If you are raising money from investors outside your home country, your data room is not just a folder of files. It is your first trust test. Cross-border investors often move fast, but they are also careful. They worry about things local investors may not worry about as much: legal gaps, tax surprises, ownership confusion, IP that is not protected in the right places, and simple misunderstandings caused by different norms.

A clean data room reduces fear. It also saves you weeks of back-and-forth. Most founders think a data room is only for “later.” In real life, it is one of the best leverage tools you have early. When you can answer hard questions with clear proof, you look like a team that can execute. And when you remove doubt, you shorten the time to a yes.

This guide will show you what to include when your investors sit in another country. Not in theory. In a practical, founder-friendly way. The goal is simple: help you build a data room that makes it easy for a serious investor to keep going, not to pause, not to worry, and not to walk away.

If you are building in AI, robotics, or deep tech, this matters even more. Your work is often hard to explain in one meeting. Your moat is often invisible to non-technical people. Strong IP and clean ownership make your story real. That is where Tran.vc can help. Tran.vc invests up to $50,000 in in-kind patent and IP services so you can build defensible assets early, before your seed round pressure hits. If you want help making your IP “investor-ready” for cross-border diligence, you can apply anytime here: https://www.tran.vc/apply-now-form/

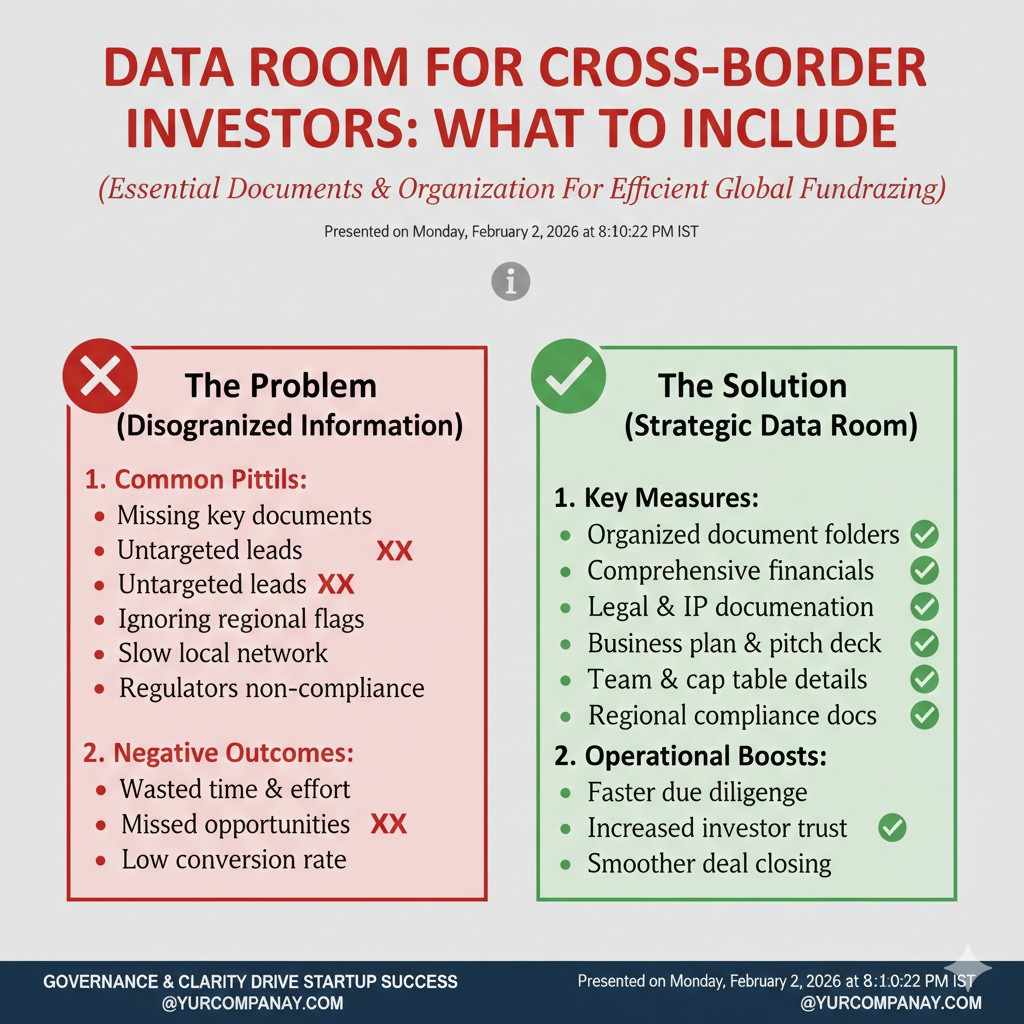

Data Room for Cross-Border Investors: What to Include

Why a cross-border data room is different

When an investor sits in another country, they do not just check your company. They also check your “risk map.” They ask themselves where the deal can break because of laws, taxes, or unclear ownership. Even if they love your product, they may slow down if your files feel messy or incomplete.

A strong cross-border data room is built to remove friction. It is set up so a smart person who does not know your local system can still understand your company in one pass. If they need five emails to understand one document, your process becomes expensive for them. And expensive often means “no.”

This is also where many technical founders lose time. You may be building fast, shipping code, and hiring. But a cross-border investor will still expect clean proof of what you own, how you earn, and how money moves through the business. The faster you can show those facts, the more control you keep in the raise.

If you are in AI, robotics, or deep tech, there is another layer. Your value often sits in models, methods, and know-how. If that value is not protected or clearly owned, the investor’s job is to assume the worst. Tran.vc helps founders avoid that trap by investing up to $50,000 in in-kind IP and patent services so your “moat story” is backed by real documents, not just slides. If you want help, apply anytime: https://www.tran.vc/apply-now-form/

