Most founders think IP assignment is a “legal cleanup task.” Investors don’t.

To an investor, your IP assignment structure answers one simple question: Does this company truly own what it sells? If the answer is unclear, even a strong product can become a risky deal. And in deep tech—AI, robotics, hardware, biotech-adjacent tools—risk around ownership is a deal-killer because your real value is not the UI or the pitch deck. It’s the know-how in your code, your models, your data work, your schematics, your designs, and the hard choices you made while building.

Here’s the hard truth: you can do everything right in the product, and still lose trust in diligence because of one missing signature, one outdated offer letter, one contractor agreement with the wrong words, or one “side project” that wasn’t properly handled. The scary part is that these gaps often happen when you’re moving fast, hiring scrappy, and building at night—exactly how early-stage companies are born.

This article is going to show you what investors look for in IP assignment structure, in plain language, with a heavy focus on what you can actually do this week to tighten things up. Not theory. Not legal poetry. Just practical moves that make your company easier to fund and harder to copy.

And if you want experienced help doing this the right way from day one—without giving up control early—Tran.vc invests up to $50,000 in-kind in patent and IP services for AI, robotics, and other technical startups. You can apply anytime here: https://www.tran.vc/apply-now-form/

What Investors Want in Your IP Assignment Structure

Why investors care so much about “who owns what”

Investors are not trying to be difficult when they ask about IP assignment. They are trying to avoid a simple, painful outcome: paying for a company that does not fully own the thing that makes it valuable. In software, that “thing” might be your core codebase or model training pipeline. In robotics, it might be your control stack, sensor fusion methods, mechanical designs, or test rigs. If ownership is not clear, the company can’t defend itself, can’t license safely, and can’t sell cleanly later.

This matters even more at seed and pre-seed because your business is still fragile. You may not have long customer contracts or steady revenue yet. So the investor leans harder on foundational proof. Clean ownership tells them the company is real, serious, and built for the long run.

When an investor pushes on IP assignment, they are also testing founder maturity. They want to see if you can handle boring but important details. It signals how you will handle security, compliance, and customer trust later. For deep tech companies, these details are not “later problems.” They are the core of the deal.

If you want a team that helps you build this foundation early, Tran.vc supports technical founders with up to $50,000 in-kind patent and IP services. You can apply anytime here: https://www.tran.vc/apply-now-form/

The real question behind the legal words

In diligence, investors rarely start with complex legal language. They start with plain questions, even if they use formal terms. Who wrote the code? Who designed the hardware? Who trained the model? Was that person an employee, a contractor, or a co-founder? Did they sign an agreement that assigns their work to the company?

If you can answer those questions fast and with confidence, you remove friction. If you hesitate, or if your answers depend on “we meant to do it,” investors begin to worry. They don’t need perfection, but they need a clear path to certainty. The cleaner your structure, the faster your round moves.

Investors also want to know what happens if someone leaves. Many companies break here. A key engineer quits, and suddenly the cap table is messy, the repository is tied to a personal account, and the invention paperwork is incomplete. A strong structure makes departures boring, not dangerous.

In other words, investors want an IP assignment setup that still works on your worst day. They want ownership to survive stress. That is what “investable” looks like in practice.

What this article will help you build

By the end, you should be able to look at your company and say, with a straight face, “Yes, we own what we built.” You should also be able to show it. Investors respond well when you can produce signed documents quickly and present a simple story that matches the paperwork.

You will also learn how investors think about risk around prior employers, side projects, contractors, and open-source usage. Those areas are where most early-stage teams get surprised. Not because they did something wrong on purpose, but because they did not set things up early.

This is not about being paranoid. It is about being prepared. The best founders don’t just build product. They build a company that can be funded, defended, and acquired without drama.

