Most founders do accounting the way they do laundry in college: only when they run out of clean clothes. It works—until it doesn’t.

If you ever plan to raise venture money, sell your company, or even bring in a serious angel, your books stop being “an admin task” and become proof. Proof that you know what you spend. Proof that your numbers match reality. Proof that your company is not hiding risk inside messy files and missing receipts.

This guide is about setting up clean accounting early so VC diligence later feels boring. Boring is good.

And if you are building deep tech—AI, robotics, hard tech—clean books matter even more because you will spend on contractors, cloud, labs, parts, legal, patents, and long build cycles. That mix creates confusion fast if you do not design a simple system up front.

Quick note: Tran.vc helps technical founders build real moats with strong IP from day one, by investing up to $50,000 in in-kind patent and IP services. If you want support building an IP plan that investors respect, you can apply anytime here: https://www.tran.vc/apply-now-form/

What VCs really mean by “clean books”

A VC does not expect you to have Big Company finance. They do expect three things:

- Your books match your bank.

If your accounting says you have $72,114 and your bank says $61,909, they will assume you do not know where money goes. That is a trust problem, not a math problem. - Your categories make sense.

If every cost is “misc” or “software,” it signals you are not watching burn. VCs want to see that you can steer. - You can answer basic money questions fast.

“How much are you spending each month?”

“What is payroll vs non-payroll?”

“How much went to contractors?”

“What did you spend on cloud?”

If you need two weeks and three panic attacks to answer, diligence becomes a mess.

Clean accounting is not “perfect.” Clean accounting is “clear.”

The real goal: no surprises

Diligence is less about the numbers and more about surprises. Surprises kill deals. Examples:

- You told them your burn is $35k, but the real burn is $55k because you forgot annual software renewals.

- You said you own your IP, but contractor payments were done with no signed agreements (this is both a legal and accounting mess).

- You claimed revenue, but invoices do not match bank deposits.

- You used one card for personal and company buys, and now no one knows what is what.

If you set up accounting the right way now, you remove surprise later. You also make your own life calmer every month.

Start with the foundation: separate everything

This sounds basic, but it is the #1 thing that breaks early-stage books.

Open a company bank account.

All money in and out goes through it. No exceptions.

Get a company card.

Even if the limit is low. Use it for company spend. If you buy something personal by mistake, reimburse the company and note it clearly.

Do not pay vendors from your personal account.

When a founder does this “just once,” it becomes a habit. Later, diligence becomes a detective story.

If you already mixed spending, you can still fix it. But it will take time, and you will hate past you.

Choose a simple accounting tool and lock it in

Most VC-backed startups use QuickBooks Online, Xero, or a similar tool. The tool matters less than consistency. Pick one, set it up properly, and stop bouncing around.

Here is the part founders miss: the tool is not “set it and forget it.” The setup choices you make in week one decide whether your reports are useful in month twelve.

So do it with intention.

Your chart of accounts should be boring

A “chart of accounts” is just your money buckets. Each transaction lands in a bucket. The buckets should tell a story.

Founders often do one of two wrong things:

- They make 200 buckets because they want detail.

- They make 5 buckets because they want simplicity.

Both can fail.

Too many buckets means no one uses them well. Your bookkeeper will guess. Guessing creates noise.

Too few buckets means your reports do not help you make choices.

A good startup chart of accounts is small, clear, and built around how you will talk to investors.

Think in terms of questions you will be asked:

- How much is payroll?

- How much is contractors?

- How much is cloud and tools?

- How much is legal and IP?

- How much is travel and events?

- How much is equipment and parts?

- How much is rent or coworking?

- What is “one-time” vs “every month”?

You do not need dozens of line items. You need the right ones.

For deep tech teams, I strongly suggest you separate these cleanly:

Payroll

Employees only.

Contractors

And if you use many contractors, track them well by vendor, not by tiny expense buckets.

Cloud / compute

This is often a top 3 cost for AI teams.