How to think about the structure before you upload files

Cross-border investors do not want a dump of PDFs. They want a clear path. You are building a guided tour that answers their questions in the order they will ask them. If you set that order well, diligence feels smooth and calm. If you set it poorly, they keep getting stuck, and each stuck moment adds doubt.

A simple way to design the structure is to imagine three stages. First, they want to confirm you are real and investable. Second, they want to confirm your numbers and contracts match your story. Third, they want to confirm nothing hidden will explode after they wire funds. Your data room should follow that flow.

Also, do not hide the hard stuff. Cross-border investors are used to seeing issues. What they hate is surprise. If you have a risk, show it with context and a plan. That moves you from “problem” to “managed problem,” which is a very different feeling.

What “good” looks like to a cross-border investor

A good data room lets them answer key questions without calling you. It also makes it easy to share with their lawyers, tax team, and partners. That means your files should be readable, named well, and grouped in a way that makes sense in any country.

You also want one short document that acts like a map. Think of it as a welcome note that explains what is inside and where to find it. It should not be long. It should be clear. It should reduce the chance that they misread something and assume you are hiding it.

One more detail matters a lot: dates. Use dates that are easy to read. Write “31 Jan 2026” instead of “01/31/26” or “31/01/26.” Different countries read those formats differently, and small confusion can cause big mistakes in legal review.

Common mistakes that slow down cross-border diligence

Many founders try to keep things “light” early and only share serious files later. With local investors, that can sometimes work. With cross-border investors, it often does not. They are already taking distance risk. If you also make them chase facts, they may choose a closer deal.

Another mistake is mixing drafts and final versions. If the investor sees three versions of the same contract, they do not know which one counts. That creates a trust gap. You can still keep drafts, but put them in a separate folder labeled clearly as drafts, with a note that says what is final.

A third mistake is treating IP like a slide topic. For deep tech, IP is not decoration. It is proof that the company can defend what it is building. If your IP files are missing or unclear, cross-border investors may worry you cannot enforce rights in their markets, or that employees could claim ownership later.

Tran.vc exists for this exact pain point. The firm supports technical founders with up to $50,000 in in-kind patent and IP services so you can show strong, clean IP early, without burning cash. If you want to set this up the right way, apply here: https://www.tran.vc/apply-now-form/