If you want hands-on help turning your inventions into defensible assets, Tran.vc can help you do it early and correctly. Apply here whenever you’re ready: https://www.tran.vc/apply-now-form/

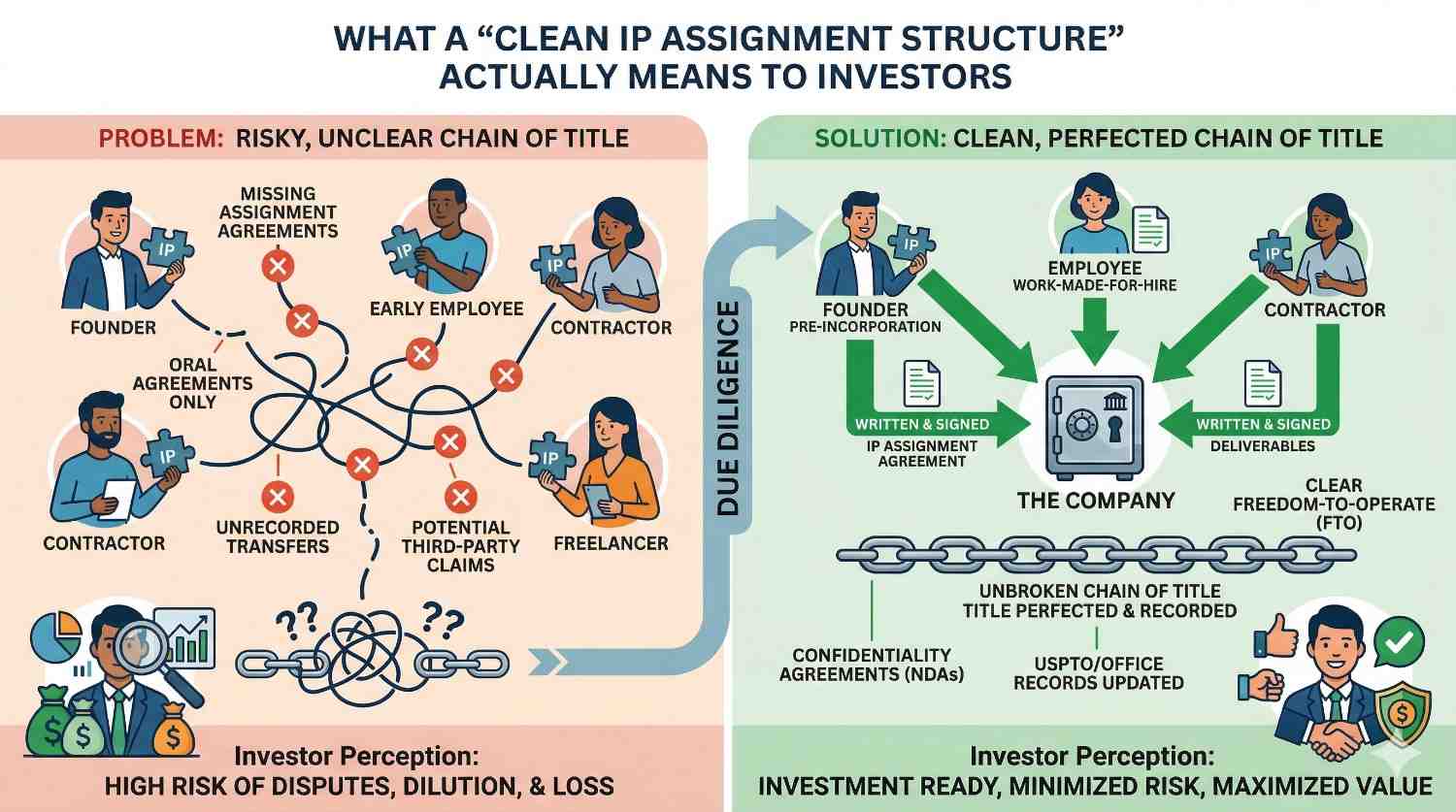

What “clean IP assignment structure” actually means to investors

A structure, not a stack of PDFs

A common mistake is thinking IP assignment is a set of documents in a folder. Investors are looking for something more like a system. They want to see that every person who contributes to the product is captured by the same process, every time, with no special cases that create holes.

This is why a single missing contractor agreement can matter. It breaks the story. Investors start wondering what else is missing. They may ask for a full audit, which adds cost and time. Or they may step back from the deal if the risk feels too hard to price.

A clean structure means the company has a repeatable way to handle contributors. When someone joins, they sign the right paperwork before they push code or start CAD work. When someone leaves, access is removed and the record stays clean. The company does not rely on memory, goodwill, or informal promises.

