Most founders wait too long to think about company structure. They focus on the product, the demo, the launch, and the next hire. That makes sense—until an investor, a customer, or a future acquirer asks a simple question: “Who owns what?”

If your answer is messy, the deal gets slower. If your answer is unclear, the deal gets smaller. And if your answer is risky, the deal can die.

A parent-subsidiary structure is one of the cleanest ways to make that “who owns what” answer simple. Done right, it can protect your core invention, reduce risk, support global sales, and make future funding easier. Done wrong, it can create tax headaches, IP ownership confusion, and investor fear—right when you need speed and trust.

In this guide, I’m going to explain parent-subsidiary setups in plain words, with the exact angles investors care about. Not theory. Not legal jargon. Real founder decisions: where the IP should live, how to keep liability away from your core assets, what to do if you have a services arm, how to handle a second product line, and how global investors view US vs non-US structures.

And because Tran.vc works with robotics, AI, and deep tech founders, we’ll focus on the things that matter most in those worlds: patents, trade secrets, and how to build a real moat early—before the first big check arrives.

If you want Tran.vc to help you build an investor-friendly structure and protect what you’re building with patents (up to $50,000 in in-kind IP and patent services), you can apply any time here: https://www.tran.vc/apply-now-form/

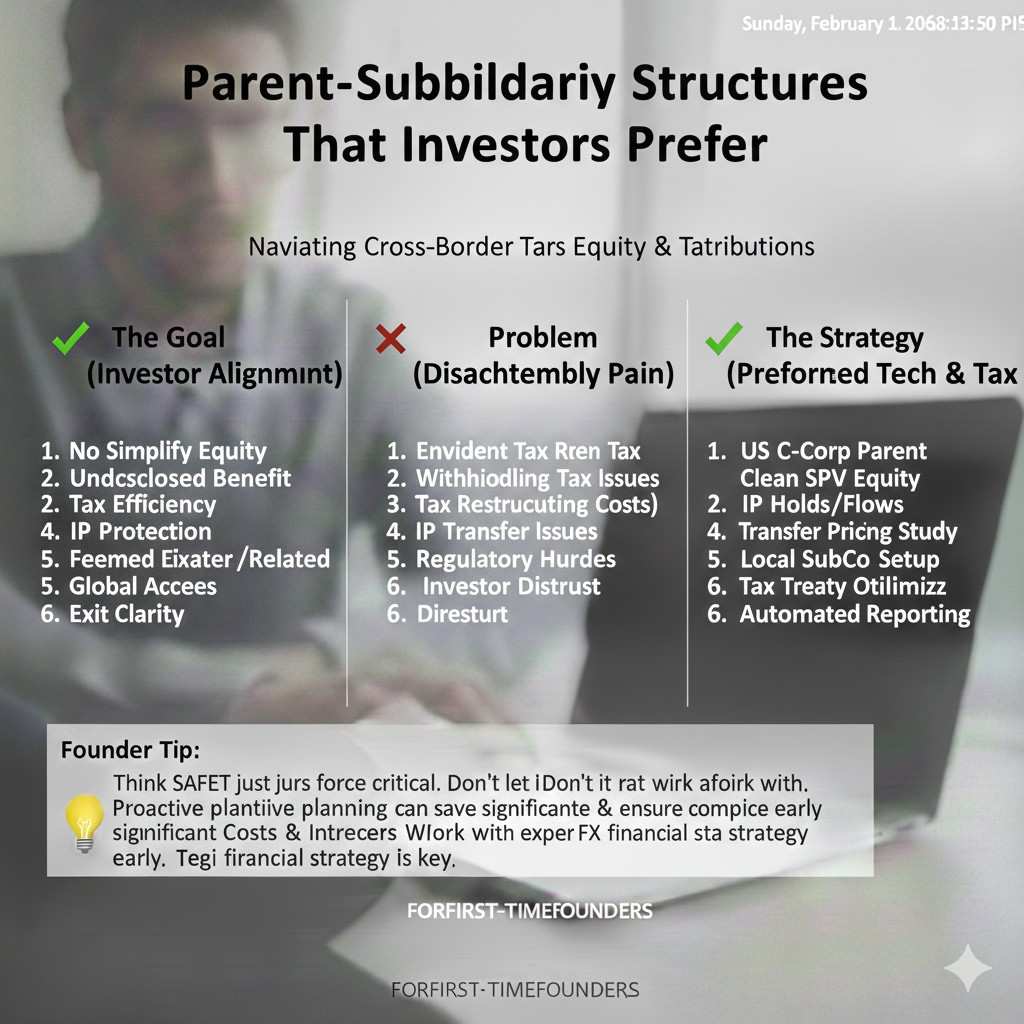

Parent-Subsidiary Structures That Investors Prefer

