Side letters feel harmless.

A quick extra promise. A short email. A one-page note that says, “Sure, we can do that,” so a check comes in faster.

But later, when you raise a bigger round, that “small” promise can turn into a deal-breaker. It can scare off the next investor, slow down legal review, or force you to renegotiate when you have the least power.

This article is about how side letters hurt later rounds, why they show up in the first place, and how to avoid them without losing the investor. If you want to build real leverage early, protect what you build, and raise on your terms, Tran.vc can help you do that with strong IP work from day one. You can apply anytime here: https://www.tran.vc/apply-now-form/

Avoiding Side Letters That Hurt Later Rounds

The quiet paper that can cause loud problems

A side letter is a separate note that sits next to your main investment papers.

It usually gives one investor something extra that the others do not get.

It might feel normal because it is short, fast, and often framed as “just a small ask.”

The problem is not the paper length.

The problem is the long tail.

A side letter can follow your company into every future round.

When later investors review your deal history, they look for surprises.

Side letters are often the biggest surprise.

Even if the promise was made with good intent, it can look unfair or risky later.

If your goal is to raise cleanly and move fast, you want simple terms.

You want fewer special cases and fewer “extra promises.”

That is how you keep control when the stakes get bigger.

Tran.vc works with technical founders early, before these traps get baked in.

Strong IP planning and clean early paperwork give you leverage later.

You can apply anytime here: https://www.tran.vc/apply-now-form/

Why side letters show up in the first place

Most founders do not wake up wanting complicated legal baggage.

Side letters happen because the founder is trying to close the round.

A small concession can feel like the price of speed.

Some investors also ask because they want comfort.

They may have been burned before.

Or they may be used to getting “extras” in every deal.

A side letter can also appear when the main documents feel rigid.

Instead of changing the core terms for everyone, people try to patch the deal.

That patch later becomes a weak spot.

The most common driver is time pressure.

If payroll is close and runway is short, founders sign things quickly.

Later, when you have traction, you realize you gave away power too early.

Side letters versus standard rights

Not every extra document is evil.

Some side letters are harmless, like small admin items.

The risk comes when the side letter changes control, money flow, or access.

Standard investor rights usually live in one place.

They are seen by everyone in the round.

They are designed to be consistent across investors.

A side letter, by design, breaks consistency.

It creates one-off rules.

That makes later legal review slower and more nervous.

The real test is simple.

If a future lead investor reads it, will they say, “This is fine,” or “Why is this here?”

If you cannot answer that in one clean sentence, it is a red flag.

The real damage side letters cause in later rounds

How future investors read your past deals

In a later round, the new lead investor becomes your main buyer.

They are buying preferred stock, but they are also buying your story.

They want proof that the company is well run and fair.

During diligence, their counsel reads everything.

They look for hidden obligations, special rights, and unequal treatment.

They also look for anything that could create a future fight.

Side letters often trigger more questions than they are worth.

Questions lead to delays.

Delays can lead to a weaker price or a lost deal.

Even if the side letter is not “enforced,” it still exists.

Lawyers cannot ignore paper.

If it is signed, it is part of the company’s risk profile.

The fairness problem that makes everyone uneasy

Later investors care deeply about equal treatment.

Not because they want to be nice, but because unfairness creates chaos.

Chaos kills companies, and investors do not fund chaos.

If one investor has a special right, others may demand it too.

If they do not get it, they may feel second-class.

That can show up in board votes and consent rights later.

Founders also get trapped in a fairness squeeze.

You either keep honoring special deals forever, or you renegotiate.

Renegotiating costs time, legal fees, and goodwill.

A clean cap table is not just about who owns what.

It is also about who can demand what.

Side letters clutter that second part in a way most founders miss early.

The hidden veto that can stop a round

Some side letters quietly create a veto.

Not always a direct “no,” but a practical “no.”

For example, they can require consent before new financing.

If the investor is slow, hard to reach, or upset, you are stuck.

