If your startup has a team, a contractor, a lab partner, or a parent company in another country, you may already be doing “transfer pricing” without knowing it. Transfer pricing is simply the price you charge when one part of your business provides something to another part of your business across borders. That “something” can be software work, AI model training, product design, support, licensing, data access, or even the right to use your brand.

Founders often ignore this until a bank, investor, or tax advisor asks a hard question. Or until you open a second entity in another country and suddenly there is money moving between the two. Then it gets stressful. Not because transfer pricing is evil or complex by nature, but because it punishes late setups. If you wait, you may be forced to explain old choices with weak proof.

The good news is that early-stage transfer pricing can be simple, clean, and low-cost to maintain if you set it up early—before the amounts get big and before the structure gets messy. And if you are a deep tech startup building real IP (like robotics, AI, sensor tech, autonomy, vision systems, edge compute, or new control methods), early setup matters even more. Why? Because your “value” is often in the work your team does and the inventions you create. Those things cross borders easily, even when products do not.

Tran.vc helps technical founders turn inventions into protected assets early, through up to $50,000 of in-kind patent and IP services. If you are building in AI, robotics, or deep tech, you can apply anytime here: https://www.tran.vc/apply-now-form/

In this guide, we will start at the beginning: what transfer pricing really is for startups, why it shows up earlier than most people think, and how to set it up in a way that does not slow you down.

Transfer Pricing for Startups: The Early Setup

Why this matters earlier than you think

If your startup has people, partners, or entities in more than one country, transfer pricing is already close to your doorstep. Many founders assume it only shows up once they are large, profitable, or “global.” In real life, it can show up the moment you pay a contractor overseas, move engineering work into a second entity, or let one company in your group use the other company’s software.

Transfer pricing is not about playing games. It is about explaining, in a clear and fair way, how money moves inside your own setup when two related parties do business with each other. The “price” you choose becomes the story you tell to tax teams, auditors, and sometimes investors. When the story is missing, people assume the worst.

The early setup is your chance to keep it simple. You can build a clean pattern now, when the amounts are small and the structure is still flexible. Later, you will be grateful that you did not have to rebuild the plane while flying it.

Tran.vc works with technical founders who are building real inventions in AI, robotics, and deep tech. We invest up to $50,000 in in-kind patent and IP services, so your inventions become assets you can defend. If you are building something that matters, you can apply anytime: https://www.tran.vc/apply-now-form/

What Transfer Pricing Really Is

The simple definition

Transfer pricing is the price charged when one related company provides something to another related company. “Related” usually means the same founders, the same parent company, or common control. The “something” can be services, software, data, equipment, loans, or rights to use IP.

This is not limited to big companies. Startups create related-company transactions all the time, often without noticing. The moment you have two entities in two places, you have the chance that one is doing work for the other.

The goal is to set a price that looks like what two unrelated companies would agree to. Tax rules in many countries use this idea. It is often called the “arm’s length” principle. You do not need to memorize the term, but you do need to follow the spirit of it.

The practical meaning for a startup

For a startup, transfer pricing is less about fancy models and more about habits. You want a simple way to answer questions like, “Who did the work?” “Who owned the risk?” “Who paid the cost?” and “Who should earn the upside?” Those questions show up in taxes, but also in investor diligence.

If your structure is clean, your answers will be consistent. If your structure is messy, you may give different answers to different people, and that creates risk. The risk is not just tax risk. It can also create confusion over IP ownership, which can scare off buyers and investors.

Because Tran.vc focuses on building strong IP foundations early, we see this overlap all the time. The IP work you do today should match the legal and tax story of who created it, who paid for it, and who owns it. If you want help thinking through the IP side while you build, apply here: https://www.tran.vc/apply-now-form/

What transfer pricing is not

Transfer pricing is not the same thing as “moving money around to avoid tax.” Some people talk about it that way online, but that framing is not useful for a founder. Early-stage founders need a stable setup that can survive questions later.

Transfer pricing is also not only about profit. Even if you have no revenue and no profit, you may still need a method to price intercompany services. Many rules care about how costs are shared and whether the charges make sense.

It is also not only about documents. Documents matter, but the real core is your operating truth. If your documents say one thing and your team behaves another way, problems appear. The best setup is one where the paperwork matches what you already do.