Software tools

Not cloud. Keep it separate. Things like Slack, Notion, GitHub, Figma, etc.

Lab / parts / equipment

Robotics teams: this is where things get messy fast. Put it in its own lane.

Legal & IP

Very important. Investors want to see you treat IP as a real asset. Also, it helps you understand your true cost to build a moat.

Tran.vc’s entire model is built around this: turning your inventions into protected assets early. If you want to build that protection without giving up control too soon, apply anytime: https://www.tran.vc/apply-now-form/

Marketing

Even if it is near zero.

Insurance

Many startups forget this until it becomes urgent.

Travel

Keep it separate.

Meals

Separate from travel.

Rent / coworking

If you have it.

Other

Yes, one “other” is fine, but you should review it monthly and move items out if it grows.

This structure helps you answer diligence questions without doing gymnastics.

Decide your accounting method early: cash vs accrual

Most tiny startups run “cash basis” accounting because it is easier. Money out is expense, money in is revenue.

But VCs and buyers often prefer “accrual basis,” where you record expenses and revenue when they happen, not just when cash moves. Example: you pay an annual tool bill in January. On cash basis, January looks expensive. On accrual basis, it spreads across 12 months.

What should you do?

If you are pre-seed and tiny, cash basis is fine. But you should still track big annual bills clearly so you can explain burn.

If you have revenue, or you plan to raise soon, or you want clean monthly reporting, talk to a bookkeeper about moving to accrual. Many startups start cash and shift later. That is normal. The key is to be consistent and document the switch.

VC diligence does not punish cash basis. It punishes confusion.

Create a monthly close habit (and keep it small)

“Monthly close” sounds like a corporate thing. It is not. It is just a rhythm:

- You import all transactions.

- You categorize them correctly.

- You match them to receipts or invoices.

- You reconcile bank and card statements.

- You review basic reports.

That is it.

The magic is not doing it once. The magic is doing it every month. When you skip three months, the cleanup becomes painful and errors pile up.

A clean close should take hours, not weeks.

If you do not have a finance person, do a “micro close” every two weeks. Even 30 minutes helps. The point is to stop the mess from growing.

Receipts are not optional in diligence

This is another founder trap. You think receipts are a tax thing. They are also a diligence thing.

In diligence, someone may sample your expenses to see if they look real and reasonable. If you cannot back up charges, they worry about controls. It raises questions like: “Are there hidden personal expenses?” That is the last thing you want.

Simple system:

- Every card purchase gets a receipt uploaded.

- Every invoice gets saved.

- Every contract gets stored.

- Every reimbursement has proof.

Use a tool like Dext, Expensify, Ramp, Brex, or even a shared drive system if you are very early. The tool matters less than the habit.