Why investors care so much about structure

Investors do not just invest in a product. They invest in an ownership story. They want to know what the company owns, how clean that ownership is, and what could break it later. A strong structure makes that story easy to believe and easy to defend.

When structure is weak, investors picture hidden problems. They worry about lawsuits hitting the wrong entity, tax issues showing up after the round, or a co-founder dispute pulling IP into a fight. Even if none of that happens, the fear alone can slow a deal down.

A clean parent-subsidiary setup is one of the simplest ways to lower that fear. It gives investors clear lines: where the valuable assets sit, where the risk sits, and how money flows. It also shows you think like a builder, not just a coder.

If you want help setting this up in a way that feels “fundable” to seed investors, you can apply to Tran.vc any time here: https://www.tran.vc/apply-now-form/

The simple idea behind a parent and a subsidiary

Think of the parent company as the main holder. It is the entity investors fund. It owns the important things, like shares, key contracts, and usually the core IP. It sets the rules for the group.

A subsidiary is a company the parent owns. The subsidiary can run a specific part of the business. It can hold risk, hire people in a certain country, sell to a certain customer type, or run a side activity that you do not want mixed into the parent.

This is not about making things complex. It is about keeping things separated so you can grow without dragging risk into everything else. Investors like separation when it is used with purpose and when it stays easy to explain.