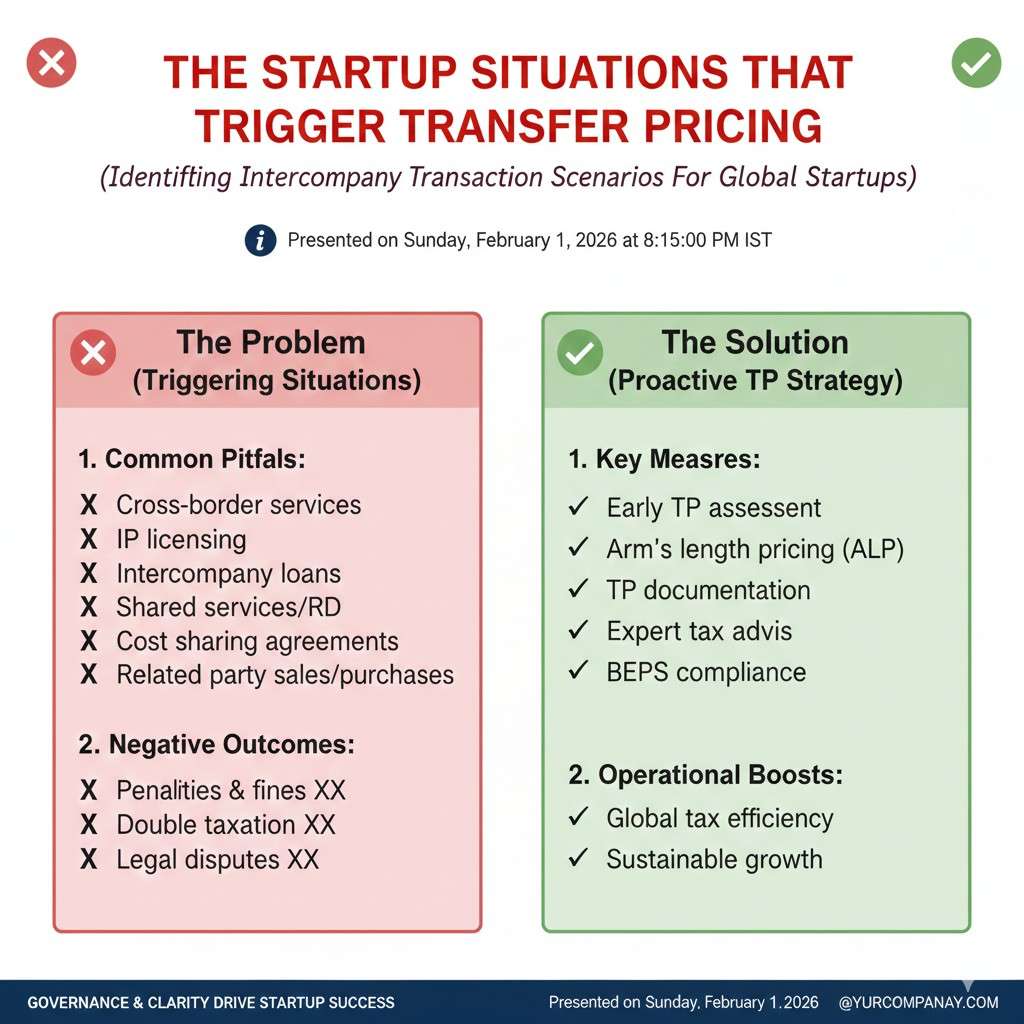

The Startup Situations That Trigger Transfer Pricing

The “two-entity” moment

The most common trigger is when you create a second company. This often happens when you incorporate a U.S. parent and keep an India engineering entity, or when you set up a subsidiary for hiring. It can also happen when founders incorporate in one place, then create another entity to access grants, customers, or local hiring.

From that point, work crosses a line. Engineers in one entity build a product sold by another entity. One entity pays cloud bills, the other entity uses the results. Even if you never send an invoice, value is moving.

This is when founders tend to say, “We will fix it later.” That is the costly mistake. Later, you might have two years of mixed expenses with no clear pattern. Cleaning that up is harder than setting it up right at the start.

Offshore contractors and related parties

A second trigger is when contractors are overseas, especially when they are tied to founders, early team members, or related companies. If you are paying a team that also works for a sister company, or you route payments through a related entity, you may be creating related-party flows.

Even if you pay the contractor directly, the question becomes, “Which company benefits from the work?” If the contract is with one entity but the work builds the other entity’s product, you are creating a mismatch. Mismatches are where audits and disputes begin.

A clean early step is to align the contract, the invoices, and the “benefit” in the same direction. When those three point the same way, the story stays simple.