You cannot close the round until they sign.

That is a lot of power to hand over for a small check.

Even worse, this power often was not priced in.

You did not get a higher valuation for it.

You just gave it away to get to the finish line.

In later rounds, new investors hate this.

They want certainty that the company can raise again.

If your past paperwork blocks that, they may walk away.

The “most favored nation” trap

One common side letter idea is “most favored nation,” often called MFN.

It says this investor gets any better terms you give anyone else later.

That sounds fair on the surface, but it can poison your flexibility.

In a later round, you may need to offer a key investor a small extra.

Maybe they bring a major customer, or they are leading the round.

With an MFN promise, that small extra spreads to others.

Now your “small extra” becomes expensive.

It can change economics across the round.

It can also create a messy argument about what counts as “better.”

Lawyers then spend hours debating language.

Hours turn into days, and days can turn into a missed funding window.

This is how an MFN clause becomes a silent round-killer.

Tran.vc pushes founders to keep terms clean early.

If you build leverage with real IP and a strong moat, you negotiate from strength.

You can apply anytime here: https://www.tran.vc/apply-now-form/

The side letter terms that cause the most pain

Extra information rights that become a burden

Some investors ask for special reporting.

Monthly calls, custom dashboards, or deep financial detail.

At seed stage, founders often agree because it feels polite.

Later, your company grows, and the reporting burden grows too.

Now you are spending time feeding one investor special updates.

That time comes straight from building product and shipping.

There is also a privacy angle.

Some reports can reveal sensitive plans or customer details.

If that investor has other bets in the same space, risk increases.

Future investors may ask, “Why did you agree to this?”

If they fear leaks or conflicts, they may reduce interest.

What felt like simple transparency can become a serious concern.

