

So MFN often shows up when:

- you are raising in pieces (not all at once),

- you are still learning your terms as you go,

- you are talking to different types of investors (angels, micro funds, strategic, accelerators),

- the market is shifting and the “standard” SAFE terms are changing.

MFN can be a tool to keep momentum. You might say: “I can’t promise these are final terms, but I can give you MFN so you won’t be disadvantaged.”

That can close a check faster.

But speed has a price. MFN can become a silent promise to many people at once.

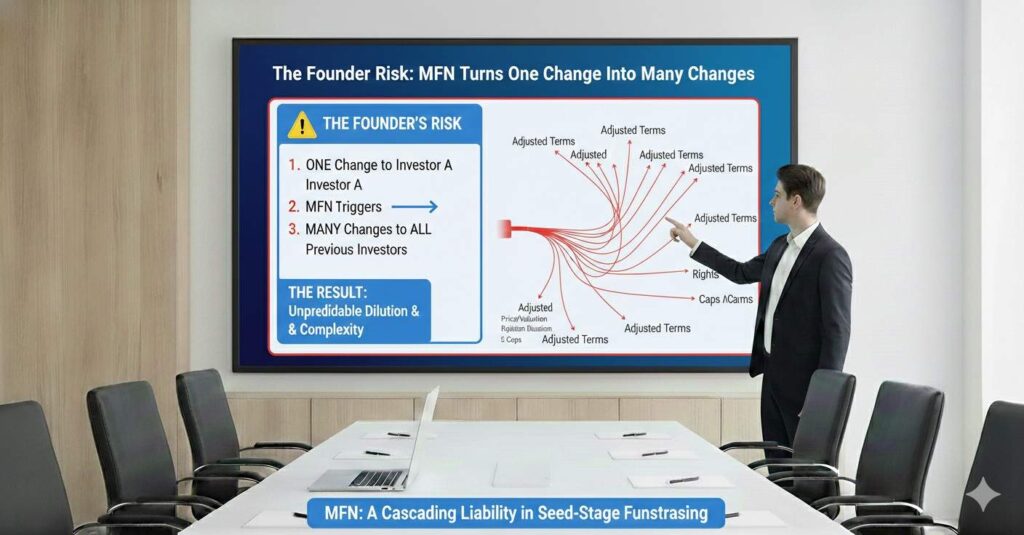

The founder risk: MFN turns one change into many changes

Here is the key issue.

In a rolling early round, you might sign 10 SAFEs over 3 months. If most of them have MFN, then every time you offer one person better terms, you may be offering those terms to all 10.

You may not notice the impact until later, when you are trying to close the round or prepare the priced seed.

Then you learn that the “one special SAFE” you used to land a strategic investor also upgraded everyone else. Now your cap table math looks very different.

This is why founders get burned by MFN:

- They treat MFN like a harmless fairness clause.

- They do not model what happens if it “spreads.”

- They do not limit what “better terms” means.

- They do not set a time window.

- They do not restrict MFN to only the same type of instrument.

And the hardest part: it is not always obvious. A clause might look short but still create a large ripple.

MFN is not always bad

Let’s be fair.

MFN can be useful when you are doing an early raise and you honestly do not know yet what terms the market will demand.

Example: you start raising with an uncapped SAFE. Two weeks later, stronger investors say they want a cap. You can either:

- go back and change earlier deals (slow, awkward), or

- offer MFN up front so you can improve terms later without drama.

In that case, MFN can reduce friction.

Also, MFN can keep you from playing favorites. If you do not want to be in the business of giving ten different deals, MFN can help you stick to one direction as you learn.

But “useful” is not the same as “safe.”

MFN needs boundaries.

The two biggest flavors of MFN you will see

Most founders first see MFN in one of these forms:

1) MFN on economic terms only

This means the earlier investor can adopt better economic terms you later offer to another investor in the same round. Economic terms usually mean things like valuation cap and discount rate.

This is the “lighter” version. It is still meaningful, but at least it is contained.

2) MFN on all terms (economic + rights)

This means if you later give any investor better terms of any kind, the earlier investor can elect to take them too. That can include rights that are not obvious: pro rata, information rights, board observer, side letter perks, or special approval rights.

