When you build a startup, you are not just building a product. You are also building a “box” that will hold the product, the team, the money, and the risk. That box is your company.

If you incorporate outside the United States, that box changes. Sometimes the change is small. Sometimes it changes everything about how venture capital works with you.

This article is about those changes—what VCs care about, what they worry about, and what you can do, step by step, so you do not get stuck later.

And if you want help building your IP the right way from day one, you can apply to Tran.vc anytime here: https://www.tran.vc/apply-now-form/

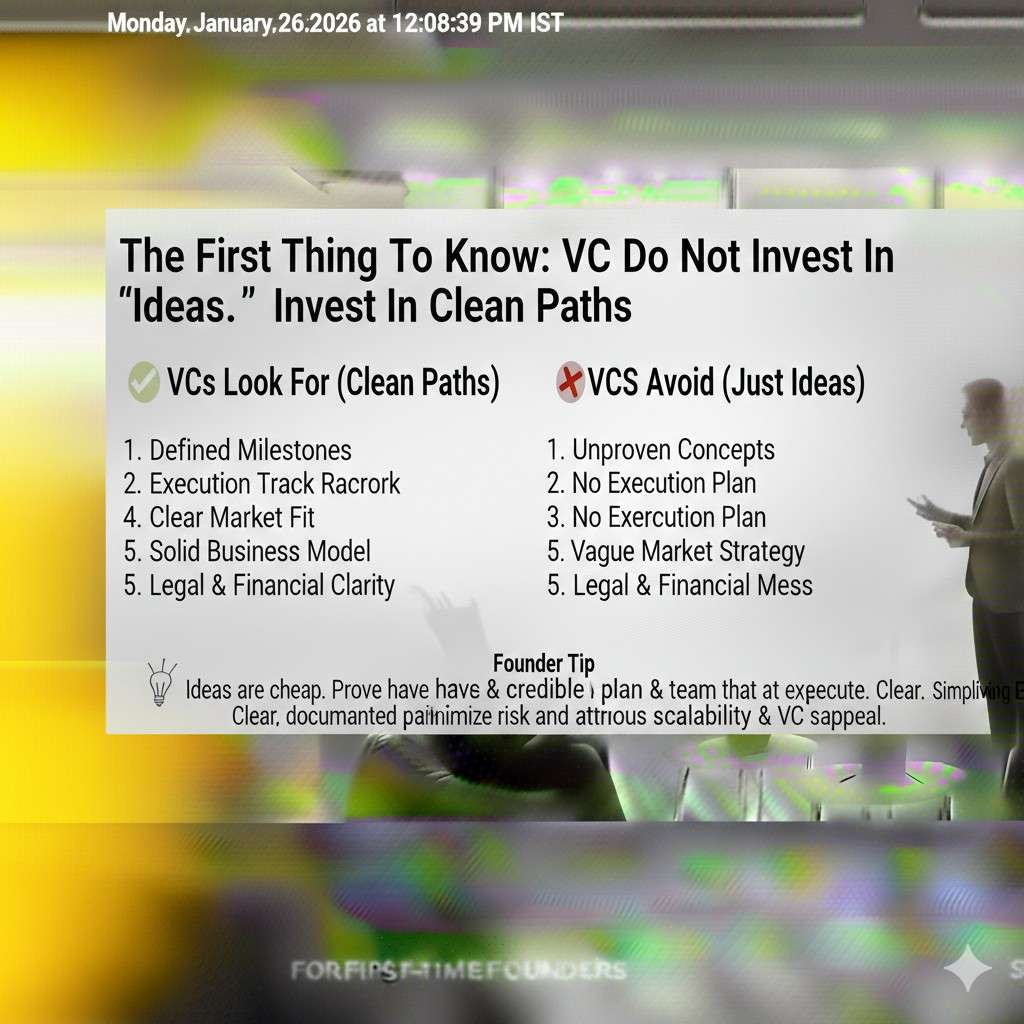

The first thing to know: VCs do not invest in “ideas.” They invest in clean paths.

Most technical founders think the hard part is the tech. The hard part is also the structure.

Venture capital is a system. It has rules, habits, and guardrails. The people inside that system can move fast when the path is clear. They slow down when the path is messy.

When you incorporate outside the US, a US VC will ask one main question, even if they do not say it out loud:

“Can I own this investment in a simple, safe way—and can I exit in a simple, safe way?”

Your country may be great for building. Your engineers may be excellent. Your customers may be there. But venture money has to travel through legal pipes. Those pipes are not equal in every place.

So the core change is not “Are you outside the US?” The core change is:

“How much extra work and extra risk does this add for the fund?”

If the answer is “very little,” many VCs will be open. If the answer is “a lot,” many will pass, even if they love the product.

Why many US VCs prefer a US parent company

This is not always about bias. It is often about friction.

A typical US venture fund is set up with its own rules. It has investors behind it (limited partners). Those investors have constraints. Some cannot hold certain foreign assets. Some have strict tax limits. Some have reporting rules that get painful when the investment is overseas.

So a VC might personally like your company, but the fund structure might make the deal hard.

