Most-Favored Terms sounds fair. Even friendly. Like you’re just promising to treat someone well.

But in startup deals, “most-favored” language often means this:

You are promising a person today that they will automatically get the best deal you give anyone later.

That one sentence can quietly take control away from you.

It can also break future fundraising, scare off real investors, and force you into messy side letters and rewrites when you should be building product.

Founders sign these terms when they are tired, rushed, or grateful someone said “yes.” And later, when a serious investor shows up, that early “yes” becomes a chain around your cap table.

This article is about the most common “most-favored” clauses founders sign without meaning to. It is also about what to do instead, how to spot the trap early, and how to keep your next round clean.

Tran.vc works with technical founders early, before things get messy, to protect what matters most: your leverage, your cap table, and your core IP. If you want help reviewing terms like this, or building an IP plan that makes investors take you seriously, you can apply anytime here: https://www.tran.vc/apply-now-form/

Most-Favored Terms: What Founders Should Never Sign

What “most-favored” really means in plain English

A most-favored term is a promise you make today about the deal you will give tomorrow. It usually says that if you later give anyone a better deal, you must upgrade the early signer to match those better terms.

That sounds like “fairness,” but it is not fairness. It is a moving target that follows you into every future round, every bridge, every SAFE, and sometimes even partnerships and vendor deals.

The core problem is simple. You cannot predict the future terms you will need to offer later. Yet the clause forces you to treat the first signer as if they were in every later negotiation, without them doing any later work.

Why founders sign it even when it is risky

Most founders sign most-favored language because they want to close. They are trying to get the first check, the first pilot, the first partner, or the first “yes” that makes the startup feel real.

The other side often frames it as harmless. They say it is only there “just in case.” They say it will never trigger. They say it keeps everyone aligned.

What they do not say is that it makes later fundraising slower and harder. It can also make your company look inexperienced, because seasoned investors know this clause can create chaos.

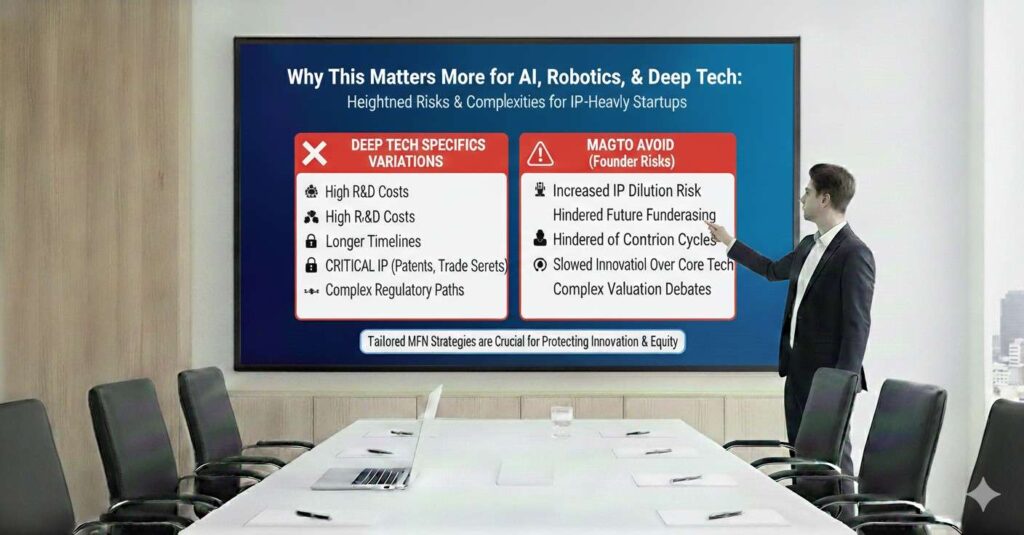

Why this matters more for AI, robotics, and deep tech

Deep tech deals change fast. Your valuation can jump when a demo works. Your terms can shift when a strategic investor shows up. Your risk profile changes when you file patents and lock in ownership.

Most-favored clauses are dangerous in fast-changing companies because the “better deal later” is not a rare event. It is normal. The clause is built to trigger at exactly the moment your company is gaining strength.

