Cross-border cap tables can feel like a simple spreadsheet until the day a serious investor looks at it and goes quiet.

Not because your idea is weak. Not because your team is wrong. But because the ownership story is messy, hard to read, and hard to trust.

A “VC-readable” cap table is not about perfection. It is about clarity. It answers basic questions fast:

Who owns what?

What did they pay?

What happens next round?

And can a new investor buy in without stepping on legal landmines?

When founders build in one country and raise in another, those questions get harder. You might have a Delaware C-Corp with a team in India. Or a Singapore HoldCo with a U.S. investor lead. Or an India company that now wants U.S. money, but the cap table still looks like a local angel round from three years ago.

This is common. It is also fixable.

In this article, I’m going to show you how to keep a cross-border cap table clean and “VC-readable” before you are deep in diligence. I’ll explain what investors look for, where founders get trapped, and how to design ownership that works across borders without turning your company into a legal maze.

And if you are a robotics, AI, or deep tech team, there is one more layer: your IP. In cross-border setups, IP often ends up in the wrong place, owned by the wrong entity, or assigned too late. That can kill a round or cut your valuation. Tran.vc helps founders avoid that early by investing up to $50,000 in in-kind patent and IP work, so your cap table and your IP story match from day one. If you want help, you can apply anytime here: https://www.tran.vc/apply-now-form/