A US company is familiar. Delaware is familiar. The standard VC deal docs are familiar. The court system is familiar. The stock option plans are familiar. The exit paths are familiar.

It is not that a foreign company cannot be great. It is that the VC is trained to avoid “surprises.” Foreign structures can create surprises.

That is why you will hear this phrase again and again in founder circles:

“Just flip to a Delaware C-Corp.”

That advice can be right. But it can also be expensive, slow, and sometimes unnecessary.

The right move depends on your plan, your country, your customers, your team, and your timeline.

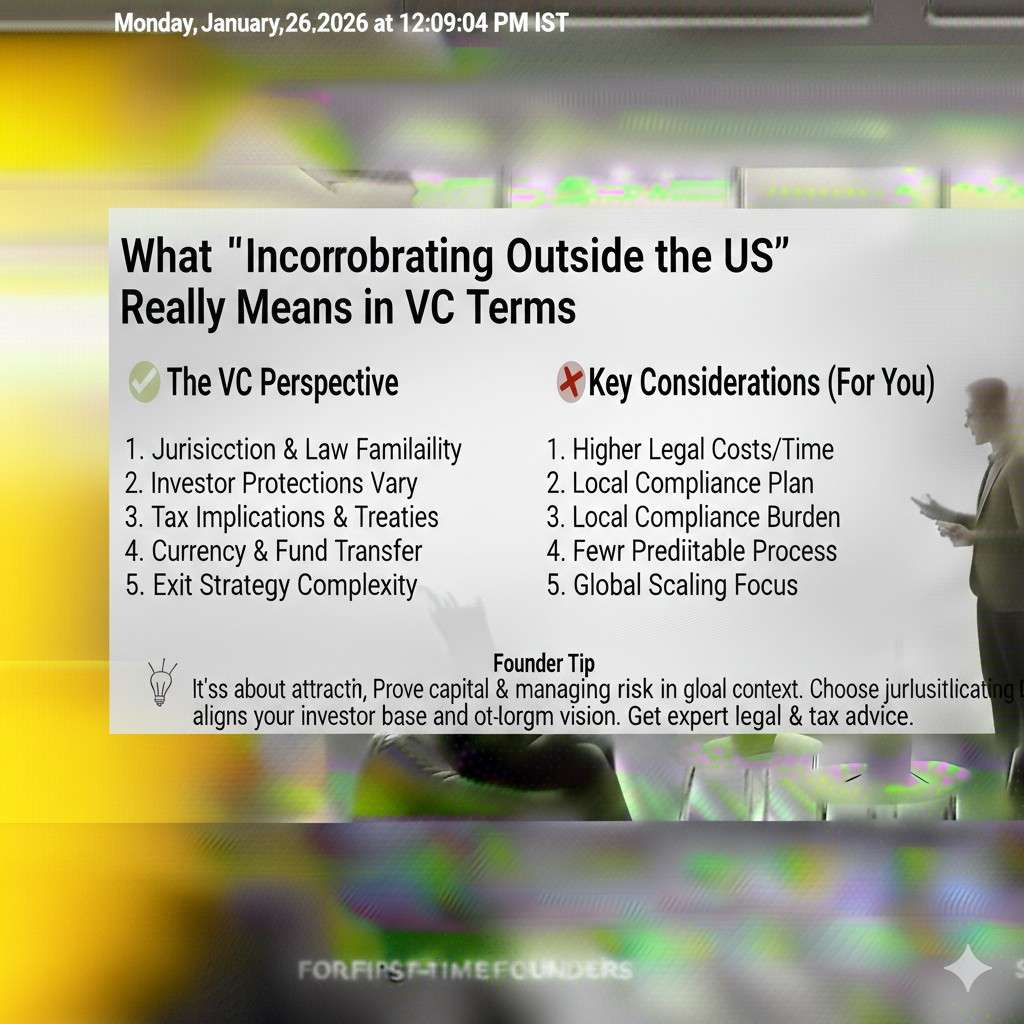

What “incorporating outside the US” really means in VC terms

Many founders think this is one decision: “US or not US.”

In VC terms, it is more like four decisions that stack on top of each other:

- Where the parent company sits

- Where the operating company sits

- Where the IP is owned

- Where the founders and key builders sit

You can be “outside the US” in one of these ways, or all four. Each one changes how a VC sees you.

A simple example:

- Parent company in Delaware

- Operating company in India

- IP owned by the Delaware parent

- Founders split between US and India

Many VCs can handle this. It is common.

A harder example:

- Parent company in India

- Operating company in India

- IP owned personally by founders

- Contractors across three countries, with loose contracts

Even if the tech is strong, a VC will worry about ownership, taxes, transfer rules, and future cleanup.

So when you talk to VCs, do not say only “We are incorporated in X.” Instead, be ready to explain the full picture in plain words:

“Here is where the parent sits. Here is where the team works. Here is who owns the IP. Here is how it is assigned.”

This one habit can save you months.

Tran.vc works with technical founders on exactly this kind of early structure and IP ownership so you do not have to redo it under pressure later. If you want to talk, apply here: https://www.tran.vc/apply-now-form/

The biggest VC fear: unclear IP ownership

If you remember only one section of this whole post, make it this one.

