Before we talk numbers, let’s talk about the mistake almost every technical founder makes with advisors.

They treat advisor equity like a thank-you gift.

A “you helped me, so here’s a slice” kind of thing.

But advisor equity is not a gift. It is a business deal. And like any deal, the terms you set now can help your company grow… or quietly drain it for years.

At Tran.vc, we see this up close. Many AI, robotics, and deep tech teams come to us with strong tech and a real chance to win. But their cap table is already messy because they “handed out” equity early. They gave away too much to someone who stopped showing up. Or they gave equity with no clear job, no timeline, and no way to end it.

That problem does not just feel bad. It harms your next steps.

When you go to raise money, investors will look at your cap table. They will ask why an advisor owns a meaningful chunk of the company when the product is still early. They will wonder if you can make clean decisions. They will worry you will do the same thing again.

And in deep tech, you already have enough to prove. Your story needs to be simple, tight, and easy to trust.

So this guide is about doing it the right way.

Not “the friendly way.” Not “the normal way.” The right way.

We are going to walk through how to split equity with advisors so it matches real value, protects founder control, and stays fair to the people who will truly help you. You will learn how to think about advisor roles, how to price the help, how to set terms, and how to avoid the deals that look small now but become painful later.

One more point before we begin: the best equity split is the one you never regret.

That sounds obvious, but it is useful. Regret usually comes from one of two things:

You gave equity without clear proof of work.

Or you gave equity without a clean way to stop it.

We are going to fix both.

And if you want hands-on help building the right structure around your company—especially if your core value is in code, models, hardware design, or novel methods—Tran.vc can help you lock in a real moat early through patent strategy and filings. That is our focus: turning your work into protected assets, before you give away leverage. You can apply anytime here: https://www.tran.vc/apply-now-form/

