Foreign money can help you move fast. It can also quietly break your company if you don’t set it up right.

That sounds harsh, but it’s true. Most founders don’t mess up FDI (Foreign Direct Investment) compliance on purpose. They mess it up because they don’t even know it exists until a bank, a lawyer, or an investor asks a scary question like:

“Is your cap table FDI-compliant?”

And then you realize: the issue is not only the money. It is the paper trail, the pricing, the sector rules, the timing, and the forms you should have filed weeks or months ago.

This matters very early—often before your first real “round.” Because FDI can enter your startup in many ways that don’t feel like FDI:

A US-based angel who sends funds to your India company

A Singapore holding company you create to make global sales easier

A SAFE note that converts later

A foreign co-founder who owns shares

A foreign parent company that funds the India subsidiary

Even some cases of “services for equity” or IP being moved across borders

If any of that touches your setup, you need to know what you’re checking. Not later. Now.

This article is written for founders who want to build clean from day one. The goal is simple: help you avoid the common traps early, so you don’t pay for them later when you’re busy shipping product, hiring, and trying to raise.

Also, quick note: Tran.vc helps technical founders build strong IP from the start—patents, strategy, and filings—so you create real assets that investors respect. If you’re building in AI, robotics, or deep tech, you can apply anytime here: https://www.tran.vc/apply-now-form/

Before we go deep, one important line: FDI rules are country-specific. In India, they are shaped by FEMA and RBI rules, plus sector policy. In the US, it’s different. In the EU, different again. Many Tran.vc founders build “global-first,” so they end up with more than one jurisdiction in play. In this post, I’ll speak in a way that stays practical and widely useful, but I’ll often use India-flavored examples because that’s where founders get hit the most by FDI filings and bank checks.

Now let’s start the real work.

FDI compliance is not one thing. It is a chain.

Think of FDI compliance like a chain of small steps that must match each other:

Who invested

Where they invested from

What your company does

What your share structure is

How much you charged per share

When money came in

When shares were issued

What filings were made

How the money was used

Whether any IP moved across borders

When one link is weak, the chain breaks. And when it breaks, it almost never breaks when you have time. It breaks during diligence, during a bank remittance, or during a follow-on round when a new investor does a deeper check.

So the goal is not to “do everything.” The goal is to set up a simple system so you don’t miss the few things that matter most.

Let’s talk about the checks founders must do early. Not a long list. Just the ones that stop disasters.

The first check: Are you even allowed to take foreign money?

This sounds basic, but it’s where many issues begin.

FDI rules often depend on what sector you operate in. Some sectors allow 100% foreign investment with no special approval. Some allow it but only up to a limit. Some need approval first. Some have special conditions.

The painful part is that the sector is not always obvious. A founder may say, “We are an AI company.” But regulators and banks may classify you based on your real use case.

If you are building software for hospitals, you might touch health services rules.

If you are building drones, you might touch defense or aviation rules.

If you are building a lending product, you might touch finance rules.

If you are building a marketplace, you might touch ecommerce rules.

If you are building a data product, you might touch data rules.

The early action here is not to panic. It is to write a clear one-paragraph description of what you do, how you make money, and who pays you. This single paragraph becomes the base for:

your sector classification

your investor memo

your bank explanation

your diligence response later

When you don’t write it early, every document says something different. And inconsistency is what makes compliance teams nervous.

If you are unsure whether your sector has limits, treat that as a red flag and check it immediately. Because if you take foreign money into a restricted sector without following the right path, fixing it later can become slow and expensive.

Also, if you are building deep tech, you may be more likely to touch controlled areas like aerospace, defense, telecom, mapping, and certain hardware supply chains. It’s not about fear. It’s about clarity.

If Tran.vc supports you, one of the side benefits of strong IP work is that you’re forced to describe your tech precisely. That same clarity helps when you explain what you do to banks and investors. If you want help building that foundation, apply anytime: https://www.tran.vc/apply-now-form/

The second check: Who is “foreign” in your cap table?

This is where founders get surprised.

Many people think “foreign investor” means a big VC fund outside the country. Not true.

Depending on your country’s rules, “foreign” can include:

A non-resident individual

A foreign citizen living in your country

A company registered outside your country

A fund with non-resident control

Sometimes even an entity that looks local but is controlled from outside

This matters because the same person can be “resident” for tax but “foreign” for investment rules. Or the opposite. The definitions are technical and can change based on facts like where they live, how long they’ve lived there, and what documents they hold.

