Advisor agreements are one of those “small” papers that can quietly decide whether your startup stays clean and easy to fund… or turns into a messy problem later.

Founders usually bring advisors in for good reasons: you need fast answers, warm intros, hiring help, product feedback, or credibility. But the moment an advisor starts giving real help, you need clear writing around what they do, what they get, and what happens if things don’t work out.

Because here’s the hard truth: most advisor problems don’t come from bad people. They come from fuzzy promises.

And fuzzy promises become hard feelings later.

So in this guide, we’ll get the paperwork right—without turning it into a legal class. You’ll learn what to write, what to avoid, and how to set this up in a way investors like.

Also, quick note: if you’re building in AI, robotics, or deep tech, your advisor agreements should match your IP plan. If you want help setting up your IP the right way from day one, Tran.vc can invest up to $50,000 in in-kind patent and IP services. You can apply anytime at https://www.tran.vc/apply-now-form/.

What an advisor agreement really does

An advisor agreement is not “just paperwork.” It is a simple trade:

You get help.

They get a clear benefit.

Both sides know the rules.

That’s it.

And yet, most advisor agreements fail at that basic job because they are copied from a template with no thought. Or worse, nothing is signed at all.

When there is no agreement, the advisor may still believe they “own” something: equity, credit for an idea, a right to be involved, or a right to be paid. The founder may believe the opposite. Both may be honest. Both may feel hurt later.

A good agreement stops that.

It also tells future investors that you run a tight ship. Investors don’t panic when they see advisors. They panic when they see unclear deals, missing signatures, or advisors who can claim they helped invent the core tech.

So the real goal is not to “protect yourself from an advisor.” The goal is to protect the company from confusion.

The biggest mistake founders make: being too generous too soon

A common story:

A founder meets an experienced person. The advisor sounds sharp. The founder feels grateful. The founder offers equity fast—sometimes 1%, 2%, even more—because they want the advisor to feel valued.

Then one of three things happens:

- The advisor helps for two weeks, then fades away.

- The advisor keeps helping, but not in the way the founder needs.

- The advisor becomes a “shadow decision maker” without being on the team.

In all three cases, the founder is stuck because the deal was not shaped around real work.

This is why your paperwork must do one thing very well: it must connect reward to action.

Not to reputation. Not to “maybe.” Not to “we’ll see.”

Action.

