Founders move fast. You ship code, talk to users, hire friends, sign tools, take meetings, and try to keep the lights on. In that rush, it is easy to miss a quiet risk that can follow you for years: personal liability. That is when a problem in the company lands on you as a person—your savings, your home, your future paychecks.

This article will show you how to reduce that risk early, while your startup is still small and messy. I’ll keep it simple, direct, and practical. And since Tran.vc helps technical teams protect what matters from day one, I’ll also point out where strong IP and clean paperwork can make your company safer and easier to fund. If you want that kind of help, you can apply anytime here: https://www.tran.vc/apply-now-form/

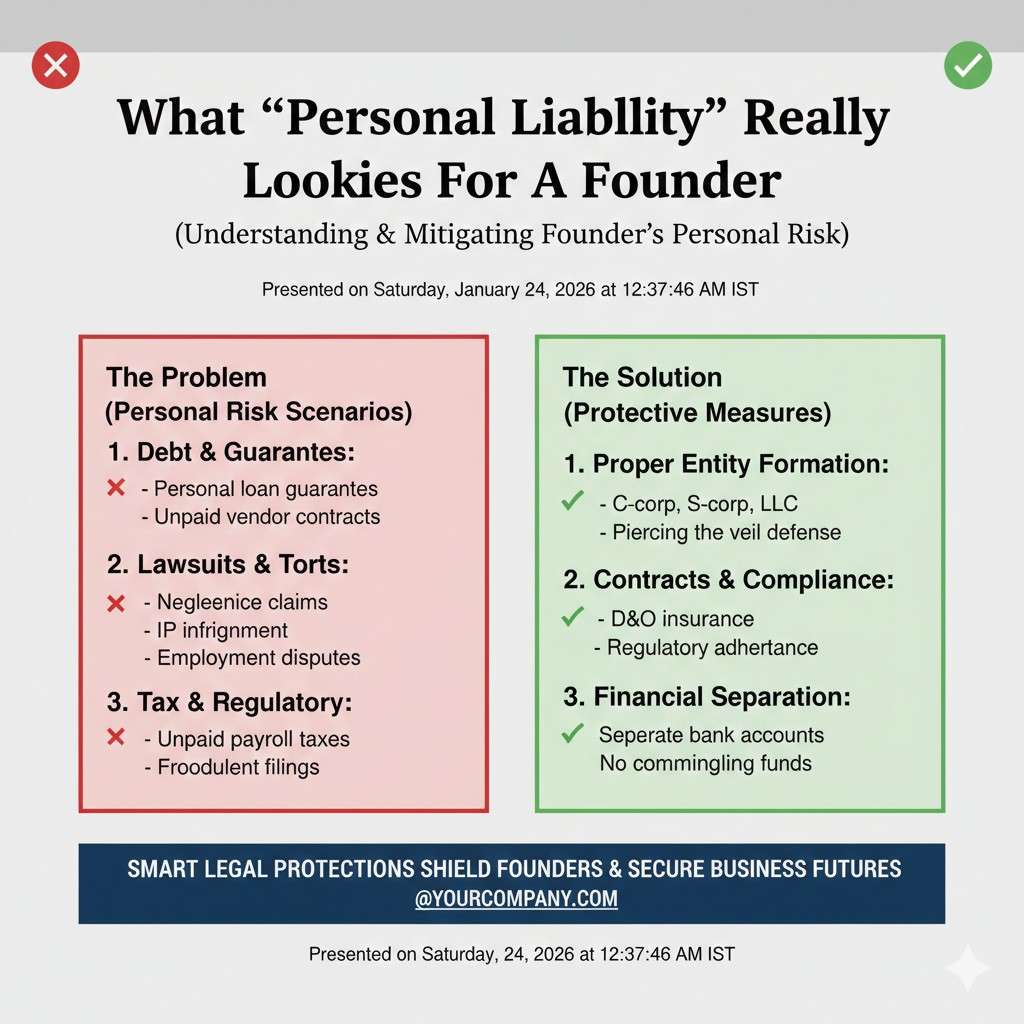

What “personal liability” really looks like for a founder

A lot of founders hear “limited liability” and relax. “I formed an LLC” or “we’re a C-Corp now,” so I’m safe. That is a good start, but it is not the whole story.