Early founder move: treat “who is foreign” as a field in your cap table, not a guessing game.

Add a simple column in your cap table notes: Resident / Non-resident (based on the applicable rule set). And keep the proof in your records. Not because you want paperwork for fun. Because six months later, you won’t remember why you tagged someone a certain way, and you’ll be stuck.

This becomes extra important with co-founders.

If one co-founder is non-resident and holds equity from day one, you may already have a foreign holder. That is not wrong. It just means you have compliance steps from day one. And you want those steps clean before you add outside investors.

The third check: Are you taking money as equity, debt, or something in between?

This is the most common trap in early-stage fundraising.

Founders use SAFE notes, convertible notes, simple agreements, and “advisor equity” deals because they feel easy. But different countries treat these instruments in different ways for FDI purposes.

Some instruments may be treated as equity from the start.

Some may be treated as debt until conversion.

Some may not be allowed for foreign investors without conditions.

Some may need specific reporting at receipt, even before conversion.

And here’s the twist: banks often do not care what you call it. They care how it fits into their compliance checklist.

So, early action: before you accept funds from outside your country, decide what instrument you will use and confirm whether it is allowed for that investor type.

If you’re thinking, “But we’re only raising a small angel round,” that is exactly when you should do this. Small rounds are where messy paperwork begins. Big rounds are where investors discover it.

The fourth check: Pricing and valuation are not “just internal”

This part hurts founders because it touches ego and negotiation.

FDI rules in many places require that when you issue shares to a foreign investor, you follow a pricing guideline. In India, for example, equity shares issued to a non-resident must follow a valuation approach that meets certain standards. If you price shares too low, you can get flagged.

Founders sometimes do “friendly pricing” for early foreign angels. They set a very low price per share because it feels generous and simple. Then later, when the next round prices higher, the earlier issuance looks like a discount that may not fit rules.

The fix is not to overprice. The fix is to document.

If you issue equity to a foreign investor, have a valuation basis on file. It can be a proper valuation report when needed. It can also be a documented method based on the rules. The key is that you can defend it later.

Because diligence is not only “Did you file a form?” It is also “Was the issuance done at a valid price?”

If you plan to build patents and other IP assets early, that can support your valuation story in a very real way. Investors understand IP as value. Clean IP plus clean documentation makes your valuation easier to defend. If you’re building something technical and want that leverage, apply anytime: https://www.tran.vc/apply-now-form/

The fifth check: Timing is everything

A lot of FDI compliance is about deadlines.

Money comes in on a date.

Shares are issued on a date.

Government reporting has a deadline from those dates.

Your corporate approvals (board, shareholders) must also happen in a certain order.

Founders often do the work in reverse.

They take money first.

Then they “figure out paperwork.”

Then they issue shares late.

Then they miss the filing window.

Then the bank asks questions during the next remittance.

This is not a moral failing. It’s normal startup chaos. But you can stop it with a simple habit:

Before you accept any foreign funds, write down the timeline you will follow.

Date money arrives → within X days do board approval → within Y days issue shares → within Z days complete reporting.

The exact X, Y, Z depend on your country, your instrument, and your sector. But the principle is universal: treat it like shipping code with deadlines. If you miss it, you create tech debt. Compliance debt works the same way, except the interest is paid in legal fees and delayed rounds.

The sixth check: Your bank is part of your compliance system

Many founders believe compliance is between them and the government. In practice, your bank is a gate.

Banks run checks on foreign remittances. They ask for forms, declarations, and documents. If the bank is not satisfied, money can be held, returned, or delayed.

The painful moment is when your runway depends on that wire.

So early, build a strong relationship with your bank branch and the person who handles inward remittances. Ask them what documents they typically ask for. Then create a folder with those items ready.

This is not overkill. This is survival.

Also, when you have IP work going on—patent drafting, invention disclosures, filings—keep records clean. When someone asks why funds were used, being able to show real IP work products is strong proof that money went into company building, not personal benefit.

Tran.vc’s model is in-kind IP services up to $50,000 value. That means you get real patent attorney work without draining early cash. It’s also easier to document because the scope is clear and professional. If that is useful, apply anytime: https://www.tran.vc/apply-now-form/

The seventh check: IP movement can trigger cross-border issues

This is a big one for AI and robotics founders.

