Most founder fights don’t start with ego. They start with paperwork that felt “small” on day one.

Founder stock is one of those things.

It seems simple: “We’ll split it fairly. We trust each other.” Then six months later, someone leaves, a new co-founder joins, an investor asks for clean cap table docs, or your lawyer says, “Wait… who actually owns what?” And suddenly you are doing surgery while the patient is awake.

This guide is here so you don’t have to learn the hard way.

Founder stock is not just a number on a spreadsheet. It is a set of promises about ownership, control, risk, time, and what happens if life gets messy. If you set it up right, it keeps you fast, focused, and fundable. If you set it up wrong, it can scare investors away, poison trust inside the team, and limit your options right when you need them most.

Tran.vc works with technical founders who are building hard things in AI, robotics, and deep tech. These teams often move fast on product and research, but they delay the company setup because it feels “legal” and not “real work.” Here’s the truth: your stock setup is part of your product. It is the frame that holds the whole thing together.

And one more thing before we begin: nothing here is legal or tax advice. Founder stock is full of rules that change by country and state. Use this as a clear playbook, then confirm the final moves with a startup lawyer and a tax pro. The goal is to help you ask the right questions and avoid the common traps.

If you want Tran.vc to help you build a strong foundation early—so you can raise later with leverage and protect what you’ve built—you can apply anytime at: https://www.tran.vc/apply-now-form/

Now let’s get into it.

Founder stock, in plain words, is the ownership you and your co-founders get at the start. It is usually “common stock,” meaning it is the basic ownership class, not the special class investors may get later.

When people say, “We each have 50%,” they are talking about founder stock. But the real setup is not only the split. It includes:

Who gets how many shares

When those shares are truly earned

What happens if someone leaves

How decisions get made

How the company stays able to hire and raise

If you only do the split and skip the rest, you are leaving the door open to chaos.

Here is the most common founder stock mistake: giving shares that are fully owned on day one.

It sounds kind. It feels trusting. It seems fair.

It is also risky.

Because early-stage startups are not stable jobs. People leave. People burn out. People get sick. People move. People find out the role is not what they thought. If someone owns a huge part of the company and then stops contributing, the team has a serious problem. You can’t easily fix it later.

That’s why “vesting” exists.

Vesting means shares are earned over time, not all at once. You still issue the shares at the start, but the company has the right to buy them back if a founder leaves early. This protects the people who stay and keep building.

Decide the Split Without Regret

Start with the real question, not the math

A founder split is not only about fairness. It is about what keeps the team steady when things get hard. Most startups do not fail because the idea is weak. They fail because the team breaks under stress.

So the right first question is simple: if this company works, will everyone feel proud of the deal they made at the start? If the answer is not clear, you should slow down and talk more before you lock anything in.

Talk about risk in plain words

Two founders can work the same hours and still take very different risks. One person may quit a stable job and lose income. Another may keep a salary while testing the startup on nights and weekends.

Risk also shows up in personal life. One founder may move countries or change visa status. Another may put their savings in the company. These things matter because they shape how much the company costs each person.

If you skip this talk, it comes back later as quiet resentment. That resentment is much harder to fix than a hard talk today.