This is also why investors care about dates. If a document is signed months after the work started, it raises questions. It might still be fixable, but it creates more diligence work. Clean structure reduces the number of “fixable but messy” issues.

The assignment chain must be simple and complete

Investors like simple chains of ownership. A clean chain usually looks like this: each inventor or creator assigns their work to the company, and the company holds it. That’s it. The more side paths you have, the more questions you invite.

Side paths can show up in many ways. Code might live in a founder’s personal repo created before incorporation. A prototype might be built under a university lab environment. A contractor might have reused old code from a previous client. A co-founder might have built the first version while still employed elsewhere. Each of these can disrupt the chain.

Investors do not expect you to have avoided every complex situation. They do expect you to have documented it and cleaned it up. The key is that the chain ends in the company, with clear proof, and without hidden claims from other parties.

If your chain is not simple, investors will ask for comfort through extra documents. That can include confirmatory assignments, invention disclosures, board consents, or releases. It is better to fix the chain early than to scramble in the middle of a round.

Investors want clarity on “background IP” versus “company IP”

One of the most confusing areas for founders is the difference between what you brought in and what the company built. Investors want this distinction because it impacts value and control. If the company relies on something that is personally owned by a founder, the investor worries about leverage and continuity.

Background IP is what existed before the company’s work began. It can include a personal library, a prior patent filing, a research result, or a method you developed in another setting. Company IP is what was created for the company, using company time, resources, or direction.

The clean way to handle this is to identify background IP early and decide how the company can use it. Sometimes it is assigned to the company outright. Sometimes it is licensed to the company under clear terms. The wrong way is leaving it vague and hoping it never comes up.

Even if you fully trust each other as founders, investors can’t base a deal on trust alone. They need documents that survive changes in relationships. Clear separation between background and company IP makes the business safer and easier to underwrite.

Tran.vc helps founders make these lines clear early, and also helps you convert key work into patent assets that investors respect. Apply anytime here: https://www.tran.vc/apply-now-form/

The exact risks investors look for in diligence

The “missing signature” problem

The most common investor red flag is the simplest one: a key contributor never signed an IP assignment. It happens when teams move fast, hire friends, or use contractors for short bursts. It also happens when co-founders start building before incorporation and never backfill the paperwork.

From an investor’s view, missing signatures create two risks. First, that person might later claim ownership. Second, even if they never claim it, an acquirer or future investor might still walk away because the record is incomplete. The problem is not only lawsuits. The problem is uncertainty.

Fixing missing signatures is usually possible. But if the relationship is strained, it can become expensive. Investors know this, so they care early. They would rather fund a company that has boring paperwork than one that needs a delicate negotiation with a former teammate.

You can reduce this risk by treating signatures as part of onboarding, not an afterthought. The person should sign before they contribute. That one habit alone removes a surprising amount of future friction.

The contractor trap

Contractors are a major source of IP confusion. Many founders assume that if they paid for work, they own it. In many places, that is not automatically true. Without the right contract language, the contractor may still own the copyright, or may have rights to reuse the work.

Investors look closely at contractor agreements for two reasons. Contractors often touch core parts of the product early. And contractors often work for multiple clients, which raises questions about reuse and contamination. If your contractor pulled in code from another project, you could inherit someone else’s problem.

A strong contractor agreement is clear about assignment, confidentiality, and the obligation to help with patents if needed. Investors also like to see that contractors were managed well, with scope, deliverables, and access controls. It tells them you run a serious shop.

If you used contractors for anything core, you should assume investors will ask for those agreements. Having them ready makes you look prepared. Missing agreements make you look careless, even if the product is great.

The prior employer shadow

Investors pay attention to where the founders came from. If you worked at a big tech company, a robotics lab, or a well-known AI group, investors will want comfort that your new work is not tied to your old job. The risk is not only theft. The risk is that your old employer might claim inventions created during employment, or claim misuse of confidential information.

This can be messy because many employment agreements have invention assignment clauses. Some are broad, some are limited, and some depend on state law. Investors do not want to discover later that your core algorithm is covered by a claim from a previous employer.

