If you are building a startup, you will hear the word “valuation” a lot. People will throw it around like it is one clear number. It is not.

In the real world, founders deal with at least two kinds of valuation conversations:

One is the 409A valuation. This is the one most founders first meet when they start granting equity to employees in the U.S.

The other is what I’ll call local valuations. This could mean many things depending on where you are and what you are doing: a valuation for local tax filings, a valuation needed for local compliance, a valuation used for share transfers, a valuation required by a bank, or even a number an advisor says you “should” use because “that’s how it’s done here.”

And then there is the third thing, the one founders care about most, even if they do not say it out loud: the number that shows up in a priced fundraising round. That is the headline number people put in decks and on LinkedIn. It is also the number that can change the tone of your next 18 months.

Here is the hard truth: these numbers are not trying to do the same job. When founders mix them up, they get trapped in avoidable problems. They set option prices too high, upset early hires, create tax risk, or waste months cleaning up paperwork right when they should be shipping product and signing customers.

So this article is about one question: what actually matters.

Not in theory. Not what a blog says. What matters when you are hiring, granting equity, raising money, and building an IP moat that makes your company harder to copy.

At Tran.vc, we work with technical founders in AI, robotics, and deep tech. Many of you are building something real, something that can be patented, defended, and turned into a strong asset. In those companies, valuation talk gets confusing fast because value is not only revenue. It is also the strength of your invention, your data edge, your design choices, and your ability to keep competitors from cloning your work.

That is where smart IP work changes the game. A strong patent plan does not only protect you. It can also support your story when you are priced, and it can remove doubt when investors ask, “What stops a bigger team from doing this too?”

If you want help building that kind of foundation early, you can apply anytime here: https://www.tran.vc/apply-now-form/

Now, before we go deeper, let’s set the tone.

This is not a legal guide. Your lawyers and tax advisors will still matter. But it is a practical guide for founders who want to make good choices, avoid ugly surprises, and keep control while building something that lasts.

In the next section, we’ll break down what a 409A is in plain language, why it exists, when you need it, and what it does not mean. Then we’ll talk about “local valuations” and why they often create confusion. After that, we’ll get into what matters most: how to keep your equity plan clean, how to price options fairly, how to avoid accidental tax problems, and how to protect your long-term fundraising story.

Also, one quick point that will save you stress: a 409A is not your startup’s “real value.” It is a compliance tool. It influences the strike price of options. It is not a trophy. It is not a fundraising number. And it is not a signal that you “made it.”

If you remember only one thing from this introduction, remember this: different valuations are built for different reasons, so you should not treat them like the same thing.

409A vs Local Valuations: What Actually Matters

What most founders get wrong at the start

Valuation sounds like one clean number. But in a startup, it is usually a set of numbers made for different jobs. Each number is created for a reason, by a certain method, for a certain audience. If you treat them as the same thing, you can make choices that feel small today but become painful later.

The big mistake is using one valuation to “prove” something it was never designed to prove. A 409A can be used to set option prices, but it should not be used as your fundraising headline. A local valuation can satisfy a local rule, but it should not be used to price equity for U.S. employees. A priced round valuation can make you look strong, but it may not keep you compliant if you ignore tax and equity basics.

If you want to build fast without creating hidden risk, you need to learn the purpose of each type of valuation. That is how you keep your company clean, fair, and ready for investors.

The simple rule that will guide the whole article

Think of valuations like tools in a toolbox. A hammer is great for nails, but it is not for screws. A screwdriver is great for screws, but it will not help you cut wood. If you use the wrong tool, you can still “get something done,” but it will look messy and break sooner.

A 409A is a tool for option pricing and U.S. tax safety. A local valuation is a tool for local compliance and local tax rules. A fundraising valuation is a tool for setting the price investors pay and the ownership they get. Each tool matters, but in different ways.

If you are building a deep tech company, there is one more tool that quietly shapes value over time: your IP foundation. Strong patents and smart filing strategy can change how your risk looks, how defendable you seem, and how confident investors feel when you say your tech is not easy to copy.