You may have an India dev team and a US parent.

You may incorporate in Delaware and have an India subsidiary.

You may file patents in one country while R&D happens in another.

You may assign inventions from founders to the company.

All of that touches cross-border IP and payments.

If your India company pays your US parent for “IP license,” that can trigger rules on royalties, transfer pricing, withholding tax, and sometimes caps or approval. If your US parent “owns” the IP while India team builds it, you need clean agreements to show who created what, who owns it, and how value moves.

This is where many startups accidentally create a future tax and compliance fight, because the early documents were copied from the internet and don’t match reality.

The early action is simple: map the IP path.

Who is writing the code?

Who is inventing the system?

Which entity will own the patents?

Which entity will sign customer contracts?

Where will revenue land first?

How will money move between entities?

You do not need a 40-page memo. You need a one-page map that matches how you actually operate.

Tran.vc is built for this kind of founder problem, because IP strategy is not only about filing patents. It is also about ownership, assignments, and clean chains of title. That chain is exactly what investors want to see later. If you want help getting it right early, apply anytime: https://www.tran.vc/apply-now-form/

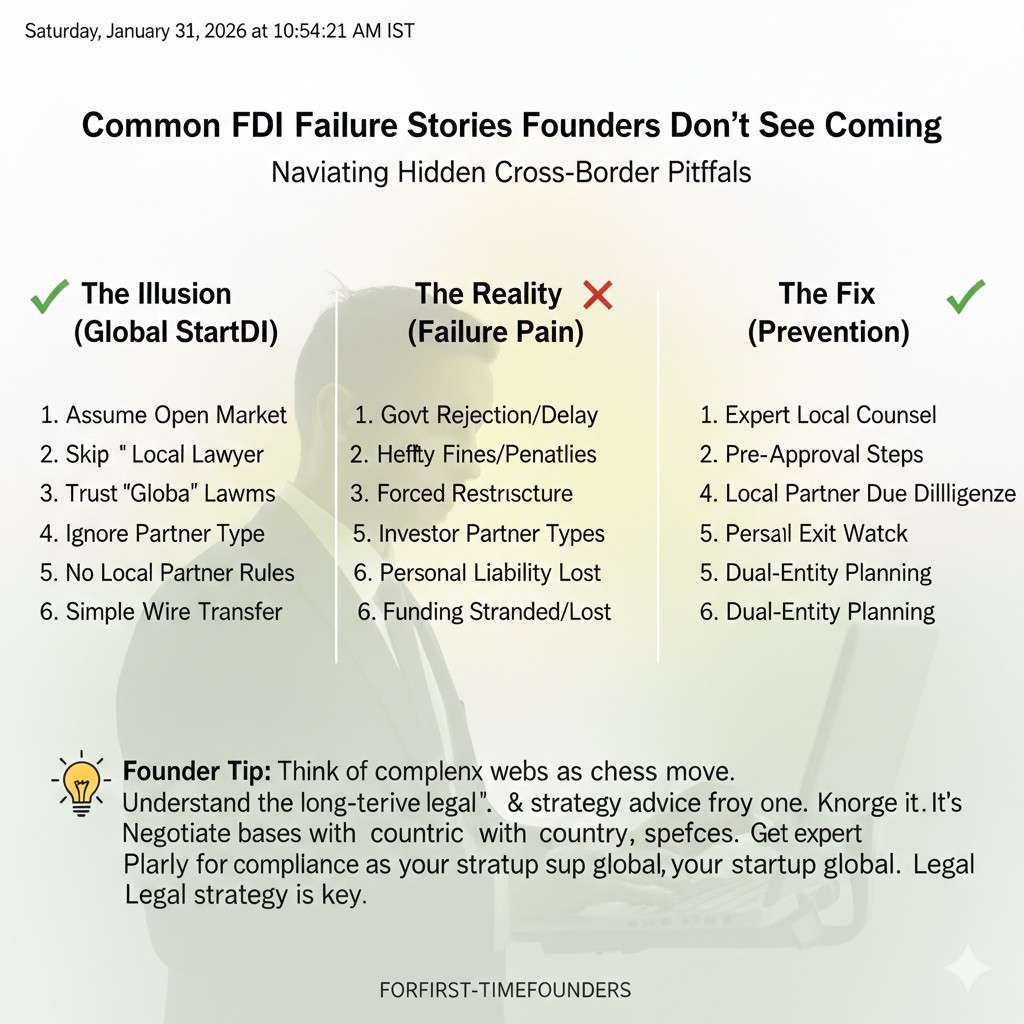

Common FDI Failure Stories Founders Don’t See Coming

The “Friendly Angel” Problem

One of the most common failure stories starts with good intentions. A founder meets an early supporter living overseas. The person likes the idea, wires a small amount quickly, and asks to “figure paperwork later.” It feels harmless because the amount is small and the relationship feels personal.

Months later, when the startup tries to raise a priced round, the lead investor asks for proof that the earlier foreign money followed FDI rules. There is no clear valuation basis, the share issuance happened late, and the reporting was missed. The issue is no longer the old angel. It is now blocking new capital.

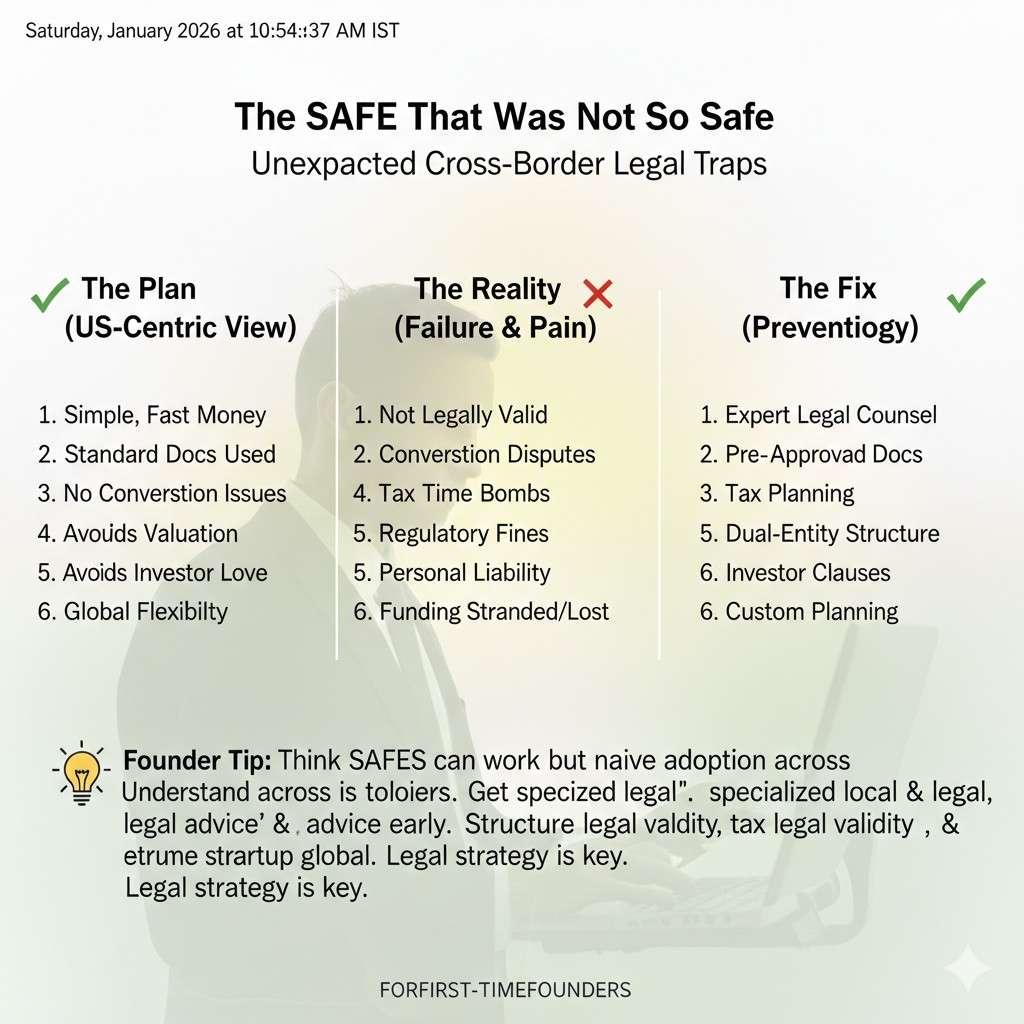

The SAFE That Was Not So Safe

Many founders believe SAFE notes avoid compliance because they are “not equity yet.” In practice, regulators and banks often still treat them as foreign investment instruments. If the SAFE came from a non-resident, the receipt itself may require reporting, even before conversion.