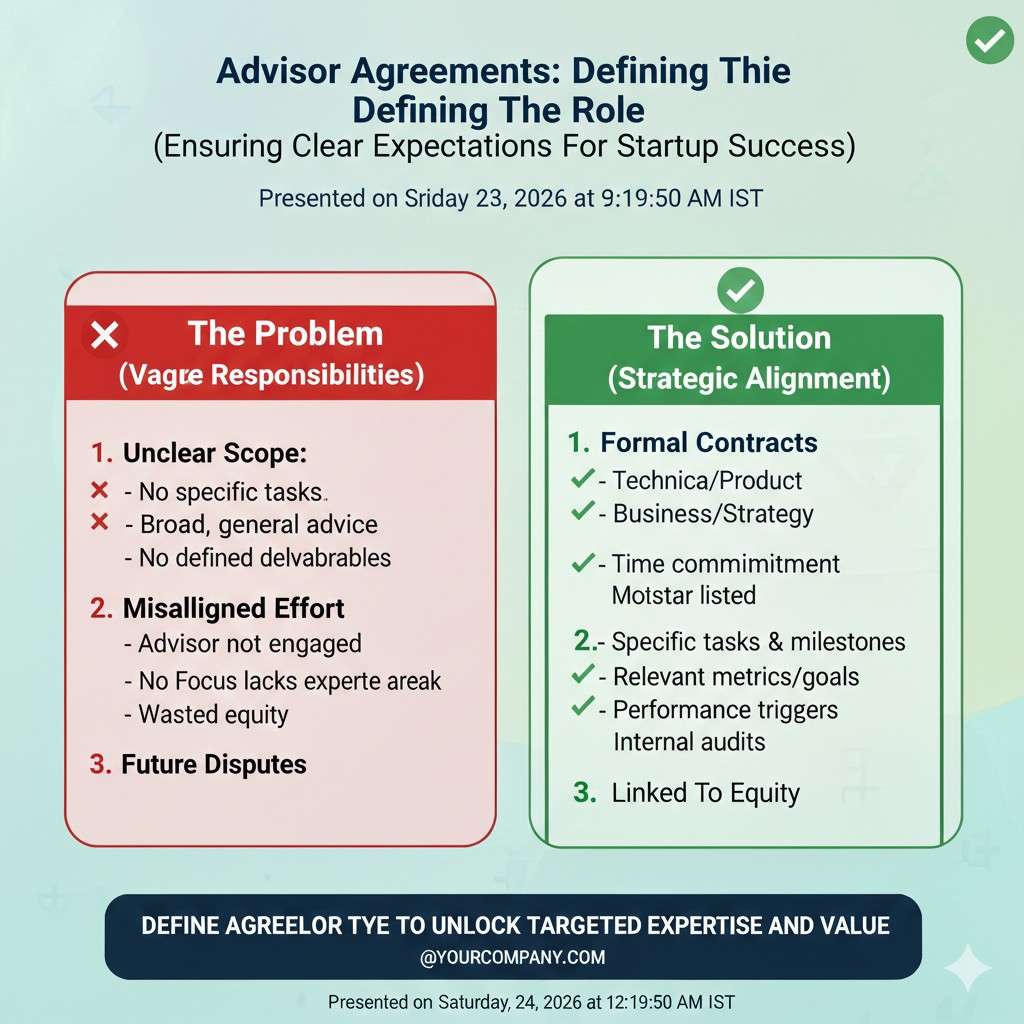

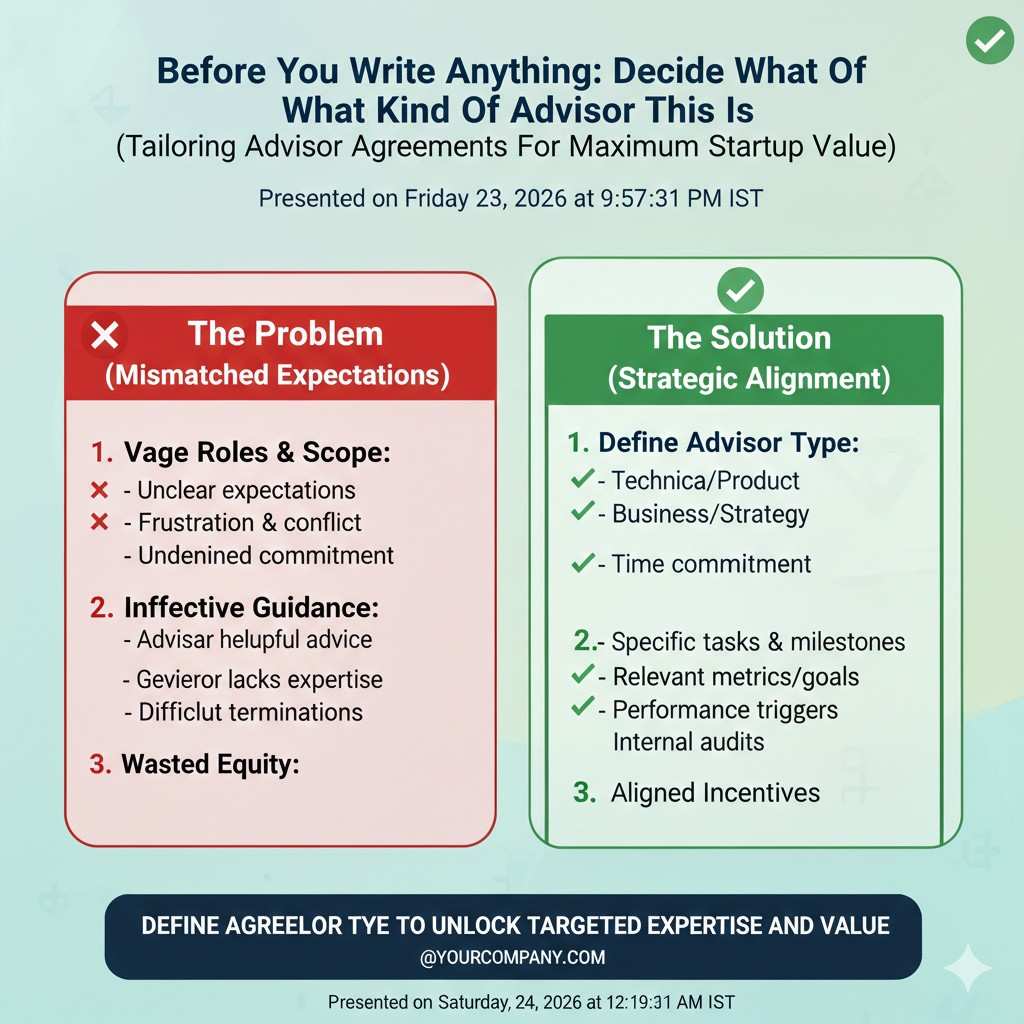

Before you write anything, decide what kind of advisor this is

This part feels basic, but it is where most problems start.