If you want help building that IP foundation early, you can apply anytime at: https://www.tran.vc/apply-now-form/

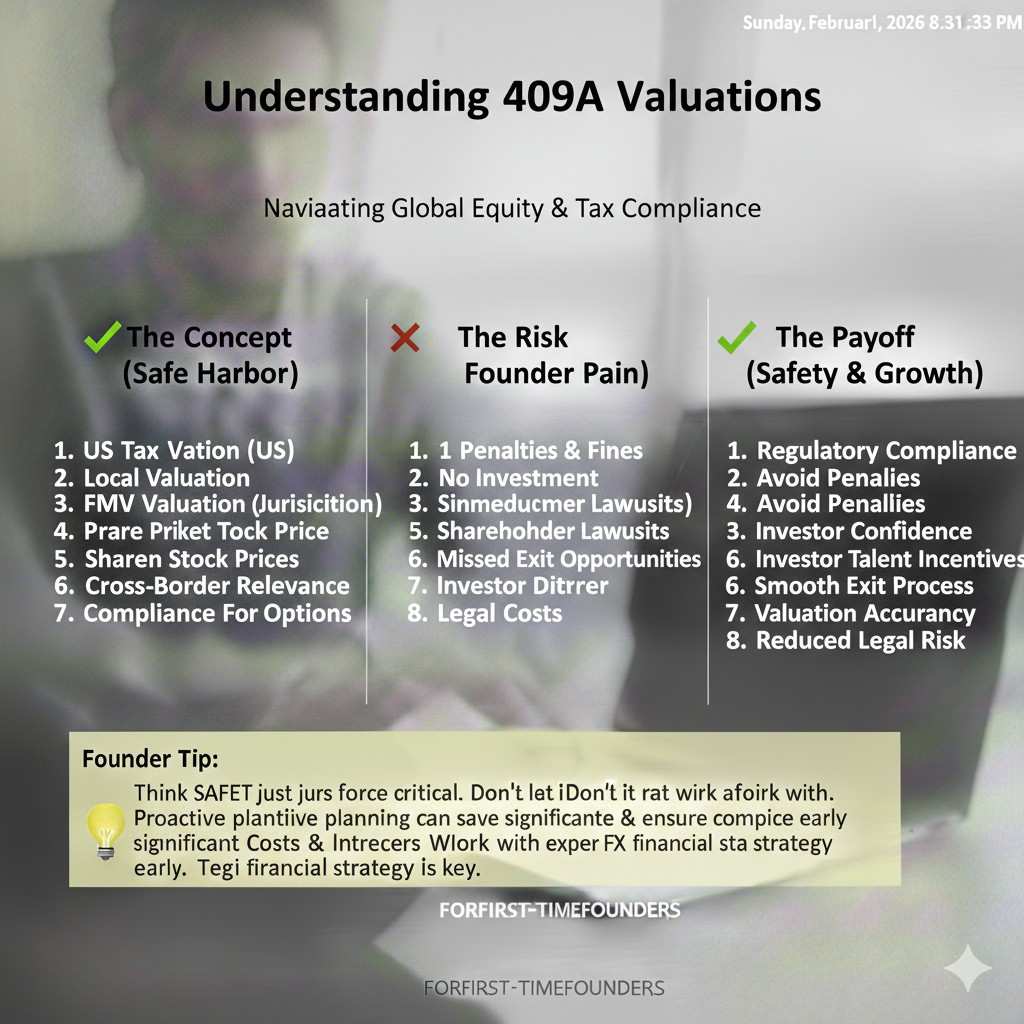

Understanding 409A valuations

What a 409A valuation is, in plain words

A 409A valuation is an independent estimate of what your company’s common stock is worth today. It exists because the U.S. tax system does not want companies giving employees stock options at a fake low price. If options are granted too cheaply, the IRS can treat that as hidden pay, which can create tax penalties for the employee.

So the 409A process is meant to create a reasonable, documented price for common stock. That price becomes the “strike price” for the options you grant. In simple terms, it is the price your team must pay later to buy the shares if they exercise their options.

This is why founders should care: the 409A affects how attractive your options feel to your team. If the strike price is high, options feel less valuable. If the strike price is low and still defensible, options feel better and your hiring story gets easier.

What a 409A is not

A 409A is not your fundraising value. It is also not the same as what an investor would pay for preferred stock in a priced round. Preferred stock often has rights that common stock does not. Things like liquidation preference, anti-dilution, and other protections can make preferred more valuable than common.

Because of that, the 409A common stock price is usually lower than the per-share price in a priced round. That gap is normal, and it does not mean you are doing something wrong. It means the system is separating two different things: the value of common shares for employee options, and the value of preferred shares for investors with extra rights.

