Most founders wait too long to set up vesting. They think it is “legal stuff” they can fix later. Investors see it very differently. To them, vesting is not paperwork. It is proof that your team is stable, fair, and serious. It shows you understand how to build a company that can survive hard months, not just good weeks.

If you are building robotics, AI, or deep tech, this matters even more. Your work is hard. It takes time. It often takes years before the market fully “gets it.” Investors know that. So when they look at your cap table, they want to see a clean, simple vesting plan that protects the company if someone leaves early. If they do not see it, they worry you will get stuck later—when you should be building.

At Tran.vc, we see this pattern a lot: smart technical teams move fast on product, but they delay the boring parts. Then, right before fundraising, they rush to clean things up. Vesting is one of the first things investors check, because it is one of the first places early-stage companies break. And once it breaks, it creates tension, slows hiring, and makes funding harder.

This article will walk you through vesting in plain language. You will learn what investors expect, what mistakes to avoid, how to set it up in a founder-friendly way, and how to use it to build trust with future teammates and seed investors. And if you want hands-on help building a fundable setup—plus IP and patent strategy that makes your company stronger—you can apply anytime at https://www.tran.vc/apply-now-form/.

Why Investors Care So Much About Vesting

Vesting is a trust test, not a legal test

Investors back teams more than ideas. Even in v, where the tech is complex, the real bet is still on people. Vesting helps an investor believe the people who own the company will still be there when things get hard.

If a founder owns a big chunk on day one with no vesting, an investor sees risk. They think, “What happens if this person leaves in six months?” The company could lose a key builder, but that person could still keep a large piece of the company. That is not fair to the founders who stay, and it is not good for future hires either.

A simple vesting plan tells investors you have planned for real life. Co-founders fall out. Family needs happen. Health changes happen. Sometimes a person just is not a fit. Vesting is how you protect the company from turning into a mess when those things happen.

Vesting shows you can run a clean company

Many founders assume investors only care about product, revenue, and traction. Those things matter, but investors also look for signs that you can handle basics. Vesting is one of the basics.

When vesting is missing, it creates hard questions later. Investors wonder what else is missing. They start to expect more surprises. That can slow a deal, lower confidence, and create extra legal work right when you need speed.

The goal is not to impress anyone with fancy documents. The goal is to reduce doubt. A clean vesting setup removes a big source of doubt in a very simple way.

In AI and robotics, the time horizon is longer

If you are building a SaaS app, you may hit product-market fit faster. In robotics and AI, you may need longer cycles. You might need more testing, more data, more training runs, more safety work, or more hardware revisions.

Investors know that long cycles can strain teams. They want to see that the cap table will stay fair across time. Vesting helps make sure the people who carry the company through the long cycle are the ones who earn the upside.

If you plan to raise capital, vesting is not optional. It is part of the basic setup investors expect, like having a company formed and shares issued correctly.

What Vesting Really Means in Simple Words

Vesting is “earning your shares over time”

Vesting means you do not fully “own” all your shares on day one, even if they are in your name. Instead, you earn them step by step as you keep working for the company.

This does not mean you are not a real founder. It means the company is built to be fair. It also means your co-founder cannot walk away early with a large stake while you keep grinding for years.

It is helpful to think of vesting as a seatbelt. You hope you never need it. But if something goes wrong, it prevents damage that can break the company.

The company can “buy back” unvested shares if someone leaves

A common setup is that if a founder leaves, the company has the right to buy back the shares that are not vested yet. Usually this buyback is at the same low price the founder paid at the start.

That sounds harsh at first, but it is actually what keeps things fair. The company should not lose major ownership to someone who is no longer building it. The company needs room to reward the people who stay, and to hire new talent to replace what was lost.

This is also why vesting helps your future team. New hires will not want to join if most of the company is locked up with people who left years ago.

Vesting can cover founders, early employees, and advisors

Most people hear about vesting for employees, like stock options. But investors also expect founders to have vesting. That is where many teams slip up.

Advisors can also be put on vesting, especially if they are getting meaningful equity. If they stop helping, the company should not keep paying in equity forever. Vesting protects you from “dead equity” that does not create value.

A healthy rule is simple: equity should match work. Vesting is how you keep that match over time.