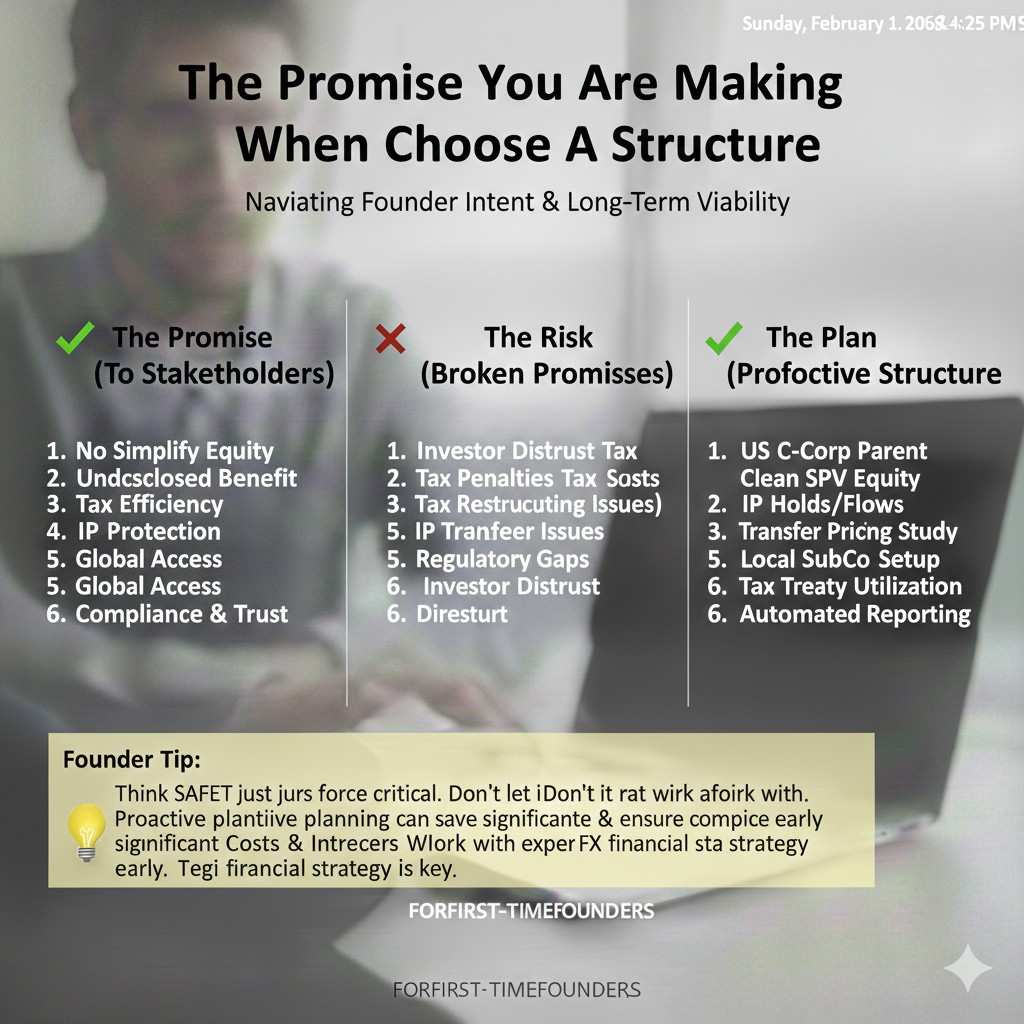

The promise you are making when you choose a structure

A structure is a promise that your company will behave in a predictable way. Investors want that. They want to know that the parent is the “safe place” where value builds over time, and that problems in one area do not poison the whole company.

They also want to know that if your startup wins, the parent captures the win. That means the parent owns the assets that create leverage. It also means the parent has control over subsidiaries so the group can act as one unit when needed.

If you set this promise up early, later rounds become simpler. You spend less time rewriting history. You spend more time showing progress.

What investors prefer at seed stage

The investor view: one simple cap table, one clear owner

At seed, most investors want simplicity first. They want a single company they can invest in, with a clean cap table. They want to see clear founder ownership, clear option pools, and no strange side agreements.

If you already have multiple entities, that is not always bad. But it raises questions. Investors start asking why you did it, what sits where, and whether the structure was made for business reasons or for personal reasons.

When your setup feels like it was built to “hide” something, trust drops. When it feels like it was built to protect the business and support growth, trust rises.

The common setup that feels “normal” to most investors

The setup investors see most often is one parent entity that raises money, with subsidiaries used only when there is a clear need. This might happen when you expand into a new country, when you take on regulated work, or when you run a services arm.

This is not because investors love complexity. It is because they have seen too many companies get hurt by mixing everything together. They prefer simple structures, but they also prefer smart risk control.

If you can explain your structure in thirty seconds without sounding defensive, you are usually on the right track.

When a parent-subsidiary structure is a green flag, not a red flag

A structure becomes a green flag when it solves a real problem. If you are entering Europe and need local hiring and payroll, a local subsidiary makes sense. If you are doing hardware testing that could create product liability risk, a separate subsidiary can make sense.

The key is that the parent remains the center of gravity. The parent should be where investors feel safe. The subsidiaries are tools, not competing power centers.

This is also where IP matters. If the IP is scattered or owned by the “wrong” entity, investors get nervous fast.

The IP question: where investors want the crown jewels

Why IP placement is the first serious diligence topic

In robotics, AI, and deep tech, the IP is often more valuable than the first product. Investors know that. They also know that early-stage teams can accidentally lose IP through simple mistakes.

If your patents, code rights, and invention assignments are not clean, investors worry that someone else can claim your work later. They also worry that a lawsuit or a breakup could pull the IP out of the company.

That is why many investors start diligence by asking who owns the IP today. Not who created it. Not who paid for it. Who owns it.