This is the version that can turn into a problem.

Even if you think “we won’t give special rights,” reality is that early rounds often come with side letters. One investor asks for a small extra promise. It feels harmless. But MFN can “copy” that promise across your whole round.

So the biggest practical question is: what exactly is MFN allowed to match?

What “better terms” really means in practice

Founders often assume “better terms” means a lower valuation cap or a higher discount.

That is only part of it.

“Better” can show up in subtle ways. For example:

If you issue a SAFE that has a valuation cap and earlier ones did not, that might be “better” for the investor and would trigger MFN.

If you issue a SAFE with “cap + discount” and earlier ones only had a cap, that might be “better.”

If you issue a note with an interest rate or maturity date that is more favorable, that could count.

If you attach a side letter giving extra rights, that could count.

Even the definition of “future financing” can matter. Some MFNs allow matching if you issue a new convertible instrument; others are written broadly enough that a priced round might be implicated (depending on the wording).

This is why you do not want MFN language that is vague.

Vague language always becomes “clear” later, when there is conflict, and that clarity rarely helps founders.

The real-life moment MFN becomes a headache

The most common scenario looks like this:

You raise an early pre-seed on uncapped SAFEs. An angel writes $25k. You also give them MFN because they asked and you want to close fast.

A month later, a micro fund says they will invest $250k, but only if there is a valuation cap. You agree, because the round needs that anchor check.

Now your earlier angels with MFN can say: “Great. We take that cap too.”

If you have multiple MFN angels, they all upgrade.

Now you might think: “So what, they are small checks.”

But in early rounds, small checks stack. Five angels at $25k is $125k. Ten angels is $250k. If they all upgrade to a cap, you have changed the conversion economics for a big portion of your round.

That can matter a lot later when you do the priced seed and the math squeezes your founder ownership more than you expected.

MFN did not create the cap. But it amplified it.

And it amplified it without you having to sign new documents, which is the tricky part.

How MFN can quietly weaken your leverage in the next round

When you go raise a priced seed, good investors look at your existing stack of SAFEs and notes. They want to know how much will convert and under what terms.

If MFN clauses have made your SAFE stack messy, you may face:

- slower diligence,

- more legal cleanup,

- more confusion in the cap table model,

- pressure to renegotiate earlier instruments,

- or a seed investor asking you to “make the SAFE stack clean” before closing.

That is not fun when you are trying to hit payroll and build product.

The deeper issue is leverage.

Founders have the most leverage before they create complexity. Once complexity exists, your choices narrow.

So the goal is not “avoid MFN at all costs.” The goal is “use MFN in a way that does not reduce your options later.”

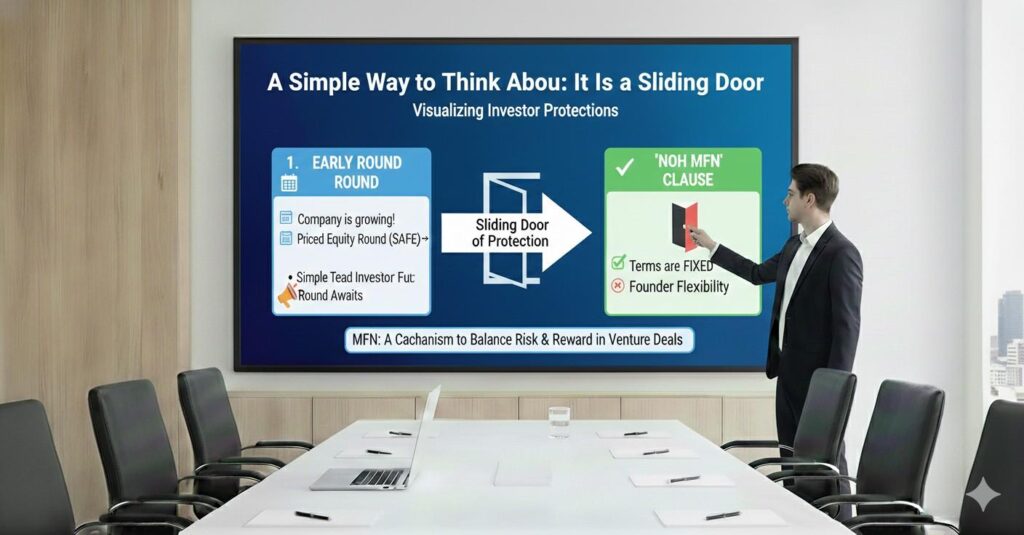

A simple way to think about MFN: it is a sliding door

Picture your round as a hallway with doors.