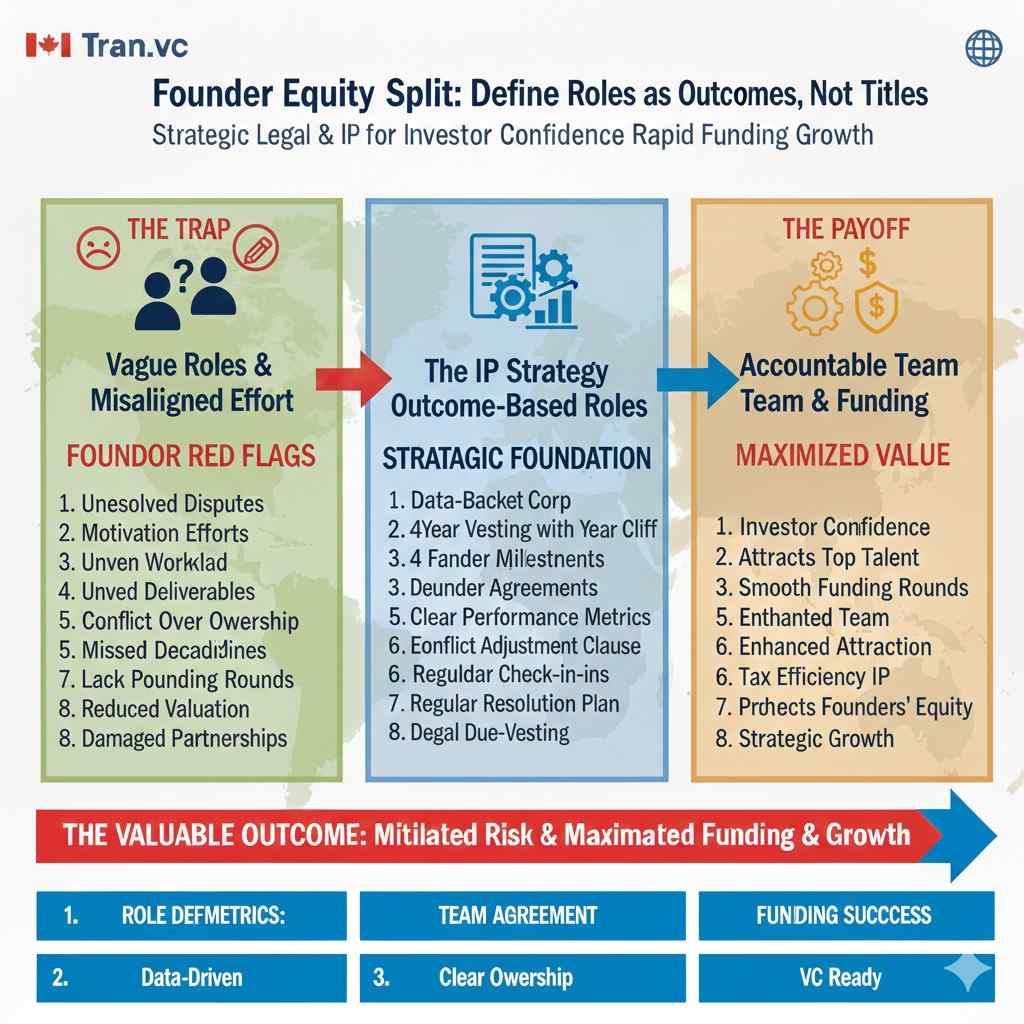

Define roles as outcomes, not titles

Early teams love titles because titles feel official. But titles do not build companies. Outcomes do. “CTO” can mean ten different things. “CEO” can mean one person does sales, hiring, and money, or it can mean none of that.

A better way is to say what each founder will own. Who will ship the product. Who will talk to customers. Who will hire. Who will raise money. Who will handle legal and finance. The split should reflect who carries which outcomes for the next two years.

Make the future workload visible

Early work is exciting. Later work is heavier and less fun. The later work includes missed deadlines, support calls, hiring mistakes, investor pressure, and tough customer feedback.

Some founders naturally take on those messy parts. Others prefer clean research and clean builds. Both are valuable. But the split should match the future load, not only the past effort.

If one person will carry most of the “people work,” they often deserve more equity, because that work is constant and draining.