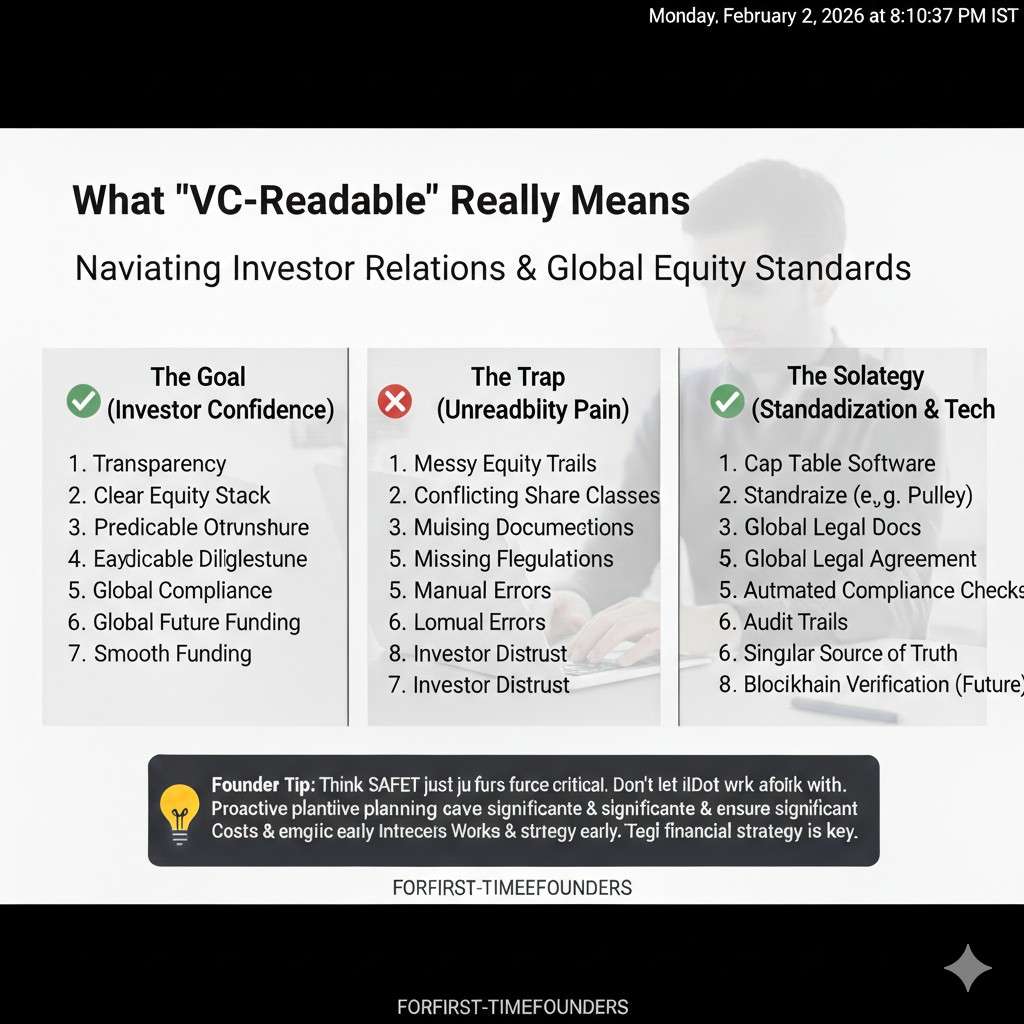

What “VC-Readable” Really Means

The first test is speed

A VC-readable cap table is one that a partner can understand in minutes, not hours. When an investor opens your cap table, they are not trying to admire your formatting. They are trying to see if the ownership story is clean enough to fund.

If they cannot tell who owns the company, how much is already promised away, and what the next round will look like, they will slow down. In a competitive round, slowing down often means losing momentum.

Cross-border companies get judged even faster. Investors assume there may be extra risk, extra paperwork, and extra surprises. A clear cap table is your first signal that you run the company with discipline.

Clarity matters more than creativity

Founders sometimes try to “solve” cross-border complexity with clever structures. The problem is that clever looks like hidden. Hidden looks like risk. Risk looks like “not now.”

VC-readable means simple enough that the structure can be explained without a long call. It also means the paper trail matches what the cap table says. If the spreadsheet says one thing and the legal docs say another, investors believe the docs, not the spreadsheet.

The cap table must match the legal truth

Many early cap tables are built by copy-pasting a template and then patching it every time something changes. That works in a single-country setup for a while. In cross-border setups, it breaks quickly.

VC-readable means every number has a document behind it. It means every share class has a clear reason to exist. It means every option grant is properly approved. If any of those pieces are missing, the cap table becomes a story with missing pages.

Why this is harder across borders

Cross-border ownership brings extra moving parts. Different countries treat shares, options, and taxes differently. Some countries make it hard to issue equity to non-residents. Some countries require special filings for cross-border transfers.

Investors do not expect you to be an expert in every country. But they do expect you to have a structure that can survive diligence without major surgery.

If you want to keep your structure VC-readable early, Tran.vc can help you design it with IP in mind too. Deep tech rounds often fail when IP ownership and cap table ownership do not line up. You can apply anytime here: https://www.tran.vc/apply-now-form/