If someone brags that their 409A is “close to the round price,” that is not automatically a win. It can be a sign they do not understand what the 409A is trying to do. In many cases, a too-high 409A makes hiring harder, not easier.

When you need a 409A and when it becomes urgent

You usually need a 409A when you are about to grant stock options to employees, advisors, or contractors, and you want to do it the right way. Many early founders wait until they make their first hire or until they are about to issue a real option grant. That is often fine, as long as you are not handing out options casually without proper pricing support.

It becomes urgent when you are growing the team, giving out equity as a key part of pay, or when you are approaching a financing event. Financing events can change value quickly, and your 409A should reflect the company’s situation in a reasonable way.

Founders often learn this too late. They hire fast, promise equity, and then realize they need a 409A to formalize grants. If the company has progressed a lot since the promises, the strike price can rise, which can create awkward conversations with early hires.

What drives the number in a 409A

The 409A value is shaped by facts about your company. Things like stage, revenue, customers, growth rate, funding terms, and risk. It can also be influenced by market conditions and comparable company data, depending on the method used.

Another big driver is whether you have done a priced round, and what those terms were. A priced round provides a clear signal of what investors paid for preferred stock. The valuation provider will usually start from that and then adjust to estimate common stock value.

If you have not done a priced round, the provider relies more on financial models, comparable companies, and risk factors. This is where clean documentation matters. If your numbers are sloppy, your story is inconsistent, or your cap table is messy, you may get a higher number than needed simply because the risk looks unclear.

Deep tech adds another layer. If your core work is defendable and clearly owned by the company, risk can look lower. If your core work is not protected and can be copied, risk can look higher. That is one reason why early IP strategy is not just legal work. It can shape how credible your value story looks.

Tran.vc focuses on helping founders lock in that defensible layer early through in-kind patent and IP support. If that is relevant to you, you can apply anytime at: https://www.tran.vc/apply-now-form/