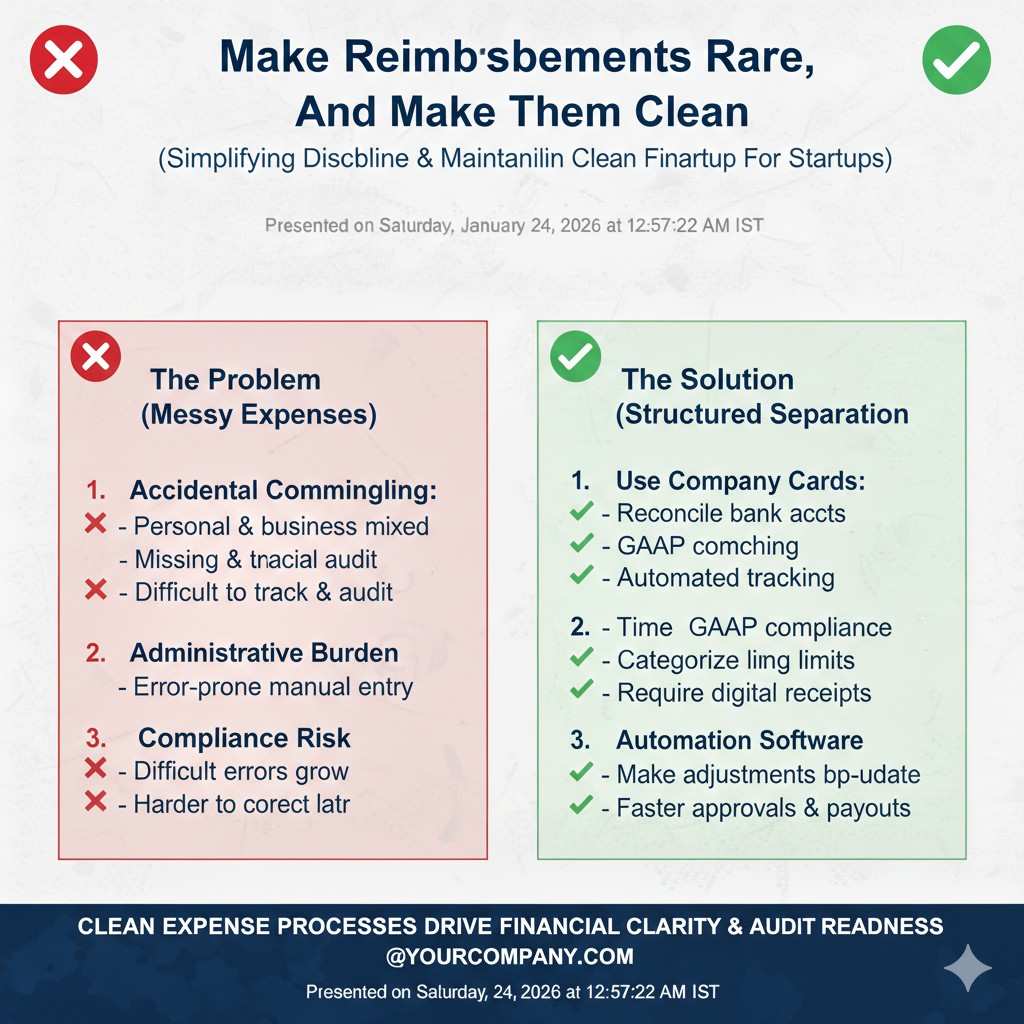

Make reimbursements rare, and make them clean

Founders love reimbursements because they feel flexible. VCs hate them because they hide messy spending.

If you must do reimbursements:

- Use a simple form.

- Attach receipts.

- Write the business reason in plain words.

- Pay it quickly.

- Record it clearly as reimbursement, not as a random expense.

Also, do not reimburse through weird methods. Use the company bank account. One clean trail.

Reconcile like your deal depends on it (because it does)

Reconciliation means your accounting matches your real bank and card statements.

If you do not reconcile, your reports are fiction. A VC will not say that to your face. They will just slow down, dig deeper, and sometimes walk away.

Make reconciliation non-negotiable. It is the simplest way to keep trust.