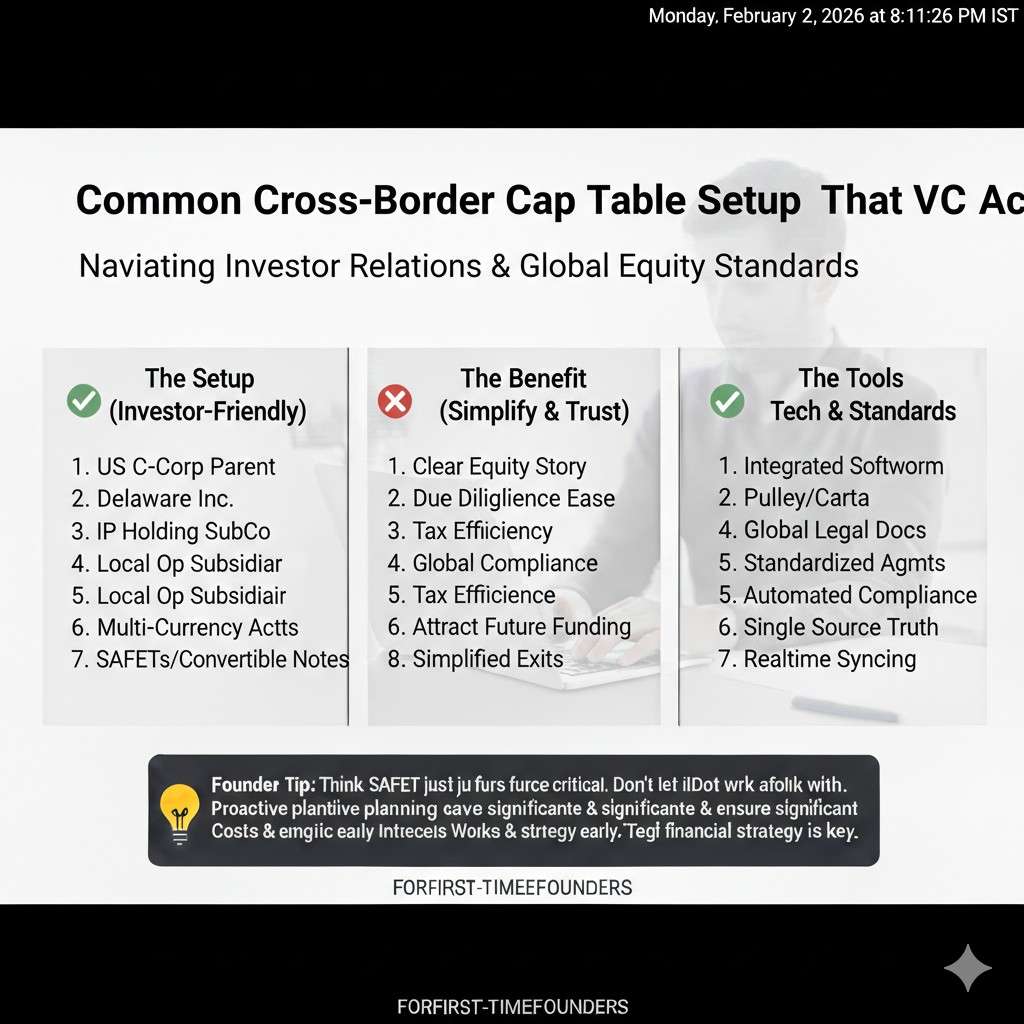

Common Cross-Border Cap Table Setups That VCs Accept

The “Delaware parent with foreign team” setup

This is the most common pattern when U.S. investors are involved. A Delaware C-Corp sits on top. The product team may be in India, Europe, or elsewhere. The foreign operation often runs through a local subsidiary or through contractors in the early days.

VCs like this because it fits their playbook. Most U.S. funds have standard documents, standard tax handling, and standard exit paths for Delaware companies. It reduces friction during financing and during acquisition talks.

The danger is not the structure itself. The danger is when the foreign work creates IP that never gets properly assigned to the U.S. parent. If the people building the core tech are outside the parent company and you do not have strong IP assignment agreements, the cap table may look clean while the company’s core asset is legally fuzzy.

The “Singapore or other holdco on top” setup

Some founders choose a non-U.S. holding company, often for regional reasons, investor mix, or future expansion plans. Singapore is a popular choice in Asia because the legal system is stable and investors are familiar with it.

VCs can accept this if the structure is clean and the U.S. investor rights are well handled. But some U.S. funds still prefer Delaware, especially for later rounds. So if you choose a non-U.S. holdco, you need to be prepared to explain why and show that it will not block future financing.

The cap table must also show that all key ownership sits at the top entity, not scattered across operating companies. Investors fund the entity that owns the core business. If value is split between entities, the cap table becomes harder to trust.