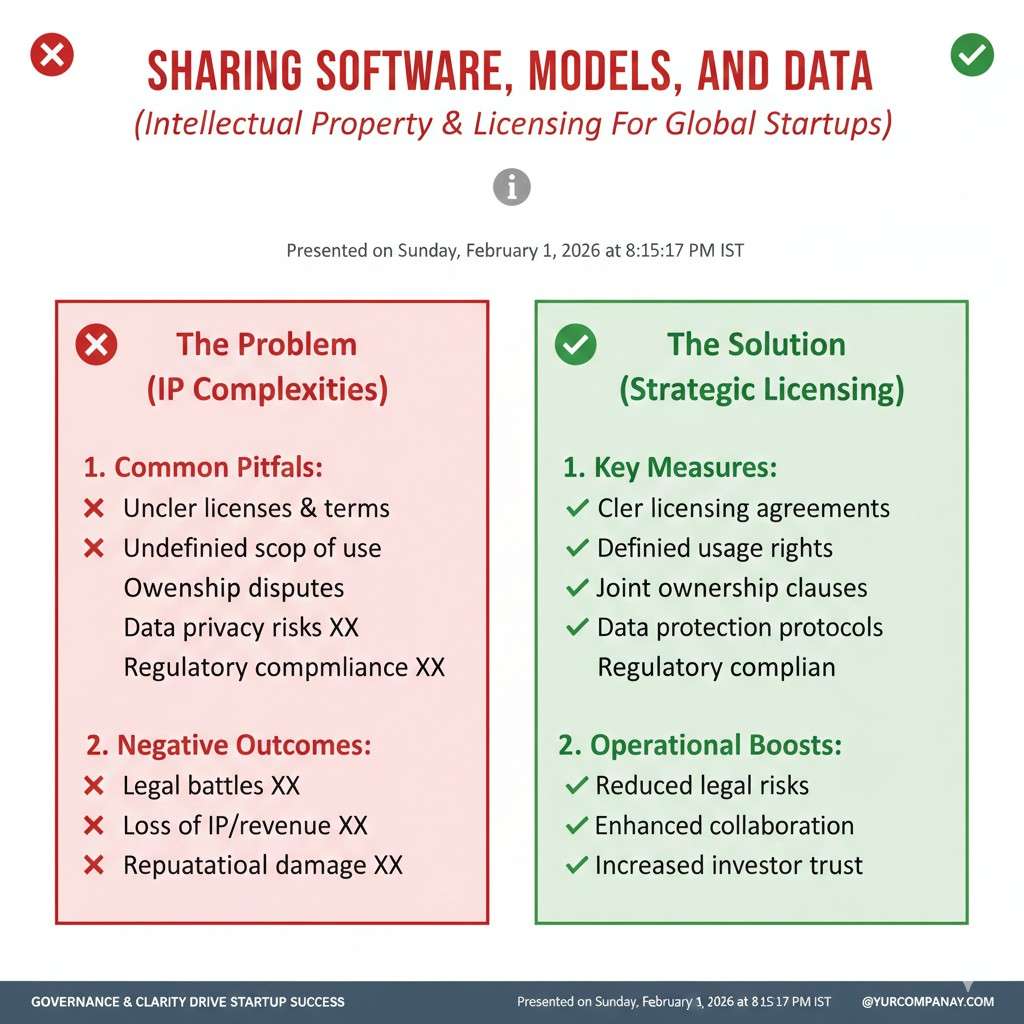

Sharing software, models, and data

Deep tech teams share assets all the time. One entity may host the code repo. Another entity may run training jobs. A third entity may do labeling. If those entities are related, the sharing is not “free” from a tax view, even if it feels free operationally.

This gets more intense with AI. Your model weights, training pipelines, prompts, data sets, and evaluation tools can be core assets. If one entity builds them and another entity sells access, the “who owns what” question becomes real fast.

Founders often think, “We are one team, so it does not matter.” But law does not see it that way. Entities are separate. If you want the upside in one place, you need to plan how the value is created and paid for.

Cross-border hiring and seconded staff

Sometimes the startup hires people in one country but they “report” to another country leader, work on the other entity’s roadmap, and attend the other entity’s meetings. The HR contract might sit in one entity, but day-to-day control sits elsewhere.

This is a common pattern when a U.S. company uses an India entity as an employer for payroll ease. It can be fine, but you need to structure the charges and responsibilities in a clean way.