The failure usually shows up during conversion. When the SAFE turns into shares, the pricing and timing are questioned. If the original receipt was not handled properly, fixing it later becomes slow and stressful, especially when investors are waiting.

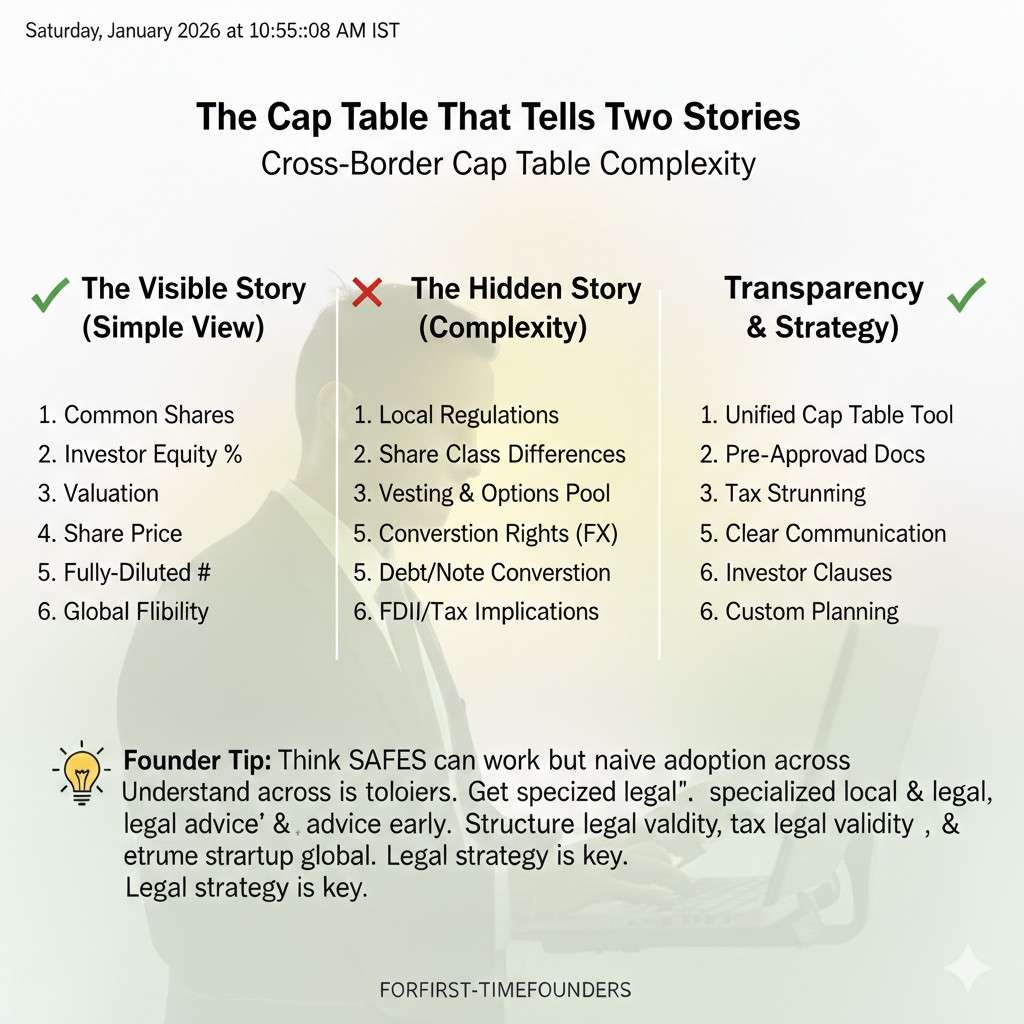

The Cap Table That Tells Two Stories

Another quiet failure comes from inconsistency. The founder’s internal cap table shows one version of ownership. The filings show another. Emails tell a third story. When diligence starts, these gaps create doubt, even if no one intended to break rules.