Some advisors are “light touch.” They answer a few questions a month. They might do one intro every now and then. They are useful, but they are not building with you.

Other advisors are “hands on.” They review decks, join sales calls, help hire, help with roadmap, give weekly feedback, or open doors that truly matter.

Both types can be great. But they should not be paid the same.

If you treat every advisor like a co-founder, you will end up giving away your cap table for work you did not actually receive.

So ask yourself: what do we truly need this person to do in the next 90 days?

Not “in theory.” Not “over a year.” The next 90 days.

If you can’t answer that in one plain sentence, you are not ready to offer equity yet. Start with a friendly trial period instead.

The simple structure that keeps you safe

A strong advisor agreement usually has a few core parts. I’ll walk you through them in plain language, like we’re reviewing the document together.

1) Role: what the advisor is actually doing

This should be written like a short job description.

Not long. Not fancy. Clear.

A good role section answers:

What topics will they advise on?

How often will you meet?

What kind of access will they have?

It also says what they are not doing.

This matters more than it sounds. Because if the role is wide and vague, you create room for drama later. The advisor might think they have a voice in hiring. Or pricing. Or product. Or funding. You might not agree.

So define it.

For example, if the advisor is there to help with enterprise sales intros, say that. If they are there for technical review, say that. If they are there for fundraising, say that.

And if they are not there to manage staff, make decisions, or speak for the company, write that too.

This section is a quiet pressure release valve. It stops ego battles before they happen.

2) Time: when the relationship starts and ends

Many founders forget this: an advisor deal should not be “forever.”

It should have a term. A start date and an end date.

Often, one year is fine. Sometimes two years if the advisor is truly active. But there should be an end point where you can renew if it’s working.

And you should include a simple way to end it early.

Because not every advisor fit will work out. People get busy. Priorities change. Life happens.

A clean ending clause makes it easy to part ways without a fight.

If you skip this, you may end up in an awkward spot where you feel trapped. And when founders feel trapped, they avoid the conversation. That’s how small issues become big.