Tran.vc helps founders build strong IP foundations early, including patent strategy and filings as in-kind support up to $50,000. If that would help you, apply here: https://www.tran.vc/apply-now-form/

The most investor-friendly IP setup in plain words

Most investors prefer the parent company to own the core IP. That includes patents filed, patents planned, key code, models, and trade secrets. When the parent owns the IP, the value sits in the same place where investor money sits.

Then the operating company, if different, licenses the IP from the parent under a simple agreement. That license can be exclusive, and it can be designed to match your business needs.

This approach gives investors comfort. Even if an operating unit gets sued, or even if you need to sell part of the business later, the IP stays protected at the top.

The mistake that scares investors: IP owned by the wrong entity

A common mistake is filing patents or signing invention work under a subsidiary, a founder’s personal name, or a contractor’s company. It can happen by accident. It can also happen because a founder thinks it is “fine for now.”

Investors do not see it as fine. They see it as future pain. They know that moving IP later can create taxes, legal steps, and delay. They also know that if one document is missing, the whole chain becomes questionable.

The safest path is to keep IP ownership simple from day one. The earlier you clean it up, the cheaper and easier it is.

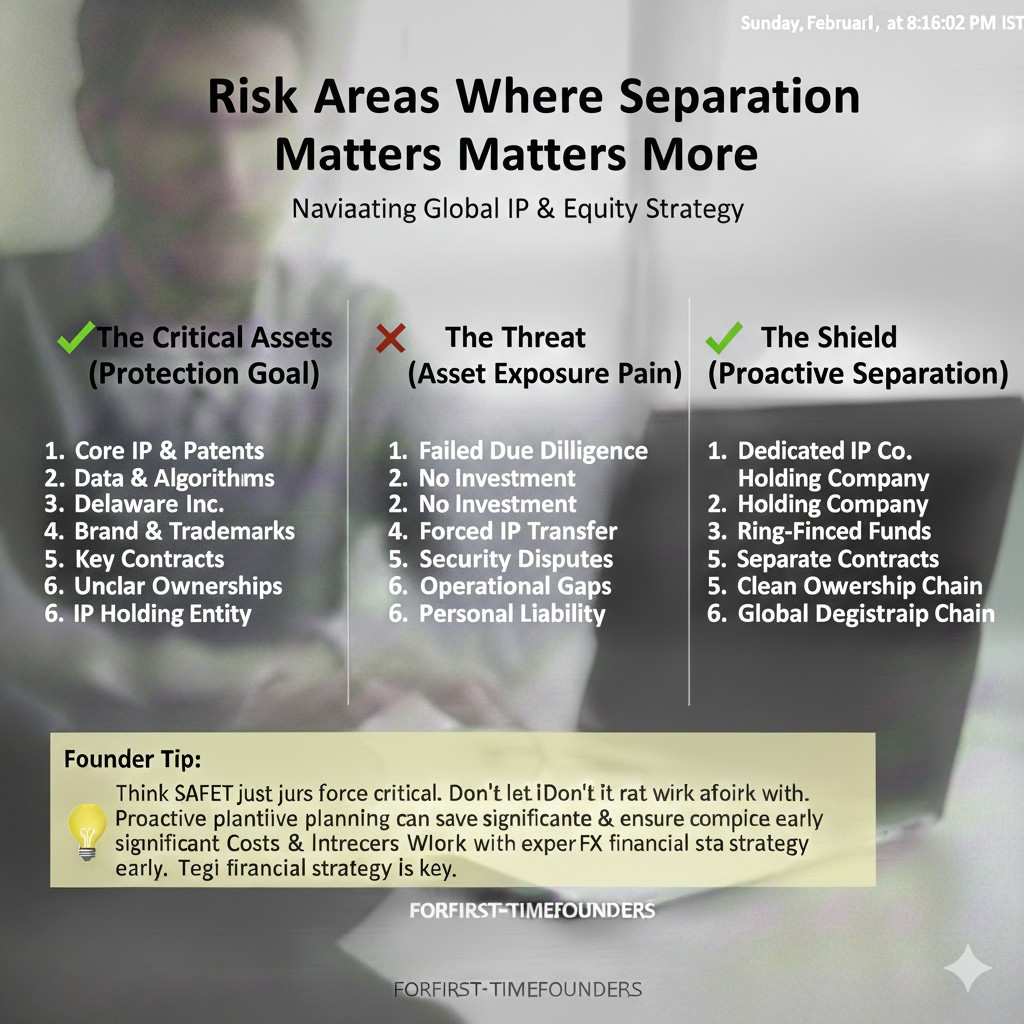

Liability: why investors like risk to live away from the parent

The idea investors keep in their head

Investors want the parent to be the “vault.” They want the valuable assets to sit there. They also want risk-heavy activity to happen somewhere else when possible.

This is because lawsuits and debts do not care about your pitch deck. If your operating activity creates risk, that risk should not sit in the same entity that holds the assets.

A subsidiary can act like a buffer. It is not a magic shield, and it must be managed properly, but it is a real tool when used correctly.

Risk areas where separation matters more

Hardware testing, field deployments, and anything involving physical work tends to carry higher liability risk. Robotics companies often touch real environments, real people, and real property. That changes the risk profile compared to pure software.

Certain customer contracts also add risk. If you sign large indemnities, service-level penalties, or strict delivery terms, you can create financial risk that investors would rather not place in the parent entity.

When investors see that you understand these risks, they relax. They feel you can scale without stepping on landmines.

What “clean separation” actually means

Separation is not just filing paperwork. Investors look for real separation in behavior. That includes separate bank accounts, clean intercompany agreements, and clear roles for each entity.