If you do not, you can end up with a situation where a tax authority says, “This looks like a hidden permanent establishment” or “This looks like the wrong profit split.” Those are big issues, and they start with small habits.

The Core Principle: Match Work, Risk, and Reward

Who actually does the work

Transfer pricing starts with a simple map. Who is building the product? Who is doing research? Who is doing customer work? Who is managing vendors? You do not need a massive chart. You need a truthful picture.

In many startups, most of the work is in one place, even if the company is incorporated elsewhere. That is normal. The key is to avoid pretending the work happens in the place you wish it did. Tax teams can tell the difference when they look at payroll, Slack logs, Git commits, and contracts.

When you accept where the work is done, you can price it in a fair way. That is usually safer than trying to force a story that does not match reality.

Who controls the decisions and takes the risk

Risk is not just legal risk. In transfer pricing, risk often means business risk. Who decides what to build? Who decides when to pivot? Who chooses the vendors and signs the big contracts? Who carries customer liability?

A company that controls key decisions is often seen as taking more risk. That can justify more reward. But you need consistency. If the U.S. entity claims it takes all risk, but the India entity makes all product decisions, the story breaks.

This is why founders should design decision-making early. It is not about politics. It is about clarity. Clarity keeps you out of fights later.

Who owns and funds the IP

This is where startups often slip. If one entity funds R&D and another entity claims to own the output, you need a legal and financial bridge between those facts. Sometimes that bridge is a service agreement. Sometimes it is a cost-sharing setup. Sometimes it is a license.

The right choice depends on your stage and goals. But the key idea is simple: the entity that wants to own the valuable IP should have a strong reason for owning it, and the paperwork and payments should support that reason.

Tran.vc helps early founders turn inventions into protected assets and patents, which also forces a clear view of ownership and invention flow. If you want to build an IP foundation that is clean for investors later, apply anytime: https://www.tran.vc/apply-now-form/

The Easiest “Early-Stage” Transfer Pricing Setup

Start with the simplest transaction type

In the earliest stage, the cleanest setup is often a service arrangement. One entity provides development or support services to the other, and charges cost plus a small markup. This can be easier to defend than complex profit splits when you have no revenue.

This approach fits many startups that have a parent company and a service company. The service company hires engineers and performs R&D support. The parent company owns the product plan, raises money, and signs customers. The service company bills for its costs plus a margin.

This is not the only valid setup, but it is common because it is easy to track. It also creates a routine: monthly cost collection, monthly invoice, and clean books.

Keep the method stable, not “perfect”

Founders often chase a perfect markup number, like it is a magic key. The truth is that early stage is about reasonable, not perfect. A small markup that is supported by basic comparables and consistent charging is often better than a fancy number with messy execution.

Stability is your friend. A stable method creates a history. History is what gives you credibility later. If you change the method every quarter, you signal that it was not grounded.

Your goal is not to optimize tax. Your goal is to reduce surprises. Investors and acquirers hate surprises more than they hate ordinary costs.

Put it on rails with simple monthly steps

The real win is operational. Set a monthly rhythm where the service entity tracks its direct costs, adds the agreed markup, invoices the other entity, and gets paid. Even if cash is tight, recording the payable cleanly matters.

If you cannot pay every month, you can still book the charge and settle later, but you must be consistent and document why. Random settlements without a pattern look strange.

A simple spreadsheet and a recurring calendar reminder can be enough in the first year. The key is that someone owns the process and does it the same way each month.

Early Documents That Make a Big Difference

A basic intercompany agreement

You do not need a 60-page legal novel in the beginning. You do need a clear agreement that states what services are provided, how costs are calculated, when invoices are issued, and when payments are due.

This agreement should match how you actually work. If it says “marketing services” but your team is building robotics firmware, it will not help you. If it says “R&D services” and the work is R&D, it supports your story.

A good agreement also states who owns what output. If the service entity creates code or inventions while providing services, the agreement should address IP assignment or ownership in plain terms.

A short transfer pricing memo

A memo is a simple note that explains your method and why it is reasonable. It can be short at the start, but it should cover the basics: the entities involved, what each one does, what is being charged, and how the price is set.

This memo is not just for tax. It becomes part of your institutional memory. When your first finance hire joins, they will rely on it. When an investor asks questions, it helps you answer cleanly.

The memo can grow later as you scale. The early version is still valuable because it shows you cared from day one.