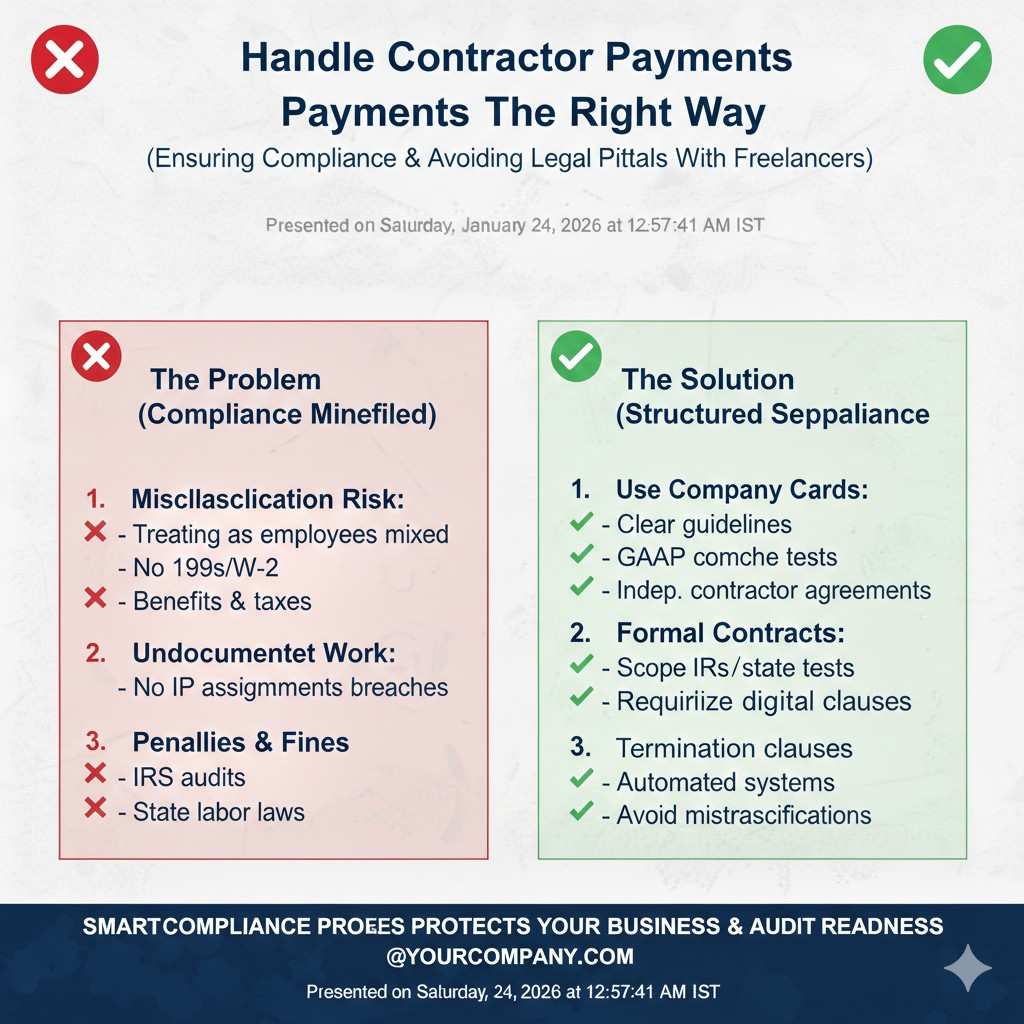

Handle contractor payments the right way

Deep tech startups rely on contractors. Diligence teams look at contractors for two reasons:

- Cost control

- IP and legal risk

On the accounting side, be consistent:

- Pay contractors through the same method each time.

- Put them in the same category each time.

- Keep invoices and statements.

On the diligence side, you also need clean agreements. This is where IP and accounting connect.

If you pay a contractor who wrote code, designed hardware, trained models, or created product designs, and you do not have an agreement that assigns work to the company, you may not fully own what you built.

That is a huge red flag.

Tran.vc focuses on helping founders build defensible IP early—patents, strategy, and clean foundations that investors respect. If you want help turning your tech into protectable assets while keeping control, apply here: https://www.tran.vc/apply-now-form/

Track legal and IP spend in a way that tells a story

When you raise, investors will ask:

- What have you spent on legal?

- What have you spent on IP?

- What did that get you?

If your books mix IP work into “legal misc,” you lose an easy credibility win.

Even if you do not spend much, separate it. It signals maturity. It also helps you budget for the next steps: filings, office actions, international plans, and ongoing strategy.

If Tran.vc is your partner, those services may be in-kind. You still want to track them properly so you can explain the value you received. That value is real. It is part of your moat story.