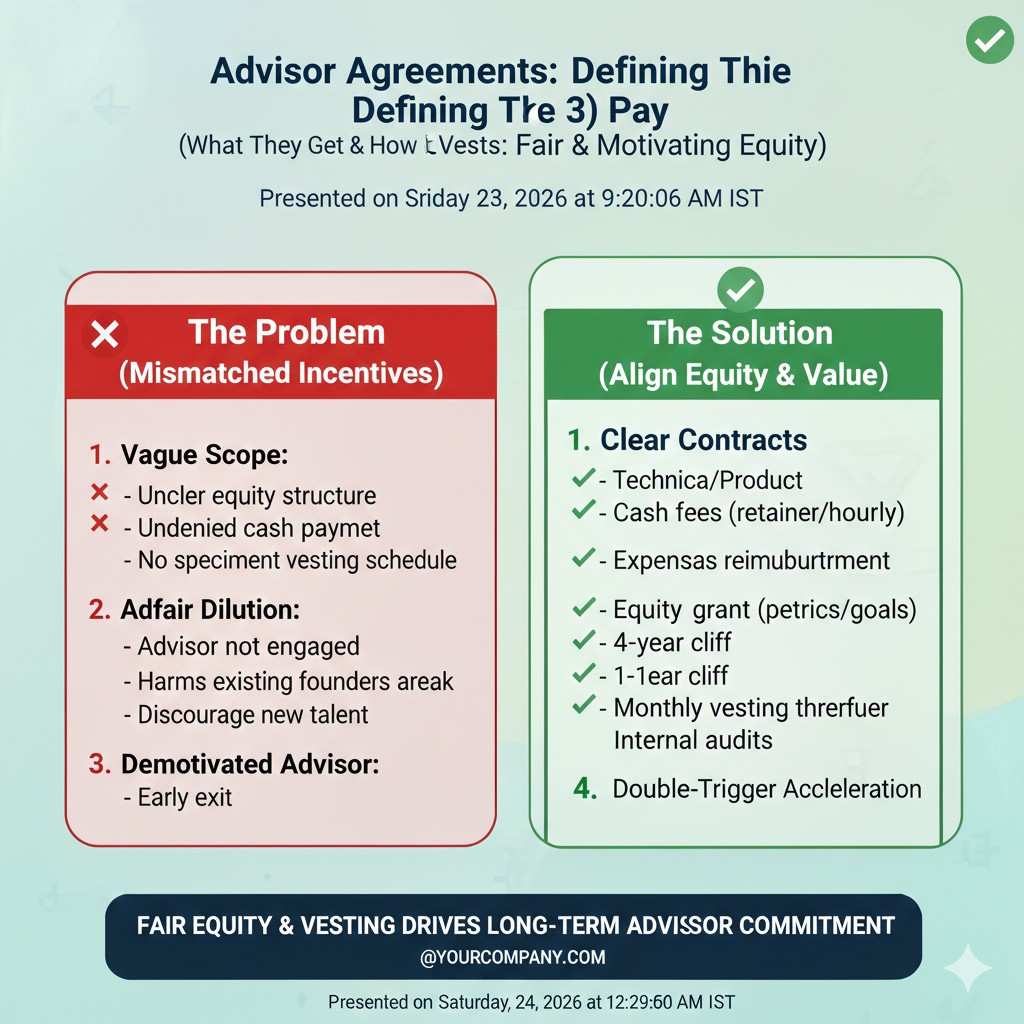

3) Pay: what they get and how it vests

This is where many founders either overpay or under-structure.

Most advisor pay is equity, not cash, early on. That’s normal. But equity should almost always vest over time.

Vesting means they earn it slowly, by staying involved.

Without vesting, you can give away equity on day one for help that never shows up later.

So your agreement should say:

How much equity they can earn

How long it takes to earn it

What happens if you end the relationship early

In simple terms: if they disappear, they don’t keep getting paid.

One more key point: many advisor agreements also include a short “cliff.” That means they earn nothing until they have stayed for a set time, like three months. After that, vesting starts.

Why is this useful? Because it gives you a real trial. It protects you from the “two good calls” advisor who then goes silent.

Now, I’m not giving legal advice here, but from a founder perspective, the mindset is: reward should follow proven value.

Also, if you are a deep tech startup, equity is not the only value at stake. Your patents and invention rights matter just as much, sometimes more.

Tran.vc is built around that idea: make your IP strong early so you don’t lose control later. If you want help building that foundation, you can apply anytime at https://www.tran.vc/apply-now-form/.

4) Confidential info: what they must keep private

This part is not about distrust. It’s about focus.

Advisors often advise more than one company. That’s fine. But you must set clear rules about your private details: your code, your roadmap, your customer list, your pricing, your pitch deck, your data.

So your agreement should say they must keep your private info private.

It should also say they must return or delete company materials when the relationship ends.

This is basic hygiene. Investors like hygiene.