If money flows randomly and decisions are mixed, the separation starts to look fake. In a worst case, a court can treat the entities as one. Investors know this, so they look for signs that you respect the structure.

This is one reason to keep subsidiaries limited. Too many entities too early increases the chance you will run them loosely.

The most common investor-loved patterns

The “one parent, one operating subsidiary” pattern

This is a common and simple model. The parent is the company investors buy into. The operating subsidiary runs day-to-day operations, signs customer contracts, hires staff, and carries operational risk.

In this setup, the parent often owns the IP and licenses it to the operating subsidiary. The operating subsidiary pays a small royalty or fee, or the agreement can be structured in a way that fits your stage.

Investors like this because it is easy to explain. It also makes future moves easier, like selling a business unit or spinning out a product line without breaking the whole company.

The “parent with country subsidiaries” pattern

If you hire or sell in multiple countries, investors often expect local subsidiaries. Payroll, taxes, and employment laws can be hard to manage from one entity across borders.

A country subsidiary can hold local employment contracts and handle local compliance. It also reduces the chance that one country’s legal issue spreads into the entire group.

Investors prefer when country subsidiaries are created only when needed. They do not want a “world map” of entities that have no staff and no real activity.

The “services subsidiary” pattern for deep tech founders

Many deep tech startups do some services work early. Sometimes it is pilot work. Sometimes it is custom integration. Sometimes it is consulting that funds the team while product matures.

Investors can be cautious here because services can pull focus and create messy obligations. A services subsidiary can help separate that work from the product company.

It can also protect the parent from contract risk and payment disputes. The key is making sure services work does not quietly swallow your IP or your team’s time in a way that hurts the product story.

How to decide if you need this now or later

A simple way to sense the right timing

If you are pre-seed with no revenue and one product direction, you often do not need multiple entities right away. Investors usually prefer you keep it simple until there is a clear reason to split.

But if you have high liability activities, complex customer terms, global hiring needs, or multiple product lines that could diverge, then it can make sense earlier.

The right answer depends on your business, not on what other founders are doing. Investors respect founder judgment when it is clear and well explained.

The cost of building structure too early

Structure has upkeep. Every entity needs accounting, tax filings, and compliance work. Even if you are careful, it creates more decisions and more paperwork.

If you build a multi-entity setup too soon, you can burn time and money that should go into product and customers. Investors do not want that either.