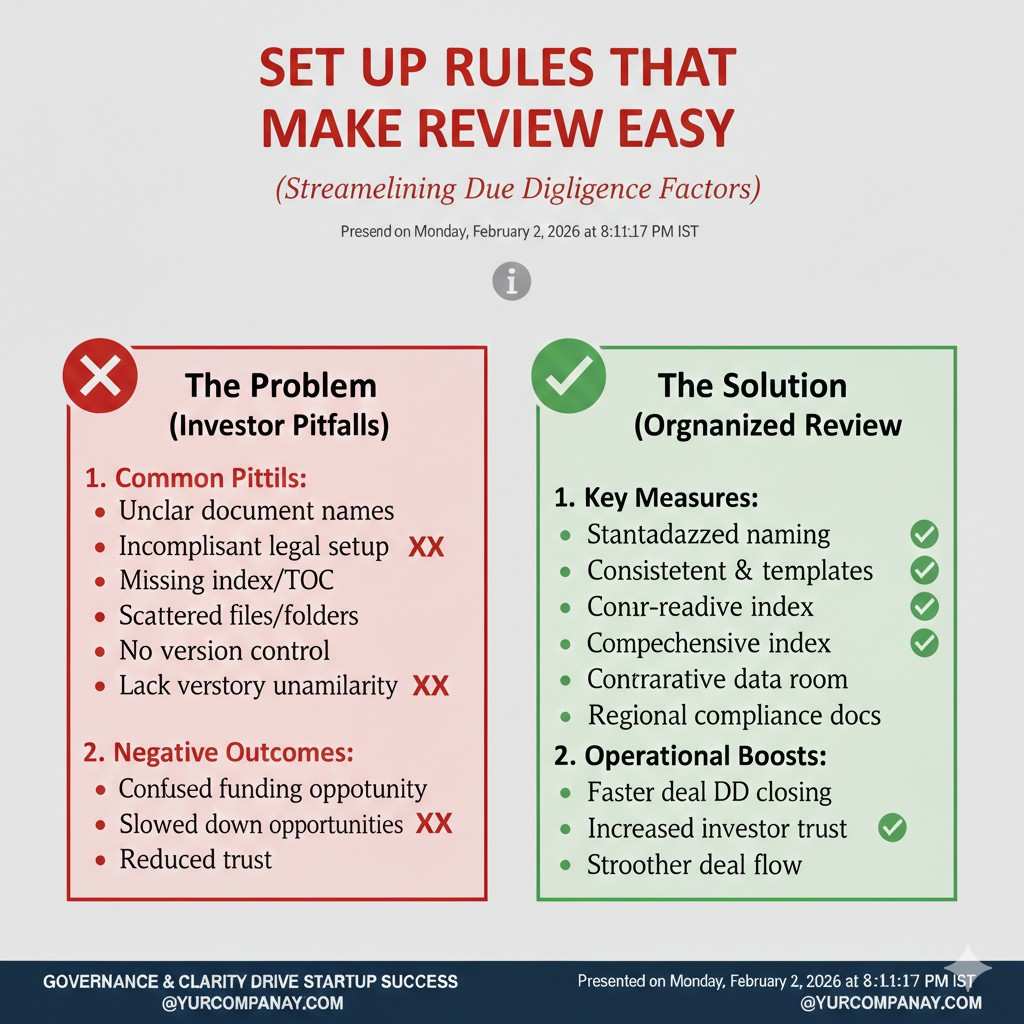

Set Up Rules That Make Review Easy

File naming that works across countries

Choose one naming pattern and stick to it. The pattern should tell them what the file is, the date, and whether it is final. For example, “Customer_A_MSA_2025-11-08_FINAL.pdf” is boring, but it is perfect. It removes guesswork, and guesswork is what causes delay.

Avoid names like “final_final_reallyfinal2.pdf.” Investors see that and assume the company is chaotic. You may be moving fast, but the data room should feel controlled. That is the whole point. You want them to feel that even under pressure, you run clean operations.

Also, make sure your file names do not rely on local shortcuts. If you use short local words for tax forms or legal filings, add a small note in the folder that explains what those words mean. Do not assume they know your local terms.

One-page “data room guide” that saves days

Add a single document at the top called something like “Read Me First.” In it, explain how the folders are organized and what each section covers. If there is anything unusual about your structure, explain it there. This helps an investor team split work without losing context.

Include one simple point of contact in that guide. It can be you, your CFO, or your counsel. Cross-border teams often work in different time zones. If they do not know who to ask, questions sit unanswered for days. A clear contact reduces that risk.

This guide is also a good place to say what is missing and when it will be added. If a key contract is still being signed, say so. If you are still waiting on a government filing, say so. You do not need to over-explain. You just need to be honest and clear.