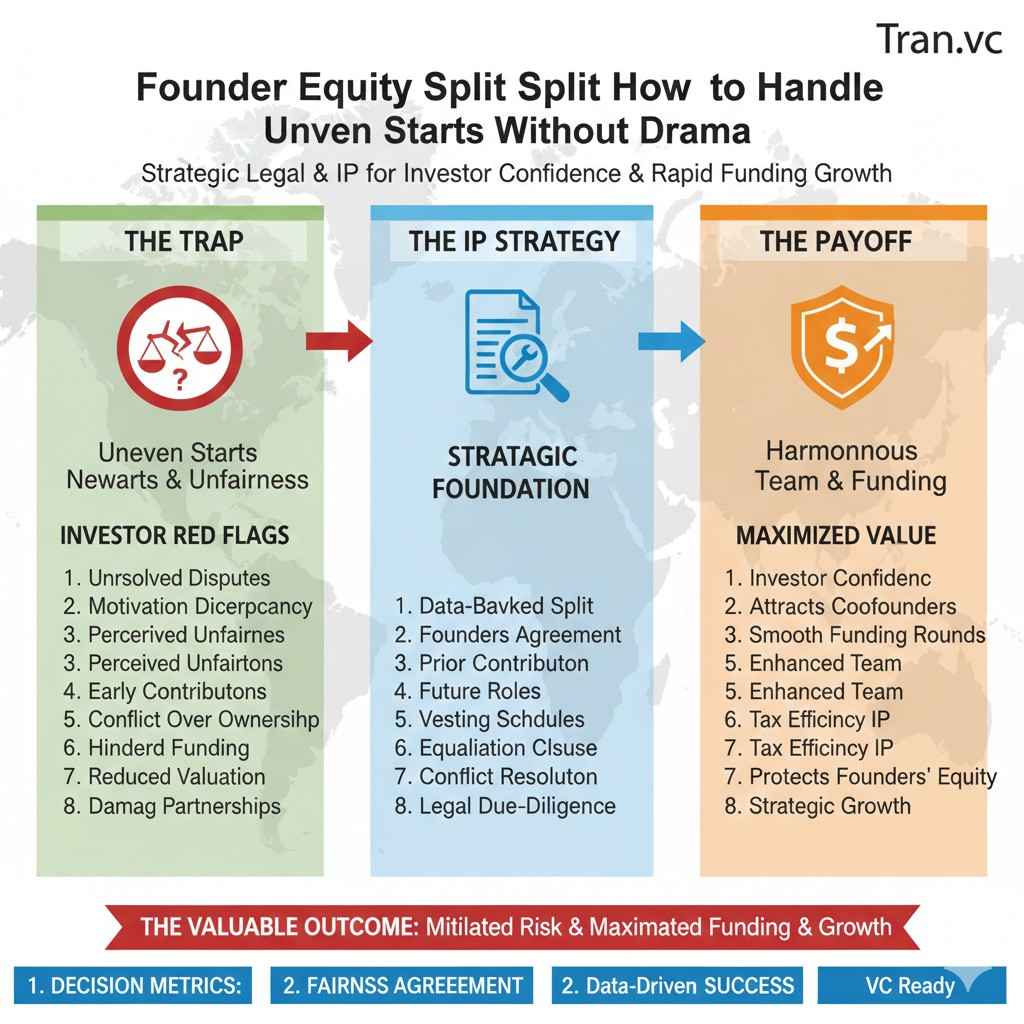

Handle uneven starts without drama

It is common for founders to start at different times. One founder may have built the first version before the other joined. If you pretend that did not happen, you are setting a trap for later.

You do not need to create a complex formula. You can simply agree on a small adjustment. Or you can align vesting start dates to reflect when each founder truly began contributing.

The key is to name reality out loud and match the deal to it.

Use a calm “what if” check

Before you finalize the split, run a few “what if” stories. Not to scare anyone, but to protect everyone. What if one founder leaves in month nine. What if a third founder joins in month six. What if an early investor demands a larger option pool.

If the split still feels stable through those stories, you are close. If it starts to feel fragile, you need to adjust before you sign.

If you want Tran.vc to help you think through this in a clean, founder-friendly way, you can apply anytime at: https://www.tran.vc/apply-now-form/