Tran.vc works with technical teams to build real, defensible value early, especially through patents and IP strategy. That value often improves your next deal terms, which is great—unless a most-favored clause forces you to give away that upside. If you want help setting up IP and deal readiness early, apply anytime: https://www.tran.vc/apply-now-form/

The hidden cost: how most-favored terms quietly take your leverage

Your future deal becomes less flexible

Fundraising is not one negotiation. It is many small negotiations over time, with different people, different risk levels, and different goals.

When a most-favored clause is present, you lose the ability to tailor terms for a specific situation. You cannot say, “This investor gets X because they are leading,” without thinking, “Does that automatically upgrade someone from six months ago?”

That means you may avoid offering strong terms that could help you close a lead investor, because you fear triggering the upgrade. You end up stuck in the middle, offering bland terms to everyone, which can make your round weaker.

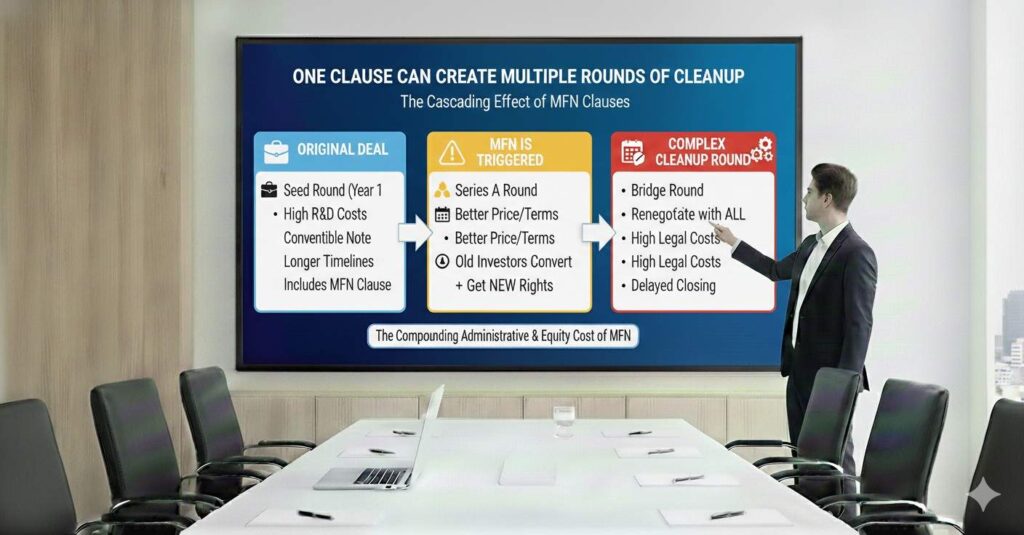

One clause can create multiple rounds of cleanup

Most-favored language often triggers side letters, amendments, and quiet back-and-forth that burns time. That time cost is real.

Instead of building, hiring, and shipping, you are digging through old documents. You are calling old investors. You are asking lawyers to interpret vague wording. You are trying to keep everyone calm.

Even if you “solve” it, the record stays. Future investors may ask why it existed, whether it triggered, and what else might be hidden.

It can scare away the investor you actually want

Strong investors want clean cap tables and simple terms. They want to know that if they lead, they can set the round and not be surprised later.

When they see most-favored clauses, they worry about silent passengers in the deal. They worry that their carefully negotiated terms will leak to others without those others doing lead-level work.

Some will still proceed, but they will demand fixes. Others will walk, especially when there are easier deals to do.

If you want your company to feel “investor-ready” before the first serious round, Tran.vc helps founders do the early work that matters—IP, patents, and strategy—so later investors feel confident. You can apply anytime: https://www.tran.vc/apply-now-form/

