Provisional patents get talked about like they are a magic shield. File one, and investors will instantly take you seriously. Your startup is “protected.” Your pitch gets stronger. Your round gets easier.

Sometimes that is true.

But just as often, a provisional patent does almost nothing for fundraising. Worse, it can quietly hurt you if it is rushed, vague, or filed at the wrong time.

This article is about the real moment a provisional helps you raise. Not in theory. In practice. Especially for AI, robotics, and other technical startups where the product is hard to copy, hard to explain, and even harder to defend.

And if you are building something technical and you want to use IP to raise with leverage, you can apply anytime here: https://www.tran.vc/apply-now-form/

What a provisional patent really is (and what it is not)

A provisional patent is not a “patent.”

It is a filing that gives you a date. That is the main value. It says: “On this day, we disclosed this invention to the patent office.” That date can matter a lot later.

It also lets you say “patent pending.” That phrase can matter earlier, but only in certain fundraising situations.

A provisional does not get examined. It does not turn into an issued patent by itself. It does not stop a competitor from copying you tomorrow. It does not give you the right to sue anyone.

So why do founders file provisionals?

Because for the right company, at the right time, with the right content, a provisional can do three things investors care about:

It makes your story clearer.

It makes your moat more believable.

It reduces one big risk in a buyer’s or investor’s mind.

Those are fundraising benefits, not legal benefits.

The legal benefit is the priority date. The fundraising benefit is what that date can unlock—if you use it correctly.

The fundraising question investors are really asking

When a technical founder brings up patents, investors are not thinking, “Great, they have protection.”

They are thinking:

- Is this team building something real, or just describing an idea?

- If it works, can others copy it fast?

- If it becomes valuable, will the company own it, or will it leak out?

- Will IP become a deal blocker later?

Most seed investors will not fund you “because you filed a provisional.” They fund you because they believe you can win. A provisional only helps if it supports that belief.

So the better question is not, “Should we file a provisional?”

The better question is: “What fundraising risk are we trying to reduce, and will this provisional actually reduce it?”

If you cannot name the risk, you are likely filing for comfort, not strategy.