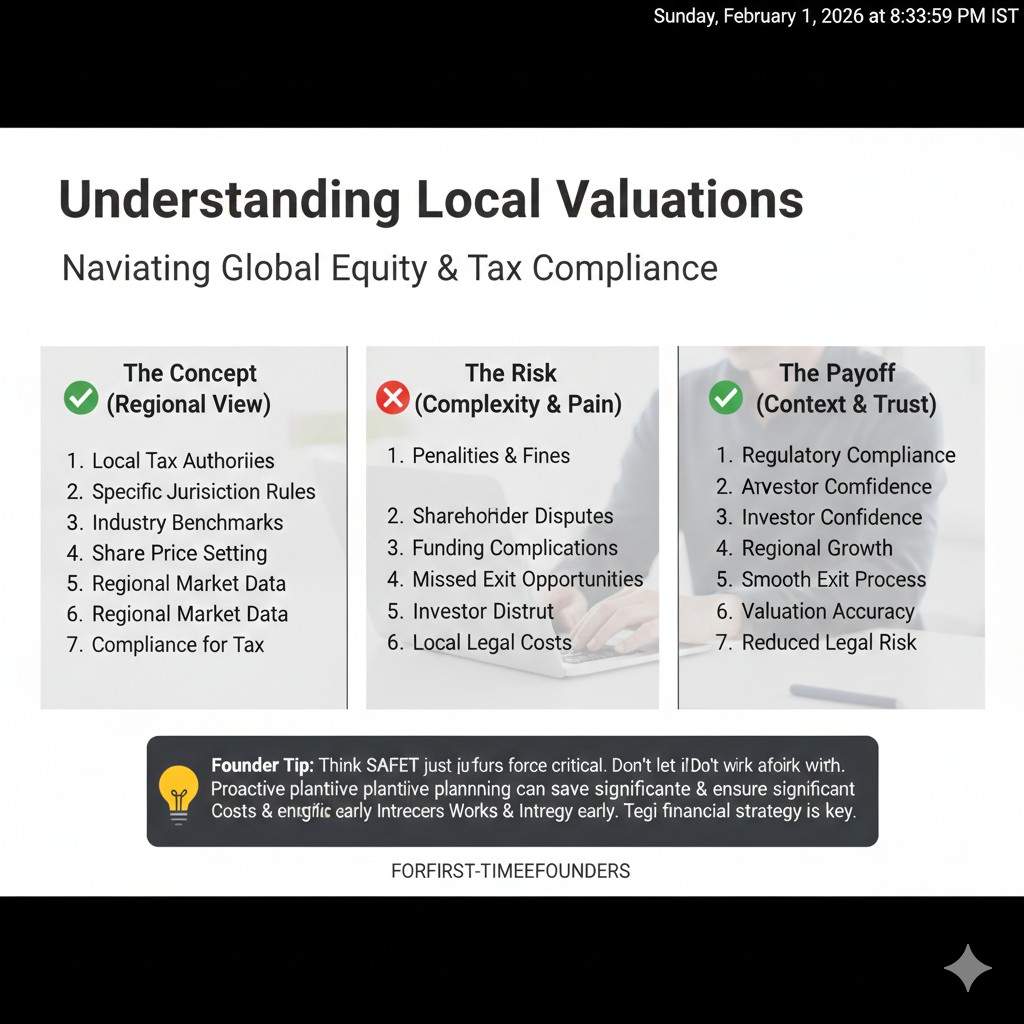

Understanding local valuations

What “local valuation” often means in real life

When founders say “local valuation,” they might be talking about a formal report required in their country. Or they might mean a value used for tax purposes, for filings, or for internal share transfers. In some places, local rules ask for a valuation if shares are issued, transferred, or if equity is granted under an employee plan.

The key issue is that local systems can define “fair value” in ways that do not match U.S. rules. The methods can be different, the assumptions can be different, and the goal can be different. Some local approaches aim to prevent tax avoidance. Some aim to protect minority shareholders. Some aim to set a value for stamp duty or capital gains tax.

So when a founder asks, “Can we just use our local valuation instead of a 409A?” the honest answer is that they are not interchangeable. You can sometimes reuse inputs and business facts, but the report and the standard are often not the same.

Why local valuations create confusion for global teams

Startups today are global early. A Delaware C-Corp can have founders in India, engineers in Eastern Europe, and customers in the U.S. or Europe. That makes the equity plan more complex, because each country may treat equity, options, and share pricing differently.

The confusion happens when the company tries to use one value everywhere. It sounds efficient, but it can create two kinds of problems. First, you might not satisfy the legal or tax rules in one place. Second, you might accidentally create an unfair outcome for your team, where employees in one country get meaningfully worse option economics than employees elsewhere.

A smart approach is to accept that you may need more than one valuation standard, while still keeping one consistent story about the business. That means your internal narrative is aligned, even if the compliance documents differ.