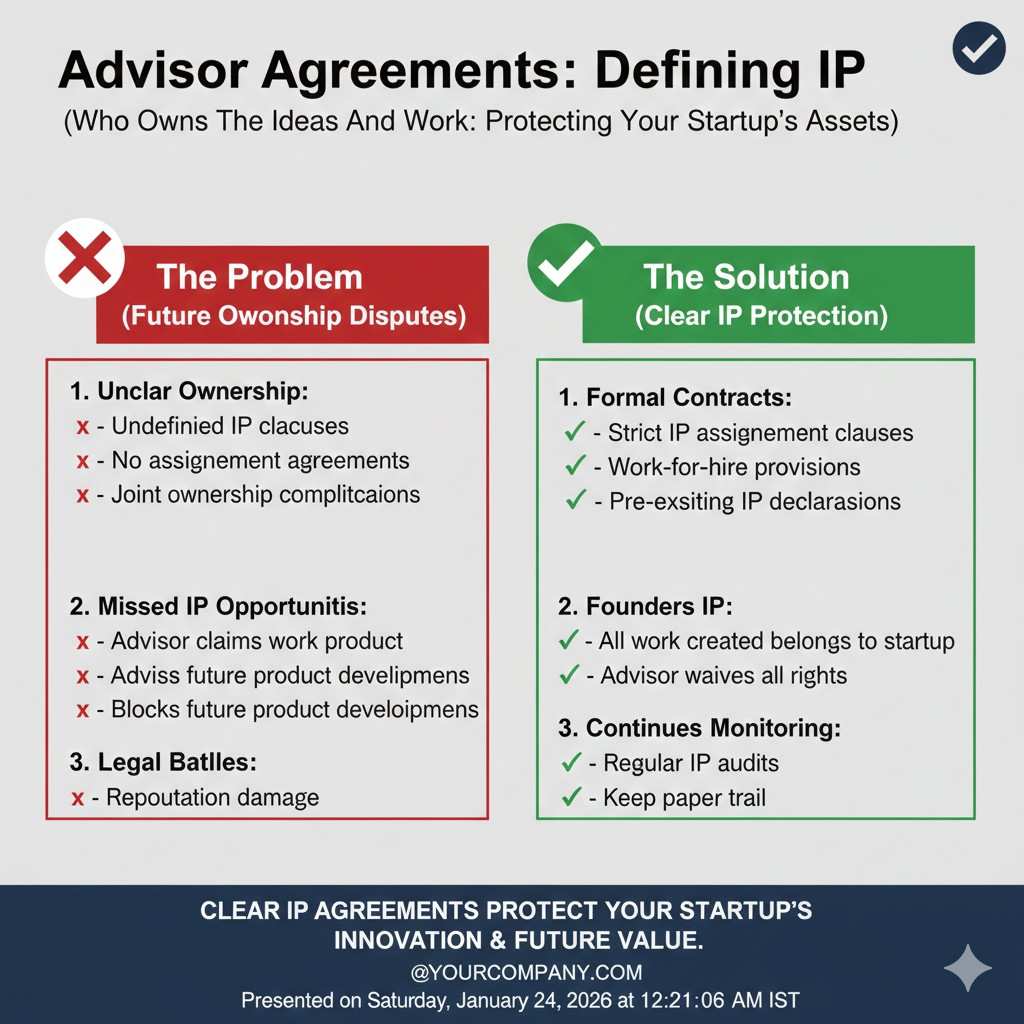

5) IP: who owns the ideas and work

This is the section that founders in AI and robotics cannot treat like a copy-paste checkbox.

Because advisors often give ideas. Sometimes those ideas are small. Sometimes they are huge. Sometimes they directly shape the invention.

If your advisor gives you a new approach, a key method, a model design, a system flow, or a new mechanism, you need the ownership to be clear.

A strong agreement usually says something like:

If the advisor creates work for the company, the company owns it.

If they help invent something tied to the company, the company has rights.

You want the company to own what is built for the company.

This does not mean the advisor gets nothing. They get their agreed equity. That is the trade.

But it does stop a nightmare scenario later: you file a patent, raise money, and then an advisor claims they are a co-inventor or that they own part of the core idea.

Even if you are “right,” fighting about it is expensive and distracting.

So you prevent it now, with clean paper.

This is also where Tran.vc can be a big help, because our whole model is built on making sure your IP story is strong and fundable early, not patched later. If you’re building real tech and want to protect it the right way, apply anytime at https://www.tran.vc/apply-now-form/.

6) Conflicts: what happens if they advise a competitor

This is another area where founders either go too soft or too strict.

You usually can’t stop an advisor from living their life. But you can set a clear rule: they should not advise a direct competitor while advising you, and they should tell you if a conflict shows up.

The goal is not control. The goal is clarity.

You don’t want to discover six months in that the advisor has been sharing “general advice” with two teams building the same thing.

That’s rare, but it happens.

So you write it down, kindly and clearly.