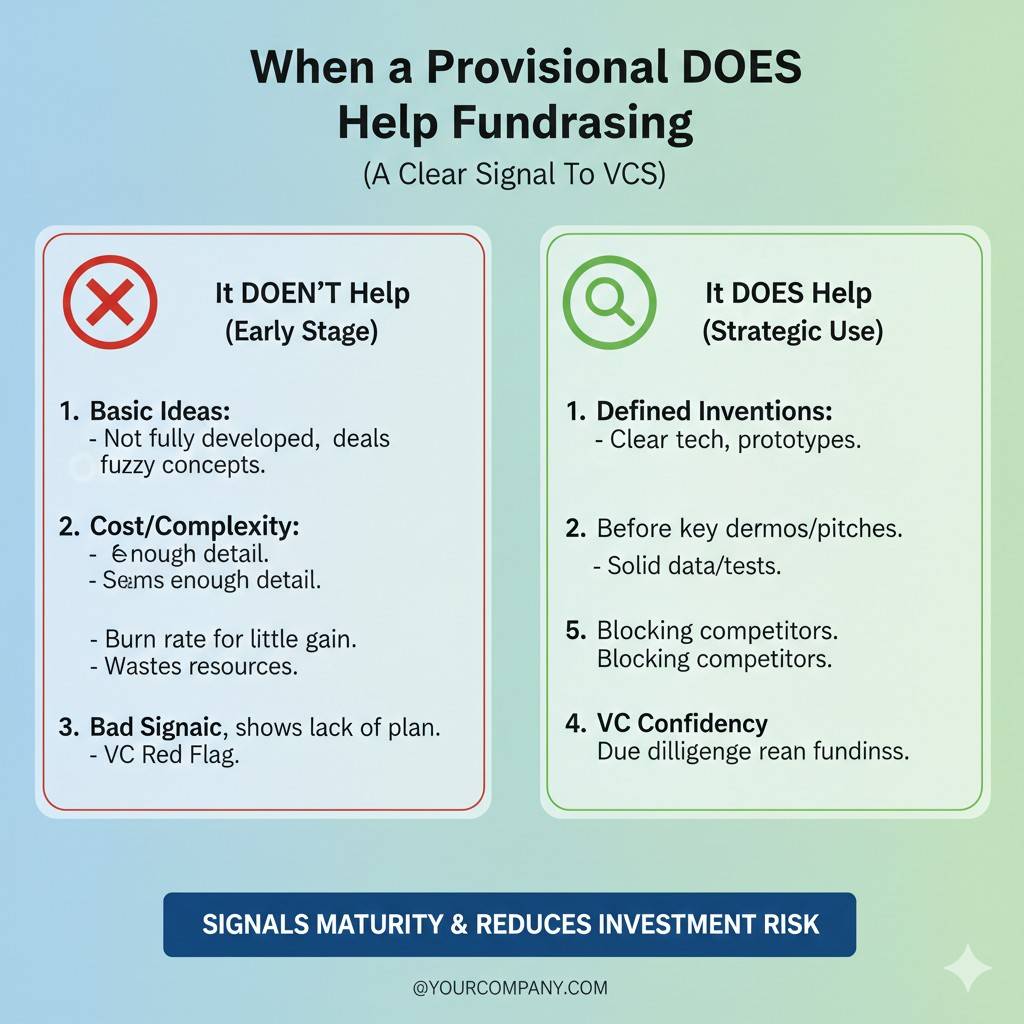

When a provisional does help fundraising

A provisional helps fundraising when it turns uncertainty into confidence.

That happens in a few common situations in AI, robotics, and deep tech.

1) When the investor needs proof you are past the “idea stage”

Some startups pitch like this:

“We are building a system that uses AI to do X.”

That can be real, or it can be vapor.

When you file a good provisional, you are forced to write down what is actually new. You describe the system, the steps, the logic, the workflow, the inputs and outputs, and the edge cases. You capture how it works in enough detail that a skilled person could reproduce it.

That level of detail is not just for the patent office. It becomes a powerful internal asset.

It shapes your pitch.

It sharpens your demo.

It makes your deck less vague.

It makes the investor feel you have substance.

In fundraising, clarity is power. A strong provisional often creates clarity because it forces you to stop hand-waving.

But this only works if the provisional is detailed. A rushed “five-page” filing with generic language does not create clarity. It creates questions.