They want “right-sized” structure. Enough to protect value. Not so much that it slows you down.

The cost of waiting too long

Waiting too long can also create pain. If you sign contracts under the wrong entity, or file IP under a founder name, fixing it later can be harder.

It can also slow fundraising. Diligence becomes a cleanup project. Some investors will still proceed, but they may reduce valuation, change terms, or require fixes before closing.

A good approach is to set up the parent cleanly early, keep IP ownership clear, and add subsidiaries only when a real trigger appears.

If you want Tran.vc to guide that setup and build your patent plan early as part of up to $50,000 in in-kind IP services, apply here: https://www.tran.vc/apply-now-form/

Parent-Subsidiary Structures That Investors Prefer

Defining each entity’s job so investors feel calm

Investors get uneasy when a structure exists but has no clear reason. They do not want to see a parent, two subsidiaries, and a holding company if nobody can explain what each one does. The best way to avoid that is to give each entity a simple job and keep that job stable over time.

The parent is usually the story investors buy into. It holds the key assets, controls the group, and is the place where long-term value builds. It should not feel like a shell with nothing inside. Even if operations happen elsewhere, the parent must still own the important rights and set the rules.

The operating subsidiary is usually the “hands.” It signs day-to-day customer contracts, pays the team, and runs projects. If something goes wrong in the field, the operating company is the one exposed first. This is not about hiding risk. It is about keeping risk from touching the assets that should remain protected.

A services subsidiary, if you have one, has a different job. It exists to take on short-term work that brings cash but also carries contract risk and time risk. Investors like when that work is kept in a box. It makes it easier to prove your product company is not just a consulting shop.

If you want Tran.vc to help you map these roles in a way that makes investors nod instead of worry, you can apply any time here: https://www.tran.vc/apply-now-form/

The “rule of one sentence” for every entity

A practical test is this: you should be able to describe each entity in one sentence. Not a long explanation. Not a history lesson. One clean sentence that says what it does and why it exists.

If you cannot do that, the structure is either too complex or not thought through. Investors will keep asking questions until they understand it, and that costs time. Time kills deals, especially at seed where investors move fast and compare many companies at once.

When your structure passes the one-sentence test, investors usually relax. They may still ask for documents, but the tone changes. It becomes routine diligence, not “we found a problem.”

Avoiding the hidden fight: control and decision power

Sometimes founders create subsidiaries and accidentally split control in confusing ways. A parent that owns only 60% of a key subsidiary can raise alarms. So can a subsidiary where a co-founder is a direct owner outside the parent.

Investors want the parent to have clear control. That does not always mean 100% ownership in every case, but it does mean there should be a strong reason if it is less. If a subsidiary is critical to the product, investors prefer it to be wholly owned by the parent.

This matters because funding rounds and exits depend on control. If control is fragmented, every future step becomes a negotiation with extra parties. That is not a risk most seed investors want.

How IP should move between parent and subsidiaries

What investors want to see in real documents

It is easy to say “the parent owns the IP.” Investors want proof. That proof comes from clean paperwork: invention assignment agreements from every founder and employee, contractor agreements that clearly assign work to the right entity, and records of patent filings that match the ownership story.

If your operating team sits in a subsidiary but the parent owns the IP, investors will also want to see the IP license agreement. It does not need to be fancy. It needs to be clear.

The agreement should state what is licensed, who can use it, and what happens if the relationship changes. Investors like when the license is exclusive for the operating company, because it reduces confusion about who can sell what.

The difference between owning IP and using IP

This distinction matters more than most founders think. Owning IP means you control it. You can stop others from using it. You can sell it. You can license it. You can use it as leverage in deals.

Using IP is different. A subsidiary that only uses IP is dependent on the license. That is fine when the parent controls the subsidiary, because the group moves together. But it becomes risky when control is unclear or when there are outside owners in the subsidiary.

Investors prefer when “ownership” stays at the top and “use” happens where operations happen. This model supports protection and flexibility. It also helps in exits, because you can sell a business unit without accidentally giving away the entire technology base.