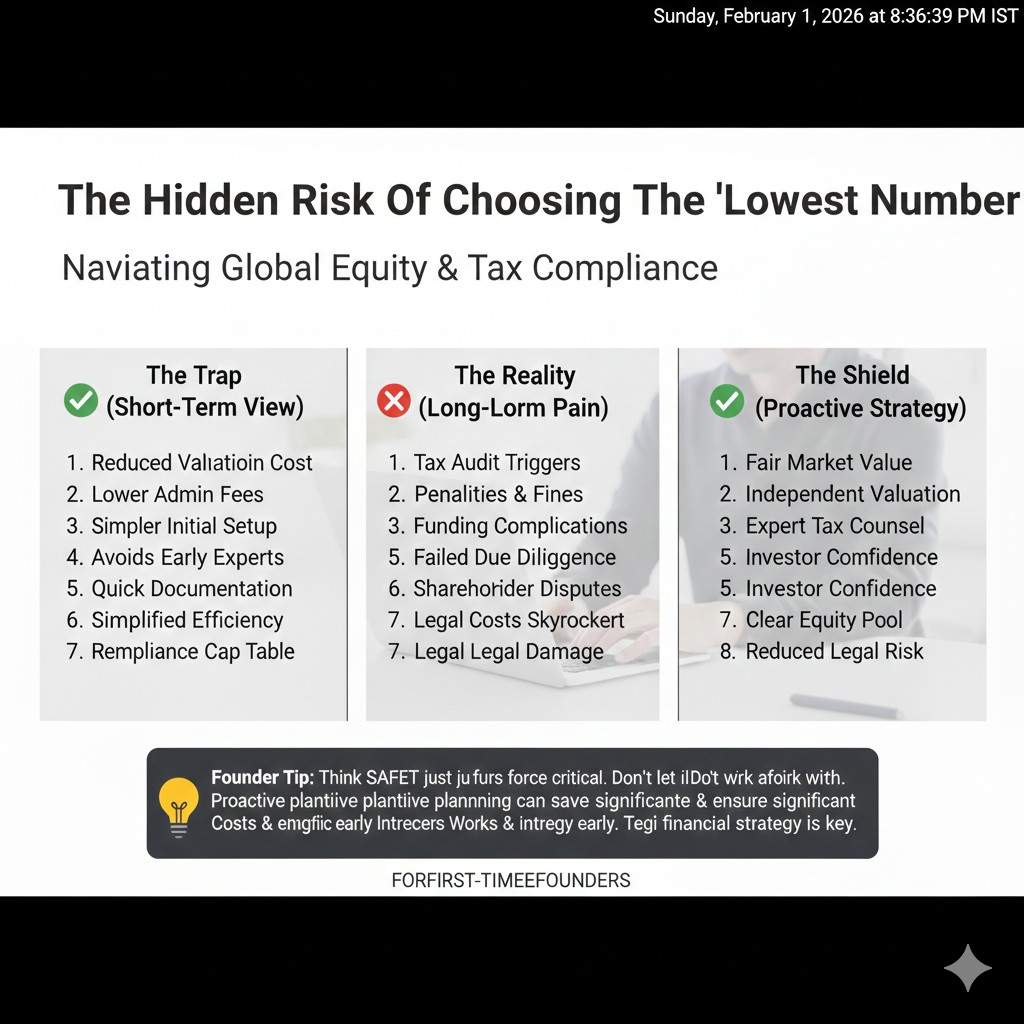

The hidden risk of choosing the “lowest number”

Some founders chase the lowest valuation because they want the lowest strike price. This is understandable, but it can backfire if the number is not defensible. If a local valuation is very low and it does not match how your company is behaving, it can attract questions later.

The risk is not only audits. It is also investor diligence. When investors review your equity history, they look for red flags. A pattern of undervalued equity grants can create uncomfortable discussions during a priced round. In the worst cases, it can lead to costly cleanup work, and it can slow down a deal.

The better goal is not “lowest possible.” The better goal is “reasonable and supported.” That keeps your team happy and keeps your company safe.

The real distinction that matters

Different valuations answer different questions

A 409A tries to answer: “What is the fair value of common stock for option pricing today, under U.S. tax rules?”

A local valuation often tries to answer: “What value should we use for a local tax or compliance purpose, under local rules?”

A fundraising valuation tries to answer: “What price will investors pay for preferred stock, and how much of the company will they own?”

These questions look similar, but they are not the same. Each one uses different assumptions, different rights, and sometimes a different definition of what “value” even means. That is why founders get into trouble when they mix them up.

The rights attached to the shares change the story

Common stock and preferred stock are not equal in most startups. Preferred usually comes with protections. Those protections matter most when things go wrong, like a down round, a sale at a low price, or a shutdown. Because investors have extra protections, preferred can be worth more than common.

A 409A is focused on common. A priced round is focused on preferred. A local valuation could be focused on either, depending on what it is required for. This is not a small detail. It is a core reason why numbers do not match, and why they should not be forced to match.

What investors actually care about when they see these numbers

Investors do not invest because your 409A is high. They invest because the company can become big, and because the risk feels manageable. They want to see that your equity is clean, your option grants are properly priced, and you are not building hidden compliance debt.

They also care about your moat. In AI and robotics, a lot of the “value” is future value. It is your ability to keep a lead when others chase you. A strong IP plan can help here, not as a vanity move, but as proof that your key inventions are real, owned, and defendable.

That is a core part of what Tran.vc supports with up to $50,000 in-kind patenting and IP services. If you are building technical work that can be protected, you can apply here: https://www.tran.vc/apply-now-form/