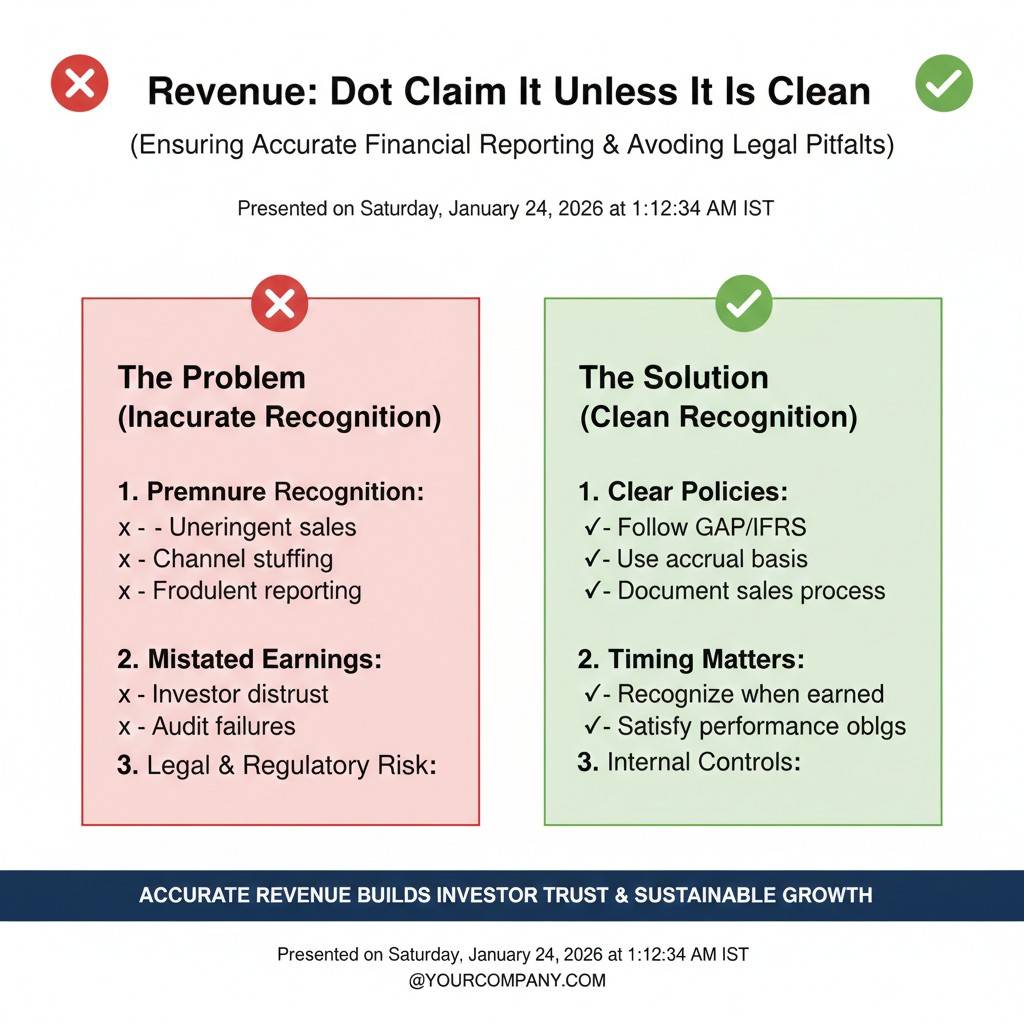

Revenue: do not claim it unless it is clean

If you have paying customers, the biggest diligence pain is messy revenue tracking.

Common mistakes:

- Money comes in, but there is no invoice.

- Invoices exist, but they do not match deposits.

- Deposits are bundled (Stripe payouts) and no one can break them down.

- Refunds and chargebacks are not tracked cleanly.

Clean system:

- Every payment ties to a customer record.

- Every invoice ties to a payment or a clear “unpaid” status.

- Stripe or other processors get reconciled monthly.

- You separate revenue from “other income” like grants or rebates.

Do this early and diligence becomes easy.