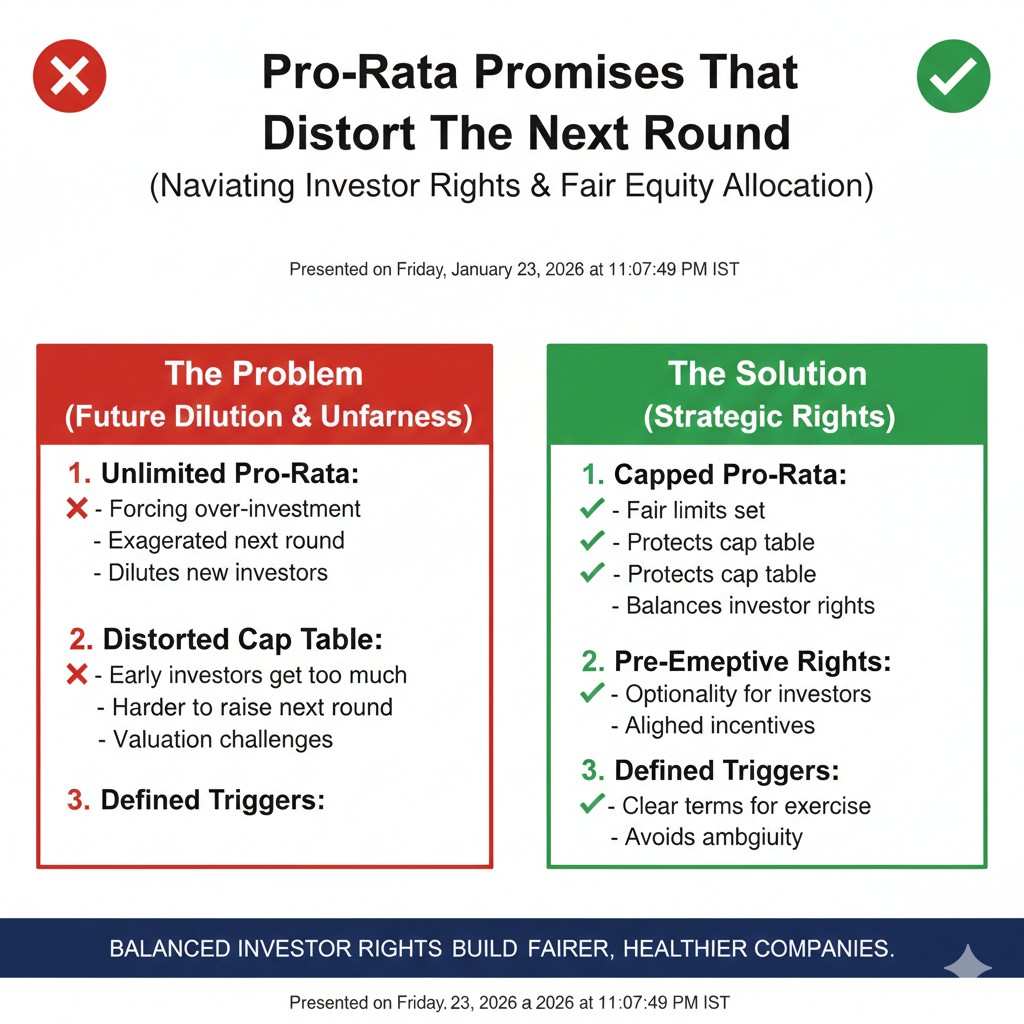

Pro-rata promises that distort the next round

Pro-rata rights are common and often fine when standard.

The problem is when a side letter expands pro-rata beyond normal limits.

That can crowd out new money in the next round.

In later rounds, you want room for a strong new lead.

You may also want room for strategic investors.

If one early investor has an oversized right, the pie gets tight.

When allocation gets tight, someone gets upset.

Sometimes it is the new lead who cannot get enough ownership.

Sometimes it is you, because you cannot bring in the partner you need.

Then the negotiation becomes about squeezing into a cap table.

This is not how you want to spend your funding window.

You want momentum, not a math fight caused by old paper.

Board observer rights that change board dynamics

A board observer sounds harmless.

They do not vote, so what is the issue?

The issue is what happens in the room.

A board meeting is where hard truths come out.

Founders share bad news, risk, and sensitive strategy.

When extra observers sit in, people talk differently.

That can reduce honesty.

It can also increase leak risk if the observer is loosely connected to the investor.

Future leads may ask for stricter governance because of it.

Even if the observer is great, the next investor may still dislike the structure.

They may want a clean board that matches standard norms.

Side letters make governance feel improvised, and that is not comforting.