Personal liability usually shows up in a few common ways:

It shows up when you sign something in your own name, not the company’s name. It shows up when you promise to pay if the company cannot. It shows up when you mix your personal money with company money. It shows up when you cut corners on taxes and payroll. It shows up when you sell something risky without basic safety steps. It shows up when you use code, images, or data that you do not have rights to. It shows up when you raise money the wrong way and someone claims you misled them. It shows up when a contractor says, “You hired me, not the company,” because that is what the paper says.

The hard part is that most of these risks don’t feel urgent in the moment. The urgent thing is “close the deal,” “ship the demo,” “pay the rent,” “get the pilot.” Liability is usually a slow leak. Then one day, it becomes a flood.

So the goal is not to be paranoid. The goal is to build a few simple habits early so your company, not you, holds the risk.

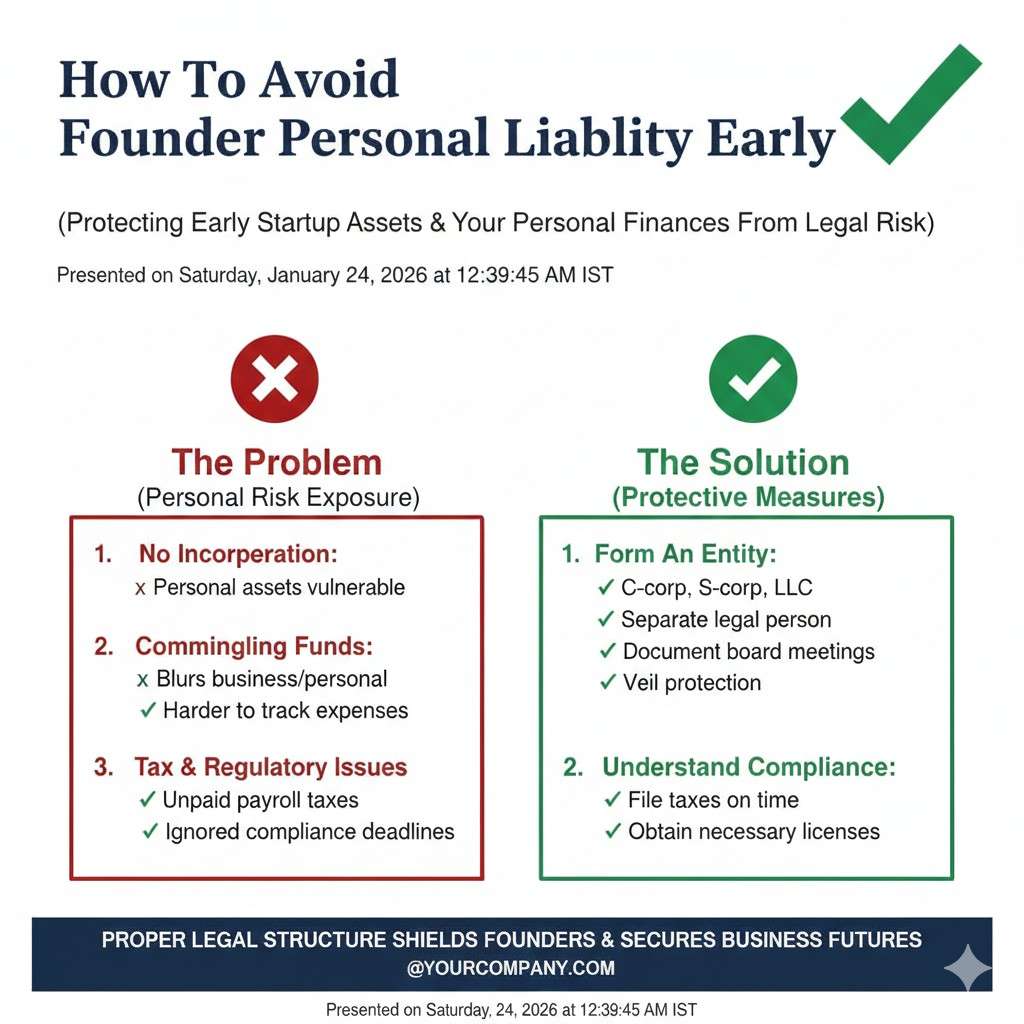

Step one: make sure the company exists in the real world, not just in your head

If you are still building before you incorporate, you are not alone. Many teams do that. But understand the trade: if there is no company, then you are the company. Any promise you make is your promise.