Grants, credits, and “free money” still needs clean tracking

Many robotics and AI teams get grants, research funds, or cloud credits. Those are great, but only if tracked clearly.

- Grants may have restrictions.

- Credits may expire.

- Some funds must be used for certain costs.

If you cannot show clean tracking, it creates risk.

Even if the amounts are small, treat them with respect. Investors notice.

Clean Accounting Setup for Future VC Diligence

1) Set the goal before you pick the tools

What you are really building

You are not “doing bookkeeping.” You are building a record that another adult will trust without knowing you. In diligence, investors do not have time to guess what you meant. They want to see a clean trail that explains how you earn, how you spend, and what you still owe.

When your setup is clean, your story becomes simple. When your setup is messy, every number turns into a debate. That debate slows the round and makes people nervous, even if your product is strong.

What “future-proof” looks like

Future-proof accounting means the basics are always correct, month after month. Your bank balance matches your books. Your invoices match deposits. Your bills match vendor statements. Your payroll matches filings. Nothing is hidden in random buckets.

You also want your setup to be easy to maintain. If it takes too much effort, you will stop doing it. The best accounting system is the one you can keep running even during a hard sprint.

A quick promise to yourself

Make a decision now that you will never let accounting fall behind more than one month. This one rule prevents most founder finance disasters. It also makes taxes cheaper, because your accountant is not forced to untangle a year of confusion.

If you are building deep tech and also doing IP work early, this matters even more. Clean financial records help you show that your moat is real, not just words. If you want help building that IP moat with real patent and IP services, you can apply anytime at https://www.tran.vc/apply-now-form/

2) Build the “separation wall” first

Separate money like your deal depends on it

The fastest way to lose investor trust is mixing personal and company spending. It does not matter if you meant well. In diligence, mixed spending looks like weak controls, and weak controls look like risk.

Set the rule that all company money stays inside company accounts. It sounds strict, but it is actually freeing. You stop wondering if a charge was “okay.” You stop hunting for receipts in your personal email. You stop explaining basic things to investors.

Bank account and card setup that stays clean

Use one main company checking account and one main company card program. If you must open more accounts later, do it for clear reasons, like a payroll account or an account for a foreign entity. Avoid collecting random accounts “just in case.”

When you have fewer places money can hide, your records stay clean. Your reconciliations are faster. Your reports become more reliable. That reliability is what investors feel when they review your numbers.

Handle founder out-of-pocket costs the right way

Sometimes you will pay for something before the company card exists. That is fine, but do not normalize it. Treat it as a bridge, not a lifestyle.

When you do reimbursements, document the business reason and attach the receipt. Pay it back from the company account and record it clearly. This keeps the story simple: the company paid for company work, and you can prove it.

3) Pick one accounting stack and commit

The tool is not the strategy

QuickBooks, Xero, and similar tools can all work. The mistake is thinking the tool alone solves the problem. The tool only reflects your habits and your rules.

If you start with messy categories and missing receipts, the tool becomes a storage box for chaos. If you start with clean rules, the tool becomes a dashboard you can trust. The same software produces two very different realities.

Start simple, but do not start sloppy

Choose a setup that a part-time bookkeeper can manage easily. Many founders fail here because they build a system only they understand. Later, when they hire help, the new person rewrites everything, and your history becomes inconsistent.

A simple setup is not the same as a vague setup. You want clear categories, clear vendor names, and a clear monthly close habit. Simple means repeatable, not “I will guess later.”

Add receipt capture from day one

Do not wait until you “have time.” You will not have time. The only time that works is now.

Use a card program or expense tool that makes receipt upload painless. If you are very early, a shared folder plus a strict naming rule can work. The goal is not fancy software. The goal is proof.

4) Design a chart of accounts that tells an investor story

Your categories are your narrative

In diligence, your categories are the lens investors use to understand you. If everything is “misc,” they cannot see what you value or how you run the company. If your chart is too detailed, they cannot see patterns.