Every time you offer a new investor a different term, you open a door.

MFN means earlier investors can walk through that door too.

If you only plan to open one or two doors, MFN might be fine.

If you expect many special cases, MFN can turn your hallway into a wind tunnel.

This is also why experienced founders try hard to keep early rounds tight: one SAFE template, one set of terms, minimal side letters, minimal special promises.

MFN is often a sign that the round is drifting.

Where MFN shows up most often: SAFEs, notes, and side letters

You will commonly see MFN in:

- uncapped SAFEs (investor wants protection if cap appears later),

- notes with uncertain terms (investor wants matching if better note appears),

- side letters (investor wants to ensure they get the same extra rights later offered to others).

Side letters are worth special attention. Many founders do not treat side letters as “real deal terms.” They see them as small add-ons.

But MFN can treat them as part of the bargain.

The practical rule: if you agree to a promise in writing, assume MFN might copy it.

This is one reason Tran.vc pushes founders to treat early paperwork like product design. A small decision early can shape your system later. The same is true with IP: a single patent filing strategy choice can either give you a clean moat or a weak fence.

If you want a strong early foundation—both in deal terms and in IP—you can apply anytime: https://www.tran.vc/apply-now-form/

The most common MFN trap: “better” rights, not better price

Founders expect MFN to affect valuation caps and discounts.

What surprises them is rights.

One investor asks for pro rata. You say yes.

Another asks for information rights. You say yes.

A third asks for a “future advisory” right, or a right to participate in a pilot.

If your MFN clause is broad, earlier investors might be able to claim these too.

Now you have a situation where ten investors each think they have the right to more ownership later or more access now.

And the issue is not just legal. It is relationship management. You may spend time dealing with investor expectations instead of building.

So, even if you accept MFN, you want it to be focused.

What you want MFN to be tied to

Founders tend to do best when MFN is tied to:

- the same round,

- the same instrument type,

- and only a limited set of terms.

When MFN is tied to the “same round,” you avoid a world where terms from a later bridge financing or a different instrument suddenly apply.

When it is tied to “the same instrument,” you avoid cross-matching between SAFEs and notes, or between different SAFE versions.

When it is tied to “limited terms,” you avoid side letter spillover.

This is still a concept, not a negotiation script. But if you hold this concept in your head, you will spot problems faster.