When you incorporate outside the US, the single most common deal killer is not revenue. It is not growth. It is not even competition.

It is: “Who owns the IP, and can they prove it?”

This gets worse across borders because:

- People work in different legal systems

- Contractor rules vary a lot

- Employee invention laws differ by country

- Government grants or university ties may create hidden rights

- IP transfers can trigger taxes or approvals in some places

A VC is not being dramatic here. IP is the asset. If the IP is “dirty,” the company is “dirty” to an investor.

Here are a few real-world patterns that cause problems:

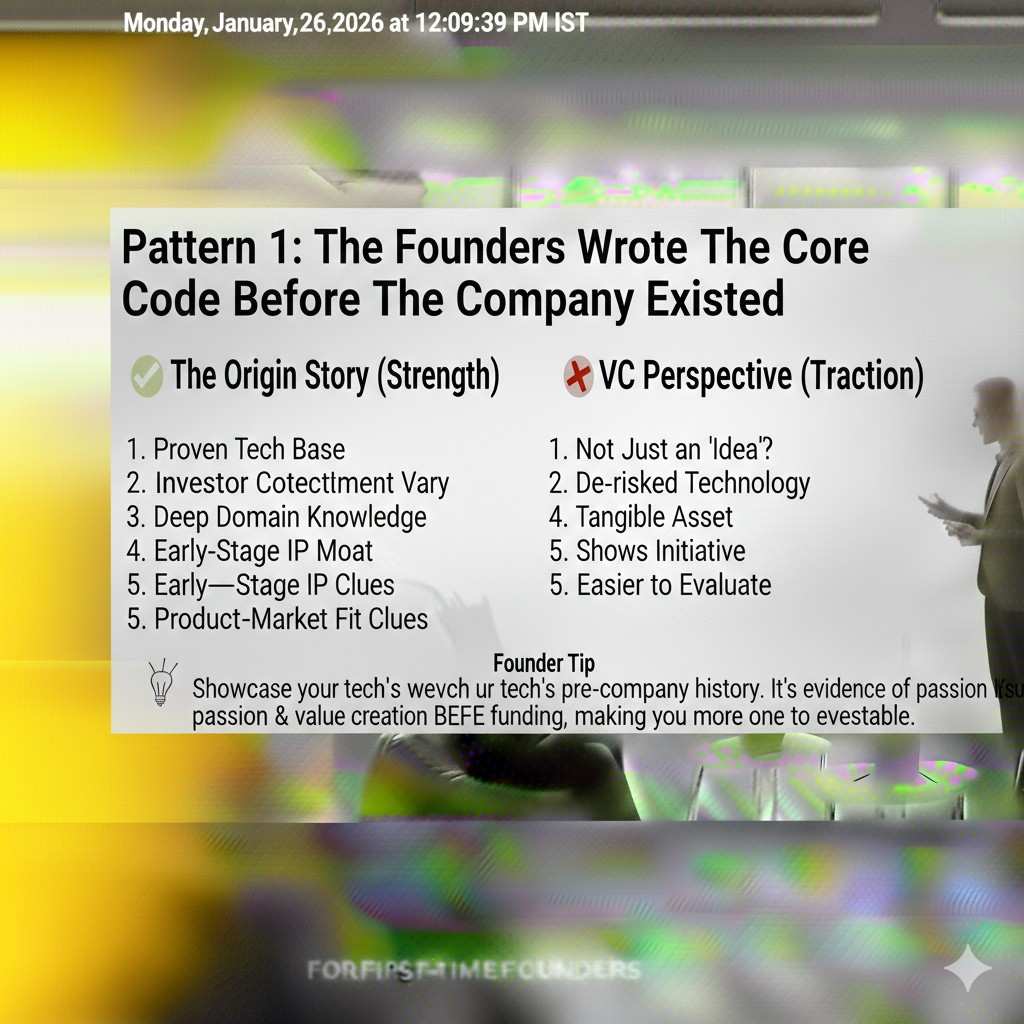

Pattern 1: The founders wrote the core code before the company existed

This is normal. Almost every founder does this. The issue is what happens next.

If the code was written before incorporation, then in many cases the code is personally owned by the founders. Later, the company must receive a clear assignment of that code and related inventions.

If you skip this, a VC will ask for it later, and now you are doing cleanup in the middle of fundraising.

Pattern 2: Early builders were “friends” or “part-time contractors”

A friendly relationship does not replace a signed agreement.

If someone wrote key parts of your stack, your model pipeline, your firmware, or your robotics control code, you need a clear invention assignment.

If you do not have it, that person can later claim rights, even if they never want to. A VC cannot take that risk.