Clean IP assignments and invention capture

If you are building AI or robotics, your IP is often the main asset. That makes invention capture and assignments critical. You want invention assignments from employees and contractors, and you want them aligned with the entity that should own the IP.

If the “wrong” entity owns early inventions because of sloppy contracts, fixing it later can be painful. Sometimes it is still fixable, but it can delay funding or deals.

Tran.vc is built for this exact moment: turning your technical work into real, defensible assets early, with expert patent and IP services. If you want to set this up the right way while you build, apply here: https://www.tran.vc/apply-now-form/

Choosing the Right Early Transfer Pricing Structure

Why “one size fits all” fails for startups

The biggest mistake founders make is copying a template from another company without checking if it fits how their own team works. Two startups can look similar on the surface and still need very different transfer pricing setups. One might have all engineering in India and sales in the U.S. Another might have R&D split across two labs, with patents filed from day one. The money flows may look the same, but the value creation is not the same.

A workable structure is the one that matches your reality today and does not block your reality tomorrow. That means you choose a model you can run every month with your current team, and that still makes sense when you add revenue, new hires, and new countries. When a structure is too complex early, founders stop following it. When founders stop following it, the structure becomes useless.

In early stage, your goal is not to squeeze every possible tax benefit. Your goal is to keep your company safe, credible, and investable. You want a setup that looks reasonable to a tax authority and also looks clean to an investor who has seen deals fall apart due to cross-border mess.

The three models you will hear about

In startup transfer pricing, people usually circle around three main approaches. The first is a simple service model where one entity charges another for work done. The second is a license model where one entity owns IP and licenses it to the other. The third is a cost-sharing style setup where two entities share R&D costs and share rights. These can be combined, but early on it is wise to avoid piling on complexity.

Each model answers the same question in a different way: “Where is value built, and how do we pay for it?” The right answer depends on what you are building and where you are building it. A robotics startup creating new control methods and filing patents may want a different approach than an AI SaaS startup shipping fast and iterating weekly.

The key is to understand what each model is trying to accomplish, what it asks you to track, and what it implies about who owns the important assets.

The Service Model

What it means in plain words

The service model says: one company in the group provides services, and the other company pays for those services. It is the closest thing to everyday business behavior. If the India entity provides engineering services to the U.S. entity, it charges for the costs of that team plus a reasonable margin. The invoice is recorded, the money moves, and the books stay clear.

For early-stage startups, this model is often the easiest to operate because it matches how founders already think. A team works. That work costs money. Someone should pay for it. When the work is across borders, the payment needs a method.

This approach also works well when the entity doing the work is not supposed to own the long-term upside of the product. If your U.S. entity is meant to own the product and raise money, and the offshore entity is meant to be a delivery arm, the service model can fit.

What you must get right

The service model breaks down when you treat it as “just paperwork.” Tax teams will look at whether the service company is really acting like a service company. Does it have the right people? Does it take direction? Does it bear limited risk? Does it avoid making final product decisions? If the answers do not line up, the service model can look fake.

To make it real, you need a few clear habits. The service company should have job descriptions and contracts that match a service role. It should have a manager who coordinates deliverables. It should have a clean process for collecting costs. And it should invoice in a consistent way.

You also need to be careful about what the services are called. “Software development and R&D support” can be accurate for many deep tech teams. “Back office support” is often not accurate if the team is building core product code. Accuracy matters because the label becomes part of the story later.

How the “markup” should be handled

People get nervous about the markup. The markup is simply the service provider’s profit on top of its cost. In practice, early-stage startups often use a modest markup that is supported by basic market references. The exact number depends on the country, the function, and the risk profile, but the deeper point is consistency.

If you pick a markup and then forget to invoice for three quarters, the markup does not matter. If you invoice every month with a consistent method, the method becomes credible. That credibility is what you are buying. When the numbers grow, you can refine the support behind the markup.

A strong early move is to document why you chose your approach in a short memo and then follow it without drama. That memo can be updated later, but the early version still proves that you acted with intent.

The License Model

What it means in plain words

The license model says: one company owns IP, and the other company pays to use it. This can include patents, source code, model weights, training pipelines, industrial design, schematics, and even know-how. The “price” is a royalty or a license fee.

Founders like this model because it feels aligned with the idea of protecting IP and concentrating ownership in one place. If the U.S. entity owns the IP, it can license it to an operating entity elsewhere. That can feel clean.