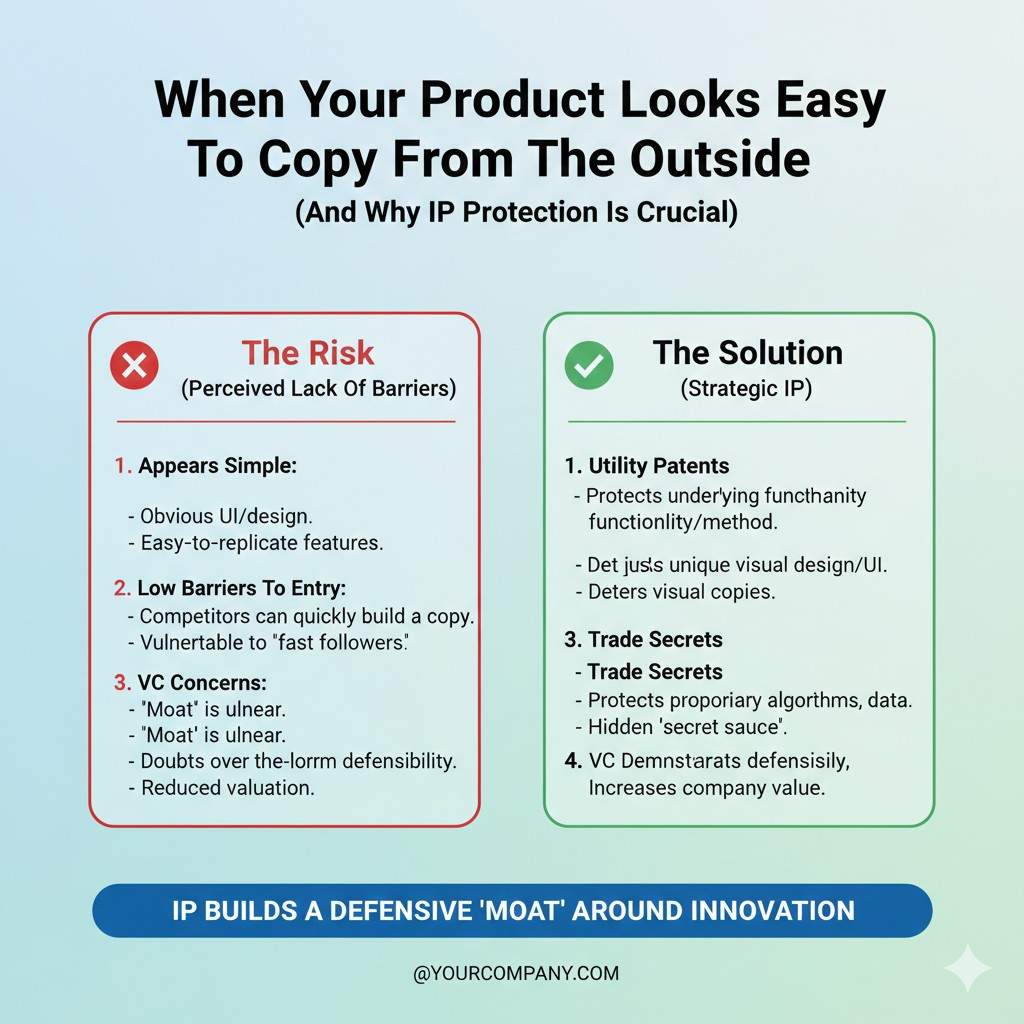

2) When your product looks easy to copy from the outside

Many AI and robotics startups have the same problem.

From the outside, the product looks simple.

A robotics company might say: “We pick items from bins.”

An AI company might say: “We summarize calls.”

A computer vision company might say: “We detect defects.”

An investor hears that and thinks: “So what? Ten teams can do that.”

If your real advantage is inside—your motion planning method, your calibration approach, your data pipeline, your feedback loop, your training method—then you need a way to show there is hidden depth.

A provisional can help by letting you claim ownership of the “inside” work. Not in a braggy way. In a grounded way.

You can say: “We filed on our method for X.”

You can show a simple diagram in your deck that matches what you filed.

You can explain that your approach is not just a model choice, it is a full system.

This does not mean the investor thinks, “Competitors can’t touch them.”

It means the investor thinks, “They have a real technical wedge, and they are taking it seriously.”

That is often enough at pre-seed.

3) When you are raising from investors who care about IP as a filter

Not all seed investors weigh IP the same way.

Some do not care at all at pre-seed. They care about speed and market pull.

But deep tech seed investors often use IP as a quick filter. Not because they expect an issued patent now. Because they have learned that teams who do not manage IP early can create huge problems later.

Examples investors worry about:

The invention was published before filing.

The key method was disclosed in a blog post.

A founder used code from a prior employer.

A research lab claims ownership.

A contractor owns part of the work.

A competitor filed first.

A provisional does not fix everything, but it can show discipline. It signals that you know IP is part of the game.

If you are building robotics, medical tech, hardware-software systems, or frontier AI methods, many investors will ask, “What is your IP plan?”

Having no answer is a red flag.

Having a clean answer is calming.

A provisional is often the simplest “first step” answer—if it is aligned with a plan.