FDI compliance is as much about consistency as it is about correctness. When documents don’t align, investors assume there is hidden risk. Cleaning this up late often costs more than doing it right early.

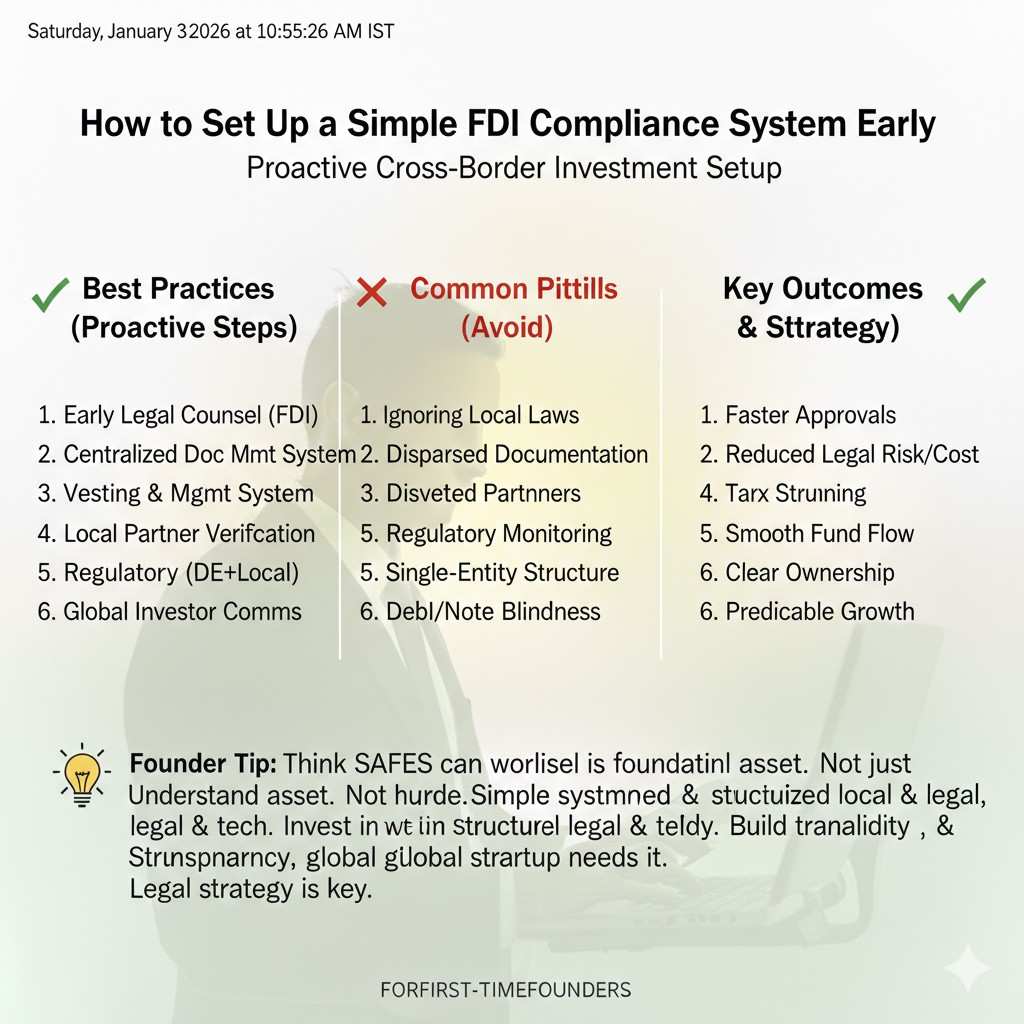

How to Set Up a Simple FDI Compliance System Early

Think of Compliance Like Engineering

Founders understand systems. FDI compliance should be treated the same way. It is not about memorizing laws. It is about building a simple process that runs every time foreign money or ownership is involved.

The system should answer three questions clearly: who is investing, what instrument is used, and what actions must follow. If these answers are written down, mistakes drop sharply.