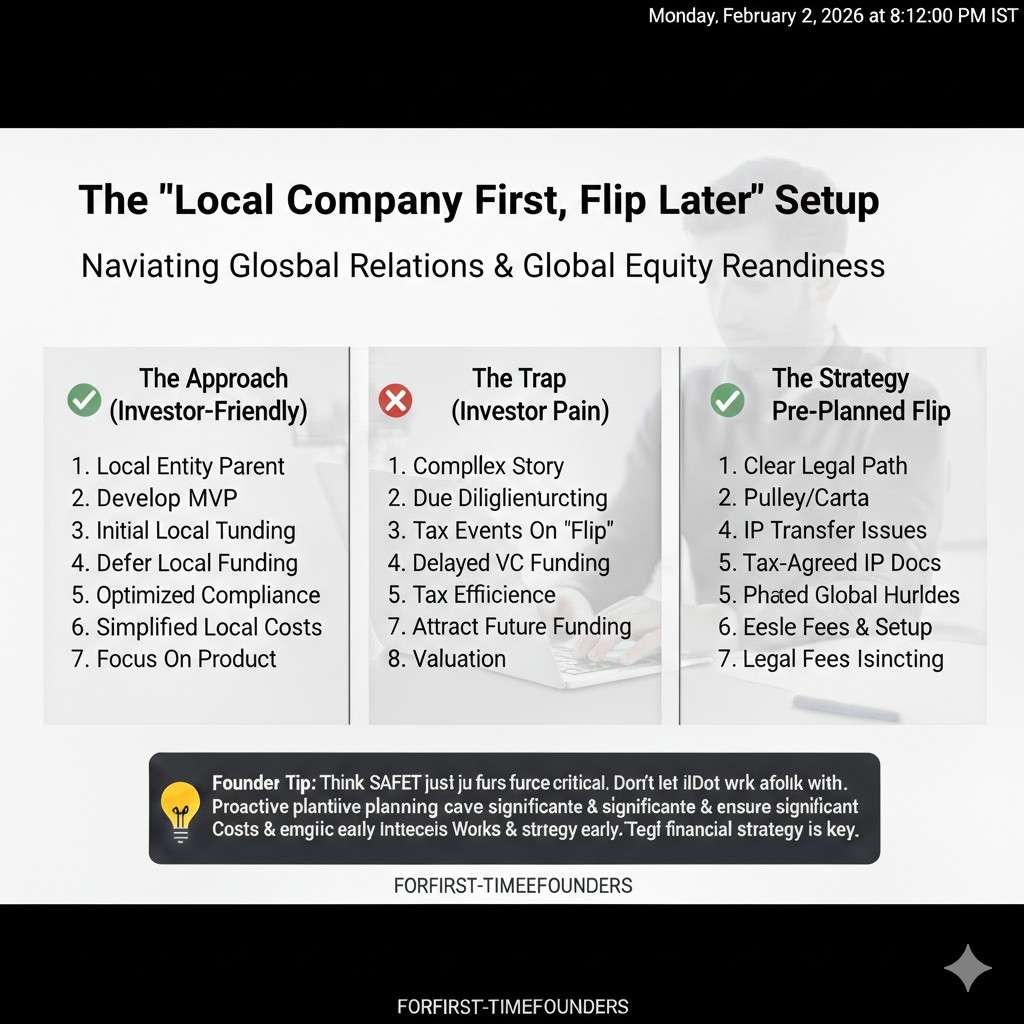

The “local company first, flip later” setup

Many teams incorporate locally first because it is fast and cheap. Then, when a serious global investor appears, they consider a “flip” into a U.S. or Singapore parent. This is common for India-first teams and EU-first teams.

Flips can work, but they must be done carefully. Investors worry about tax shocks, consent issues from early shareholders, and missing documentation. A flip also creates timing risk because it can delay fundraising when you can least afford delays.

A VC-readable cap table in a flip scenario is one that shows the current ownership clearly and also shows a realistic path to the new structure. If you cannot map how today’s shares become tomorrow’s shares, investors will pause.

What investors want to see in any setup

No matter which setup you choose, VCs want the same story. They want one “source of truth” entity where the value sits. They want clean founder ownership, clean option pools, and clean documents.

They also want confidence that the structure will not create a surprise later. That includes tax surprises, regulatory surprises, and IP surprises. In deep tech, the IP surprise is the most common and the most damaging.

Tran.vc focuses on that early. If your cap table is clean but your patents and assignments are not, you still have a risk gap. If you want to close that gap early, you can apply anytime here: https://www.tran.vc/apply-now-form/