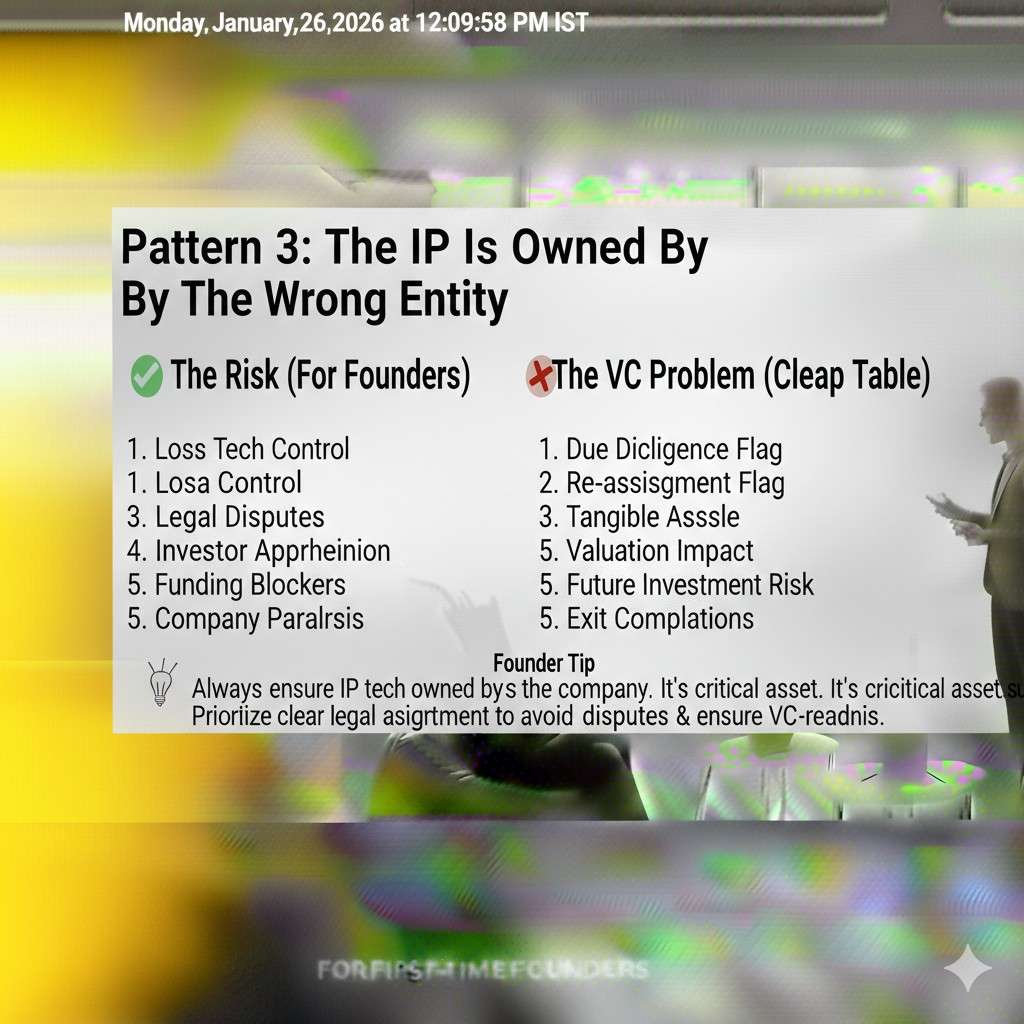

Pattern 3: The IP is owned by the wrong entity

Sometimes founders incorporate locally first, then later create a US parent.

If the IP stays in the local entity but the VC invests in the US entity, the VC may be investing in a shell that does not own the core asset.

This is a common reason VCs push for a “flip” or a restructuring.

Pattern 4: Open-source and data issues

Outside the US does not “cause” this, but cross-border teams sometimes have less consistent process.

If you used open-source with strict licenses, or trained on data without clear rights, the IP risk grows. VCs will ask.

The tactical move here is not complicated. It is just work you must do early.

You need to be able to show:

- who created what

- under what agreement

- and that the company owns it now

Tran.vc is built around helping founders do this early, with real patent and IP support—so later VC talks feel smooth, not scary. You can apply anytime here: https://www.tran.vc/apply-now-form/