If you have not formed a legal entity yet, treat every action like it could be read out loud later by a lawyer. Because it might be.

Even after you incorporate, you still need to act like the company is a real separate thing. This is where many founders slip. They form a company, then keep working like a solo freelancer.

Here is the simple way to think about it: your company must have its own “body.” It needs its own bank account, its own contracts, its own records, its own money flow, its own decision trail. If everything still runs through your personal life, it is easy for someone to argue the company is just a mask. That is how founders lose the shield they thought they had.

A clean setup is not fancy. It is basic:

Your company has its own bank account, and you use it. Your company has its own card, and you use it for company costs. When you pay yourself, you pay yourself in a clear way (payroll or a documented transfer). When you sign something, you sign as the company. You don’t “borrow” company money for personal bills. You don’t pay company bills from your personal account “for now” every week.

Yes, people do it. Yes, it feels harmless. It is also the kind of detail that becomes painful in disputes, audits, investor checks, and exits.

If you are already messy, that is okay. Clean it up now, while the volume is low. It is much harder later.

And if you want Tran.vc’s team to help you build a clean foundation early—legal, IP, and structure—apply here: https://www.tran.vc/apply-now-form/

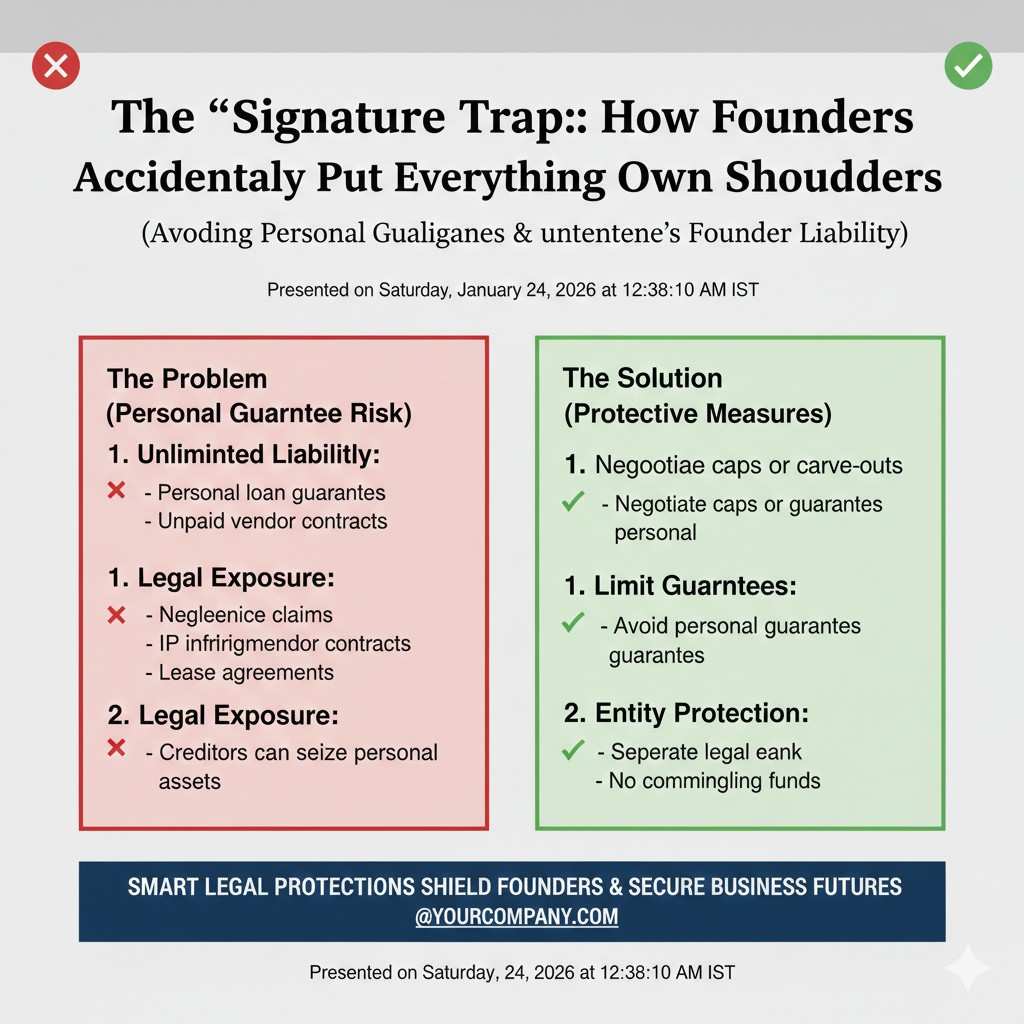

The signature trap: how founders accidentally put everything on their own shoulders

One of the fastest ways to create personal liability is very simple: you sign the wrong way.