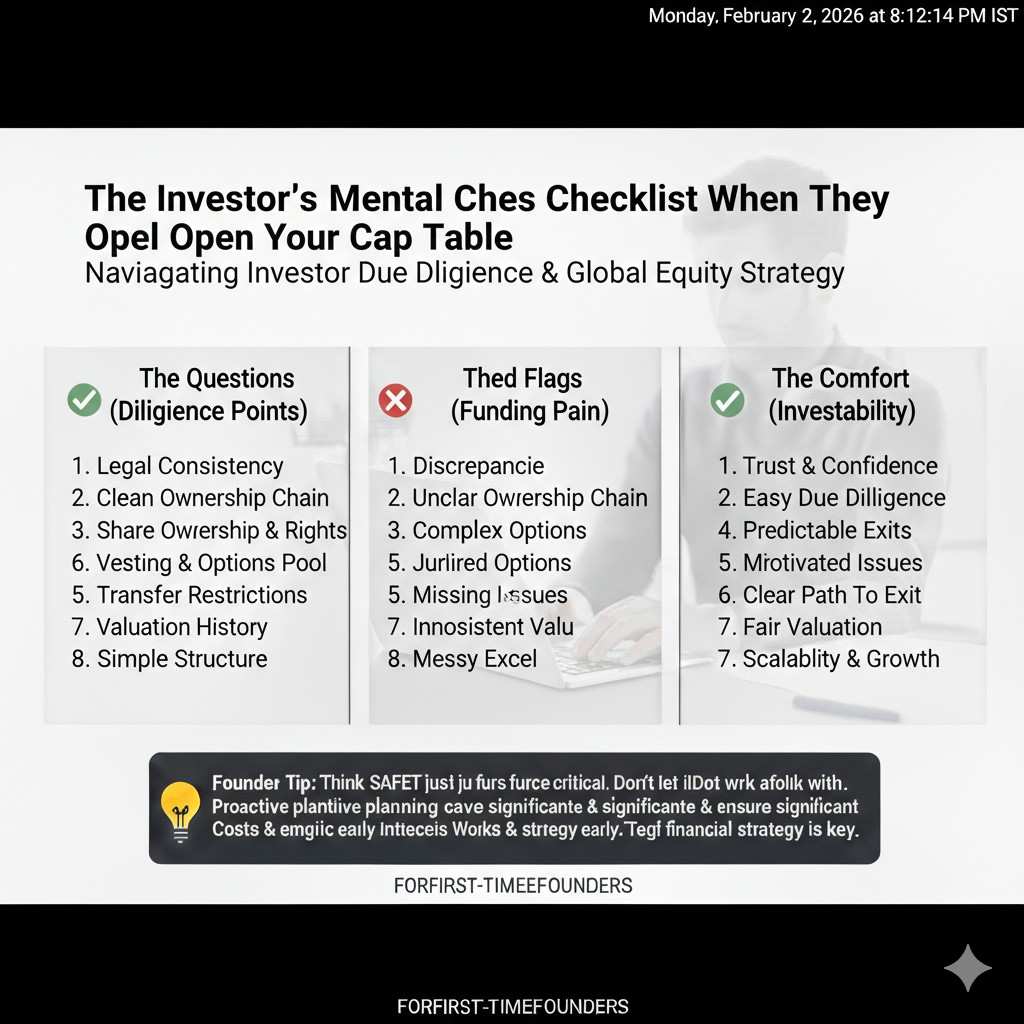

The Investor’s Mental Checklist When They Open Your Cap Table

They look for control and decision clarity

Investors check whether founders still control the company in a practical way. They look for voting power, board rights, and any special rights given away early. In cross-border rounds, they also look for who can sign documents and whether the right entity controls the bank account.

If control is split between countries in a confusing way, investors worry that decisions will get stuck. They want to know that the company can move fast without being blocked by old agreements or foreign compliance issues.

They look for hidden promises

Hidden promises are things like side letters, informal equity promises, handshake deals, and “we will fix it later” allocations. These often show up when early supporters helped in small ways and expected a future reward.

In a local-only company, you might patch that later. In cross-border fundraising, those hidden promises become landmines because they can violate local rules, tax rules, or investor rights.

A VC-readable cap table has no mystery items. If someone is promised equity, it is either already documented properly or it is clearly stated as not granted yet. Ambiguity kills trust.

They look for option pool reality

Option pools are simple in theory and messy in practice. Investors look for whether the pool exists legally, whether grants were approved, and whether the pool size matches the hiring plan. They also look at whether the pool is placed at the right level in a multi-entity structure.

A common cross-border error is granting options from the wrong entity. Another is issuing “phantom” options informally without proper approvals. That creates a mismatch between what the cap table shows and what employees think they own.

Investors do not like employee confusion because it turns into legal conflict later. They want a cap table that supports clean hiring across borders.

They look for IP ownership alignment

Even though this is not “cap table math,” it affects the cap table’s meaning. Investors want to know that the entity they are buying into owns the IP that creates value.

If your U.S. parent is fundraising but the IP is owned by a foreign operating company, or by individual founders, the cap table becomes less valuable. In that case, investors are not buying a clean asset. They are buying a negotiation.

This is where Tran.vc spends real time with deep tech teams. We help you line up ownership, assignments, and patent strategy so that the cap table and the IP story are one clean story. You can apply anytime here: https://www.tran.vc/apply-now-form/

The Most Common Cross-Border Cap Table Problems

Too many entities holding value

Founders sometimes create multiple companies across countries, and then each company starts to look like it owns part of the business. One holds contracts, another holds engineers, another holds the IP, another holds revenue.