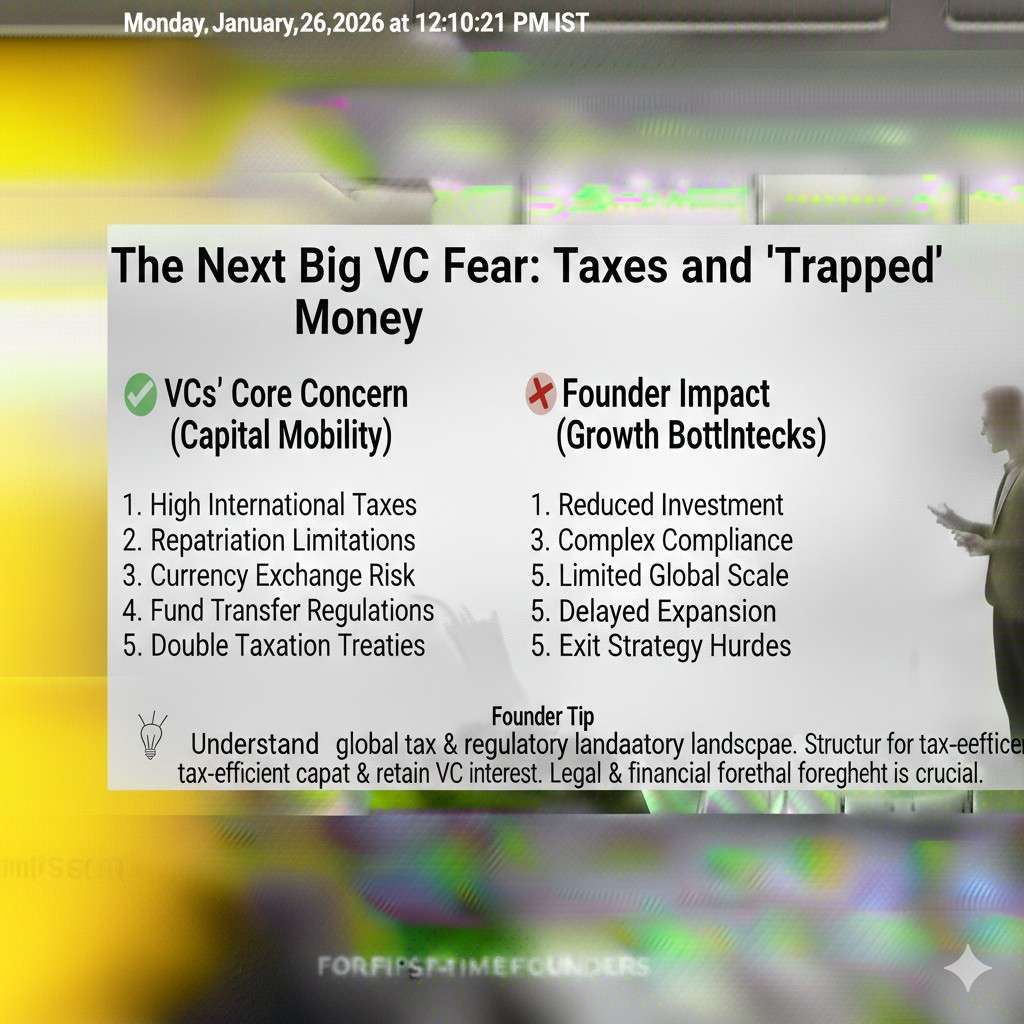

The next big VC fear: taxes and “trapped” money

VCs like simple flows.

When a VC invests, they want to know:

- how the money reaches the company

- how the company can move funds to run the business

- how profits (if any) flow

- how exit money flows back to investors

When your company is outside the US, these flows may face:

- withholding taxes on dividends or payments

- limits on moving money out

- rules about loans between parent and sub

- transfer pricing rules on cross-border services

- local taxes triggered by IP transfers

This does not mean “do not incorporate outside the US.”

It means: your structure needs to be designed, not guessed.

A common approach is a US parent with a foreign operating subsidiary. That can allow US VCs to invest in the parent while the team and operations sit where you want.

But even in this “common” setup, details matter a lot:

- Who invoices customers?

- Who employs staff?

- Who holds bank accounts?

- Where is the IP registered and owned?

- How does the sub pay the parent, or the parent pay the sub?

If you do this wrong, you can create “double tax” situations or compliance burdens that scare investors.

Most founders do not need to become tax experts. But you do need to avoid the worst trap:

Building a structure that is cheap today, but expensive to fix later.

A practical way to think about investor “fit”

Some founders take it personally when a VC says, “We only invest in Delaware.”

Do not take it personally. Think of it like this:

Different investors have different “maps.” They invest where their map works.

A seed fund in the US may have:

- deal docs designed for Delaware

- counsel that moves fast on Delaware deals

- LP rules that favor US entities

- a playbook for US exits

A local fund in your home country may have the reverse.

So you should choose your incorporation with your likely investor path in mind.

If you are building a company that will mostly raise from US investors, a US parent usually reduces friction.

If you are building a company that will mostly raise locally, staying local may be fine.

If you want both, then you plan for both from day one.

This is one reason Tran.vc exists. We help founders build leverage early—through IP and clean ownership—so they can choose investors, not beg them. Apply here if you want to explore that path: https://www.tran.vc/apply-now-form/