The best approach is to be clean from the start. Build your company work on your own time, with your own equipment, and after you leave if possible. If that is not possible, document what you did, when you did it, and why it is separate. Investors care about the story, but they care more about evidence that supports the story.

This is an area where experienced IP counsel matters. A small cleanup early is far easier than an argument later. Tran.vc specializes in building strong IP foundations for technical founders. You can apply anytime here: https://www.tran.vc/apply-now-form/

University and research entanglements

If your work began in a university lab, under a grant, or as part of academic research, investors will ask who owns the results. Universities often have policies that claim ownership of inventions created using university resources or within sponsored programs. Even student projects can fall under policies if they used lab facilities.

This does not mean you can’t build a company. Many great companies started in universities. It does mean you need clarity. Investors want to see that the company has proper rights through assignment or licensing, and that any obligations to sponsors are understood.

The risk here is not only ownership. It is also restrictions. Some licenses limit fields of use or impose revenue sharing. Investors want to know what they are buying into. If the relationship with the university is fuzzy, the company can become hard to fund.

If you have any university tie, it is worth mapping it early. What facilities were used? What funding was involved? Who was on the research? What documents exist? This is not about fear. It is about avoiding surprises.

Open-source and third-party code

Investors do not expect you to avoid open-source. They do expect you to use it responsibly. The risk is that certain licenses can require you to share your source code or impose obligations that conflict with your business model. In deep tech, this can be especially sensitive if your core moat is software.

Investors will often ask for an open-source policy or at least a clear explanation of how you track usage. They may ask whether you used any “copyleft” licenses in core components. They may also ask if you used third-party datasets and whether you have rights to use them for training and commercial use.

Many founders treat this as a later problem and then panic in diligence. The better move is to track open-source early, keep records, and avoid mixing unknown code into your core. Investors like when you can say, “Yes, we track it, and we can show you our list.”

This is not about being perfect. It is about being disciplined. Discipline signals that your IP is not fragile.

What investors want in your IP assignment structure

The investor-friendly structure you should aim for

Investors want your ownership story to be boring. Not because they dislike your company, but because boring ownership means low risk. When they can glance at your structure and immediately see that every contributor assigned their work to the company, they relax. That relaxation often shows up as faster diligence, fewer legal fees, and fewer “special conditions” in the term sheet.

A clean structure usually has one simple rule: if a person creates something for the company, the company owns it. That rule should be reflected in every relationship you have, whether it is a co-founder, an early employee, a contractor, or an advisor who wrote code or designed something.

Investors also like consistency. They do not want five different templates floating around. They want one standard employee agreement, one standard contractor agreement, and a clear founder assignment package. When your documents are consistent, you reduce the chance that one person’s paperwork quietly contradicts the rest.

Even at pre-seed, you can build this structure in a lightweight way. You do not need a huge legal team. You need a clear system and the discipline to use it every time someone touches the product.

Tran.vc helps founders set this up early, and also turns key technical work into patent assets that stand out in fundraising. You can apply anytime at: https://www.tran.vc/apply-now-form/

The “chain of title” story you should be able to tell in one minute

In diligence, you want a short, confident explanation that matches your documents. It should sound like a simple timeline, not like a debate. The more complicated your verbal story is, the more investors will assume the paperwork is worse than it is.

A strong story often sounds like this: the company was formed on a certain date, founders assigned prior work to the company, and every person who contributed since then signed an agreement that assigns inventions and code to the company. Contractors signed “work made for hire” style language where applicable, and they also assigned inventions. Open-source use is tracked. If any background IP exists, it is either assigned to the company or licensed under clear terms.

That is the story investors want to hear. Not because it is fancy, but because it is clear. It signals that the company is stable and that future disputes are unlikely.

If your story is not that clean today, don’t panic. Most early companies have gaps. The key is to clean them up before you are in the middle of a raise, when the pressure is high and the timeline is tight.