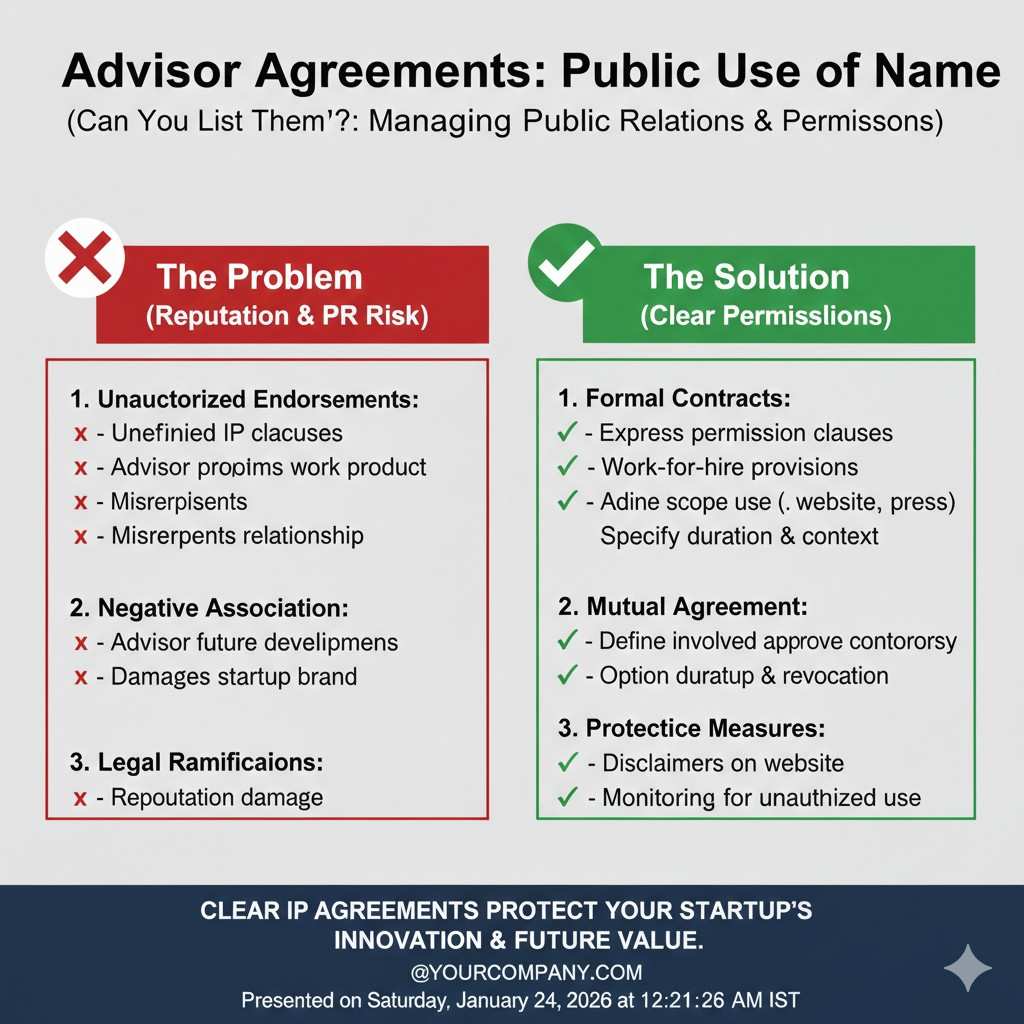

7) Public use of their name: can you list them?

Many founders put advisor logos or names on the website fast. That can backfire if the advisor did not agree, or if they later leave and you forget to remove them.

Your agreement should cover whether you can use their name, title, and photo, and where.

This also protects you if an advisor tries to distance themselves later, or if you want to keep your advisor list clean.

The hidden part: the conversation matters as much as the contract

If you want advisor relationships that work, the paper is only half the job.

The other half is the talk you have before you sign.

You want to cover:

What success looks like

How you’ll work together

What “good help” means to you

What they can realistically commit to

And you want to say one simple thing that changes everything:

“If this isn’t working for either of us, we’ll end it clean with no hard feelings.”

That sentence makes it safe to be honest.

When it’s safe to be honest, people do better work. And when the fit is wrong, it ends early instead of rotting slowly.