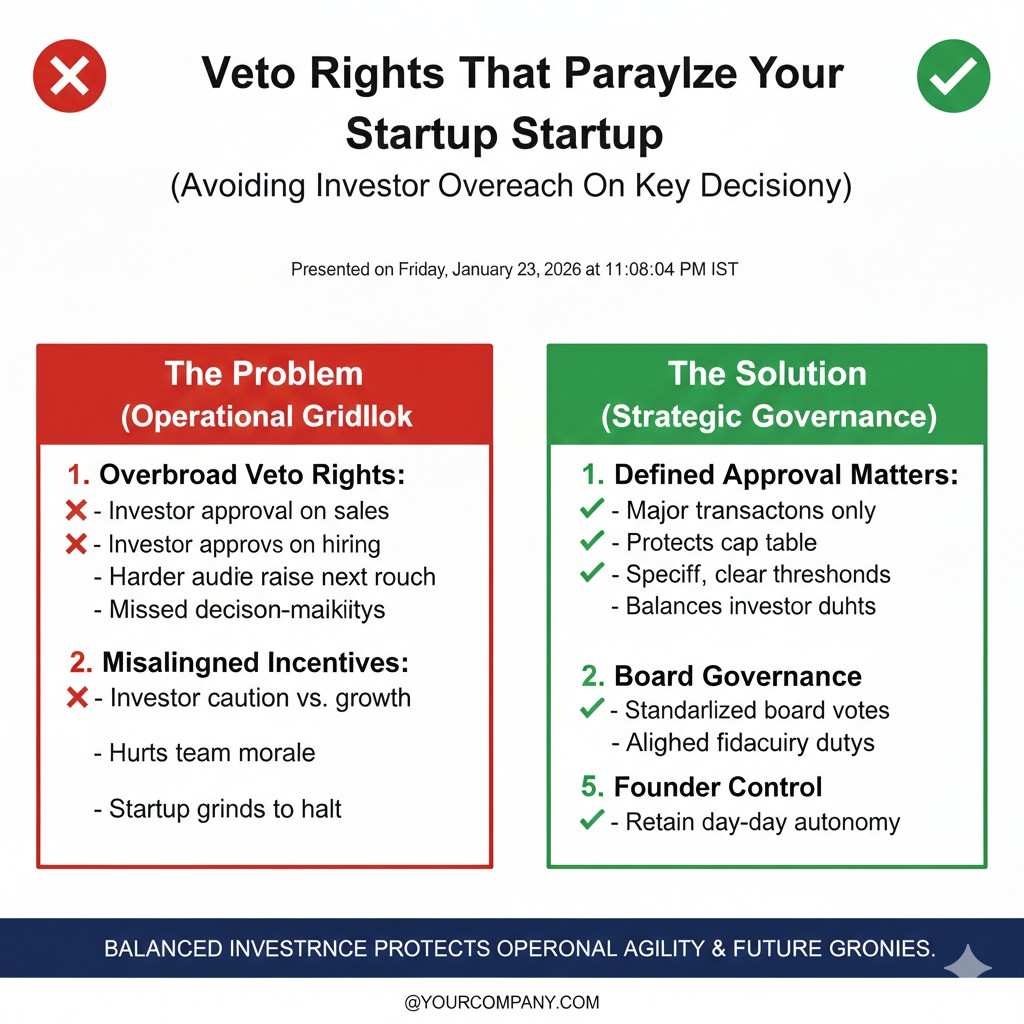

Rights tied to approval on sales, hiring, or budgets

Sometimes a side letter gives an investor “consulting” approval.

They want to approve a budget, a key hire, or a major contract.

Founders accept because it sounds like support.

In practice, it can become control.

If they disagree, you stall.

If they are busy, you stall.

Later investors will not like that.

They want founders to execute fast.

Any outside brake looks like risk.

If you need help and advice, you can build that in the right way.

Advisory relationships can be informal.

Control rights should be rare and priced properly, not slipped in quietly.

How to spot side letter risk before you sign

The “later round lawyer test”

A helpful way to judge a side letter is to imagine the next round.

Picture a top-tier seed or Series A lead and their counsel reading it.

Ask yourself what the first reaction will be.

If the reaction is confusion, you have a problem.

If the reaction is “this is non-standard,” you have a problem.

If the reaction is “why is this investor special,” you have a problem.

This mental test works because it focuses on the buyer you need next.

Your next lead investor is your future gate.

Do not hand them reasons to hesitate.