The Standard Vesting Setup Investors Expect

The common pattern: four years with a one-year cliff

The most common founder vesting setup investors expect is four years total, with a one-year cliff. This is common because it balances fairness with commitment.

The “four years” part means shares vest over four years. The “one-year cliff” means nothing vests for the first year. After one year, a chunk vests all at once, and then the rest vests monthly or quarterly.

A simple example is this: if you have 1,000,000 founder shares on a four-year plan with a one-year cliff, then after one year you might vest 25%, which is 250,000 shares. After that, the remaining 750,000 shares vest slowly over the next three years.

Why the one-year cliff exists

The cliff is there to protect the company from very early exits. If someone leaves after three months, they should not keep a meaningful piece of the company. The cliff makes that clear without a fight.

This also protects relationships. Without a cliff, you can end up arguing over tiny time periods. With a cliff, the rule is simple. Stay a year, earn the first chunk. Leave early, keep almost nothing.

Investors like cliffs because they reduce drama. They want to know that if a founder quits early, the company can recover and keep moving.

Why monthly vesting after the cliff is common

After the cliff, monthly vesting is common because it is smooth and easy. It avoids big jumps that can feel unfair. It also makes it easier to handle a departure at any point.

This matters when the company changes fast. Startups can go through big shifts. If someone leaves 18 months in, monthly vesting creates a clean number of vested shares, instead of a confusing guess.

A clean structure makes future deals easier too. Lawyers, investors, and acquirers all prefer simple, standard patterns.

Where Founders Often Get Vesting Wrong

Mistake one: no vesting at all

This happens more than you might think. Two friends start a company, split equity 50/50, and never set vesting. They think trust is enough.

Then one person burns out or gets a job offer. They leave. Now the remaining founder is building a company where half the ownership sits with a person who is gone. That makes raising money hard, hiring hard, and motivation hard.

Investors will often demand a fix, but fixing it later is painful. It can turn into a negotiation, and that negotiation can break relationships. It is far better to set vesting while everyone is still aligned.

Mistake two: uneven rules between co-founders

Sometimes one founder insists they should not vest, but the other founder should. This almost always creates long-term resentment.

Even if one person contributed more early, that can be handled with a different split, or with a clear bonus, or with role-based compensation. But vesting should be consistent unless there is a very clear reason.

Investors also dislike uneven rules. They worry it signals power imbalance, hidden conflict, or future drama. They prefer a team that has agreed on fair terms from the start.

Mistake three: vesting that is too short or too weird

Some teams try to do vesting in a “custom” way, like six months total, or complicated performance triggers. They do this to feel in control.

The problem is that investors do not want experiments on core company structure. If your vesting is strange, they will ask why. If your answer is not strong, they may push you to change it.

Standard vesting exists because it works. It is easy to explain. It is easy to accept. It saves time in fundraising. This is one place where being normal is a feature.