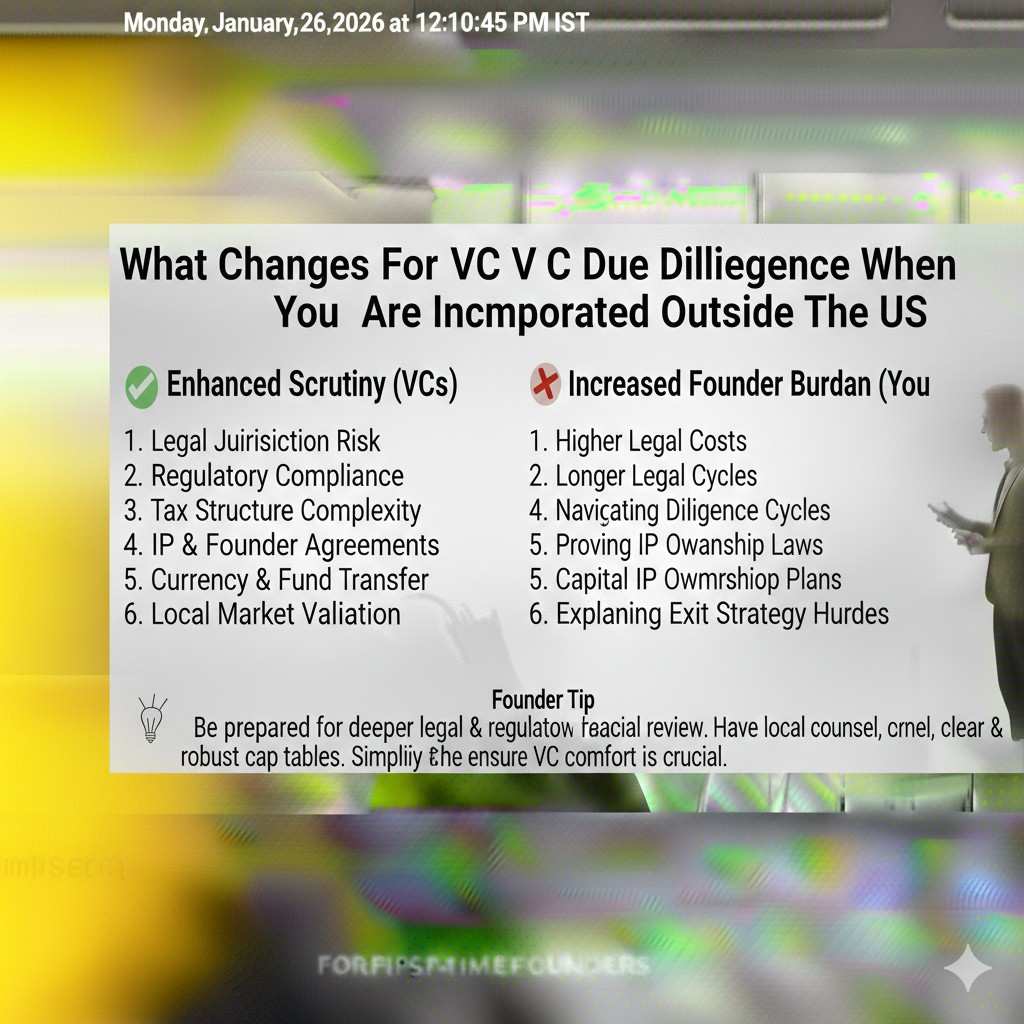

What changes for VC due diligence when you are incorporated outside the US

Due diligence is the “check before money.”

When you are a US Delaware C-Corp, due diligence is often routine. It still matters, but it is familiar.

When you are outside the US, diligence often gets deeper and slower. Not because the VC wants to be annoying, but because they must understand what they are buying.

Here are the areas that usually expand:

Corporate records

The VC will want to see your cap table, shareholder agreements, board approvals, and governance rules. In many countries, these look different from US standards.

If your country has required local filings, the VC will want proof that you are compliant.