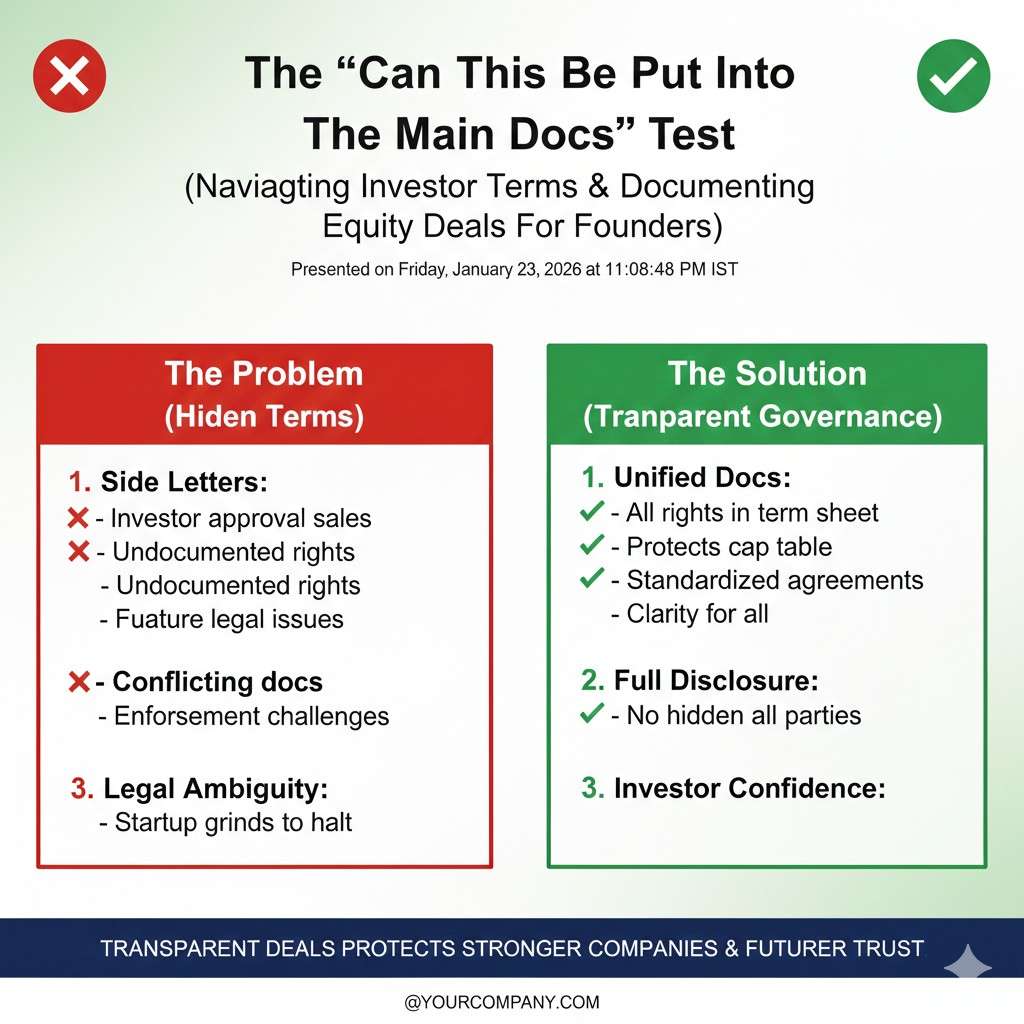

The “can this be put into the main docs” test

If an investor wants a right that is truly reasonable,

it should usually be able to live in the main documents.

That keeps the round fair and clear.

If the investor refuses to put it in the main docs,

ask why it must be hidden in a side letter.

Often, the honest answer is that others would object.

That is your signal.

If other investors would object, future investors may also object.

You are not avoiding conflict; you are delaying it until it is more costly.

The “does this create an ongoing job for the company” test

Some side letter terms create ongoing work.

Extra reporting, extra calls, special approval steps.

That work does not scale well.

Early-stage teams are small.

Every extra process steals focus.

Even if the investor is kind, the company pays the cost.

Later investors can spot this quickly.

They will ask whether your team is distracted.

They may also push you to clean it up before closing, which slows everything.

The “does this change who has leverage later” test

A side letter can look small but shift leverage.

Consent rights, MFN clauses, special redemption ideas.

These can change the balance of power in later negotiations.

When you need speed in a future round,

a single party with special rights can demand concessions.

That is leverage you handed away when you were most vulnerable.

If you want to keep leverage, build it with assets.

For deep tech, real IP is one of the strongest assets you can build early.

Tran.vc helps you do that in a founder-friendly way. Apply anytime: https://www.tran.vc/apply-now-form/

How to say no without losing the investor

Start by naming the shared goal

Many founders avoid “no” because they fear losing the check.

But you can say no in a way that keeps the relationship strong.