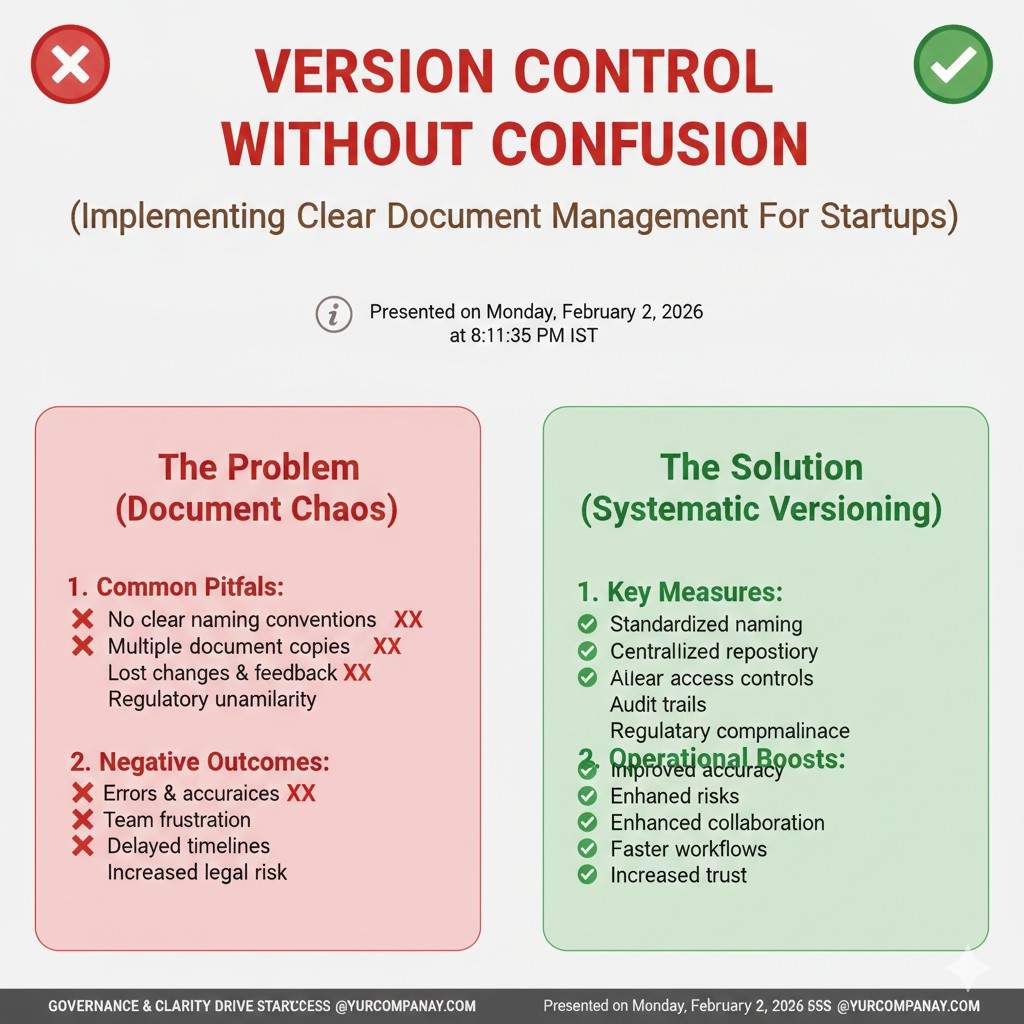

Version control without confusion

Use “FINAL” only when it is truly final. If you want to keep a signed copy and an editable copy, label them clearly. For example, “Signed” and “Editable” are easy labels. Your goal is to make it hard to misread the state of a document.

If you have a cap table tool export, include the export date in the file name. Cross-border investors care a lot about “as of” dates. If they do not see a date, they assume the file is stale. Stale files lead to extra questions and slower momentum.

If you have contracts that were amended, include both the original and the amendment, plus a combined “restated” copy if you have one. This is not about volume. It is about making it easy for legal review to see the full picture.

Language, translation, and what you should not do

If some documents are not in English, consider adding short translations or summaries for the key ones. You do not need to translate every page of every file, but you should remove blockers. Investors should not have to pay for basic translation just to decide if they want the deal.

Be careful with informal “founder summaries” that conflict with the real document. If you add a summary, make sure it matches the contract. If there is a mismatch, the contract wins, and the mismatch becomes a trust issue.