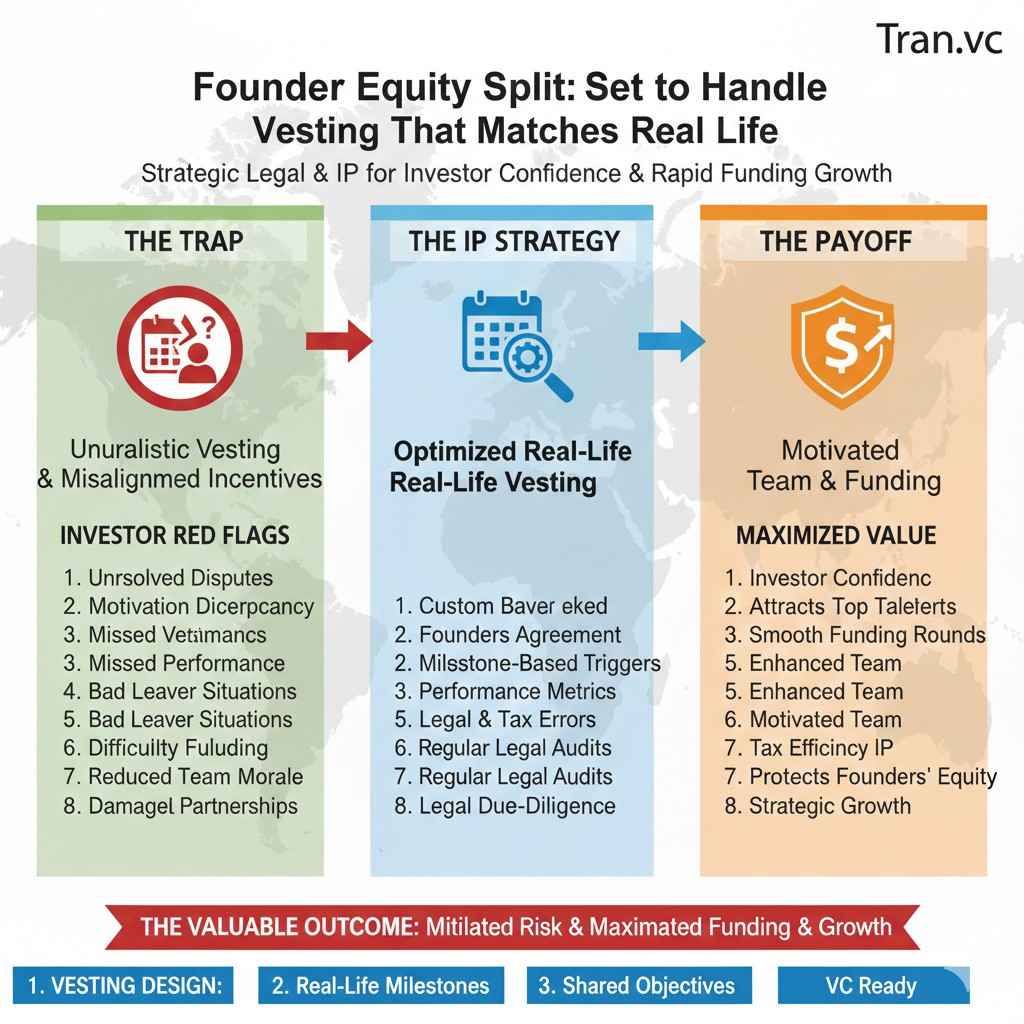

Set Vesting That Matches Real Life

Why vesting is a trust tool

Founders often see vesting as a legal trick. It is not. It is a simple trust tool. It protects the people who keep building, while still honoring the work someone already did.

When vesting is clear, the team can focus on product, customers, and IP. When vesting is vague, every hard week turns into a fear that someone might walk away with a large piece of the company.

The “four years with a one-year cliff” idea

This pattern is common because it is easy to understand and easy to explain to investors. The one-year cliff is the proof period. After that, shares vest over time, usually each month.

That said, the “standard” is not sacred. It is only a starting point. The right schedule is the one that fits your team and your risk.