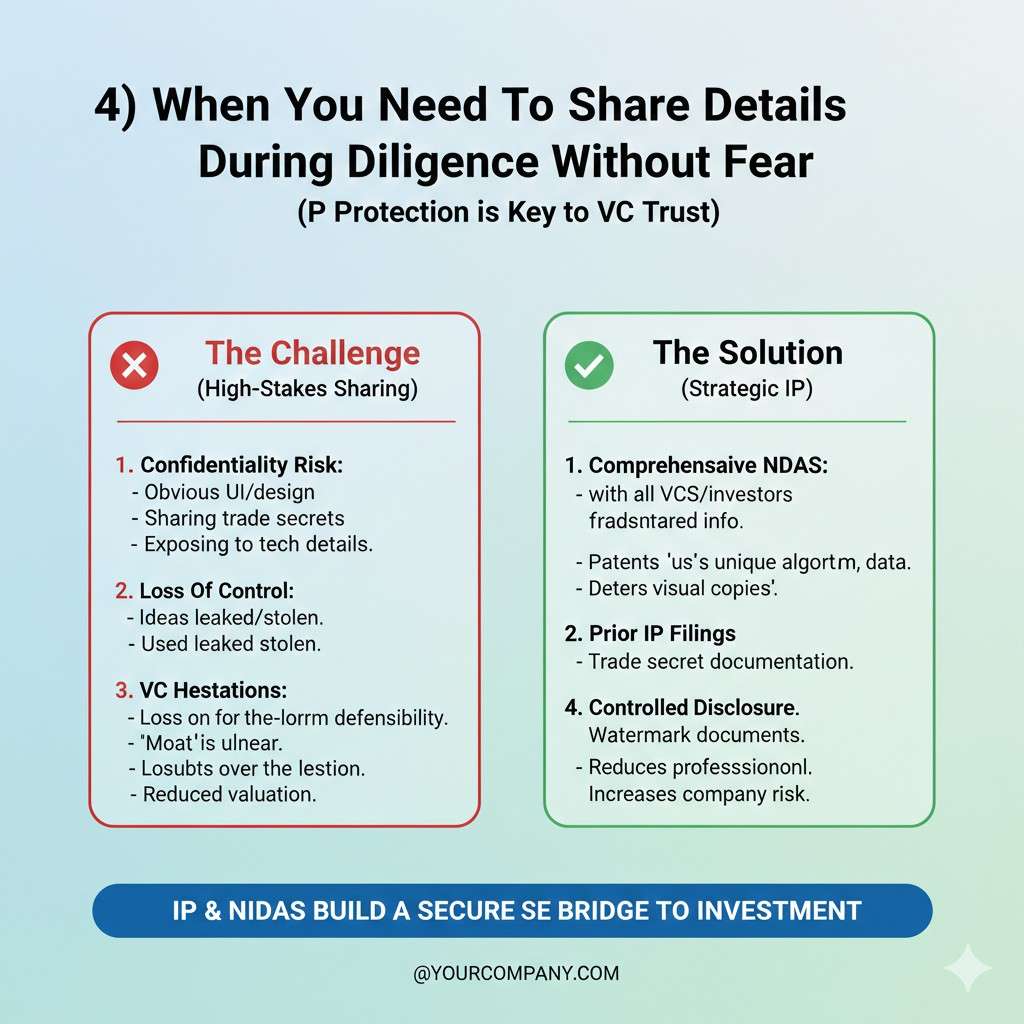

4) When you need to share details during diligence without fear

Fundraising has an awkward problem:

To raise, you need to explain your product clearly.

But if you explain it clearly, you feel exposed.

Some founders respond by being vague. That hurts the raise.

A provisional can reduce that fear. It gives you a date. It gives you language. It gives you a way to disclose more comfortably.

This is especially useful when:

You are pitching strategic angels who understand the space and will ask hard questions.

You are talking to corporate partners.

You are pitching investors who will run detailed technical diligence.

A good provisional does not mean you can share everything without thought. You still should be careful. But it can help you speak more openly, which often helps you raise faster.

5) When your company may exit through acquisition

Many deep tech companies do not go public. They get acquired.

Acquirers care about IP in a very practical way: they do not want to buy a lawsuit.

During an acquisition, lawyers ask:

What patents do you have?

What did you file?

When did you file?

Do you own it?

Did you disclose it before filing?

A provisional can become part of the chain that answers those questions.

This matters for fundraising because some investors are already thinking about the exit path. If they believe the likely exit is acquisition, they may care more about early filings than a typical SaaS investor would.