For deep tech IP documents, translation issues can be costly. Patent language is precise. If you are sharing filings from another country, it helps to include an English summary from counsel. This is one area where Tran.vc’s IP support can save you real time and avoid misunderstandings with global investors. Apply anytime: https://www.tran.vc/apply-now-form/

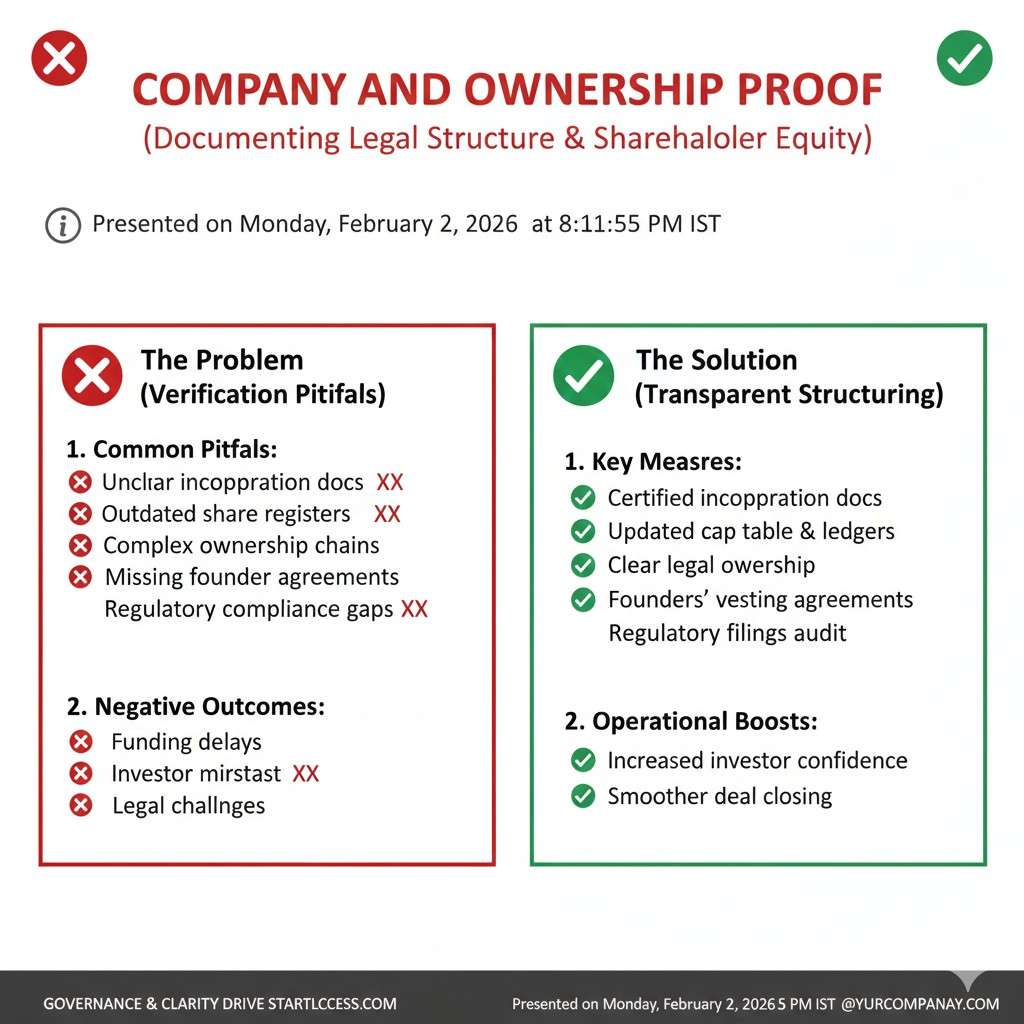

Company and Ownership Proof

The basic company documents investors will ask for first

Cross-border investors often begin with “Are you properly formed?” They want proof your company exists, is active, and is owned the way you say. That means your incorporation certificate, bylaws or equivalent, and any shareholder agreements should be clean and easy to find.

If you have multiple entities, such as a local operating company and a parent holding company, explain the structure. Do not make them guess why there are two names. If they have to guess, they may assume the structure is meant to hide something.