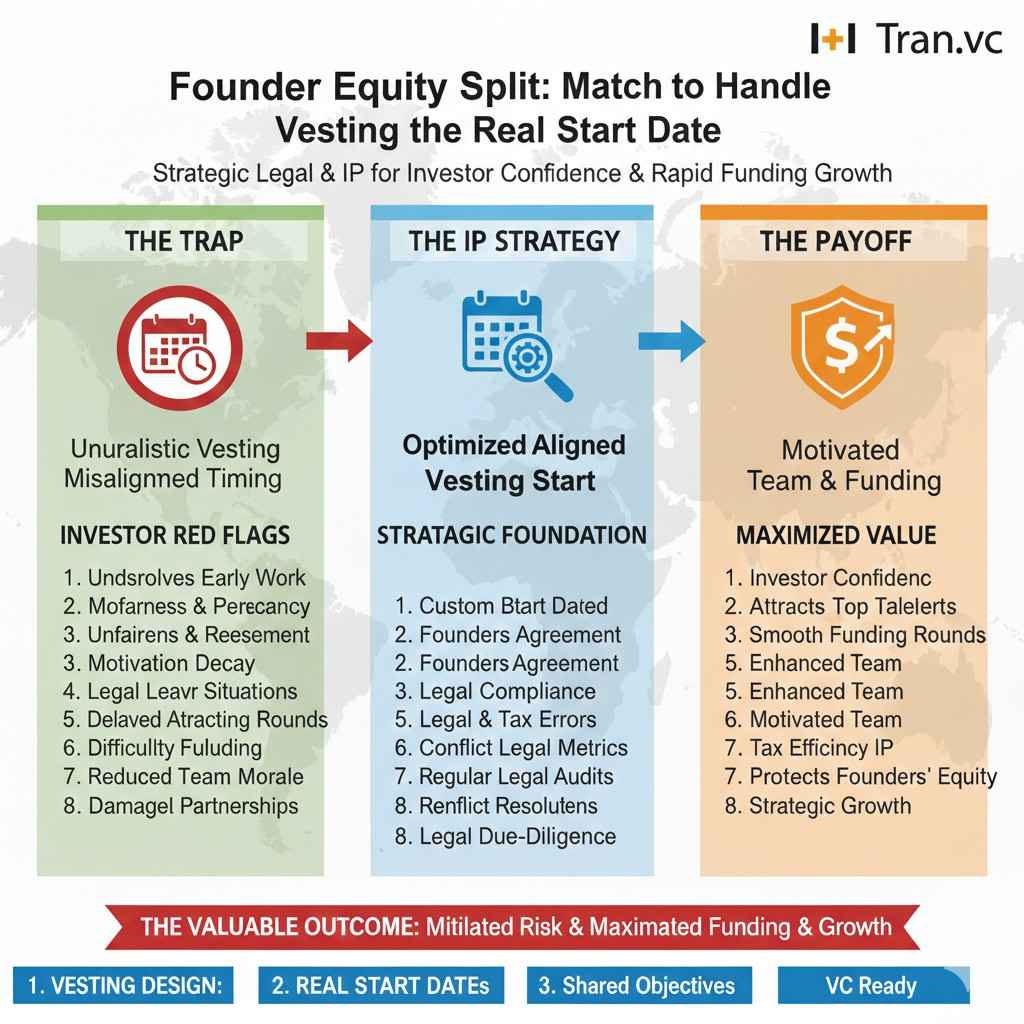

Match the vesting start date to the real start date

This is where many teams slip. They sign documents on the same day, then set the same vesting start date, even if the founders did not start together.

If one founder was building for six months before the company formed, it can make sense to credit that time in the vesting schedule. This is not about being nice. It is about preventing future anger that damages the company.

The clean way is to talk about it openly, then reflect it in the documents.

Decide what happens if a founder leaves

You want a rule that is simple enough to follow during an emotional moment. The most common clean approach is that unvested shares return to the company, while vested shares stay with the founder.

Even with that simple rule, you still need to define the process. Can the company buy back shares. At what price. Over what time. Who approves it. If you do not define the process, you end up in a fight when stress is high.

A good startup lawyer can put this into clear language that investors understand.