Investors do not want to buy a puzzle. They want to buy one clear company that owns the core value and controls the rest through standard subsidiary relationships. When value is spread across entities, diligence becomes a negotiation about what is really being invested in.

A VC-readable structure makes the “value center” obvious. It removes the need for investors to guess which entity matters.

Early shareholders in the wrong place

Sometimes early angels invest into the local operating company, and later you create a parent company for global fundraising. Now the early investors sit in the wrong entity. They may demand special terms to move. They may refuse. Or they may trigger tax issues.

This is not a moral problem. It is a planning problem. A VC-readable cap table avoids it by getting the top-level entity correct before too many people invest. If you cannot, it at least documents a clear and fair conversion path that most shareholders will accept.

Informal equity grants to foreign contributors

Cross-border teams often rely on advisors, part-time builders, and friends in other countries. Equity promises get made casually because everyone is moving fast.

Later, when it is time to formalize, you discover that issuing equity to that person is hard under local rules, or triggers tax issues, or needs government filings. Now you have a promise you cannot easily keep, and your cap table has a shadow cap table behind it.

The fix is not to avoid rewarding people. The fix is to reward them using a plan that is legal and simple from day one, like properly approved equity grants, advisor agreements, or cash-based alternatives when needed.

IP created in one country but owned nowhere cleanly

This is the silent killer for robotics and AI startups. A founder builds a core algorithm while employed by another company. An engineer builds key parts as a contractor without clear assignment terms. A local subsidiary “does the work,” but the parent entity does not receive formal assignment.

By the time you raise, investors want to see a chain of ownership. If the chain is broken, the cap table is not the main issue anymore. The core asset is at risk.

This is why Tran.vc’s model is built around IP-first execution. We do not just “talk strategy.” We help founders lock IP down early with real patent and legal work, so it holds up in diligence. Apply anytime here: https://www.tran.vc/apply-now-form/

The Practical Standard for a VC-Readable Cross-Border Cap Table

One cap table, one truth, one owner story

The most tactical way to think about this is simple. Your cap table should answer three questions without follow-up calls.

Who owns the fundable entity today, in fully diluted terms?

What is already committed, including options and promised pools?

What will it look like after the next priced round?

If your spreadsheet cannot answer those cleanly, fix the structure before you “perfect” the formatting.

The documents must be easy to match

Investors do not only read your spreadsheet. They match it against board consents, stock purchase agreements, option plan approvals, and any side letters.

A VC-readable cap table is one where every line item can be traced quickly. If your counsel has to “interpret” the cap table, you will lose speed. If investors have to request multiple corrections, you lose trust.

Cross-border does not excuse messy basics

Some founders think investors will forgive basic issues because cross-border is complicated. The opposite is true. Cross-border makes investors stricter, because the cost of fixing issues later is higher.

So the tactical move is to make the basics spotless. Clean founder issuance. Clean vesting. Clean option plan. Clean investor docs. Clean IP assignments. When those are clean, cross-border becomes a detail, not a risk.

If you want help getting those basics clean early, and you want your IP to become an asset investors respect, Tran.vc can help. You can apply anytime here: https://www.tran.vc/apply-now-form/

Designing the Top Entity So Investors Stay Comfortable

Start with the end in mind

A cross-border cap table becomes “VC-readable” when the value sits in one clear place. That place is the entity investors are buying into. If that entity is unclear, every other detail becomes harder.

So the first job is not the spreadsheet. The first job is deciding where the parent company should live and why. This is not about choosing the “best” country on paper. It is about choosing the setup that future investors understand quickly and will not fight.

Most founders who want U.S. venture money choose a Delaware C-Corp parent. Many founders with strong Asia ties choose Singapore as a parent. There are other valid choices too. The important thing is that the choice is defensible and consistent with where you plan to raise.

If you pick a structure that your target investors do not like, your cap table may be clean and still not be readable, because the structure itself creates friction.

Avoid the trap of “we can flip later”

A lot of teams say, “We’ll just flip when it matters.” The problem is that the flip often happens at the worst time, right when you are trying to close a round.