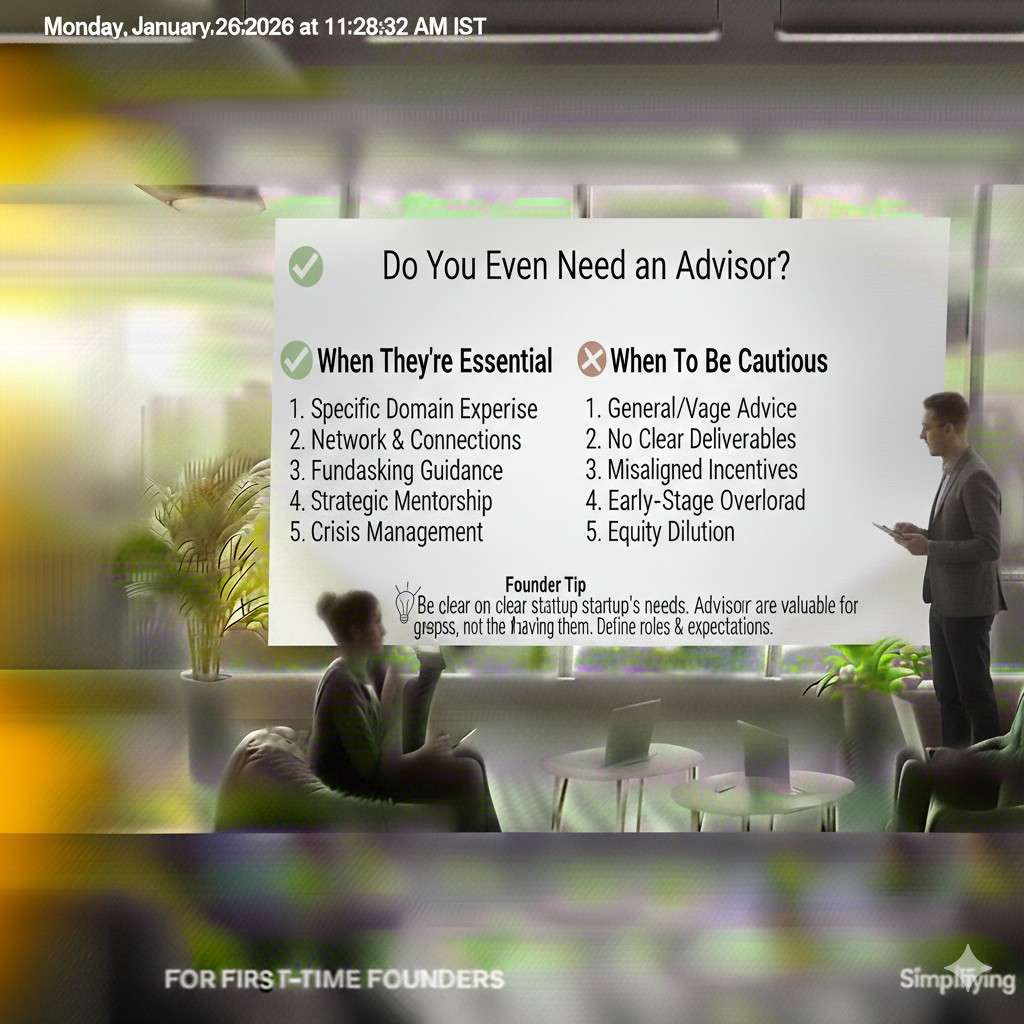

Do You Even Need an Advisor?

The real job an advisor should do

Most founders say they “need an advisor” when what they really need is one of three things: a first customer, a trusted intro to a key hire, or help making one hard decision. Those are real needs. But an advisor is not always the best way to get them.

An advisor is a person you bring close enough to shape your company. That is a serious choice. If they are good, they help you move faster with fewer mistakes. If they are not, they add noise, pull you in the wrong direction, and still keep their equity.

Before you talk about equity, you want to be sure you are solving the right problem. If your problem is “I need someone to review my pitch,” that can be a paid call. If your problem is “I need a patent plan so investors can see we have a moat,” that is a service engagement with clear deliverables, not an advisor deal.

Equity should be used when the person will keep showing up, keep carrying weight, and keep being useful as the company changes. If you cannot picture that clearly, do not start with equity.

Advisors are not part-time co-founders

A lot of founders treat advisors like light co-founders. They share ideas. They want the advisor’s name on the deck. They feel safer when a well-known person is “on the team.” That is understandable, especially early.

But a real co-founder shares the risk every day. They work through the messy parts. They take the late-night calls. They live with the hard tradeoffs. Advisors do not do that. Even great advisors do not do that.

That does not make advisors bad. It just means the deal has to match the role. When you give advisor equity like it is co-founder equity, you pay co-founder prices for non co-founder work. Later, when you need to hire leaders or bring in investors, you will wish you still had that equity to use.

If you want help with the heavy lifting, you probably want a contractor, a fractional leader, or a full-time hire. Advisors are best when they make you smarter and faster, not when they do your job for you.