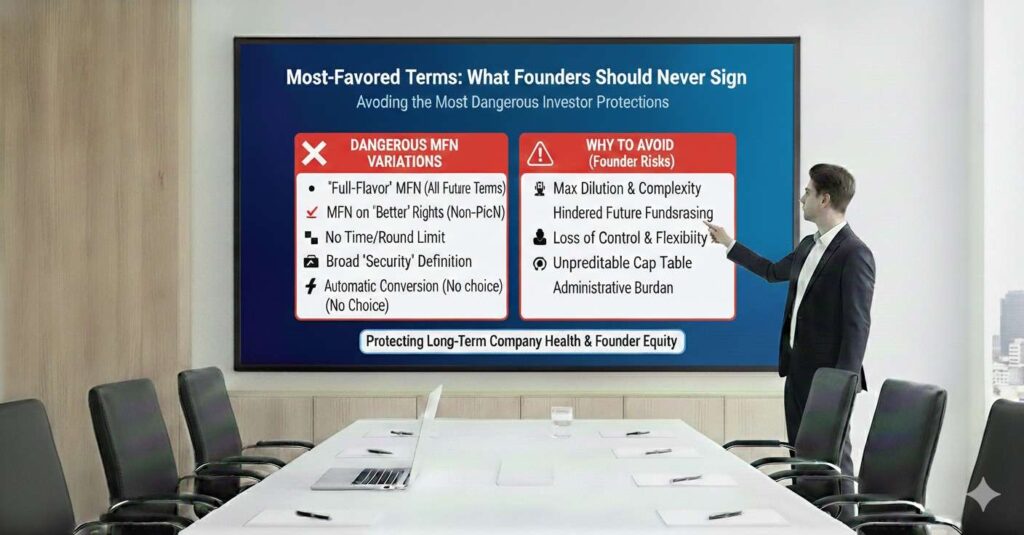

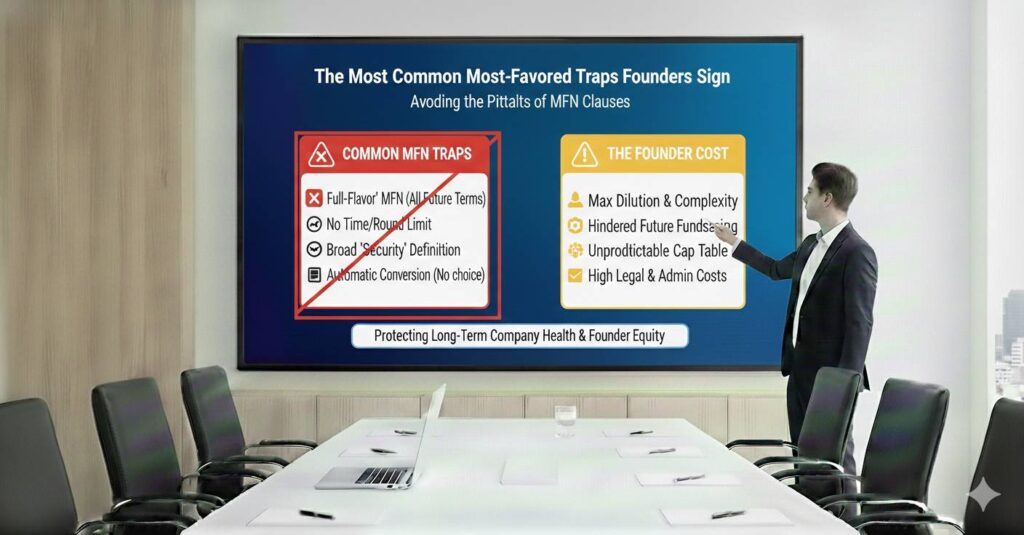

The most common most-favored traps founders sign

The “MFN” clause in a SAFE or note

This is the classic version. It says that if you issue a SAFE later with better terms, the earlier SAFE holder can switch into those better terms.

The word “better” is where the pain hides. Better might mean a lower cap, a bigger discount, extra rights, pro rata, information rights, or special protections.

Founders often think, “We will never issue a better SAFE later.” Then the market shifts, or a strong investor demands a lower cap, or you need money fast and offer a discount to close.

Now your earlier SAFEs may upgrade, and your math changes. The amount of dilution you thought you would face can grow without you choosing it.

The “best terms offered” promise in advisory or service agreements

Some advisory agreements include most-favored language. It might say the advisor will get terms equal to the best advisor terms you ever give.

This sounds small, but it can become a cap table problem. If you later bring in a high-value advisor and offer them meaningful equity, the earlier advisor could claim the same deal.

That can force you to either reduce what you offer later, or give away more than you planned. It creates tension with the very people you are trying to recruit.