The key is to frame it as a shared goal.

You can explain that clean terms help the company raise again.

If the company raises again, everyone wins.

That makes your position reasonable, not stubborn.

You are not rejecting the investor.

You are protecting the company’s ability to grow.

Most serious investors understand that logic, even if they push back.

Offer a clean alternative that does not create special rights

Often, the investor is asking for comfort, not control.

So give comfort without the trap.

For example, you can commit to standard quarterly updates for all.

If they want to help, invite them into a founder update list.

If they want access, offer an intro call when you have a major milestone.

These are relationship gestures, not legal obligations.

The investor gets respect and visibility.

The company keeps clean paper.

That is the balance you want.

Use your lead investor as a shield

If there is a lead in the round, lean on them.

Tell the investor you need to keep terms consistent.

Say the lead wants everyone under the same documents.

This is normal and widely accepted.

It also shifts the discussion away from personal conflict.

You are not “being difficult,” you are following the round structure.

Even if you do not have a formal lead, you can still use the same logic.

You can say you are aiming for a standard structure that future leads will accept.

That is a professional stance.

Slow down the signature when pressure shows up

Pressure is when bad side letters happen.

When an investor says, “Sign this today,” that is your warning light.

Fast signatures often create long-term damage.

You do not need to stall for weeks.

You do need enough time for a careful read and a clear choice.

A calm pause today can save you months of pain later.

If you are raising while building deep tech, you already have complexity.

Do not add legal complexity on top.

If you want help building leverage early, apply here: https://www.tran.vc/apply-now-form/

How to structure early rounds without side letter landmines

Why simplicity is your strongest negotiating tool

Early rounds feel fragile because capital feels scarce.

That makes founders think they need to accept complexity to survive.

In reality, simple structures make you more investable, not less.

When documents are clean, investors move faster.

When terms are clear, trust builds quicker.

Simplicity signals confidence and long-term thinking.

A simple round also reduces legal back-and-forth.

That saves money and time.

Both matter more than most founders realize in the first year.

If you want flexibility later, start clean now.

Complexity almost never shrinks on its own.

It compounds as the company grows.

Using standard documents as protection, not weakness

Standard seed documents exist for a reason.

They reflect what the market accepts.

They are designed to survive later scrutiny.

When you anchor on standard terms, you are not being rigid.

You are signaling that your company plans to grow.

Future investors feel safer stepping in.

Side letters often show up when founders treat standards as optional.

But standards protect you from pressure.

They give you a neutral reason to say no.

You can say, “We’re sticking to market terms.”

That sounds professional, not defensive.

It frames the conversation around norms, not personal preference.

Keeping all key rights visible to everyone

Transparency across investors matters more than founders expect.

When all major rights live in the same documents, trust increases.

No one worries about hidden deals.

Hidden terms create suspicion, even if harmless.

Suspicion slows decisions.

Slow decisions can kill momentum in a fundraise.

Visible terms also reduce internal conflict later.

Board discussions stay focused on the business.

They do not drift into arguments about who was promised what.

A company with clean, visible terms is easier to lead.

It is also easier to sell, partner with, or take public one day.

Designing for the next round, not just this one

Every early round should be designed backward.

Ask what your Series A investor will expect to see.

Then build toward that, not away from it.

They will expect clean governance.

They will expect predictable rights.

They will expect no surprise vetoes.

If something you sign today breaks that picture, pause.

Short-term relief is rarely worth long-term friction.

The best founders think two rounds ahead, even when cash is tight.

When side letters may be acceptable, with care

Administrative details that do not change power

Not all side letters are harmful.

Some cover simple logistics like notice addresses or reporting format.

These do not change economics or control.

The key is that they do not give leverage.

They do not create consent rights.

They do not alter future fundraising ability.

If a side letter only clarifies process,

and that process is easy to undo or ignore later,

it is usually safe.

Even then, keep it short and clear.

Ambiguity is what turns small things into big problems.