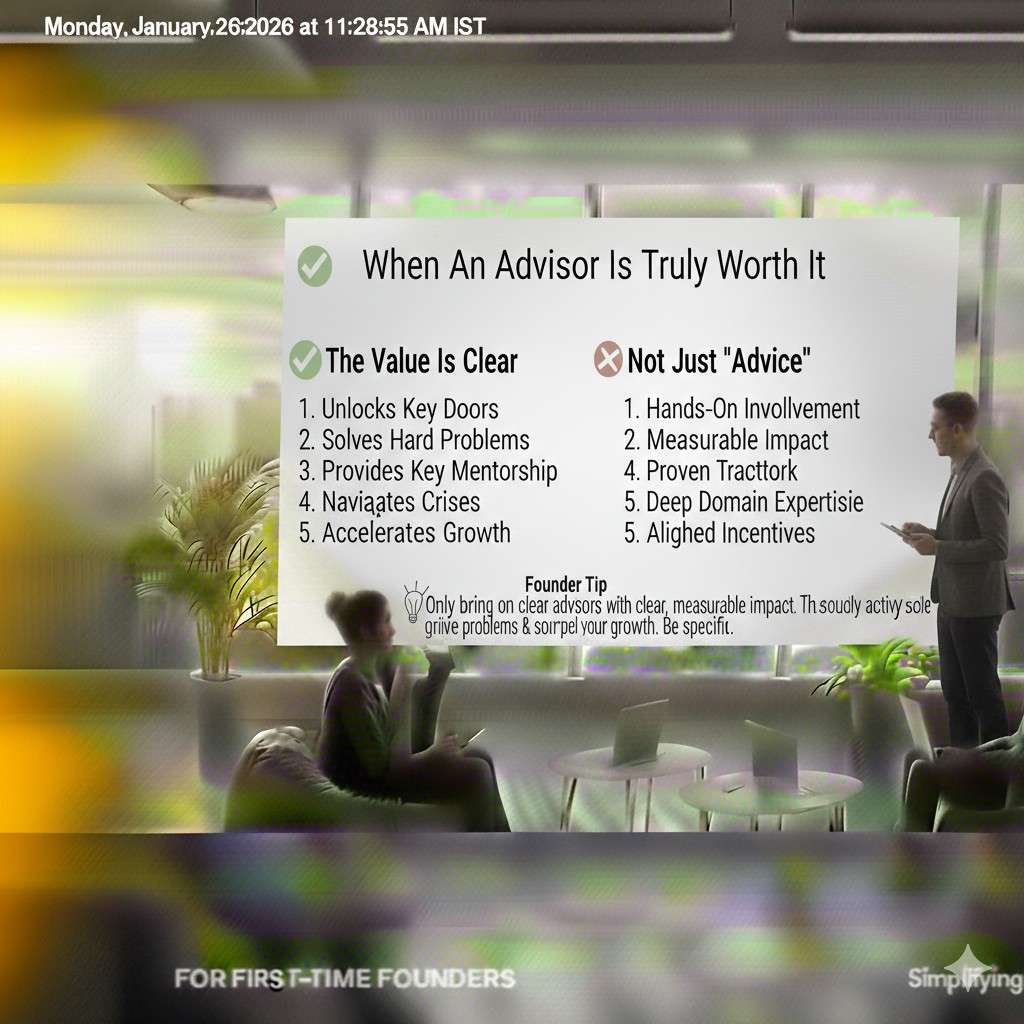

When an advisor is truly worth it

A strong advisor tends to do one of a few things very well. They open doors that are hard to open without them. They help you avoid expensive mistakes because they have been through the same path. They help you choose the right “no” when you are tempted to chase every shiny thing.

In robotics, AI, and deep tech, the best advisors also help you tell a clear story. They help you frame what is special about your work. They help you connect the tech to a real problem and a real buyer. That matters because early teams often explain features, not outcomes.

The key is consistency. A useful advisor is not someone who has one big idea and then disappears. It is someone who keeps coming back, asks sharp questions, and helps you make better calls across many months.

Signs you are about to pick the wrong advisor

It is easy to get pulled in by a big title, a famous company name, or a strong social profile. Those things can be nice, but they are not the job. The job is impact.

If the person is vague about how they will help, that is a warning. If they want equity fast, that is another warning. If they talk more than they listen, that is a warning too. The early stage is full of unknowns. You want advisors who can work with that, not advisors who perform confidence.

Also be careful if you are choosing an advisor because you feel stuck or lonely. Founding is lonely. But equity is not a good tool for emotional relief. Build a peer group, find other founders, join a community, talk to people who are in the same phase. Save equity for people who will change outcomes.