A good chart answers investor questions without extra work. It also helps you manage burn and runway without guessing. You should be able to look at one page and know where the money went.

How to split costs without overbuilding

Most startups should separate payroll, contractors, cloud, tools, legal, rent, and travel. Deep tech teams often need a few extra lanes, because hardware and lab costs can distort the picture if they get mixed into general spend.

If you are building robotics, you should track parts, prototypes, and equipment as their own area. If you are building AI, you should treat compute and data costs as first-class categories. These are not minor details in your business model.

Track legal and IP in a clean, visible way

Investors will ask what you spent on legal and what you got for it. If IP work is important to your strategy, your accounting should reflect that importance.

Separate legal work from IP work so you can show progress. Even if Tran.vc is providing in-kind patent and IP services, you still want clean records that explain the value you received and how it supports your moat.

If you want to build that moat early and make it clear to investors, apply anytime at https://www.tran.vc/apply-now-form/

5) Create rules for transactions before you scale spending

Vendor naming rules prevent future confusion

The same vendor can show up in your bank feed with multiple names. Stripe, Google, Amazon, and many tools appear in messy ways. If you do not standardize vendor names early, you will end up with duplicates everywhere.

This matters because diligence teams often scan vendors. They look for unusual payees, personal services, and risk signals. When your vendor list is clean, that review is fast and boring. When it is messy, it triggers questions.

Build a habit of memos for “odd” spend

Most transactions are self-explanatory. Some are not. When a charge is not obvious, add a short memo while it is still fresh in your mind.

Later, that memo becomes your memory. It saves hours. It also shows investors you run a tight ship, because you can explain exceptions without drama.

Decide how you will treat annual bills

Annual software and insurance payments can make one month look terrible if you track on cash basis. Even if you stay on cash basis early, you should still mark these as annual items.

You do not need a complex system to do this. You just need a consistent way to tag or note them. When someone asks about burn, you can explain the spike in seconds instead of scrambling.

6) Make monthly close a simple routine, not a crisis

The monthly close is your control system

A monthly close is just a set of small steps that keep your books aligned with reality. It is not about perfection. It is about catching errors while they are still small.

When you close monthly, your numbers become stable. Stable numbers let you make faster decisions. They also make investor updates easier, because you are not rewriting your story each month.

Reconciliation is the non-negotiable step

If your accounting does not match your bank and card statements, your reports are not real. Many founders skip reconciliation because it feels tedious. The cost of skipping it is much higher than the time you save.

Reconciliation is also where you catch fraud, duplicate charges, and subscription creep. If you want to protect runway, reconciliation is one of the best habits you can build.

Keep the close short by staying current

If you are behind by one week, catching up is easy. If you are behind by three months, catching up is painful, and you will start guessing. Guessing creates errors that become hard to unwind later.

Treat bookkeeping like brushing your teeth. Small, regular work prevents expensive pain later.

7) Contractors, payroll, and the diligence questions nobody wants

Contractors are a cost and a risk category

Contractors are common in early-stage deep tech teams. Investors will look at contractor costs to understand how you build and how you control spend. They will also ask what the contractors built, and whether the company owns that work.

Accounting should show a clear contractor picture. Legal should show a clear ownership picture. If either one is messy, diligence slows down.

Pay contractors in a consistent, traceable way

Use one payment method and keep invoices. Avoid paying contractors through random apps with weak records, unless you can export clean histories. Make sure every payment ties to an invoice, statement, or clear written agreement.

When payments are clean, your books are easier to review. It also helps you budget because you can see contractor trends clearly over time.

Payroll setup should be boring and compliant

Payroll mistakes create big diligence headaches because they can lead to tax penalties. Use a reputable payroll provider and set it up correctly. Do not treat payroll like a casual transfer.

Even if you are paying only one founder salary, do it the right way. Investors will ask if filings are current and whether taxes are paid. Clean payroll records remove fear.