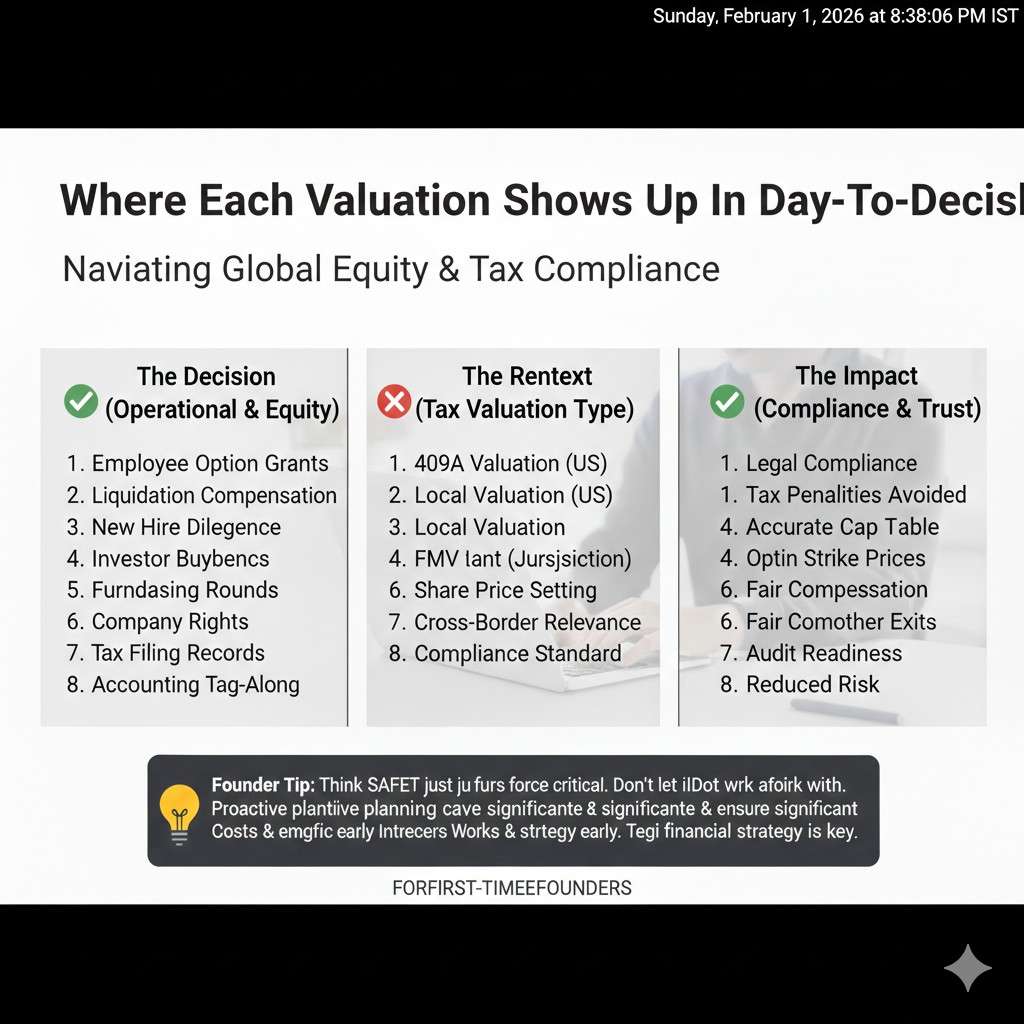

Where each valuation shows up in day-to-day decisions

Hiring and the story you tell candidates

When a strong engineer is deciding whether to join you, they are doing simple math in their head. They want to know if the upside is real, and if the equity offer is fair. They may not say it directly, but they are asking two quiet questions: “What price will I have to pay to get the shares?” and “Is there enough room for the shares to grow?”

This is where 409A matters in a very practical way. The 409A sets the strike price for option grants. If your 409A price is too high, your options feel expensive. Even if the company is promising, the offer can feel less exciting because the candidate sees less upside after they pay the strike price later.

Local valuations can affect hiring too, but in a different way. In some countries, equity is taxed or treated differently, and local valuation numbers may influence what your team owes in tax or what disclosures are required. If you ignore local rules, you can create a surprise tax bill for an employee. That kind of surprise hurts trust, and trust is your most scarce resource early on.

The action here is not complicated. You want option offers that are clean, well priced, and easy to explain. You also want a short equity explainer that you can share with candidates so they do not have to guess. Clear equity is a hiring advantage, especially in deep tech where candidates often have other choices.

Equity grants, backdating, and why timing matters

Many founders do not realize how sensitive equity timing can be. If you promise equity to someone today but only grant it months later, and your 409A price has increased, you can create a gap between what the person expected and what they receive. Sometimes that gap is small. Sometimes it is big enough to cause tension.

In the U.S., using a 409A price that does not match the grant date can create tax problems. This is where “backdating” becomes a dangerous word. Even if your intent is not bad, sloppy processes can look bad later. During diligence, investors look at grant dates, board approvals, and strike prices. They want to see that equity was handled like a real company, not like a casual side project.