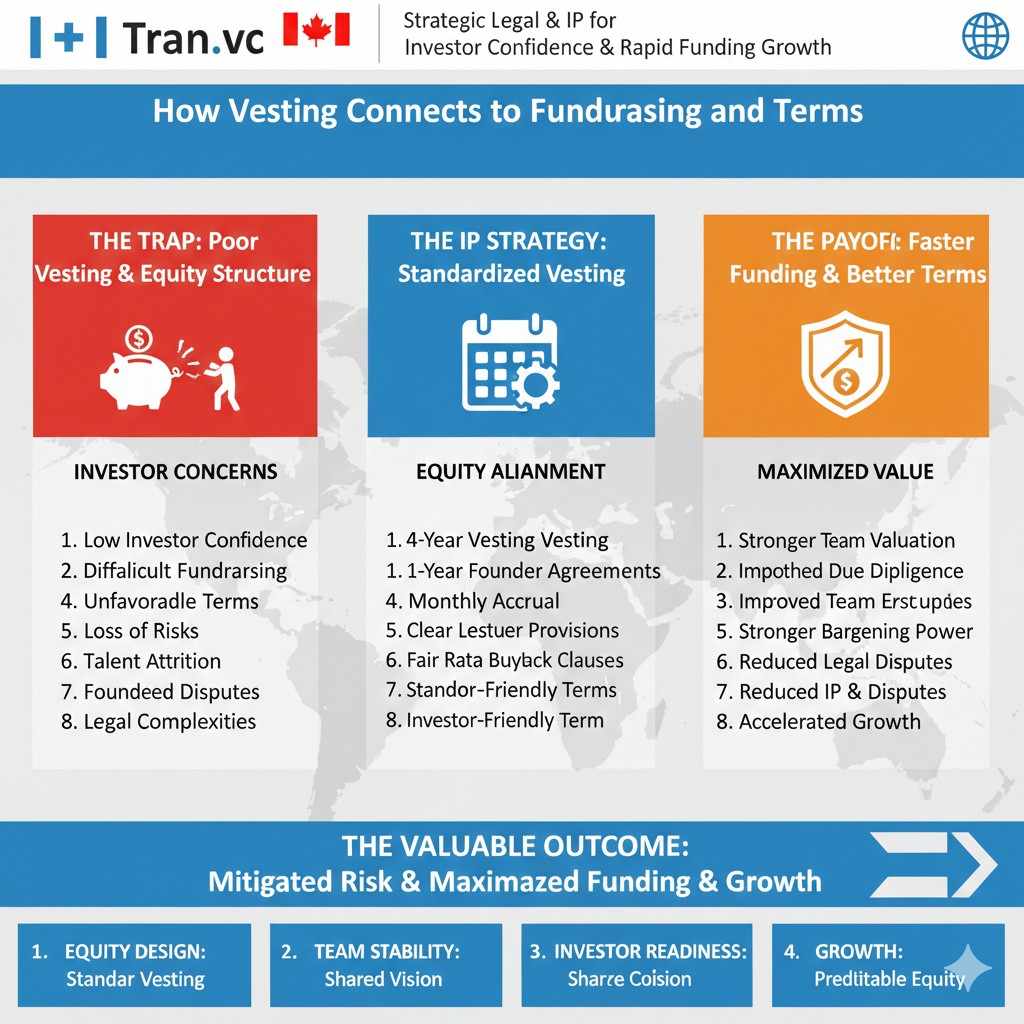

How Vesting Connects to Fundraising and Terms

Investors see vesting as part of “fundable hygiene”

When an investor reviews your company, they look for things that can blow up later. Cap table problems are high on that list. Vesting is a cap table control tool.

If vesting is missing, an investor may still invest, but they may add conditions. They might require founders to start vesting at the time of the investment. They might require a “reverse vesting” agreement. They might require that unvested shares be subject to repurchase.

Those requirements can feel like pressure. But the deeper truth is simple: investors want the company to be investable. Vesting is one of the easiest ways to make it investable.

Your future team will ask about it too

It is not only investors. Strong hires ask tough questions. They will ask who owns what, who is still active, and how equity is handled.

If a hire sees that big ownership belongs to someone who left, they will feel the company is unfair. They may demand more equity, or they may walk away.

Vesting protects your ability to build a team. It keeps your equity pool useful. It signals that value is earned, not just claimed.

Vesting makes dilution feel more fair

Founders often fear dilution. That fear is normal. But dilution becomes harder to accept when people who are not working still hold large pieces.

When vesting is in place, dilution feels more fair because the people being diluted are still the people building. It reduces emotional conflict. It makes negotiations cleaner. It helps the company stay aligned when raising money.

This is one of the quiet benefits of vesting. It keeps your company from becoming a story of “who deserves what” and keeps it focused on building.

Tactical Setup: How to Put Vesting in Place Early

Do it while the team is still friendly

The best time to set vesting is when things are going well. If you wait until you are stressed, it becomes personal. If you set it early, it feels like normal structure.

A simple way to approach it is to say, “We trust each other. Vesting is for protecting the company, not for doubting anyone.” That framing helps keep the tone calm.

If you have not set vesting yet, the next best time is now. Every month you delay increases risk.

Put it in writing with proper documents

A handshake is not enough. Investors will want to see signed documents. This is not because they doubt you. It is because they need clean legal records.

In many setups, founder shares are issued early, but they are subject to a repurchase right that matches the vesting schedule. That is often called “reverse vesting” because the founder starts with the shares but earns the right to keep them over time.