But it can also be dangerous early if it does not match how the IP is being created. If most R&D work happens outside the IP-owning entity, you must be extra careful about how rights move and how costs are funded. Otherwise, you can end up with a legal claim that the wrong entity truly created the value.

When it fits well

The license model often fits when you truly have a clear IP owner that directs and funds the R&D, and other entities are mainly implementing, selling, or supporting. It can also fit when you acquire IP or spin it out from a lab and place it in one entity, then license it for product use.

It is also common when a group wants to keep core assets in a parent company and let subsidiaries operate locally. That way, the parent retains the asset even if a local subsidiary faces trouble.

For deep tech founders, this can matter because patents and invention ownership are often central to fundraising and long-term defensibility. If the IP owner is clear and credible, your story becomes easier to tell.

The early-stage trap with royalties

The problem is that royalties are hard to price when there is no revenue. Many startups have no steady sales in the beginning, which makes a revenue-based royalty awkward. Some teams pick an arbitrary percentage and hope nobody asks questions. That can create trouble later.

You can still use a license model early, but you must set it up in a way that is grounded. Sometimes that means a small fixed fee. Sometimes it means a deferred royalty that only starts after a revenue trigger. The choice depends on your facts and must be structured carefully with professional advice.

Also, a license model is not a substitute for clean invention assignments. If the wrong entity’s contractors are writing the code and signing contracts that assign invention rights to that entity, a license agreement on top does not magically fix it.

Tran.vc’s IP-first approach helps founders avoid this kind of mismatch early. When patents and IP services are handled with proper strategy, it becomes much easier to align transfer pricing with real ownership. If you want support on building that foundation, apply anytime: https://www.tran.vc/apply-now-form/

The Cost-Sharing Style Setup

What it means in plain words

A cost-sharing style setup says: two related companies share the costs of R&D, and in return they share rights to the resulting IP or benefits. This is often used by larger firms, but startups hear about it and assume it is the “advanced” option.

In theory, it sounds fair. If a U.S. parent and a foreign subsidiary both benefit from the R&D, they both pay a share. In practice, it can be hard to run because it requires careful tracking, valuations, and ongoing adjustments.

For early-stage teams, this can become a distraction. It demands time and accounting maturity that many startups do not have in the first year or two.

When it may be worth it

There are cases where it makes sense even early. If you have two real operating centers with major teams, and both are making key decisions and funding key work, cost sharing can reflect reality better than a simple service model.

It can also come up when you have strong reasons to give certain rights to different entities for local markets. For example, one entity may need rights to operate locally, sign government customers, or meet regulatory needs.

Still, if you go this route, you should do it with expert support and strong discipline. A “half-done” cost-sharing setup is worse than not doing it at all because it signals intent but fails on execution.

Why founders often regret choosing it too soon

The regret is not that it is wrong in principle. The regret is that it becomes heavy. It requires ongoing studies, periodic true-ups, and deep analysis. Early founders are usually trying to ship product, hire, and raise. The system can become another “project” that nobody owns, which leads to gaps and inconsistencies.

If you want to keep your startup fast and still safe, a service model is often the best first step. You can evolve later. You do not need to start with the hardest version of the game.

How to Choose Between These Models

Start with your future funding and exit story

Even at pre-seed, you should think about what a future investor expects to see. Many investors want a clean parent company that owns the core IP, with clear contracts that show inventions flow into that parent. They want to know the startup can protect its moat.

If your structure makes IP ownership unclear, you may pay for it later with delays, extra legal work, or reduced valuation. That is why transfer pricing and IP strategy are linked. They are different topics, but they touch the same core facts.

A good early question is: “When we file patents and capture inventions, which entity is the intended owner, and does our transfer pricing structure support that?” If the answer is unclear, fix it now while it is easier.

Match the model to where decisions happen

If product and strategy decisions happen in one entity, and execution happens in another, a service model can fit. If ownership and strategic control are genuinely centralized, licensing can fit. If decisions and funding are truly shared across two real centers, cost sharing may fit.

Founders sometimes try to claim centralized control because it sounds better, but their actual behavior shows shared decision-making. Your best defense is to be honest and then structure accordingly. It is safer to reflect reality than to fight it.

Avoid mixing models unless you have a strong reason

A common early mess is when founders set up a service model, then also add a license agreement, then also move costs around informally. That creates a story with too many moving parts. The more moving parts, the harder it is to explain.

Early on, the best setup is often the simplest setup you can actually follow. Complexity does not impress the people who matter. Clean execution impresses them.