Also include a short description of what each entity does. One or two paragraphs is enough. This is not marketing. It is clarity. It helps their counsel understand why the structure exists and whether it creates tax or control risk.

Capitalization details that cross borders make more complex

Your cap table must be current and consistent with your legal documents. If you have option grants, show the option plan, board approvals, and a clear schedule of grants. Cross-border investors often check these details early because mistakes here are expensive to fix later.

If you raised money on SAFEs, notes, or similar instruments, include each agreement and a simple summary of key terms. Do not bury this in a long email thread. Put it in the data room so they can model dilution properly.

Also include any side letters. Many founders forget these. Side letters can create special rights that other investors do not have. Cross-border investors will care because those rights can affect control, future rounds, and exit outcomes.

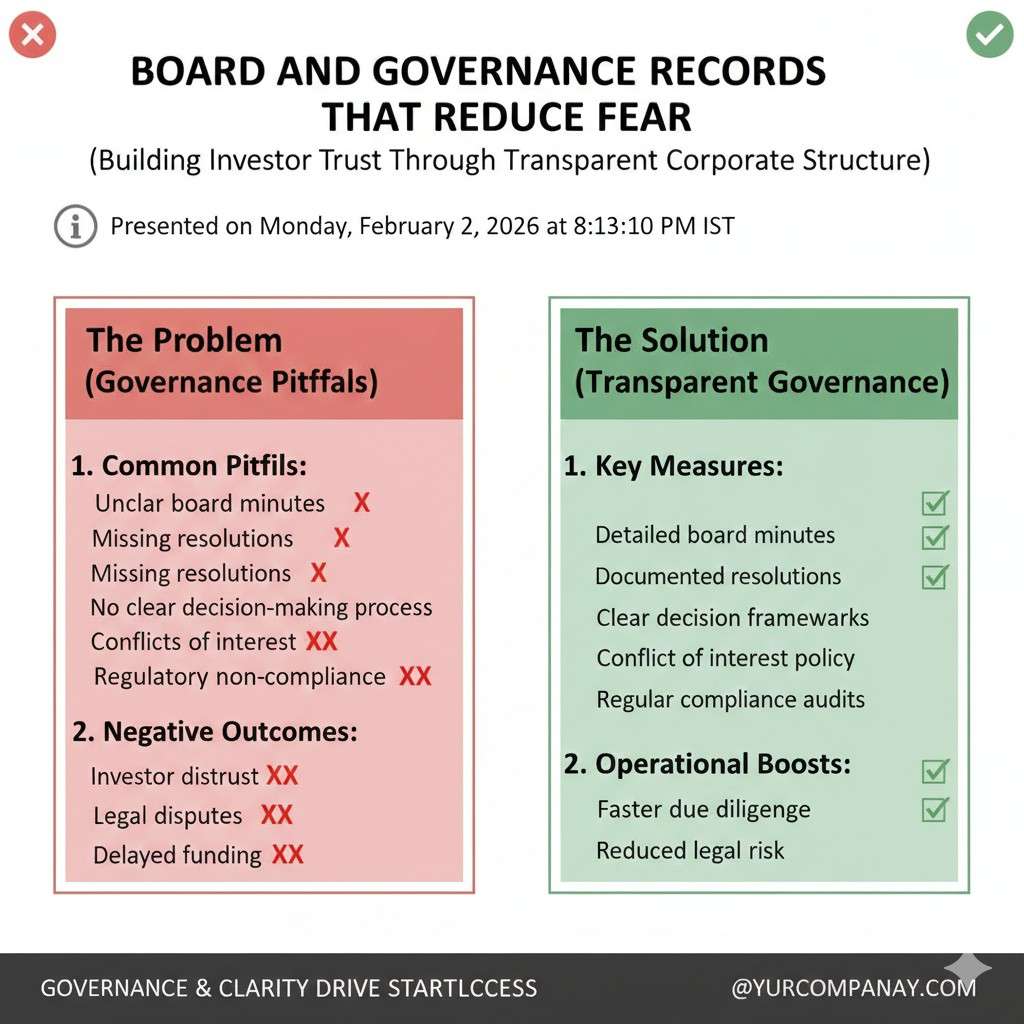

Board and governance records that reduce fear

Investors want to see that your company makes decisions properly. That means board consents, key resolutions, and major approvals should be available. You do not need to upload every minor approval, but you should include approvals tied to funding, equity, major hires, and key contracts.