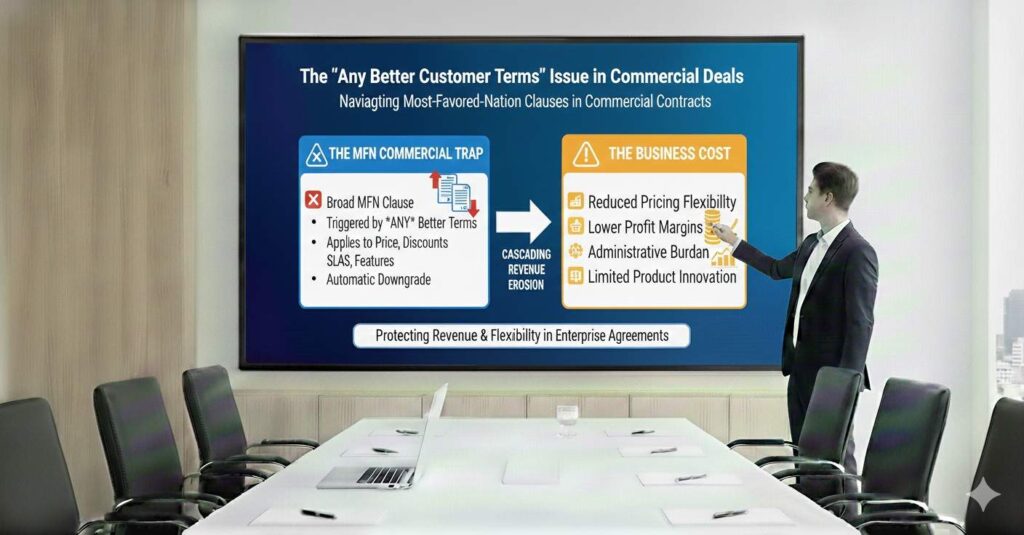

The “any better customer terms” issue in commercial deals

Most-favored language is not only about equity. It shows up in customer contracts too, especially with big companies.

A customer may ask for a promise that they will always get pricing at least as good as your best customer. Or they may ask to match discounts, service levels, or support response times.

For early-stage startups, that can be deadly. You need the freedom to experiment with pricing, pilot deals, and special one-time offers. A most-favored pricing clause can freeze your business model before you learn what works.

The “match any later investor rights” side-letter problem

Sometimes the main documents do not include MFN, but a side letter does. It might say the investor gets any rights you later give to another investor.

Founders ignore side letters because they feel “extra.” But that is exactly why they are risky. They sit in a folder until the wrong moment.

Then a new lead asks for a specific right, like stronger information rights or board observer access. If your side letter has MFN language, you may have to give that same right to earlier holders too.

How to spot most-favored language before it harms you

The keywords that should make you pause

Most-favored clauses are often labeled clearly, but not always. Sometimes they hide behind softer words like “parity,” “no less favorable,” “as favorable as,” or “match.”

You may also see phrases like “as amended from time to time,” which can expand the reach of the clause. Or you may see “any future issuance,” which can pull in deals you never expected.

The most important habit is to slow down when you see promises tied to future actions. If a term says “if you ever,” “at any time,” or “in the future,” that is your sign to read twice.

The scope question: what exactly gets upgraded

Even if you accept some form of MFN, the scope must be tight. Many clauses are written too broadly.

They might apply to all future financings, not just the same instrument. They might apply to economic terms and control terms. They might apply to rights that should never be copied, like board control or veto rights.

A clause that feels “small” can become huge if the scope is wide. Always ask: what counts as a better term, and who decides?