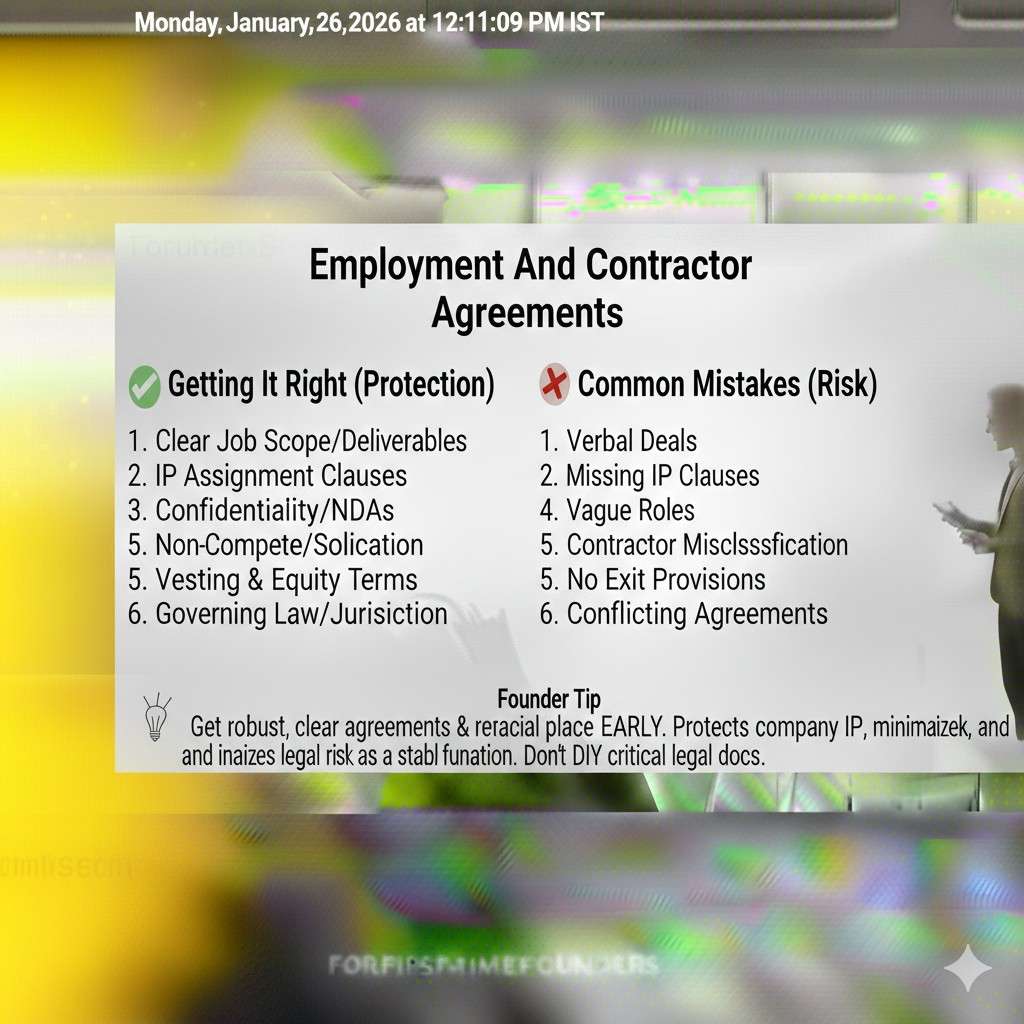

Employment and contractor agreements

They will check if your staff agreements include invention assignment and confidentiality rules that actually work under local law.

In some places, employee invention rights are strong. In others, they are weak. VCs want to know what you truly control.

IP chain of title

This is the “show me the path” topic again. It becomes extra important across borders.

Regulatory exposure

Some sectors have export controls, data laws, AI rules, robotics safety rules, or defense issues. If you are in a sensitive space, the VC may worry about cross-border limits.

Sanctions and restricted markets

Even if you are not doing anything wrong, a VC will avoid areas that could create future legal exposure.

The tactical takeaway is simple:

If you are outside the US, act like you will be audited.

Keep your documents organized. Keep signatures clean. Keep dates clear. Keep assignments clear.

This is not glamorous. But it is one of the best “fundraising multipliers” you can build.

The “flip” question: should you convert to a US parent?

This comes up constantly, so let’s speak plainly.

A “flip” is when you create a US parent company (often Delaware), and your current non-US company becomes a subsidiary under it, or is merged into it.

VCs like this because it gives them a US entity to invest in.

But flips have costs:

- legal fees

- tax risk

- time

- paperwork across countries

- potential approvals

- possible issues with early shareholders

Sometimes it is worth it. Sometimes it is not.

A useful decision lens is this:

If you are likely to raise a priced round from US VCs soon, the flip may become required anyway. Doing it earlier can reduce stress.

If you are still proving the product and you can raise locally, flipping too early might waste focus and money.

But here is the key: even if you do not flip now, you can still prepare for a clean flip later.

That means:

- keep your IP assignments clean

- avoid messy cap table moves

- avoid side agreements that conflict

- document founder contributions

- avoid giving away IP to contractors without assignments

- file patents in a way that supports future ownership changes

This is where IP strategy becomes more than “filing patents.” It becomes company design.

Tran.vc invests up to $50,000 in-kind in patent and IP services to help founders do this right early, before VC pressure shows up. Apply anytime: https://www.tran.vc/apply-now-form/

Why VCs Care So Much About Where You Incorporate

VC money comes with fixed rules

Venture funds are not just a person writing a check. A VC is managing a fund that already has its own legal and tax setup. That setup is built to move fast inside a system it understands. When your company sits outside that system, the VC has to slow down and test every step.

This is why “outside the US” can feel like a bigger issue than it is. It is not always about your country. It is about how much extra work the fund must do to stay compliant with its own investors and its own reporting duties.

“Extra steps” often kill deals more than “extra risk”

Many founders assume a VC says no because they think the company is risky. In practice, VCs often say no because the process will take too long. Early-stage deals move on momentum. If legal work turns into a long project, partners start to worry it will block other deals.

So the problem is often friction, not belief. Your job is to remove friction wherever you can, before you ask for money.

The VC exit path is part of the deal

A VC does not invest only to hold shares. They invest because they expect a future event where money returns to the fund. That exit might be an acquisition or an IPO, but the point is the same. They want a clear path that courts, contracts, and market norms already support.

When your company is incorporated outside the US, a US investor may see more unknowns in that exit path. Even if the risk is small, the unknown can still slow the deal.

If you want help making your structure and IP “easy to buy,” you can apply to Tran.vc anytime here: https://www.tran.vc/apply-now-form/

What Actually Changes When You Incorporate Outside the US

“Outside the US” is not one thing

Founders often describe this like a single choice: US or non-US. But investors see it as a set of connected choices. Where the parent company sits matters. Where the operations sit matters. Where the IP sits matters. And where the founders and key builders sit matters.

If you only say “we are incorporated in X,” you are leaving out the details that decide whether a deal feels simple or painful. The same country can look very different to a VC depending on the full setup.

Parent company location shapes the whole fundraising experience

In most venture deals, the investor wants to invest into the parent company. That is the entity that owns the shares, holds the cap table, and controls the major assets. If the parent is outside the US, many US VCs will have to do special work to invest, hold the shares, and report the holding.