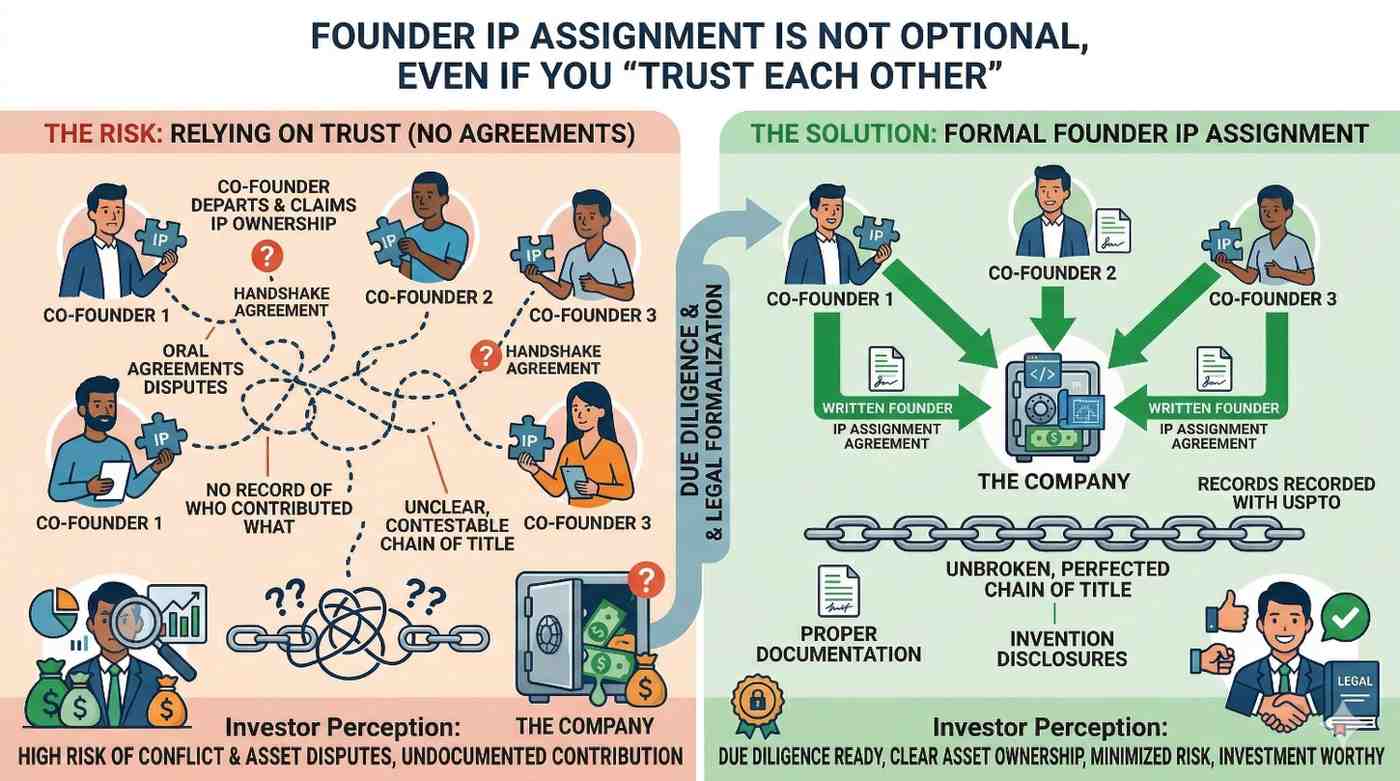

Founder IP assignment is not optional, even if you “trust each other”

Founders often skip formal assignment because it feels awkward. You may feel like it implies distrust. Investors see it differently. They see it as professional. If the founders cannot handle basic ownership hygiene, investors wonder how they will handle bigger issues later.

Founder assignment should cover work done before and after incorporation. Many teams start building months before filing the company paperwork. That early work often becomes the core product. If it is not assigned, the company may not clearly own it.

This gets even more important when founders used personal laptops, personal repos, and personal accounts early. Investors do not want a situation where the “real” codebase lives under a founder’s GitHub account and is only loosely connected to the company. They want it under company control, with company access management.

Founder assignment is also where you clarify any background IP. If a founder brings a library, a dataset, a prior patent filing, or a method they developed earlier, you should document how the company gets rights. Investors dislike informal “handshake” licenses because they can fall apart later.