Founders often sign a contract like this:

“John Smith”

instead of

“Acme Robotics, Inc., by John Smith, CEO”

That tiny difference matters.

If the contract is in your name, or if the signature line is sloppy, the other side may claim you agreed personally. And even if you meant the company, arguments cost time and money. The more money involved, the more aggressive people can get.

There is another trap that is even more direct: a personal guarantee.

This often shows up in leases, equipment financing, cloud credits, even some vendor tools. The vendor says, “We’ll do it, but only if you guarantee payment.” You want to move fast, so you sign. If the company fails, they can come after you.

Sometimes a guarantee is worth it. Often it is not. The key is to treat it like what it is: a personal debt. Not a normal startup expense.

If you feel pressure, pause and try a different move:

Ask for a smaller commitment. Ask for a shorter term. Ask for monthly payments instead of annual. Ask for a deposit instead of a guarantee. Ask if they can accept a company-only obligation with higher pricing. Ask if they can tie it to a milestone. Ask if they can limit the guarantee to a fixed amount and time window.

Many vendors start with “guarantee” because it is easy for them. It does not mean it is the only deal.

Also watch the fine print on “click to accept” tools. Some terms try to bind the person clicking. Use a company email. Make sure the account owner is the company. Save the invoices. Keep the trail.

You don’t need to be dramatic. You just need to be steady.

Co-founder risk: the liability you inherit from the person next to you

This part is uncomfortable, but it matters early.

If you have a co-founder, you are linked. If they make a promise, you may still suffer. If they misuse someone else’s code, you may still suffer. If they pitch investors with claims that are not true, you may still suffer. If they treat a contractor badly, you may still suffer. Even if you did not know, the company gets hit, and then the company’s problems become your problems.

The fix is not “don’t trust anyone.” The fix is to set basic rules while you still like each other.

Your roles should be clear. Who can sign contracts? Who can spend money? Who can hire? Who can approve open-source use? Who can talk to investors? Who controls the cap table? Who is the admin on the bank? Who owns the domain? Who owns the GitHub org?

If you skip this, the default is chaos. And chaos creates liability.

You want one simple practice: major actions require a record. It can be a board consent, a founder consent, or even a signed memo. It does not need to be long. It needs to exist.

This is not “big company behavior.” This is “protect the team behavior.”

Employment and contractors: where founders get hit hardest, fastest

Early teams hire in the easiest way possible. Someone helps for a month. You pay them. Everyone is happy. Then something breaks.

This is a major personal liability zone because founders do two risky things early:

They pay people in a casual way, without clear terms.

They treat people like contractors when the law treats them like employees.

Misclassification can create back taxes, penalties, and personal exposure in some places. Payroll taxes are not a game. Governments take them seriously.

Here is the simple approach:

If someone is working like an employee—fixed hours, your equipment, your direction, ongoing work—don’t pretend they are a contractor just because it is simpler. Talk to a lawyer or a payroll provider and do it right. Even if you start part-time, get the structure right.

If you do use contractors, you need three things early:

First, a written contract that says they are a contractor and spells out payment, scope, and timing.

Second, an IP assignment clause that says anything they build for you is owned by the company.

Third, proof that they used their own tools and control over how they work (where applicable).

The biggest mistake is assuming, “If I pay for it, we own it.” That is not always true.

This matters even more in AI and robotics, because the value is in what you build. If your codebase is not cleanly owned by the company, you can lose deals, lose funding, and walk into fights later. It can also weaken patents if inventorship and ownership are messy.

Tran.vc exists in part to stop this kind of pain early. If you’re building defensible tech and want help making sure the company owns what it should own, apply here: https://www.tran.vc/apply-now-form/

IP problems can become personal problems

Founders sometimes treat IP like “later.” Later is often too late.