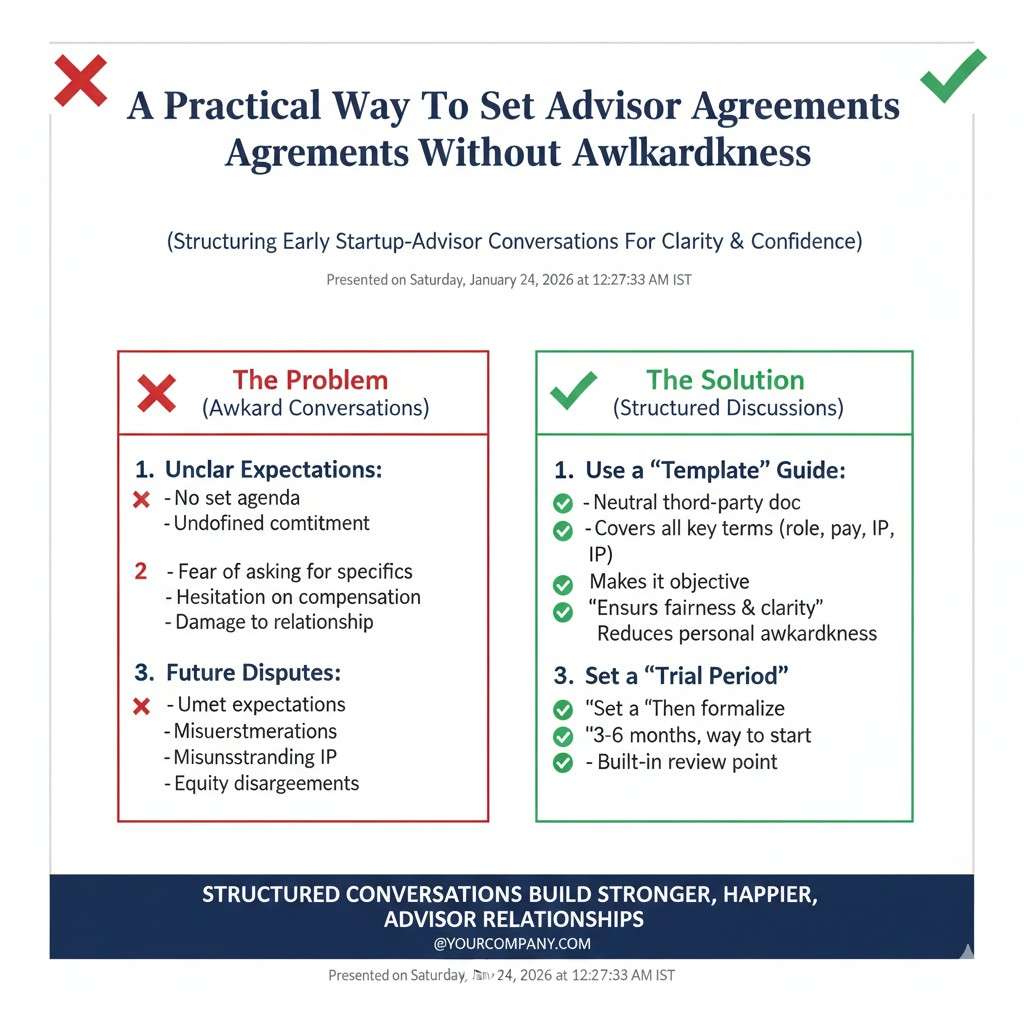

A practical way to set advisor agreements without awkwardness

Here’s a founder-friendly approach that works well:

Start with a short trial, even if informal. Two or three calls over one month.

See if the person shows up on time.

See if their advice is specific, not vague.

See if they follow through on intros.

See if they respect your time.

Then, if it’s working, you offer the formal advisor agreement with clear vesting.

This approach is fair to both sides. It stops you from doing a “hope deal.”

And it keeps your cap table clean.

The one thing investors check first

When investors review your cap table and documents, they often look for:

People with equity who don’t do real work.

Agreements that are missing or sloppy.

Anyone who might claim rights to the core tech.

Advisor agreements touch all three.

If you are building deep tech, your IP ownership story must be very clean. That is not a “later” problem. It is a “now” asset.

That is why Tran.vc exists. We invest up to $50,000 in in-kind patent and IP services so you can build a moat early, without giving up control too soon. If that sounds like what you need, apply anytime at https://www.tran.vc/apply-now-form/.

Advisor Agreements: Getting the Paperwork Right

Why this paperwork matters more than it seems

Advisor agreements look simple, but they touch the parts of your startup that investors care about most: ownership, control, and clean records. When the paper is missing or unclear, the company can feel “unsafe” to fund. That is true even if the advisor is helpful and well known. The risk is not the person. The risk is the confusion that shows up later when memories do not match.

A good agreement also protects the working relationship. It makes it easier to ask for help because both sides already know the rules. It reduces stress and avoids the awkward “wait, I thought…” talks that can ruin trust. Clear writing does not make the relationship cold. It makes it stable.

If your company is building AI, robotics, or deep tech, this is even more important. Advisors often shape the invention itself, even through casual feedback. When IP ownership is not written clearly, you can end up with problems during patent work or due diligence. If you want help building a strong IP base early, Tran.vc invests up to $50,000 in in-kind patent and IP services. You can apply anytime at https://www.tran.vc/apply-now-form/.

What an advisor agreement really does

At its core, the agreement is a trade written in plain terms. The company receives defined support, and the advisor receives a defined benefit. The document should explain what “support” means in your case, and what “benefit” means in their case. When those two parts are clear, the rest becomes much easier to manage.

The agreement also creates boundaries. Boundaries are not about mistrust. They are about keeping the advisor in the lane where they are strongest, without pulling them into day-to-day control. Startups move fast, and advisors often have strong opinions. The agreement helps you keep decisions with the founders while still using the advisor’s judgment in a useful way.

Start with the role before you talk about equity

Define the real job in simple words

Founders often jump straight to “How much equity should I offer?” That is the wrong first step. You need to decide what the advisor is actually doing, and what the company truly needs from them in the next few months. When the role is clear, the equity discussion becomes simpler and more fair.

A role should read like a short and realistic job description. It should explain what kinds of questions the advisor will help with, how often you will meet, and what access they will have. If you cannot describe the work in plain language, you do not yet know what you are paying for. That is a sign to slow down and test the relationship first.

This also stops a common future problem: the advisor acting like a decision maker. Many advisors do not mean to overstep. But when nothing is written, people fill gaps with their own assumptions. Your role section should make it clear the advisor is advising, not managing, not hiring, and not speaking for the company.

Separate “light help” from “hands-on help”

Not all advisors are the same, and treating them the same is how cap tables get bloated. Some advisors are best for quick guidance. They may do a call once a month and provide calm, high-level input. That can be valuable, but it is not the same as someone who is working with you weekly and driving real progress.

Hands-on advisors may review product plans, join sales calls, help with hiring, or help you avoid expensive mistakes. They are closer to the work and tend to influence outcomes more directly. Because they touch more of the company, the agreement must be tighter, and the expectations must be clearer.