Local valuations can have similar timing issues. If a local rule expects valuation at the time of issuance or transfer, using an old number can be risky. The details differ by country, but the pattern is the same. Timing matters because value changes as you execute.

If you want a simple operating habit, make it this: do not let equity promises sit ungranted. Treat equity like payroll. It should be handled on time, documented, and approved in the right way.

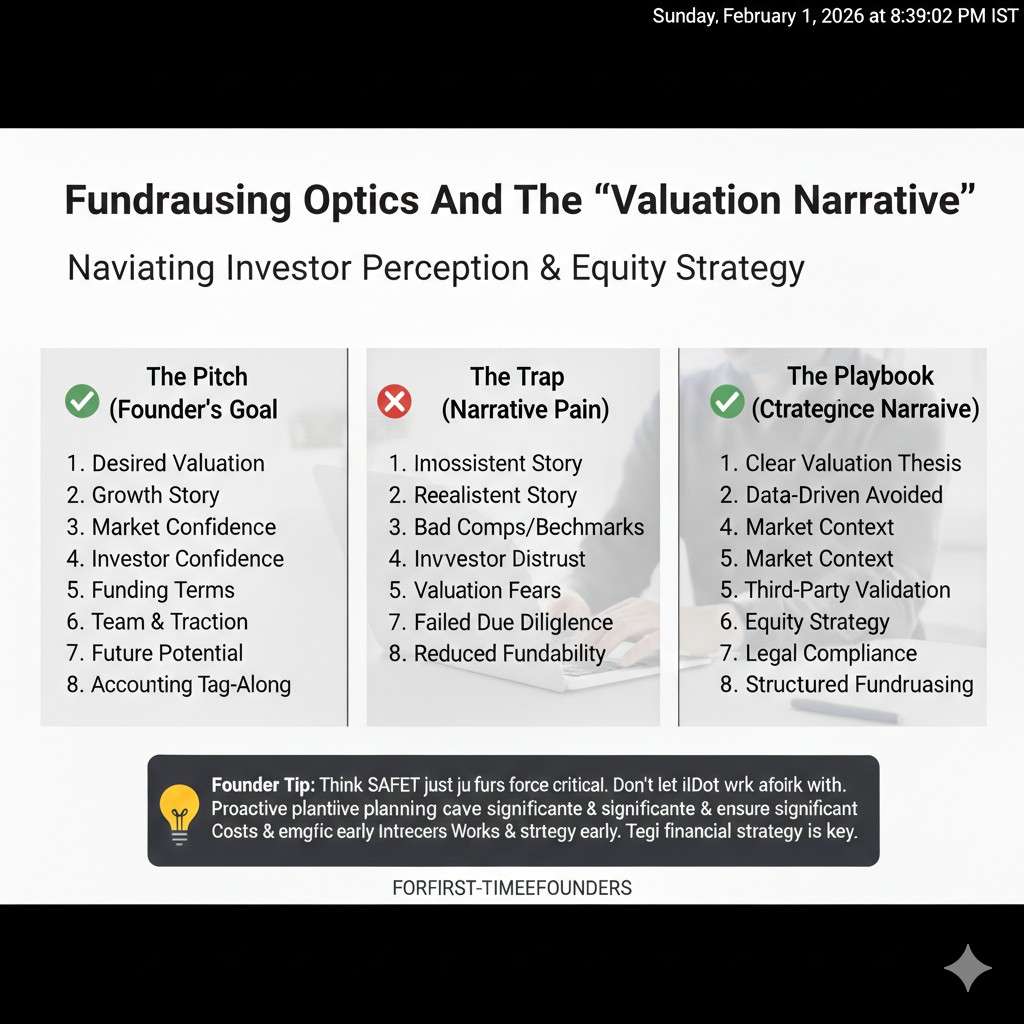

Fundraising optics and the “valuation narrative”

When you raise a priced round, you create a headline valuation. That number becomes part of your story whether you like it or not. It affects how future investors view you. It affects how acquirers think about you. It can also affect employee expectations, because people often confuse the round valuation with what their options are worth right now.

This is where founders get trapped by vanity numbers. A high priced round valuation can feel great in the moment, but it can raise your 409A later, which can make new hires harder. It can also set you up for a down round if growth does not match the story.

Local valuations can complicate this, especially if your company has global entities. If your local valuation is far from your U.S. fundraising story, you need a clean explanation. Not a clever one, a clean one. The explanation should be grounded in the purpose of the valuation and the rights attached to the shares, not in excuses.