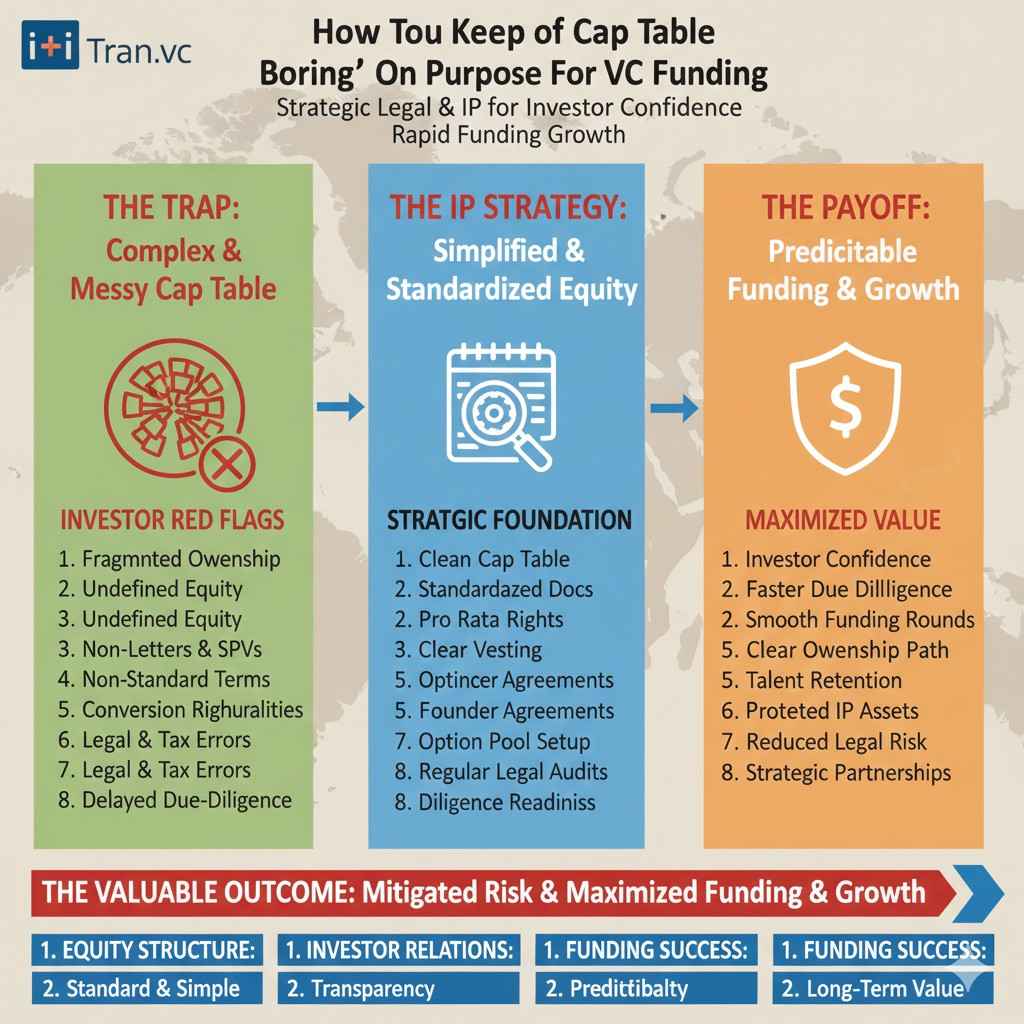

Keep the cap table “boring” on purpose

The best cap tables are boring. They are easy to read. They have standard terms. They have no surprises. Investors like boring cap tables because boring means predictable.

Founders sometimes try to add special side deals, handshake promises, or unusual voting setups. That often creates confusion and slows down a raise. Simple and standard wins most of the time.

If your company is building serious IP in robotics or AI, keeping ownership and IP clean is even more important. That is part of what Tran.vc helps founders do early, before the stakes get high. You can apply anytime at: https://www.tran.vc/apply-now-form/

Do the First 14 Days Right

Form the company in the right place for your plan

Where you form the company affects your taxes, investor comfort, and legal steps later. Many venture-backed startups use Delaware C-Corps, but the “right” answer depends on where the team is, where customers are, and what kind of raise you want later.

You do not need to overthink it, but you do need to avoid forming in a place that creates friction when you try to raise. A short call with a startup lawyer can save months later.

Authorize enough shares so you are not squeezed later

You want enough authorized shares so you can issue founder stock, set aside an option pool, and still have room for future rounds. The exact number is not magic, but the structure should be clean.

When you do it right, adding new hires and advisors is easy. When you do it wrong, you end up doing extra filings, approvals, and fixes when you should be building.

Issue founder stock early, while value is low

Founder stock is usually purchased at a very low price early on, because the company is just starting. This can be a major tax advantage when done correctly.

The key point is timing. If you wait until the company has traction, the value may be higher, and the tax outcomes can get worse. Early setup keeps things simple.

Handle the 83(b) filing with urgency

If you are in the U.S. and your founder stock is subject to vesting, the 83(b) election can be a critical step. The timeline is tight, often counted in days, not months.

Do not treat this as optional. Treat it like shipping a critical bug fix. You want your lawyer and your tax pro to confirm what applies to you, and you want to do it fast.

Lock down IP ownership from day one

Founder stock is only half the story. The other half is making sure the company owns the inventions, code, designs, and know-how that make the business real.

This means signing IP assignment agreements and making sure prior work is handled the right way. In deep tech, this is not paperwork for paperwork’s sake. It is what makes your company investable.

Tran.vc is built around this exact need: helping technical founders turn inventions into protected assets, so your company has a real moat early. If you want that kind of hands-on support, apply anytime at: https://www.tran.vc/apply-now-form/

Make your founder agreements easy to explain

A good test is simple. If an investor asks, “How is founder equity set up?” you should be able to answer in a few calm sentences.

You should be able to say the split, the vesting schedule, how IP is assigned, and that your documents are standard. When you can say that with confidence, you move faster in diligence and you look more credible.

That credibility matters, especially when you are competing for the attention of strong seed investors.

Build an Option Pool Without Surprises

Understand why the option pool exists

An option pool is a set of shares reserved for future team members. It is how you hire great people when you cannot pay big salaries yet.