When founders do not make this distinction, they often overpay for light support. Or they under-structure a hands-on relationship, which creates risk around IP and confidential info. Your paperwork should match the real level of involvement, not the advisor’s brand name.

Use a short trial when you are unsure

If you feel pressure to “lock in” a great advisor, it is tempting to sign too fast. A better approach is to start with a short trial period where you do a few meetings and see how the person works. This helps you learn if they show up, if their advice is specific, and if they can follow through on intros.

A trial also helps the advisor decide if they enjoy working with you. Many senior people want to help, but they also want to be honest about their time. A trial gives both sides room to say yes or no without drama. If it works, you can then move into a formal agreement with clear vesting and clear ownership rules.

Equity and vesting: pay for real value, not for hope

Why equity should almost always vest

Equity is not a thank-you gift. It is a long-term payment tied to long-term support. If you grant equity up front without vesting, you can end up giving away ownership for a short burst of excitement. That can harm the company later when you need clean structure for fundraising.

Vesting means the advisor earns equity over time by staying engaged. It also makes the relationship feel fair. If the advisor keeps showing up and helping, they earn what was promised. If they stop helping, the company does not keep paying for work that is not happening.

This is not about being strict. It is about aligning incentives with reality. A startup changes quickly, and the advisor fit might change too. Vesting gives you room to adapt without conflict.

How to think about a “cliff” in advisor deals

A cliff is a short period where the advisor earns nothing until they have stayed involved for a set amount of time. After the cliff, vesting begins. The cliff is useful because early relationships can feel good in the first one or two calls, but that does not always last.

With a cliff, you reduce the chance of “free equity” for someone who disappears early. It also creates a natural moment to check in. At the cliff point, you can ask: Is this working? Are we getting what we need? Is the advisor still excited? This keeps the relationship honest and avoids silent disappointment.

The cliff does not need to be harsh. It is simply a way to confirm the relationship has real momentum before equity starts to accrue. In many cases, that is better for the advisor too, because it sets a professional tone.

The right way to decide a fair equity range

Equity should reflect three things: how much time the advisor will spend, how hard it is to replace what they offer, and how early the company is. Early-stage companies often offer more equity because the risk is higher and cash is low. But “more” must still be reasonable.

A strong way to think about it is to tie equity to outcomes, not to status. If the advisor can directly move the company forward in ways that would otherwise take months, they may deserve more than someone who offers general advice. If they are making key intros that lead to real pipeline, or they help avoid a major technical mistake, their impact is real.

At the same time, you must protect the company’s future. Advisors should not end up owning a large chunk unless they are doing founder-level work. If you feel pulled toward a big number because the advisor is famous, pause and test the relationship first. Fame does not always translate into effort.

IP and invention rights: the part you cannot treat as “standard”

Why advisor feedback can become part of the invention

In deep tech, innovation is often built in conversations. An advisor might suggest a new method, a better system design, or a key improvement that changes how the product works. That might sound casual at the time, but it can become part of what you later patent or build into the core platform.

If your agreement does not address ownership of work and inventions, you risk disputes later. Even if the advisor is kind, they may remember the situation differently. Or they may later join a different company and feel they should be free to use “their” idea. Without clear terms, you are relying on goodwill alone.

Investors do not like goodwill-based ownership. They want documents that show the company owns what it is building. This is especially true when patents are involved, because patent work requires careful clarity around inventors and assignments.

What your agreement should say in plain terms

Your agreement should make it clear that work created for the company belongs to the company. It should also explain how inventions connected to the company will be handled, including signing papers needed for filings. The purpose is to keep the company’s IP story clean from the start, not to fight later when the stakes are higher.

This section should be written in a way that is understandable. If the language is too complex, founders tend to ignore it, and advisors may not realize what they are agreeing to. Simple language improves compliance because people actually read it and accept it with clear eyes.

This is one of the reasons Tran.vc focuses so heavily on early IP structure. If you are building AI, robotics, or other deep tech, and you want to protect your edge early, Tran.vc invests up to $50,000 in in-kind patent and IP services. You can apply anytime at https://www.tran.vc/apply-now-form/.

A practical habit that prevents future ownership fights

Even with a great agreement, you should build a simple habit: after important advisor sessions, send a short follow-up email summarizing what was discussed. Keep it polite and factual. This is not about “paper trails” in a paranoid way. It is about shared memory.

When you summarize key decisions and next steps, you reduce the chance of misunderstandings. You also create a natural record of what was suggested and when. If you later file patents or raise money, that kind of clarity helps. It also encourages advisors to stay focused on the topics where they are most helpful.