The best fundraising optics come from consistency. You want your documents, your cap table, your equity grants, and your IP ownership to all support one coherent story: the company is building real tech, owns it, and is growing in a way that makes the future believable.

What “matters” depends on your goal

If your goal is to avoid tax and legal pain

If your goal is to avoid tax and legal issues, then the 409A matters because it supports safe option pricing in the U.S. A defensible 409A is like insurance. It reduces the chance that employees face penalties because options were priced incorrectly. It also reduces the chance that you have to do expensive cleanup later.

Local valuations matter for the same reason, but within their own systems. If you have employees, founders, or share activity in a country that expects a local valuation or a local process, you should treat it seriously. Early-stage companies often try to postpone these steps, but postponing compliance can turn into a bigger and more expensive problem later.

This is not about being “formal.” It is about removing fragility. A startup has enough risk already. You do not need extra risk from avoidable paperwork mistakes.

If your goal is to recruit and keep great people

If your goal is to recruit strong people, what matters is that your equity offers feel fair and understandable. Most candidates do not want a lecture. They want clarity. They want to know what they get, what it costs, and what needs to happen for it to become valuable.

The 409A matters here because it shapes the strike price. But the deeper point is process. If you grant options quickly, price them correctly, and communicate simply, candidates feel safer joining. If you delay grants, change terms, or cannot explain the numbers, you create doubt.

Local valuations matter because taxes and local rules affect what equity feels like in practice. A grant that looks great in a U.S. template can feel risky in a country where taxation is harsher or where option plans are less common. If you want global talent, you must respect local reality.

If your goal is to raise a strong priced round

If your goal is to raise money, what matters most is not the 409A number. It is your traction, your team, your technical edge, and your ability to show that the company can become big. Investors will care that your equity is clean, but they are not investing because your 409A is high or low.

They do care about how your option pool is managed. They do care about whether you have created hidden liabilities. They do care about whether your cap table is simple enough to understand and your documents can survive diligence without drama.

And in deep tech, they care a lot about whether you have something others cannot copy. That is where patents and IP strategy can be a quiet multiplier. It is not about filing patents to look impressive. It is about showing that your core inventions are owned by the company and are protectable.

Tran.vc is built around this idea. We invest up to $50,000 in-kind through patent and IP services so technical founders can build a strong foundation early, without giving up control too soon. If you want to explore that, you can apply anytime at: https://www.tran.vc/apply-now-form/

The founder’s practical map: how to keep valuations from hurting you

Keep one internal story, even if you have multiple valuation reports

A common problem is that founders treat each valuation event like a separate world. They say one thing in the 409A process, another thing in a local valuation, and another thing in fundraising. This creates inconsistencies. Inconsistencies create questions. Questions create delays.

You can avoid this by keeping one internal narrative document that describes your company in a stable way. It should explain what you are building, what the product does, what the market is, what progress you have made, what your key risks are, and what has changed since the last time.

This does not need to be long. It needs to be accurate. When you work with valuation providers or advisors, you use the same base facts. The reports may still differ, because the purpose differs. But the business truth should not change.

Treat equity like a product feature, not like paperwork

In early-stage companies, equity is a core part of compensation. That means equity is part of your product for talent. If you treat it casually, you ship a broken product to your team.

The tactical move is to set a simple internal cadence. Decide when you will grant options, how quickly after someone starts, and who owns the process. Make sure board approvals and documentation happen on schedule. Make sure strike prices align with the right valuation and the right date.

This is not only for compliance. It also prevents resentment. People notice when equity is sloppy. Even if they do not complain, it changes how much they trust the company.

Make IP ownership clean before you try to prove value

Here is a truth many technical founders overlook. Value is not only what you built. It is also whether the company clearly owns what you built.

If inventions are sitting in personal GitHub repos, if contractors have not assigned rights, or if early research work was done without clear agreements, you can end up with a company that has impressive tech but unclear ownership. That makes investors nervous. It can also affect valuation work because risk looks higher when ownership looks messy.

When you clean IP early, you reduce questions later. You also make your moat story more credible. If your invention is patentable and you have filed thoughtfully, you can point to assets, not just claims.

This is one of the main reasons Tran.vc exists. We help deep tech founders build that IP backbone early through in-kind services, so the company can scale and raise with more leverage. Apply anytime here: https://www.tran.vc/apply-now-form/