A US parent company, often a Delaware C-Corp, removes most of that work. That is why many founders hear the same advice over and over. It is not magic. It is standardization.

Operating company location changes how money moves

The operating company is where the team is hired, where salaries are paid, and where day-to-day costs live. A US parent with a foreign operating sub is common because it can let VCs invest into a familiar US entity while the company builds where the talent and cost structure make sense.

But money movement between parent and sub must follow rules. If you do it casually, you can create tax issues that later force a restructure in the middle of fundraising.

IP ownership is the part founders underestimate

Many founders believe incorporation location is the main issue. In reality, IP ownership is often the true issue. If the IP is owned by a foreign entity while the VC invests in a US entity, the VC may feel they are buying into the wrong thing.

That is why IP needs to sit where the investors expect it, or at least be controlled in a way that is clear, signed, and provable.

Tran.vc helps technical founders set up clean IP ownership early, and back it with patents that investors respect. Apply here: https://www.tran.vc/apply-now-form/

How a Non-US Company Affects Common VC Deal Terms

Equity classes and standard docs may not match

US venture deals often rely on a known set of documents and share types. Preferred stock terms, option pools, protective provisions, and voting rules have patterns that lawyers can draft quickly. In some countries, the company law does not support the same patterns in the same way.

That does not mean it cannot be done. It means the VC’s counsel may need to rebuild parts of the deal from scratch. More time, more billable hours, and more chances for surprises.

Board control and approvals can work differently

VCs care about governance because it is how they protect the investment. Many countries have different rules on board powers, shareholder approvals, and director duties. Even if the rules are reasonable, they may not be familiar to US investors.

A VC may ask for stronger controls to feel safe. That can lead to tension if the founder expected a simpler governance model.

Employee option plans may need a new approach

In the US, it is common to use stock options as a key tool for hiring. In other countries, options can work differently, be taxed differently, or require special filings. If your company is not US-based, the VC may ask how you plan to recruit and retain talent, especially if you want US hires later.

A clear plan here reduces worry. A vague plan increases it, even if you have great talent today.

The Most Common Problem: IP That Is Not Clean

Why VCs obsess over IP across borders

IP is what makes your startup more than a team-for-hire. It is the asset that can be owned, defended, licensed, sold, and valued. When you incorporate outside the US, IP questions get sharper because different countries treat invention rights in different ways.

A VC is not trying to make your life hard. They are trying to avoid buying something they cannot truly control. If there is even one weak link in the chain of ownership, the whole deal can pause.

The “chain of title” is the story you must be able to tell

Chain of title means you can show the path of ownership from the person who created the invention to the company that owns it today. It sounds legal, but it is a simple idea. If you built the core technology before incorporation, you need signed documents showing you transferred it to the company.

If contractors helped, you need signed agreements showing the company owns what they created. If you used university work, you need proof the university has no claim. If you used grants, you need to confirm the grant terms do not pull ownership away.

The quiet risk: early work done “informally”

This is where many deep tech teams get hurt. Robotics and AI work often starts in research mode. People test, build, share code, and swap parts. That pace is great for learning, but it can create unclear ownership.

If a VC sees that your key pieces were built in a loose way with unclear assignments, they will assume a future dispute is possible. Even if a dispute is unlikely, “possible” is enough to slow the deal.

How patents change the VC conversation

A strong patent strategy does not only protect you from competitors. It also forces you to document inventors, dates, and ownership. That documentation often becomes part of your proof that the company truly owns the invention.

This is why Tran.vc invests up to $50,000 in-kind in patent and IP services, rather than just giving cash. In early-stage deep tech, clean IP is leverage. If you want to build that leverage early, apply here: https://www.tran.vc/apply-now-form/

Taxes and Cross-Border Cash Flow

VCs want to know how cash moves in real life

A VC is not only thinking about your next 12 months. They are thinking about what happens when you scale. If your team is outside the US, but your parent company is in the US, cash will move between entities.

That movement must have a reason and a structure. It can be payroll support, service fees, licensing fees, cost-sharing, or other models. The details matter because governments care about these flows and can audit them.

Withholding taxes and “leaky pipes”

When money crosses borders, taxes can be applied at the time of transfer. These are often called withholding taxes. Depending on the countries involved, these taxes can reduce how much money actually arrives.

If your structure causes cash to leak each time it moves, your runway shrinks. Investors do not like surprises in burn rate, especially surprises caused by preventable structure issues.

Transfer pricing becomes real as you grow

Transfer pricing is a set of rules that aims to make sure related companies do not move profits around in unfair ways. Early-stage founders often ignore this because it feels like a large-company problem.

But if you raise VC money and grow quickly, it stops being theoretical. If your parent and sub do not have a clean agreement for how they charge each other, you can face compliance work later that pulls focus from building.

The best time to plan this is before you need it

Founders often wait until they are in diligence to think about these topics. That is the worst time because you have less time, less leverage, and more stress.

A small amount of early planning can remove a large amount of later chaos. It also makes you look mature to investors, which builds trust fast.