Here is why IP connects to liability:

If you take code that you do not have rights to, you may face claims.

If you use open-source wrong and break license rules, you may face claims.

If you copy a competitor’s method or design, you may face claims.

If you use a dataset without proper rights, you may face claims.

If you promise customers “we own this” but you do not, you may face claims.

Many of these are company-level claims at first. But personal liability can creep in when someone says you personally knew, personally directed it, or personally made false statements. Even if you ultimately win, the process can be brutal.

The simple habit is this: treat IP like inventory. Know where it came from. Know who made it. Know who owns it. Keep records.

For software teams, keep a basic log of major open-source components and licenses. Don’t wait until a big customer asks. By then you are scrambling. Use a simple policy: no copy-paste from unknown sources into production. If a developer wants to use a library, they note it and its license. That’s it. Not heavy. Just real.

For robotics teams, it goes beyond code. It includes CAD files, firmware, schematics, control systems, and test data. It includes who designed what, and when. It includes whether an advisor is contributing “ideas” that could later become an inventorship fight.

And here is the part many founders miss: if you plan to file patents, you want clean invention records and clean ownership from day one. Patents can make your company safer by building a moat and making your story stronger. But messy inventorship and unclear assignments can create disputes that get personal fast.

Tran.vc invests up to $50,000 in in-kind IP and patent services to help teams avoid these traps early—before outside money, before big customers, before things get hard to change. Apply here: https://www.tran.vc/apply-now-form/