If your company is early and you do not have formal board minutes for everything, do not panic. Gather what you have, and start improving now. Investors can accept early-stage messiness if they see that you are now running with discipline.

This is one place where a short note helps. If you are missing a record, add a note that explains what happened and how you will fix it. Showing a plan is often better than hiding the gap and hoping no one notices.

Beneficial ownership and compliance expectations

Some countries require investors to check beneficial ownership rules and compliance steps. These checks can include KYC and AML requirements, and sometimes sanctions screening. You do not have to become an expert in all of this, but you should be ready with basic facts.

That means you should have founder IDs ready to share through secure channels, and you should have a list of major shareholders with ownership percentages. Investors may not ask for this on day one, but if they move forward, it often becomes urgent.

Cross-border funds also care about whether any shareholder is a government entity or a politically exposed person. This is not personal judgment. It is compliance. If it applies, it is better to address it early and calmly.

Financials and Tax

The financial story must match the legal story

Cross-border investors often start with your pitch deck, then test it against your data room. If your deck says you have steady revenue, they will look for bank statements, invoices, and contracts that show the same pattern. If your deck says you are lean, they will look for payroll, vendor spend, and burn that lines up.

This is not about being perfect. It is about being consistent. Small gaps are normal, especially early. But when facts do not match, the investor has to assume there is a hidden issue. That is what slows things down.

A good rule is to treat the data room like a courtroom. Not in a dramatic way, but in a practical way. Every big claim should have a simple proof file behind it. When that is true, diligence feels easy and the investor can focus on the deal, not the cleanup.

What to include if you are pre-revenue or early revenue

If you are pre-revenue, investors still want to see financial discipline. They want to know how you track cash, how you approve spend, and how you plan runway. That means a simple cash forecast, actual spend to date, and your current bank balance proof.

If you have early revenue, include a basic revenue schedule that shows who pays, what they pay for, and when they pay. Keep it readable. The investor should not need a finance degree to understand it. Cross-border teams often hand this to someone internal who was not in your calls, so clarity matters.

Also include your chart of accounts and your accounting method if you have one. If you do not, say what you use to track spend. Even a clean spreadsheet is fine at the start. What matters is that you can explain it and it stays stable from month to month.

Financial statements that reduce doubt fast

If you have profit and loss statements, balance sheets, and cash flow statements, include the last 12–24 months if available. If you are early and do not have full statements, include what you have, plus bank statements for key months. Investors mainly want to see cash movements and proof that numbers are real.

If you have audited statements, include them. If you do not, do not apologize. Most early startups do not. But do make sure your numbers are prepared in a clean, consistent way. A sloppy export with missing lines creates the wrong impression.

Add short notes for unusual items. If you had a one-time legal bill, or a big hardware purchase, put a short explanation in a separate note. This prevents the investor from guessing and assuming the worst.

Tax documents that matter more across borders

Tax is one of the biggest sources of cross-border fear. Investors worry that your company may have unpaid taxes, incorrect filings, or unexpected tax exposure in another country. The goal of your data room is to show that you have filed what you needed to file, and that you know what you do not know.

Include corporate tax filings, VAT/GST filings if relevant, payroll tax filings, and any tax registration documents. If you operate in more than one country, include a short note explaining where you have tax presence and why. Even a simple explanation reduces panic.

If you have received any tax notices, include them with the response and current status. This is one of those areas where hiding is worse than honesty. Investors have seen tax notices before. What they want to know is whether you handle them in an organized way.

Transfer pricing and intercompany payments

If you have a parent company in one country and an operating company in another, you may have intercompany agreements, management fees, cost sharing, or licensing. Cross-border investors will look closely here because mistakes can create future tax problems.

If you have intercompany agreements, include them. If you do not, but you do move money between entities, include a memo explaining how it works today and what you plan to formalize. Again, the goal is to replace mystery with a clear picture.

If you charge one entity for R&D done in another entity, be ready to explain the logic. You do not need to solve transfer pricing alone, but you should show you are aware it exists. This is often where good counsel helps, and it is one reason founders tighten structures before a major round.

Contracts and Revenue Proof

Customer contracts that cross-border investors will scan first

Cross-border investors want to see who buys, what they signed, and what could go wrong. They often start with your biggest contracts. They look for term length, renewal rules, termination rights, payment terms, liability limits, and any clauses that block scaling.