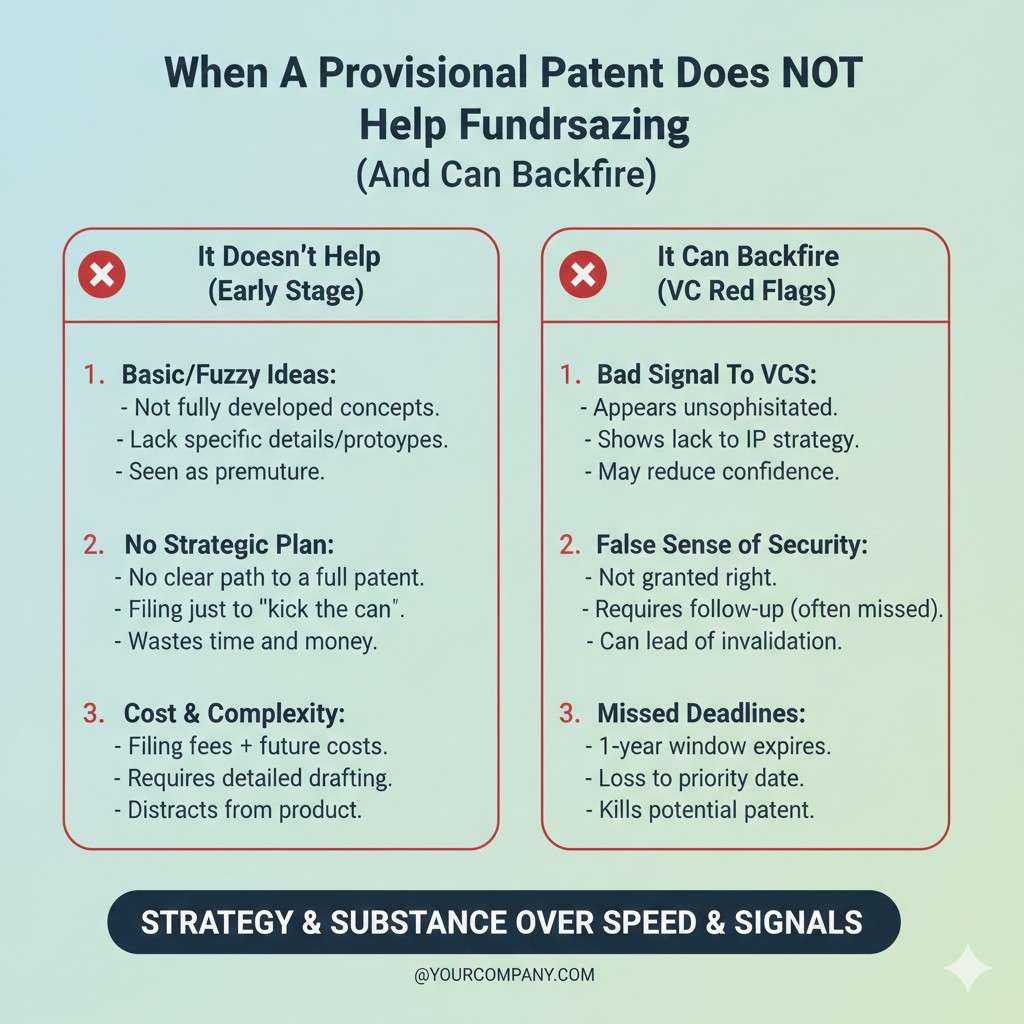

When a provisional does not help fundraising (and can backfire)

This part is important because founders waste money here.

A provisional often fails to help when it is treated like a checkbox.

The “thin provisional” problem

Many founders file something light:

A short description.

A few drawings.

A broad claim-like paragraph.

Not enough detail to reproduce the invention.

It feels done. But it is not.

Later, when you file the non-provisional (the real application), you want to rely on the provisional for your early date. But if the key details were not in the provisional, you may not get that benefit.

From a fundraising perspective, thin provisionals can also hurt because sophisticated investors can sense it. They ask:

“What exactly did you file on?”

“Can you explain the inventive part?”

“Does it cover the system or just the concept?”

If the answer is fuzzy, the investor learns something they did not want to learn: the team is either not careful, or not as deep as the pitch suggests.

That is the opposite of what you want.

Filing too early, before you know what is actually unique

Some founders file the moment they have a concept.

Then they build for six months and realize the real breakthrough is different.

Now the provisional covers the wrong thing.

This is common in AI. Early on, you think the novelty is the model. Later you realize the novelty is the data pipeline, the labeling method, the retrieval setup, the evaluation loop, or the edge deployment workflow.

A provisional should capture what is truly new. If you file before you know that, it becomes a dead document.

Filing too late, after you already disclosed

Some teams post a technical blog. Or publish a paper. Or demo at a public event. Or upload code. Or share detailed slides.

Then they file.

That can be a major mistake depending on where you want protection. It can also create messy investor questions. Even if the startup is still investable, it adds friction.

Fundraising is smoother when your IP story is clean.