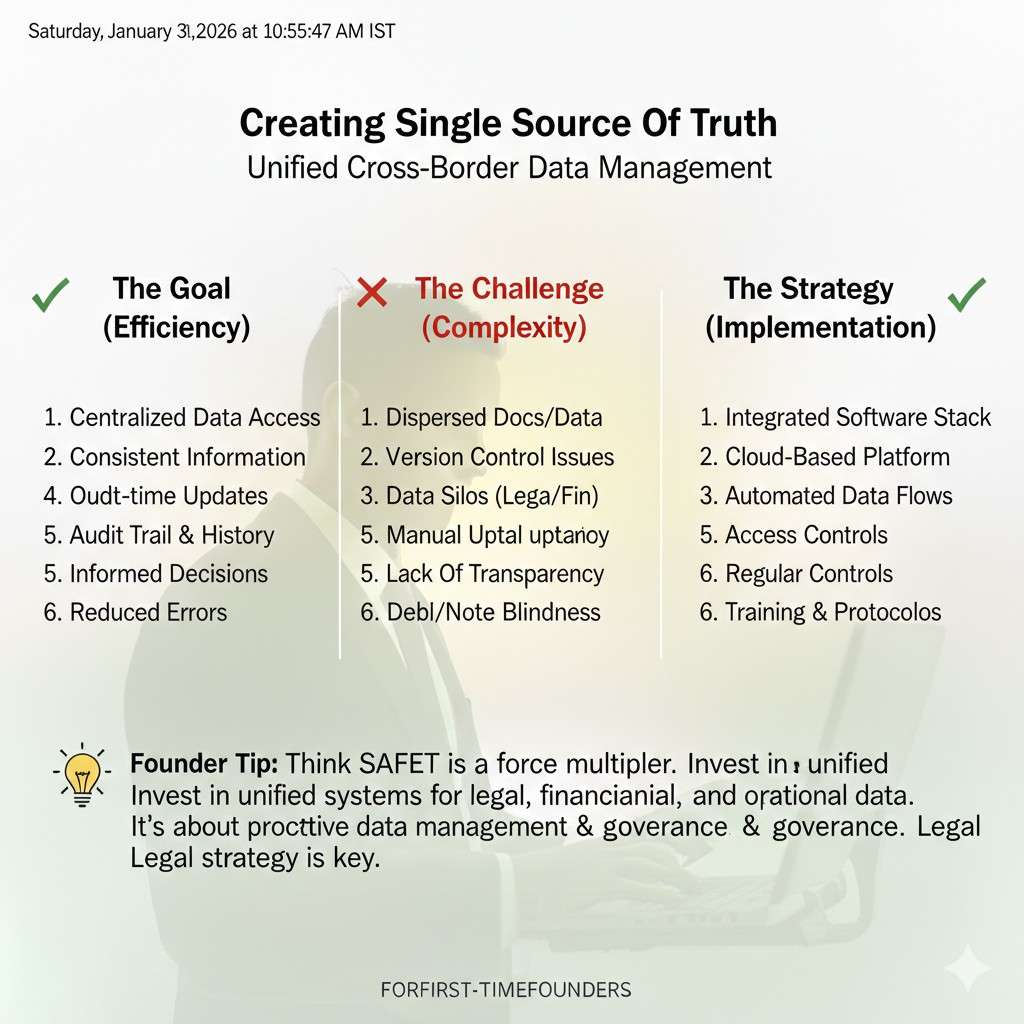

Create a Single Source of Truth

Early on, confusion comes from information being scattered. One document says one thing. Another says something else. The fix is to create a single internal note that explains your setup in plain language.

This note should describe your business, your entities, your shareholders, and any foreign connections. It does not need legal words. It needs accuracy. When questions come up, this note becomes your reference point.