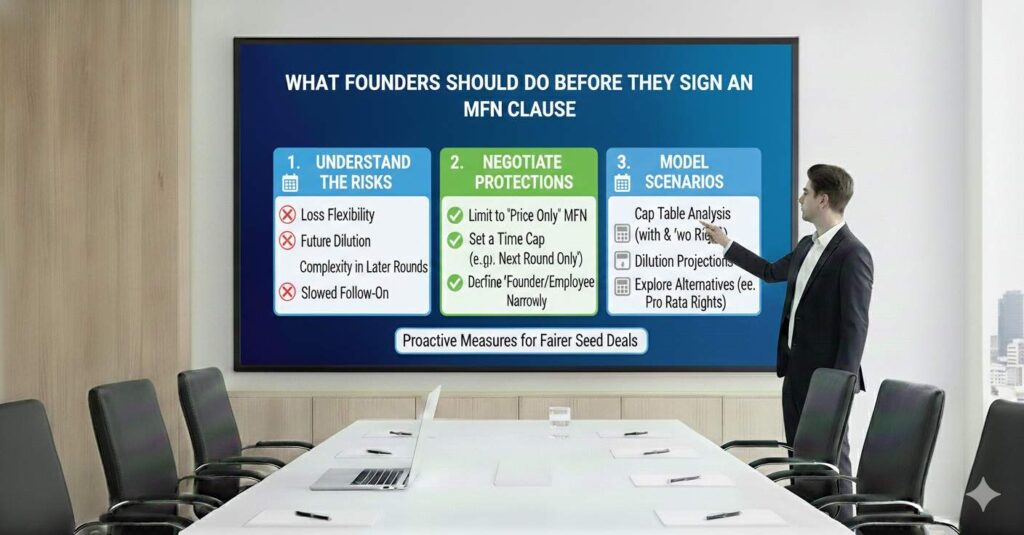

What founders should do before they sign an MFN clause

Before you sign, you need to answer one question honestly:

Am I willing for this investor to receive the best terms I offer to anyone else in this round?

If your answer is “yes,” MFN is probably fine, assuming it is written clearly.

If your answer is “no,” you need boundaries. Because you will eventually face a moment where you want to offer one investor a special term to close them.

And you do not want that special term to spread.

This is also where early strategy matters. Many teams try to “win” early rounds by being flexible. But being flexible with terms often becomes expensive later.

The best early rounds are not the ones with the fanciest terms. They are the ones that are clean, predictable, and easy to diligence.

A founder-friendly mindset: MFN is a promise, not a courtesy

Treat MFN like you would treat a product guarantee.

If you promise it, you must honor it. And it may cost more than you think.

So if someone asks for MFN, do not treat it as a small concession. Treat it as:

- a pricing policy,

- a future optionality trade,

- and a cap table complexity multiplier.

Sometimes it is still worth it. But you want to decide with open eyes.

One more thing: MFN and your story to investors

Early investors do not just look at your tech. They look at your judgment.

If your round terms look chaotic, it can signal that you are improvising.

If your terms are clear and consistent, it signals control.

That control matters in deep tech and AI, where timelines are longer and investors want proof you can manage risk.

That is part of Tran.vc’s philosophy: build leverage early. Protect what matters. Keep your structure clean. Build real assets, especially IP assets, so you are not forced to take bad terms later.

If you want that kind of help—patent strategy, filings, and real IP execution as an in-kind investment—you can apply here anytime: https://www.tran.vc/apply-now-form/

What MFN is really doing in an early round

The plain meaning behind the legal words

An MFN clause is a simple promise dressed in legal clothing. It tells an early investor: if you later give another investor a better deal, the early investor can switch to that better deal too.

In early rounds, this usually shows up inside a SAFE or a convertible note. You are not pricing the company yet, so the “deal” is mostly about what happens later when the money converts into shares.

So MFN is less about today and more about tomorrow. It is a future adjustment button that an investor can press if later reminders show up in your paperwork.

Why it feels harmless at first

MFN often looks like a short paragraph. It sounds fair, and it often is framed as “I just want to be treated like everyone else.”

Founders also like MFN because it can keep the round moving. If a small investor wants comfort and you do not want a long debate, MFN can close the gap fast.

The problem is that the short paragraph can cover a large space. If it is written broadly, it can pull in more changes than you meant to share.

Why founders must treat it like a real commitment

The safest way to think about MFN is to treat it like a binding policy. If you allow it, you are saying: I accept that this investor may later upgrade their terms.

That is not a courtesy. It is a promise that can carry real cost.

When you sign ten early checks with MFN, you are not making ten separate small promises. You are creating one large shared rule that can change your whole round.

Why early investors ask for MFN

The fairness logic investors use

Early investors take risk before the picture is clear. They invest when the product is early, the team is small, and the market proof is still forming.

They worry that the next investor will get a better deal simply because they arrived later. From their view, that is unfair because later investors often take less risk.

MFN is the way they protect against that outcome. It is their way of saying: if you improve the deal later, I should not be punished for being early.

The speed reason that makes MFN popular

Many early rounds are raised in parts. A founder might raise from angels first, then close a larger check from a fund later, and then fill the rest.

In that kind of rolling raise, terms can change as the founder learns what the market expects. MFN is used to avoid reopening old documents each time terms shift.

For investors, it reduces regret. For founders, it reduces the back-and-forth.