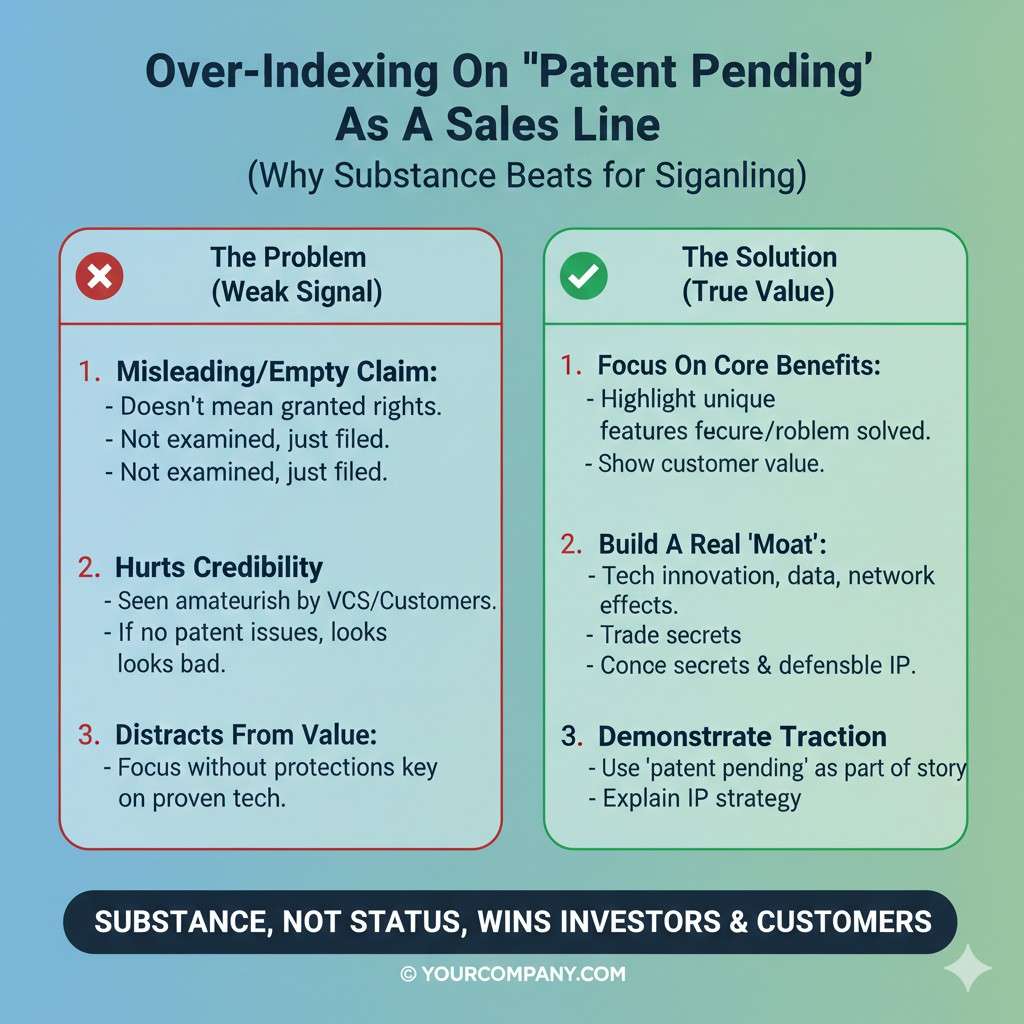

Over-indexing on “patent pending” as a sales line

Saying “patent pending” in a deck is not a strategy. Investors have seen it too many times.

The right use is not to brag. The right use is to support a specific point:

“We filed on our approach to X, which is the hardest part to reproduce.”

“We filed on the method that makes the cost drop by 10x.”

“We filed on the part that creates the data advantage.”

That shows thought. “Patent pending” alone does not.

The real “fundraising moment” a provisional supports

A provisional is most useful at a specific moment in a startup.

It is when you have enough technical shape to describe the invention clearly, but you are still early enough that the story is forming.

In other words:

You can explain what is different.

You have early evidence it works.

You are about to show it to outsiders.

You are about to pitch seriously.

That is often the pre-seed window.

This is exactly where Tran.vc fits. Instead of telling founders to burn cash on a rushed filing, we focus on helping you capture the invention properly and align it with your raise.

If you are in that window and you want IP to support fundraising, you can apply anytime here: https://www.tran.vc/apply-now-form/

What a “fundraising-ready” provisional looks like

To help fundraising, the provisional has to do one main job:

It has to capture the invention in a way that matches the story you are selling.

That sounds simple, but many provisionals fail because they do not match the pitch.

A fundraising-ready provisional typically has:

A clear problem statement tied to a real bottleneck in the market.

A plain explanation of what is new, not just what is built.

Enough detail that a skilled person could rebuild it.

Multiple versions of the core method, not just one.

Diagrams that make the system feel real.

Language that reflects your product path, not just theory.

Notice what is missing: fancy legal writing.