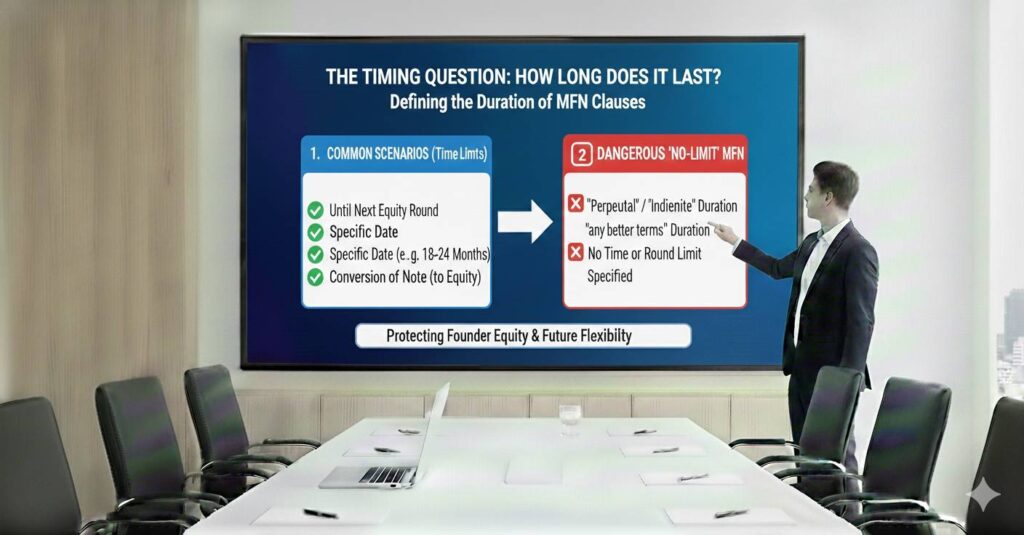

The timing question: how long does it last

Some MFN clauses never expire. That is one of the biggest mistakes founders make.

If it lasts forever, it will almost certainly trigger. Your company will evolve. Terms will change. You will do new deals with new needs.

If it is limited, it might still be a problem, but it is easier to manage. Time limits are not a perfect fix, but they reduce surprise and create an endpoint.

What to do instead: safer ways to offer comfort without giving away control

Use clear, fixed terms rather than floating promises

If someone is worried they will be treated unfairly, the answer is not a floating clause. The answer is to agree on clear terms now, and close.

Floating promises are dangerous because they shift your future bargaining power into the past. Fixed terms keep your future options open.

If the other side needs comfort, you can offer transparency. You can offer updates. You can offer a chance to invest again later under a defined process.

Those are real comforts that do not rewrite your future deals.

If you must use MFN, narrow it like a laser

Sometimes a deal is not worth losing, and you choose a limited MFN as a short bridge. If so, treat it like a hazardous material.

Limit it to a short time window, such as 30 to 90 days, not years. Limit it to a single instrument type, like “another SAFE with the same template,” not any financing.

Limit it only to one or two terms, such as the valuation cap, not “any better terms.” The broader it is, the more it will bite you.

Trade MFN for something you can live with

A better approach is to trade. If someone asks for MFN, you can offer a smaller discount, or a slightly better cap, in exchange for removing the MFN.

This keeps the deal simple. It also makes the cost visible now, rather than hidden later.

Even if the upfront terms feel a bit more expensive, the predictability is often worth it. Chaos in later rounds is far more costly than a small change today.

Real-world scenarios where MFN becomes a founder nightmare

Scenario one: the early SAFE that breaks your seed round

You raise your first small SAFE from a friendly angel. They ask for MFN “just in case.” You agree, because you want to move fast.

Three months later, a strong seed lead says they will invest if you lower your cap and add pro rata rights. You accept, because this is the investor you need.

Now your early SAFE holder can claim the lower cap and the extra rights. If you have several early SAFEs with MFN, they can all upgrade.

Your seed lead sees the expanding rights and dilution. They worry about the round getting messy. They ask you to fix it before closing.

That fix can take weeks, and your momentum slows at the worst time.

Scenario two: the enterprise customer that locks your pricing

A large customer offers a pilot. They push hard for “best pricing” language because they do not want to be the customer paying the most.

You accept, thinking your prices will only go up later anyway. Then you learn your product sells better with different packaging, and you need flexible discounts for different segments.

Now every time you offer a discount to close a new customer, your first large customer demands the same discount. Your revenue plan becomes unstable.

You may end up charging less than you should, not because it is smart, but because your contract forces you to.

Scenario three: the advisor clause that creates resentment

An early advisor helps you with intros and asks for MFN so they are not “left behind.” You accept because it feels polite.

A year later, you recruit a world-class advisor who has built in your exact space. You offer them a strong equity grant to secure their time.

The early advisor now claims they are owed the same deal. You are stuck between honoring a clause and protecting your cap table.

Even if you negotiate a compromise, the relationship damage is real, and it distracts you from building.

The founder’s checklist: how to protect yourself before you sign

Start by deciding what you are willing to promise, and what you are not

A founder who decides early will sign fewer bad clauses later. The hardest time to think is when money is on the table and time is short.

Your job is to protect flexibility. That means avoiding promises about unknown future terms.

If you want a simple internal rule, it can be this: do not sign clauses that automatically upgrade someone later, unless the clause is tight, short, and limited to one economic term.

Put someone in your corner before you negotiate

Most-favored clauses are designed to sound “reasonable.” That is why founders miss them.