Include your standard customer agreement, plus any contracts that are not standard. If a customer demanded special terms, put that version in the room. The investor will assume special terms exist even if you do not show them, so it is better to be clear.

Also include any statements of work, purchase orders, and amendments. Many startups store these across email threads. Pull them together. A contract without the SOW is like a story without the ending.

Revenue recognition and invoices that support the story

Even if an investor does not do full accounting diligence early, they will often spot-check. They may pick three customers and ask for the signed contract, the invoice, and proof of payment. If you can produce those in minutes, you look sharp and trustworthy.

If you have a billing system, export clean reports. If you do manual invoices, include a folder with sample invoices and payment confirmations for key accounts. You do not need to upload every invoice if you have hundreds, but you should be ready to show a clear trail.

If you have pilots that are free or discounted, label them clearly. Cross-border investors will still count them as proof of demand, but they need to know what is paid and what is not paid. Confusion here can make them doubt your revenue claims.

Supplier, vendor, and manufacturing agreements

For robotics and hardware-heavy AI products, vendor and manufacturing risk matters a lot. Cross-border investors worry about supply chain, lead times, and who owns tooling and designs. Include key supplier agreements, manufacturing agreements, and any important purchase commitments.

If you rely on one supplier for a critical part, include a note explaining your backup plan. It does not need to be long. It just needs to show you have thought about it. Investors often accept concentration risk if they see active mitigation.

If you have quality terms, warranty terms, or return terms with suppliers, include those. These clauses can drive future cost. Cross-border investors often come from markets where warranty issues can destroy margins, so they will look.

Data protection and security agreements

Cross-border deals often trigger questions about data laws. If you collect user data, handle sensitive enterprise data, or train models on customer data, expect questions. Include your privacy policy, security policy, and any data processing agreements you sign with customers.

If you have a security assessment, penetration test, or SOC plan, include it. If you do not, include a short note stating what you do today and what you plan to do. Many early startups are not SOC 2 yet, and that is fine. What matters is that you treat security as real.

If you operate in regions with strong privacy rules, be ready to explain how you comply. You do not need to become a lawyer. But you should be able to show which rules matter to you and who supports you on compliance.

Employment and contractor agreements tied to delivery

Investors will also check whether the people building the product are properly tied to the company. Include offer letters, invention assignment agreements, contractor agreements, and any consulting deals with key contributors.

Cross-border investors are sensitive to contractor-heavy teams because of ownership risk. If a contractor wrote core code and never assigned rights, your product can become legally shaky. This is one of the fastest ways to lose trust.

If you are missing an invention assignment for someone, do not hide it. Fix it now and then include the signed document. If you need help cleaning this up in a way that supports future patent filings, Tran.vc can guide you through it as part of its in-kind IP support. Apply anytime: https://www.tran.vc/apply-now-form/

Intellectual Property and Product Proof

Why IP is the center of cross-border trust for deep tech

In cross-border investing, IP is often the bridge between “interesting tech” and “investable company.” Investors worry about whether you can defend your edge in the markets they care about. They also worry about who truly owns the inventions and whether a future dispute could shut down growth.

A strong IP section in your data room does not need to be huge. It needs to be clean. It should show ownership, filings, strategy, and the link between the IP and your product roadmap. When that link is obvious, your valuation conversation becomes easier.

This is the core of what Tran.vc supports. Many founders wait too long, then rush filings under pressure. Tran.vc helps you build an IP plan early and back it with real patent work, worth up to $50,000 in-kind, so cross-border investors see a company that is prepared. If you want that support, apply here: https://www.tran.vc/apply-now-form/

What to include for patents and patent strategy

If you have filed patents, include the filing receipts, applications, office actions if any, and any granted patents. Also include a short, plain-language summary of what each filing covers and why it matters. Investors do not want to decode legal text. They want to understand the business value.

If you have not filed yet, include a clear plan. That plan should explain what you will file, what markets matter, and what timeline you are working on. You can do this in a couple of pages. The key is that it feels intentional, not random.

Also include inventor lists and assignment documents. Cross-border investors want proof that the inventors assigned rights to the company. If this is not clean, they may worry you cannot enforce patents later, especially in another country.