That is when you discover that early shareholders must consent, signatures are scattered, and old agreements are missing. You may also discover that a flip triggers tax outcomes for founders or early investors. Even when the flip is possible, it can turn a fast raise into a slow and stressful one.

The more tactical move is to treat the parent decision like a core product decision. You do not need to overthink it for months, but you do need to decide before too many people own shares in the “wrong” place.

Keep the value center obvious

Investors want to fund the entity that owns the thing that matters. That usually means the IP, the customer contracts, and the right to earn revenue.

When the operating team is in another country, you might set up a subsidiary for payroll and local operations. That is normal. The mistake is letting the subsidiary become the “real company” while the parent becomes a shell.

To keep the cap table VC-readable, the parent should own the key IP and the core commercial rights. The subsidiary can do work and sign local employment agreements, but it should not be the place where the business value piles up.

That single design choice makes diligence far smoother because the investor is clearly buying the business, not buying a complicated web of related companies.

Get IP assignment right early, not during diligence

This is where many robotics and AI teams get hit. The team builds in one country. The fundraising entity sits in another. Everyone assumes the IP “belongs to the startup” because the startup paid for the work or because the founders created it.

Legally, that assumption is often wrong. IP can sit with individuals, with contractors, or with the local entity that signed the work agreements. Investors know this, so they check.

The safest approach is to have clean invention and IP assignment agreements in place from day one, and to make sure the parent entity is the final owner. That includes founders, employees, contractors, and even advisors who touch core technical work.

Tran.vc helps deep tech teams lock this down early and build a strong patent plan that supports the cap table story. If you want that kind of hands-on IP support without giving up control early, you can apply anytime here: https://www.tran.vc/apply-now-form/

Avoiding Painful Cross-Border “Flips” and Restructures

Understand what a flip really changes

A flip is not just moving a logo from one country to another. It changes who owns what, where shares sit, and how future funding will work.

In a typical flip, a new parent company is formed. Shareholders of the old company swap their shares for shares in the new parent. Then the old company becomes a subsidiary.

On paper, this sounds clean. In reality, it requires clean records, clean consents, and clean tax planning. If your early cap table is messy, a flip makes that mess more expensive.

A VC-readable cap table is one that makes a flip possible without drama. Even if you never flip, having the records in shape gives investors confidence.

Fix your records before you “need” them

Founders often wait until a lead investor asks for a restructure. That is late. The worst moment to discover missing documents is when a term sheet is already on the table.

A better approach is to do a “cap table health check” before fundraising. That means making sure founder issuances are documented, vesting is correct, option grants are approved properly, and all transfers are recorded.

When this is done early, the flip conversation becomes simple. Investors see you as low risk. They may still request a structure change, but it will feel like a planning step, not an emergency.

Be careful with early foreign investors in a local entity

Another pain point is early investors who bought shares in the operating company, especially when the operating company is in a country with strict rules about share transfers to foreigners.

When you flip, those investors must swap into the new parent. If local rules make that slow or hard, the entire flip becomes slow or hard. This is one reason many founders prefer to set the fundable parent early, before taking international money.

If you have already taken local money, do not panic. But do not ignore it either. You need a clean plan to move those holders into the new structure, and you need it documented in a way investors can follow.

Avoid multiple share classes unless there is a real reason

Founders sometimes create extra share classes across borders to “make things work.” This can lead to a cap table that is difficult to read and even harder to model.

If you are early stage, keep it simple. One common share class for founders, one preferred class for priced rounds, and one option plan, all at the parent level. That is usually enough.

If your local setup forces something different, document it clearly and make sure your counsel can explain it in plain words. VCs do not fear complexity when it is necessary. They fear it when it looks accidental.

If you want support designing a structure that stays simple while still protecting your technical edge with patents, Tran.vc can help. Apply anytime here: https://www.tran.vc/apply-now-form/

Keeping Founder Equity Clean Across Borders

Founder stock should be issued correctly from day one

In diligence, investors often start by checking founder ownership. They want to see that the shares were actually issued, that the purchase price is recorded, and that vesting is documented.

In cross-border teams, founders sometimes split shares informally across local and foreign entities. Or they “plan” to issue shares later. Or they issue shares but do not complete basic paperwork.

All of those create questions. Questions slow diligence. The practical fix is simple: make sure founder shares are properly issued by the fundable parent entity, with clear vesting terms and clear documentation.