You do not win fundraising by sounding like a law firm. You win by sounding like a team that understands its own tech deeply.

A simple test: could you defend your “novelty sentence” in a meeting?

Here is a practical exercise.

Write one sentence:

“Our invention is ______.”

Now ask:

Could we defend that sentence for 10 minutes in a meeting with a skeptical technical investor?

If you cannot, filing a provisional today will likely be wasteful.

If you can, you are close. And the next step is to translate that sentence into a real disclosure with detail.

This is also a good way to avoid the common trap of filing on the wrong thing. The novelty sentence should match what makes you win.

The most common investor questions about provisional patents

If you bring up a provisional in fundraising, expect these questions.

Not always out loud. Sometimes they are thinking it.

“What exactly did you file on?”

If you answer with buzzwords, the investor will assume the filing is weak.

A strong answer is specific but simple:

“We filed on our calibration method that lets low-cost cameras hit high accuracy.”

“We filed on our planning approach that keeps the robot stable on uneven ground.”

“We filed on the workflow that creates training data from user behavior without manual labeling.”

“Is it the core of the company, or a side feature?”

Investors do not care if you filed on something that is not central.

If the filing is on the true core, it supports the story.

If it is on a side detail, it looks like noise.

“Will this matter in 18 months?”

Investors know provisionals expire after 12 months unless you convert. They want to know if you can follow through.

You do not need to promise ten patents. You need to show a plan that matches your stage.

Even a simple plan helps:

“We filed now so we can share details during diligence. We will convert once the product design is stable.”

That is sane. It shows you are not filing blindly.

How to use a provisional in your pitch without sounding cheesy

Founders often do it wrong by adding one bullet:

“Patent pending.”

That is not useful.

The better approach is to tie it to the business value.

For example, instead of “patent pending,” you say:

“We have a defensible method that reduces cycle time by 40%. We filed a provisional on the core method.”

Now the investor connects the IP to a result.

The goal is not to impress. The goal is to reduce doubt.

A quick note on “stealth” and fear of getting copied

Many early founders stay vague because they fear copying. That fear is understandable.

But in most fundraising cases, being vague is more dangerous than being copied.

Why?

Because you need belief to raise. And belief comes from detail.

A provisional can help you share detail with more comfort. But it is not an excuse to share everything everywhere. It is a tool. You still need judgment.

Where Tran.vc comes in

Most technical teams do not need “more patents.” They need a smarter first step.

Tran.vc invests up to $50,000 as in-kind patenting and IP services. The goal is not paperwork. The goal is leverage.

Leverage in fundraising.

Leverage in partnerships.

Leverage in future pricing and positioning.

And the key is doing the right filing at the right time, tied to what actually makes your company hard to copy.

If you want to see if a provisional filing would help your raise, you can apply here anytime: https://www.tran.vc/apply-now-form/

Timing a Provisional So It Helps Fundraising

The simple timing rule most founders miss

A provisional helps fundraising most when it supports a story you are already ready to tell.

That means you have a working shape of the invention, not just a goal. You can explain what you built, how it works, and why it is different. You also have enough proof to show it is not a guess.

If you file before you can explain the “different part,” the provisional becomes a weak paper trail. If you file after you have already shared details publicly, the filing can lose a lot of value in key countries.

The three “moments” when filing makes sense

The first moment is right before you start serious investor talks.

This is when you know you will be asked technical questions and you want to answer with confidence. A filing here can reduce fear and help you speak clearly, without hiding the details that make your work real.

The second moment is right before you share details with outsiders like pilots, partners, or big customers.

Robotics and enterprise AI often require early partner work. Those discussions can force you to share methods, diagrams, and workflows. A well-made provisional gives you a clean “we filed before we shared” story.

The third moment is right before a public reveal.

That could be a conference demo, a paper, a launch post, an open-source repo, or even a talk at a startup event. If you plan to share, you want the filing date to come first.

Why “file the night before demo day” often fails

Many founders treat the provisional like an emergency shield.

They rush to file the night before a pitch day or a press launch. They send a half-finished draft. They skip drawings. They skip alternate versions. They skip the edge cases.

Then investors ask simple follow-ups, and the team cannot explain what is truly covered. The filing becomes a line in a deck, not a real asset.

In fundraising, weak signals can be worse than no signals. If you mention IP, you invite scrutiny. If the filing is thin, scrutiny turns into doubt.