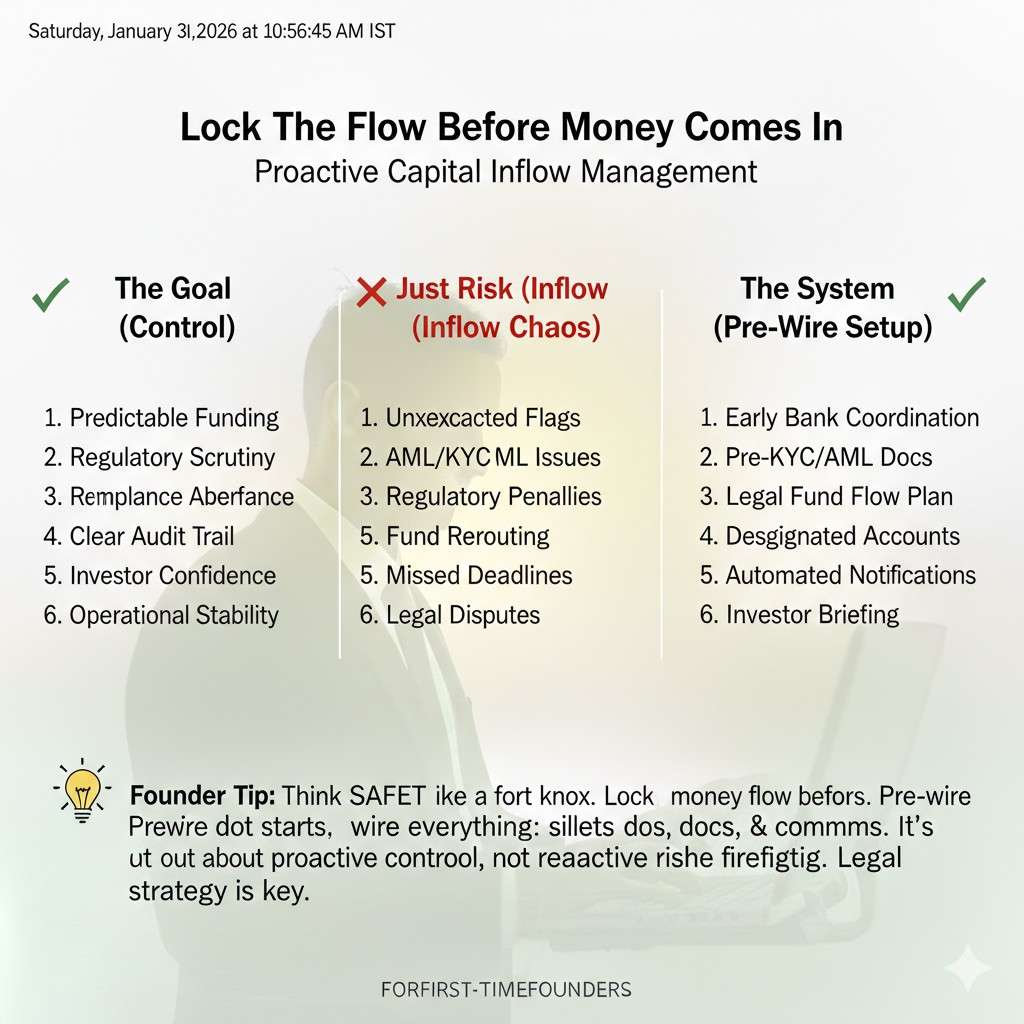

Lock the Flow Before Money Comes In

Many problems happen because founders accept money first and think later. A better approach is to pause for one hour before accepting any foreign funds. In that hour, confirm the instrument, the valuation logic, the approvals needed, and the reporting timeline.

This small pause saves weeks later. It also signals maturity to serious investors, even at an early stage.

Keep Proof, Not Just Files

Compliance is not only about submitting forms. It is about being able to explain decisions later. Why was this price chosen? Why was this person treated as non-resident? Why did money move this way?

Keeping short notes explaining these decisions is extremely powerful. Six months later, when memory fades, these notes protect you.

FDI and IP: Where Founders Get It Wrong Together

IP Is Often the Real Asset Being Funded

In AI and robotics startups, investors are often funding IP creation, not revenue. This means foreign funds are indirectly paying for invention, code, and systems that may later be patented or licensed.

If the IP ownership path is unclear, FDI questions become more serious. Regulators and investors both want to know which entity truly owns what is being built.

Cross-Border Teams Create Hidden Risk

When R&D happens in one country and ownership sits in another, founders must be precise. Who employs the engineers? Who assigns inventions? Who pays for patent filings?

If these answers are vague, foreign investment can appear to be misused or misclassified. Clear agreements and clean IP assignment fix this early.

Why Early IP Strategy Supports Compliance

Strong IP strategy forces clarity. You must define inventors, owners, and jurisdictions. This clarity helps not only with patents but also with FDI explanations during audits and diligence.

Tran.vc focuses heavily on this early alignment. By helping founders build IP correctly from day one, many downstream compliance risks reduce naturally. If this approach fits your startup, you can apply anytime here: https://www.tran.vc/apply-now-form/