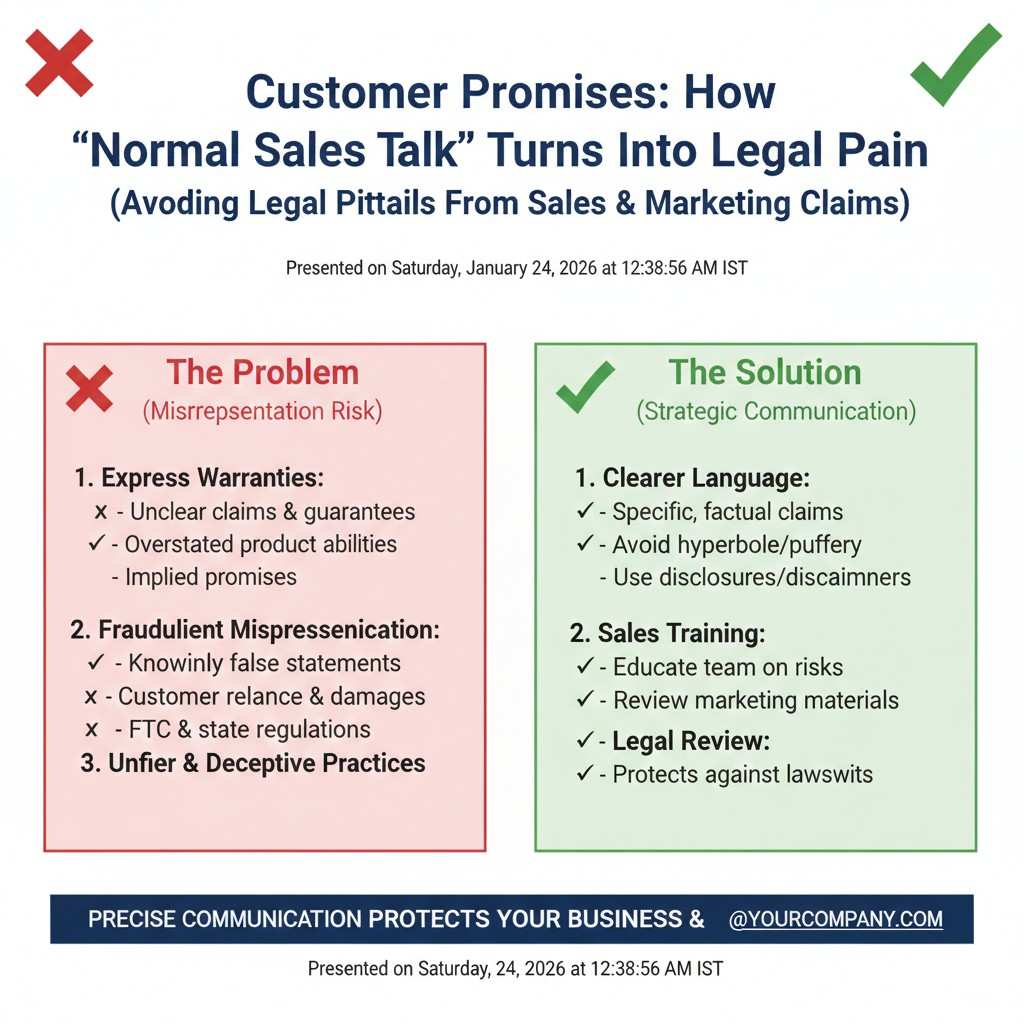

Customer promises: how “normal sales talk” turns into legal pain

Early founders sell with energy. That is good. But there is a line between strong positioning and risky promises.

Personal liability risk increases when you:

Promise performance you cannot support.

Promise compliance you have not earned.

Promise timelines you know are guesses.

Promise security you have not built.

Promise ownership you do not have.

Promise “we do not use customer data” when you do.

Promise “we are insured” when you are not.

Promise “we will indemnify you” without knowing what that means.

A founder might say, “It’s fine, it’s just talk.” But sales emails, pitch decks, and recorded calls can become evidence.

The fix is not to become timid. The fix is to be precise.

When you don’t know, say “target” instead of “will.” Say “we plan” instead of “we guarantee.” Say “we’re working toward” instead of “we are compliant.” If you are in a pilot, label it a pilot. If something is experimental, say so. If a feature is on the roadmap, call it a roadmap item.

Also, read your own contract templates with one goal: remove personal promises.

Make sure the company is the party. Make sure there is a clear limitation of liability. Make sure there is no random sentence that says you personally stand behind it.

This is one reason getting counsel early matters. Not because you want to spend money on legal. Because one bad clause can cost more than a year of legal work.

Insurance: the boring shield that founders wish they bought sooner

Most founders delay insurance because it feels like something you buy after product-market fit. But certain types matter early, especially if you are selling to businesses.

For founder liability, the key idea is not “buy everything.” The key idea is “buy what covers the most likely early hits.”

If you have employees, workers’ comp may be required depending on where you are. If you are selling B2B, you may need general liability. If you are handling customer data, cyber coverage might matter. If you have a board and investors, D&O insurance can become important. If you are shipping hardware, product liability can matter.

I’m not going to throw a giant list at you. The actionable move is this: talk to a broker who works with startups, tell them what you build and who you sell to, and ask what is common at your stage. Then compare cost to risk.

Also, some customers require proof of coverage. If you can’t provide it, you lose deals. When deals slip, founders make desperate choices, like signing personal guarantees. So insurance can reduce liability in indirect ways too.