The goal is not to trap anyone. The goal is to make the company fundable and protectable.

Employee invention assignment should be part of onboarding, not a later fix

For employees, investors look for a standard set of documents signed at the start. They want to see confidentiality and invention assignment language that clearly covers work created for the company. They also want the employee to have a duty to help with patent filings, even after they leave, within reason.

Investors also like clarity on what tools and systems employees used. If an engineer worked from a personal account and pushed code into a personal repo for months, it creates uncertainty. Even if the company later copied the repo, an investor may still worry about whether the company has full control over access and history.

A clean setup means employees use company accounts and company-managed systems. It means access is granted and removed in an organized way. These details may seem operational, but investors view them as part of IP safety. Your code is an asset, and you should treat it like one.

Another thing investors notice is whether employee agreements were updated as the company matured. Early-stage teams sometimes use a simple template from a friend, and later they adopt better templates but only for new hires. Then you have two classes of paperwork. Investors do not love that split, because the older employees often touched the most core work.

If your early agreements were weak, a good fix is to do a clean update and get confirmatory signatures. The sooner you do it, the easier it is.

Contractor agreements need stronger language than most founders expect

When investors worry about IP assignment, contractors are often the first place they look. That is because contractors can create valuable work while sitting outside your standard employee structure. They might be in another country. They might use their own tools. They might subcontract. They might reuse pieces of older work.

Investors like contractor agreements that do three things clearly. First, they make it clear that the work belongs to the company. Second, they lock down confidentiality and limits on reuse. Third, they require cooperation for patent filings and confirmatory assignments if needed.

They also like to see that contractors were not overused for core work. This is not a hard rule, but a pattern investors notice. If your core model training pipeline, your core embedded code, and your core mechanical design were all made by contractors, investors may worry about continuity and control.

If you did use contractors for core work, the best way to reduce investor worry is to show clean paperwork, clear scope, and clear handover. That includes access transfer, documentation, and the company having full possession of deliverables and source files.

If you are unsure whether your contractor paperwork is strong enough, this is exactly the kind of cleanup Tran.vc helps with as part of building an IP-backed foundation. Apply anytime here: https://www.tran.vc/apply-now-form/

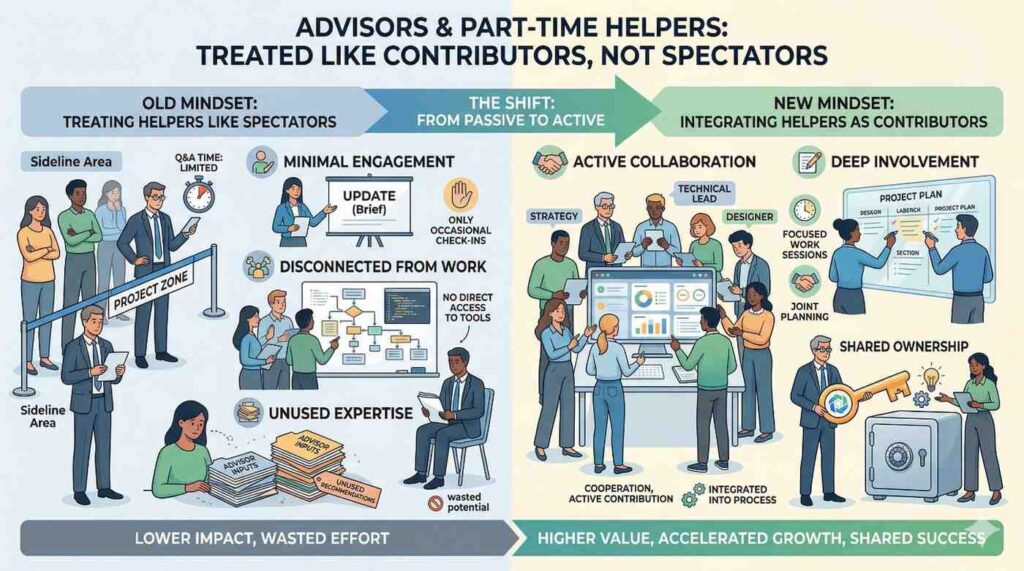

Advisors and part-time helpers must be treated like contributors, not spectators

Advisors feel informal, and that is what makes them risky. Investors will ask whether an advisor wrote code, designed features, suggested a novel method, or contributed to technical direction in a way that could be considered inventorship. They may also ask whether that advisor works at a company that could later claim a conflict.