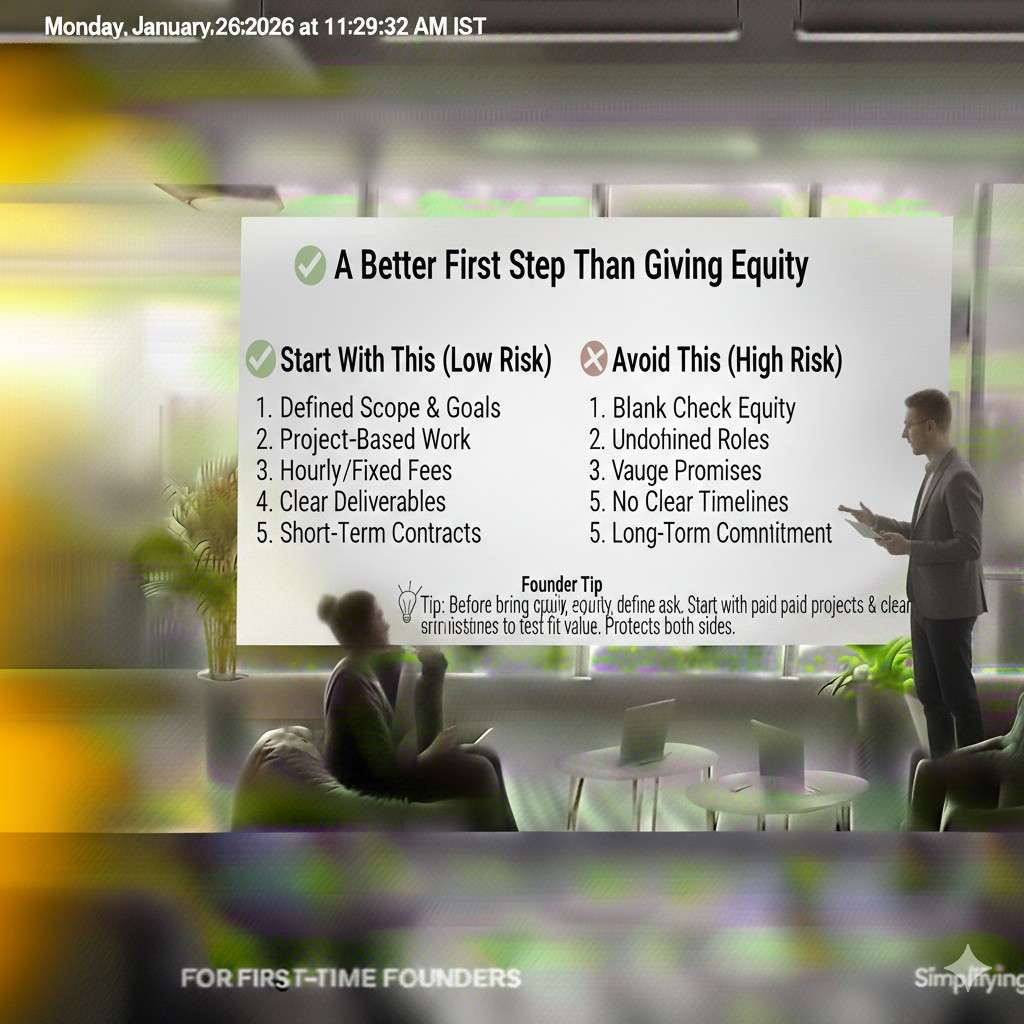

A better first step than giving equity

If you are not sure yet, start small and time-box it. Offer a short trial period with no equity. Do a few calls. Give them a real problem. See how they think. See if they follow through. See if they bring value that you cannot easily get elsewhere.

This protects you from “polite yes” advisors. Some people agree to advise because it feels nice. They like being asked. They like the title. But they do not have the time or focus to help you in a meaningful way. A trial makes that obvious without creating a messy exit later.

If the person is truly strong, they will respect this approach. They may even prefer it because it keeps expectations clear on both sides.

What Kinds of Advisors Exist, and Why It Changes Equity

The “door opener” advisor

A door opener is someone with real access. They can get you a meeting you would not get otherwise. In B2B, that can mean a buyer at a large company, a key partner, or a channel that changes your sales cycle.

The common trap is paying for hope. Founders hear “I can introduce you to people” and they picture deals closing. But an intro is not a deal. And one intro is not a long-term role. A door opener can be valuable, but you need to define what “value” means in plain terms.

If the advisor is only useful for one set of intros, you may be better off offering a success fee, a small cash consulting fee, or a short contract tied to clear results. Equity makes sense only if the relationship will keep producing wins over time.