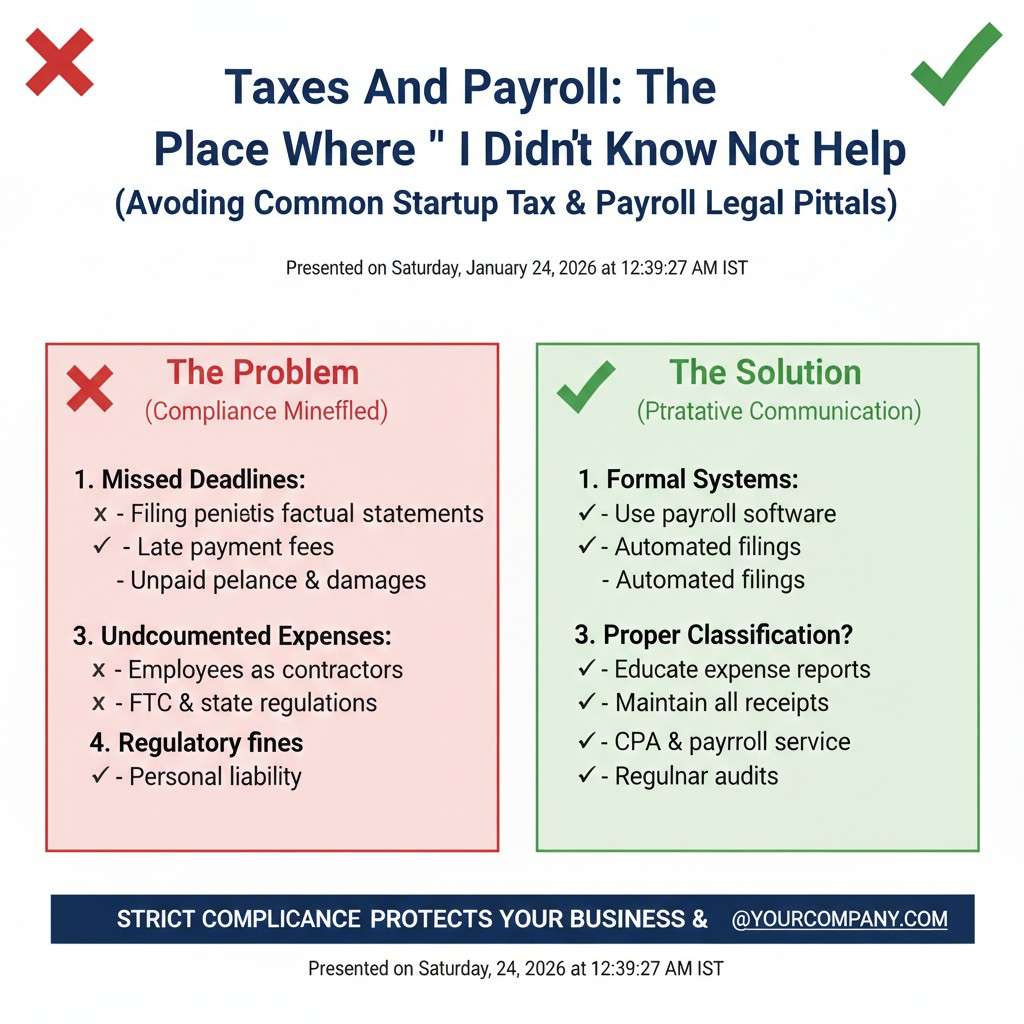

Taxes and payroll: the place where “I didn’t know” does not help

If you remember one thing from this article, remember this: do not get casual with payroll taxes.

In many places, unpaid payroll taxes can create personal liability for officers and people in control, even if the company is broke. This is not like a normal bill. This is money you withhold and owe to the government. The rules are strict.

If you are paying yourself and others, use a real payroll system. If you cannot afford payroll, consider reducing pay, switching to part-time, or pausing hiring. But don’t keep paying contractors like employees in the shadows. Don’t skip filings. Don’t ignore notices.

Also be careful with sales tax, VAT/GST, and similar taxes depending on where you sell. Software and hardware can trigger different rules in different places. The easiest path is to use a basic accounting setup early and get professional help before you scale.

This is not about being perfect. It is about not stepping into the few areas where the consequences are harsh.

“Piercing the veil”: how founders lose limited liability

You may have heard this phrase. It sounds dramatic. But the idea is simple.

If you treat the company like it is not separate from you, a court may treat it that way too. That can open the door to personal liability.

Common reasons include mixing funds, not keeping records, under-capitalizing the company while taking money out, using the company to mislead, or signing personally.

You don’t need to memorize legal doctrine. Just keep your separation clean:

Company money stays company money.

Company decisions have a basic paper trail.

Company contracts are signed by the company.

Company assets (like domain, repo access, trademarks, patents) are owned by the company, not by you personally.

Company communications are done with company email where it matters.

This is not about playing dress-up. It is about making your company real.

How to Avoid Founder Personal Liability Early

Why this matters more than most founders think

When you build a startup, you are building two things at the same time. You are building a product, and you are building a legal and money system around that product. If the system is weak, the risk does not always stay inside the company. It can slide onto you as a person.

Personal liability is not just a scary legal phrase. It is what happens when a problem becomes your personal problem. It can mean your personal savings get pulled in. It can mean your personal credit gets hit. It can mean years of stress even after the company is gone.

The good news is that early protection is often simple. It is not about doing everything. It is about doing the few things that stop the most common disasters.

The goal: keep risk inside the company

A startup should be a separate “box.” The deals, debts, and mistakes should live inside that box. Your job is to keep the walls of the box strong, even while you move fast.

This is also where clean IP work helps more than people think. When ownership is clear, and records are clean, it reduces fights. It also makes investors calmer, because fewer loose ends means fewer surprises later.