You should work with a startup lawyer to do this correctly. Poorly written vesting terms can create tax issues or legal confusion.

Tie it to roles and expectations, not feelings

Vesting should not be a weapon. It should not be used to punish someone you are upset with. It should be tied to the simple idea that ownership matches contribution over time.

A practical way to reduce future conflict is to be clear about roles early. Who is building what? Who is leading what? Who is raising money? Who is managing hiring? When roles are clear, vesting feels like a shared commitment, not a trap.

This is also where many teams benefit from outside help. A neutral third party can help you set terms without emotion.

Vesting and IP: The Link Many Founders Miss

If someone leaves, what happens to the invention work?

In robotics and AI, a huge part of your value is in your invention work. That includes algorithms, models, training pipelines, hardware designs, and system methods.

Vesting does not automatically solve IP ownership. You also need clear invention assignment agreements, so the company owns what founders and employees create.

If a key builder leaves and there is no clear IP assignment, you can end up with a serious risk. Investors will not like it. Acquirers will not like it. It can even stop a deal.

This is why we at Tran.vc focus on building strong foundations early. Vesting is one piece. IP control is another piece. When both are clean, your company becomes much easier to fund.

Patents and vesting work in the same direction

Patents protect what you build from copycats. Vesting protects your company structure from breaking when people change.

Both are about protecting the upside you are working so hard to create. If you are building deep tech, you do not want to spend years creating value only to lose it because of simple setup mistakes.

Tran.vc invests up to $50,000 in in-kind patent and IP services to help founders build real assets early. If you want support setting up strong IP strategy alongside fundable company structure, you can apply anytime at https://www.tran.vc/apply-now-form/.

Founder Vesting That Still Feels Fair

The fear behind vesting is real

Many founders hear “vesting” and feel a quiet worry. They think it means they can lose what they built. They imagine a board pushing them out and taking their shares. That fear often comes from stories told without context.

In normal early-stage startups, vesting is not designed to trap good founders. It is designed to protect the company from a bad outcome: someone leaving early while keeping a big piece. If you are doing real work and staying involved, vesting is usually a non-issue. It runs in the background like a basic system setting.

The key is to set it up in a way that feels fair to the people who are actually building. That starts with clear terms and clear expectations, not pressure or vague promises.

How founders can protect themselves inside vesting

The main protection founders get is simple: if the company wants you to keep working, it should treat you well. Vesting does not change that. If anything, vesting pushes the company to be more thoughtful, because replacing a founder is costly.

Founders can also protect themselves by making sure roles, decision rights, and board structure are balanced. Vesting is one piece of the “fair setup,” but it is not the only piece. If your governance is messy, vesting can feel scary. If your governance is clean, vesting feels normal.

It also helps to remember that investors usually want founders to be motivated and safe. If founders feel threatened, the company suffers. Most experienced investors know this and aim for a structure that keeps everyone aligned.

The words in the documents matter more than people think

Two vesting plans can look the same on the surface but feel very different in real life, based on how they are written. The documents decide what happens if someone leaves, how the buyback works, and what counts as “leaving.”

This is why doing it properly matters. A sloppy template can create unclear triggers, and unclear triggers create conflict. A good setup uses plain terms and standard definitions, so there are fewer surprises later.

If you are unsure, it is worth getting help early. Fixing it later is almost always harder than doing it right at the start.

Acceleration, Cliff Credit, and Other Common Founder Questions

Should time already worked count toward vesting?

Sometimes founders start building before they form the company. They may spend six months on nights and weekends, then incorporate and raise money later. In those cases, founders often ask if that early work should count.

Investors sometimes agree to “credit” for time already spent, but it depends on the story. If the founders truly worked full-time and made meaningful progress, credit can be reasonable. If it was light work or uncertain work, investors may prefer vesting to start at incorporation or financing.

A practical way to approach this is to be honest about what happened. If you did meaningful work, show evidence. Show prototypes, commits, user calls, experiments, or engineering milestones. That makes the request feel grounded and fair.

If you are raising, ask early in the process. Do not wait until the last moment. Late surprises during a term sheet stage often cause friction.