In simple terms, it is a hiring budget made of ownership instead of cash. If you want strong engineers, product builders, and early operators, you usually need one.

The problem is not the option pool itself. The problem is when founders “discover” it late and feel like something was taken from them.

Decide the pool size early, before you negotiate anything else

Many startups set aside something like 10% to 20% for the option pool. The right number depends on your hiring plan for the next 12 to 24 months.

If you know you will hire five key people soon, you need room. If you will stay tiny and founder-led longer, you may need less.

What matters most is that the founders agree early, in writing, on what “fully diluted” ownership means. That phrase simply means you count the option pool as if it already exists, even if you have not granted options yet.

When founders ignore this, they can be shocked later. When founders plan for it, it feels normal and fair.

Avoid the “pool comes out of your shares” confusion

Here is the clean way to think about it.

If your company has only founders and no option pool, the founders own 100% of what exists. The moment you create an option pool, the pool must come from somewhere. In practice, it reduces the founders’ percentage ownership, because it creates a new bucket of shares reserved for others.

This is not a trick. It is simply math.

The problem happens when one founder thinks the pool is “free,” while the other understands that it affects everyone. That mismatch breaks trust.

A quick fix is to build a simple cap table model and review it together. You do not need a fancy spreadsheet. You only need to see the before and after.

Set clear rules for how options are granted

The option pool should not be a casual pile of shares that anyone can hand out. It needs rules.

Who approves option grants. What vesting schedule employees get. Whether there is a one-year cliff. What happens if someone leaves.

Most startups use four-year vesting with a one-year cliff for employees as well. That keeps it consistent and easier to explain. Consistency also helps when you later raise money, because investors expect to see standard patterns.

Think about hiring needs in your world

AI, robotics, and deep tech hiring can be different from a simple software startup. You may need rare skill sets. You may need PhDs, research engineers, or people with hardware experience.

That can change how much equity you need to offer to attract the right team. If you under-size your option pool, you can get stuck later when you need to hire, because increasing the pool during a financing can become a negotiation point.

If you want help thinking through equity in an IP-heavy company, Tran.vc can help you align your cap table with your hiring plan and your patent strategy. Apply anytime at: https://www.tran.vc/apply-now-form/

Use Advisor Equity Without Creating Future Pain

Treat advisors like a business tool, not a trophy

Advisors can help a lot, but only if they do real work that moves the company forward. The mistake many founders make is adding “big name” advisors who never show up.

Equity should be earned, not gifted for a logo on your website.

If you want an advisor, start with a clear outcome. A short list of intros. A review of your go-to-market plan. Help with a key hire. Guidance on a regulated market. If you cannot name the outcome, you probably do not need the advisor.

Keep advisor equity small and time-based

Advisor equity is usually much smaller than employee equity for a key hire, and far smaller than founder equity. The exact number depends on stage and involvement.

What matters most is that it vests over time, just like other equity. If an advisor stops helping after two calls, they should not keep a chunk forever.

A common pattern is monthly vesting over one or two years, sometimes with a short cliff. The cliff prevents giving equity to someone who does not engage at all.

Avoid giving advisors actual shares too early

Many founders think they should issue common stock to advisors. That can create paperwork and tax issues.

In many cases, options are cleaner than issuing stock to an advisor. This is not a universal rule, but it is a common approach because it can reduce early complexity.

The right move depends on your country, your company type, and your legal setup. But the principle is stable: keep it simple, trackable, and standard.

Put the relationship on paper, in plain terms

Handshakes create confusion. Confusion creates conflict.

Even a simple advisor agreement should state the role, the equity amount, the vesting schedule, and what is expected. It does not need to be long. It needs to be clear.

When you later raise money, investors will look at advisor grants. If they see large blocks of equity given away with no vesting, they will ask hard questions.

Be extra careful with “strategic advisors” in deep tech

In robotics and AI, you may speak with people from large companies, labs, or government-linked groups. That can be valuable, but it can also create IP and conflict-of-interest issues.

You do not want a situation where an advisor’s employer claims rights to what the advisor helped you build. You also do not want confidential information crossing lines you cannot control.

This is where clean IP rules matter. Tran.vc spends a lot of time helping founders avoid IP traps early, because those traps can kill deals later. If you are building real tech and want to protect it, apply anytime at: https://www.tran.vc/apply-now-form/