If you want help building that clean foundation early, Tran.vc supports deep tech teams with up to $50,000 in in-kind patent and IP services. You can apply anytime: https://www.tran.vc/apply-now-form/

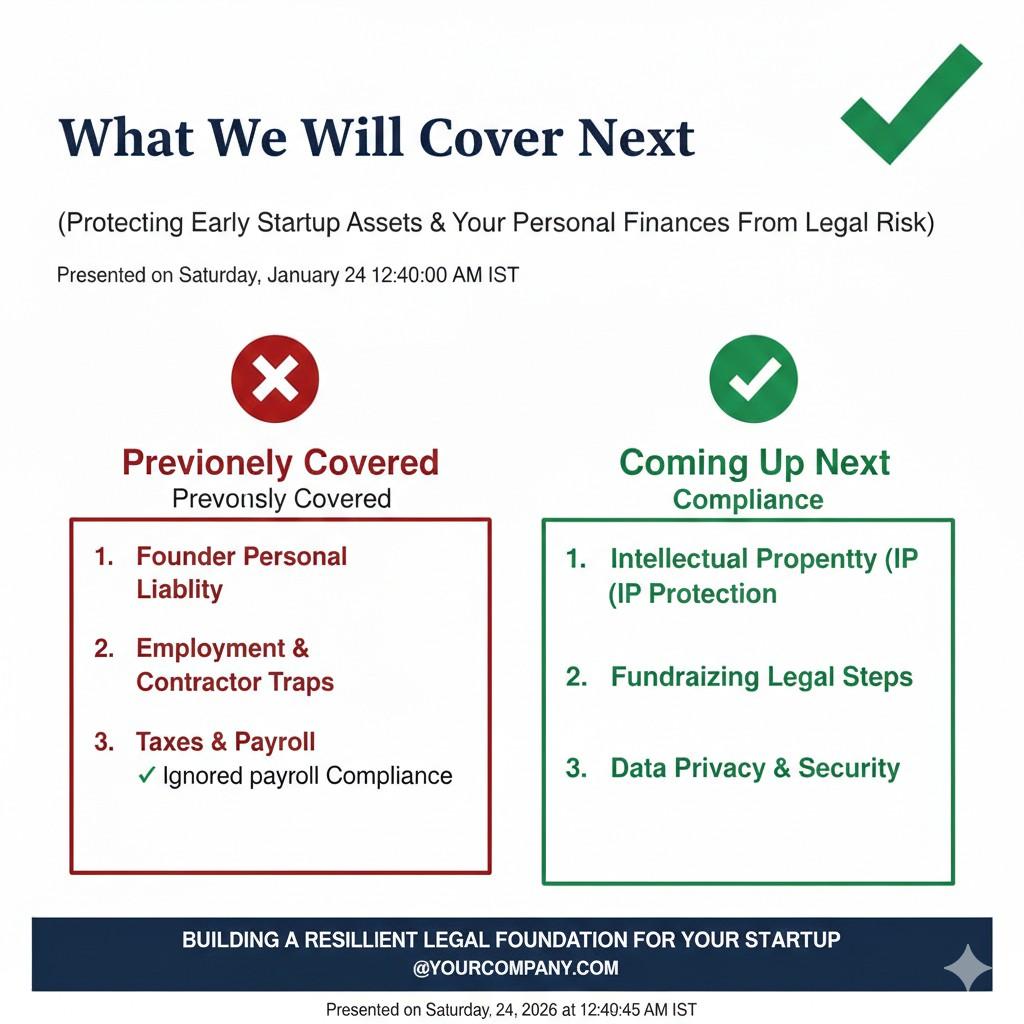

What we will cover next

From here, we will go step by step through the real traps founders fall into. We will focus on contracts, money, hiring, taxes, IP, customer promises, and the small habits that reduce risk.

This will stay practical. No fancy legal talk. Just what to do, what to avoid, and how to set your company up so it can grow without putting you in the line of fire.

Understand what “personal liability” looks like in real life

The most common ways founders get exposed

Many founders think forming an LLC or a corporation makes them safe. It helps, but it does not fix everything by itself. Personal liability usually shows up through small actions that feel normal in the moment.

It often starts when you sign something in your own name, not the company’s name. It can happen when you promise you will pay if the company cannot. It can happen when you mix personal money and company money in messy ways.

It can also show up through taxes, payroll, and worker rules. Those areas have strict rules and strict penalties. Even if you did not mean harm, the system may still hold you responsible.