You need someone to read like a skeptic, not like a polite partner. You need someone to ask, “How does this break later?”

Tran.vc supports technical founders early with IP strategy and patent work, and that early support often includes helping founders think more clearly about leverage and defensibility. When your IP is being built the right way, you usually need fewer “comfort clauses” to convince others to work with you.

If you want early-stage guidance like this, apply anytime: https://www.tran.vc/apply-now-form/

Treat every clause like it will be tested

The most common founder mistake is assuming a clause “won’t matter.” In startups, everything gets tested eventually.

If a clause exists, assume it will trigger at the exact moment you are doing better. That is how contracts work. They matter when the stakes rise.

When you read a most-favored clause, imagine your best future deal. Then imagine being forced to give parts of that deal away to people who did not earn it in that moment.

If that feels wrong, do not sign.

How investors read most-favored terms when they see them on your cap table

They treat MFN as a signal, not just a clause

Investors do not only read your numbers. They read your habits. A most-favored clause tells them how early decisions were made, and whether the company can run a clean process.

When a seasoned investor sees MFN language, they often assume two things at once. First, they assume you were under pressure when you signed it. Second, they assume there may be other “hidden” terms that will surface later.

That does not mean they will walk away every time. It does mean they will slow down. And in fundraising, slow is expensive.

A slow round weakens your position. It also gives investors more time to compare you to other deals. Many great startups lose momentum because of friction that could have been avoided.

They worry about “shadow economics” they cannot model

Good investors model outcomes. They try to understand dilution, ownership, and how control changes over time.

MFN terms make the model slippery. The investor cannot easily know who gets upgraded and when. The investor also cannot know what “better” will mean in the next negotiation.

So the investor protects themselves. They may lower the valuation they are willing to accept. They may ask for stronger rights. Or they may demand that you clean up the MFN terms before they invest.

If they demand cleanup, you are now negotiating with two groups at once: the new investor and the older holders who might be upgraded. That double negotiation is where deals get stuck.

They dislike anything that forces equal treatment when contribution is not equal

A lead investor often does more than write a check. They set the price. They help you close the round. They may help recruit or guide strategy. In return, they ask for certain terms.

MFN clauses can spread those lead terms to earlier investors who did not take lead risk. That makes the lead investor feel like they are paying a premium in effort while others get the same reward for free.

When that happens, the lead investor may stop trying to help you. Or they may decide the round is not worth the trouble.

In a tough market, investors pick the easiest clean deals first. MFN terms can move you out of that “easy” pile even if your product is strong.

How MFN clauses can quietly reduce your valuation

The clause can force you to price “against your past”

A normal fundraising process lets you match terms to the moment. Early checks are often more expensive for founders because risk is high. Later checks can be less expensive because you have traction.

MFN flips that logic. It lets early checks borrow the benefits of your later progress. If you later earn a better cap or better terms because you built real value, the MFN clause can pull that upside backward.

When you realize that, you may choose to avoid offering better terms later. That can push you into a weaker deal with a weaker lead.

So the clause can reduce valuation in two ways. It can directly upgrade early holders, and it can indirectly make you afraid to negotiate strong terms later.

It creates a “dilution surprise” at the worst time

Founders often do quick math based on what is signed today. They assume later rounds will have their own dilution, but the early round is “done.”

MFN can reopen old math. That is the worst kind of surprise because it hits when you are already busy raising.

If the upgrade changes the cap, discount, or other economics, your ownership outcome changes. Sometimes it changes enough to impact employee option pools, founder control, and even the decision to raise at all.

A good company should not be making major ownership decisions based on a clause they signed in a rush.

It can weaken your story in investor conversations

Fundraising is partly a story about clarity. Investors want to hear that you know what you are building, why it wins, and how you will use capital.

When MFN terms complicate your round, your story becomes about paperwork. You spend calls explaining why early documents are unusual, and what you are doing to fix them.

That shift is subtle, but it matters. You want investor time spent on your product, your moat, your market, and your team.

For technical founders, one of the strongest story upgrades is strong IP. Patents, defensible claims, and clean ownership can raise confidence fast. Tran.vc helps founders build that foundation early with up to $50,000 in in-kind patent and IP services, so your story stays focused on strength, not cleanup. You can apply anytime: https://www.tran.vc/apply-now-form/