If an advisor truly only gave high-level guidance, your risk is lower. But if an advisor wrote a core algorithm sketch, improved your claims, or helped design a unique system, investors may want to see that the company has rights.

Many founders forget that inventorship is not about job title. It is about contribution to an invention. If someone helped define the novel step, they might matter. Investors do not want a surprise later where an advisor’s name should have been on an invention disclosure or a patent application.

The clean approach is to treat advisors who contribute work like contractors. Use an agreement that covers confidentiality and assigns IP. Keep the relationship clear. This protects both sides and prevents confusion later.

Background IP must be handled with written rights, not assumptions

Investors will ask, “Did any founder bring something in?” The wrong answer is “Not really,” when the truth is that a founder built a library, a dataset, or a prototype earlier and the company is using it.

Background IP is not bad. It can be a strength. But it must be handled cleanly. Investors want to see that the company can keep using that IP even if the founder leaves. That is why written rights matter.

If a founder truly wants to keep background IP personally owned, a license can work, but investors will look closely at the terms. They will want it to be permanent enough, broad enough, and stable enough. If the license can be revoked, or if it can be renegotiated later, it creates leverage risk. Investors dislike leverage risk.

Often, the simplest answer is assignment of the background IP to the company, especially if it is core to the product. If it is not core, or if it is widely used outside the company, then a well-drafted license might make sense. The key is that the company’s right to operate should not depend on handshake trust.

This is a common area where founders unintentionally create future tension. Cleaning it up early is both easier and kinder.

How investors expect your “diligence folder” to look

The goal is speed and certainty, not legal theater

When investors ask for diligence materials, they want speed. They do not want you to spend weeks searching through email threads. They want you to share a clean set of documents that answers their questions directly.

A well-prepared folder also shows leadership. It tells investors you understand how fundraising works and you respect their time. It reduces back-and-forth. It also makes your counsel’s work cheaper, because there is less chaos to sort.

Investors do not need a mountain of papers. They need the right papers. They also want them organized in a way that makes sense, with names and dates that match your company story.

If your folder looks like a random dump of files, investors assume your process is random too. That may not be fair, but it is how pattern recognition works in deals.

The documents that remove the most doubt

Investors typically expect to see founder assignment paperwork, employee invention assignment agreements, and contractor assignment agreements. They also often ask for any prior IP filings, whether provisional or non-provisional, and any licenses or IP purchase agreements tied to the company’s work.

If there was university involvement, investors may ask for the license or assignment paperwork. If there were grants or sponsored research, they may ask for relevant documents that show rights and obligations.

They may also ask about open-source tracking and third-party software usage, especially if your product is software-heavy. They usually do not want every line item in the world, but they want enough to feel confident you are not sitting on a hidden license problem.

They may also ask for proof that the company owns the domains, key accounts, and repositories. This can feel operational, but it ties directly to IP control. If a founder owns the domain personally, investors worry about what happens in a dispute.

The key is not to impress them with quantity. It is to calm them with clarity.

Dates and signatures matter more than most founders realize

Investors read signatures and dates like engineers read logs. They are looking for consistency. If your founder assignment was signed long after incorporation, they will ask why. If your contractor agreement starts after the contractor delivered code, they will ask what happened before the start date.

These questions do not automatically kill a deal. But each one adds time. Each one invites more follow-up. And each one slightly lowers confidence until it is resolved.

This is why “confirmatory assignments” exist. If you missed something early, you can often fix it by having contributors sign a statement confirming they assigned the work. Doing this before fundraising makes you look proactive. Doing it under deadline makes you look reactive.

If you have gaps, a good approach is to make a list of every person who touched product work and check whether you have a signed agreement for each. That simple audit often reveals the real holes quickly.

Tran.vc often helps founders run this audit and clean up the structure while also building a patent plan that fits the product roadmap. Apply anytime here: https://www.tran.vc/apply-now-form/