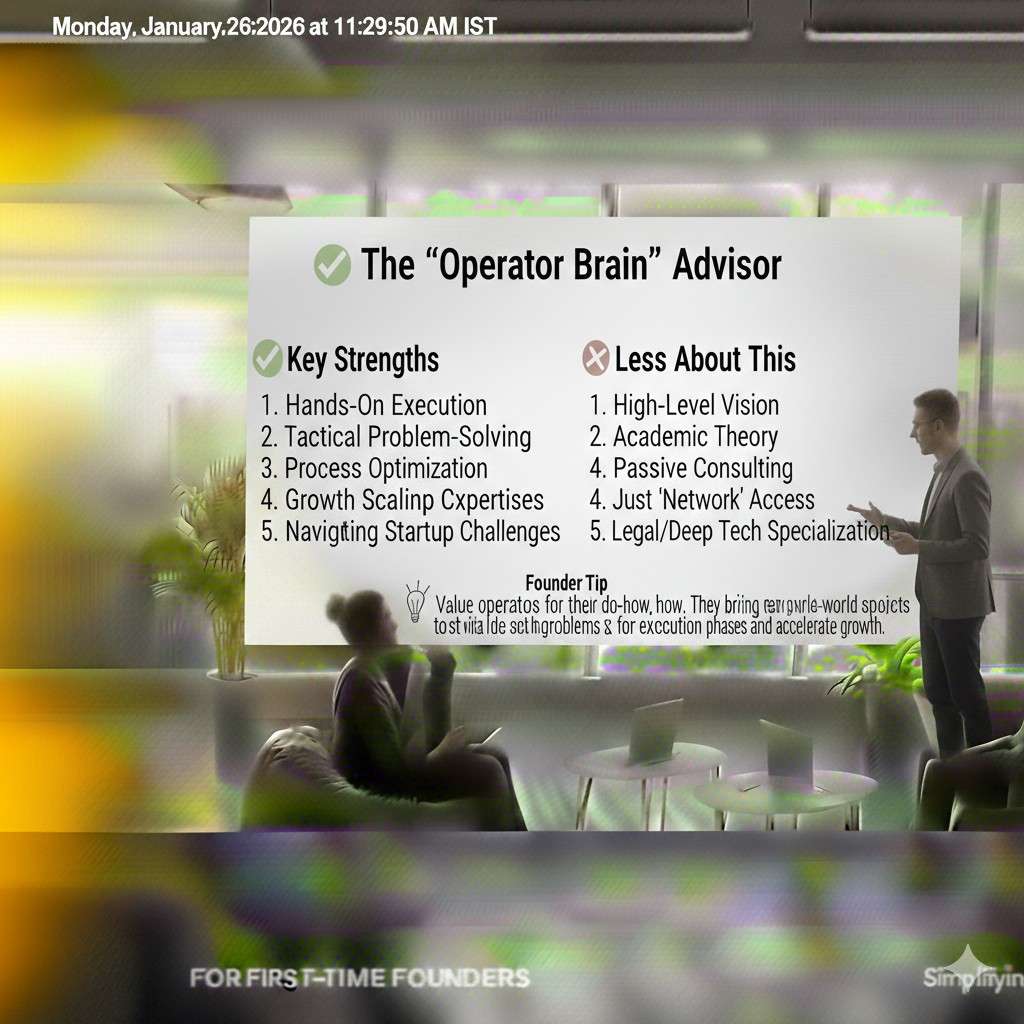

The “operator brain” advisor

This advisor has built and run things. They know how companies break. They know how teams get stuck. They can look at your plan and tell you which parts will hurt later.

Operator advisors are often the best fit for deep tech founders because they help bridge the gap between lab-grade work and real-world execution. They can help you set priorities, build a roadmap, and stop wasting time on work that will not move the company forward.

Because their help can span many topics over time, equity can make sense here. But only if they truly show up consistently and if you can define their lane. “General advice” is too broad. You want the relationship to have a center of gravity, even if the talks range widely.

The “industry truth teller” advisor

This is the person who knows the market from the inside. They know how buyers think. They know how budgets work. They know what gets blocked by policy, safety rules, or procurement. They can tell you if your pricing is fantasy or if your go-to-market plan is real.

In robotics and AI, this matters because the product can look amazing in a demo and still fail in the field. Industry truth tellers help you design for the real world, not the lab.

Their value is often in preventing bad moves. That is hard to measure, but you can still make it concrete by focusing on decisions. For example, they might help you pick which vertical to start with, which compliance path is realistic, or which integration you should build first.

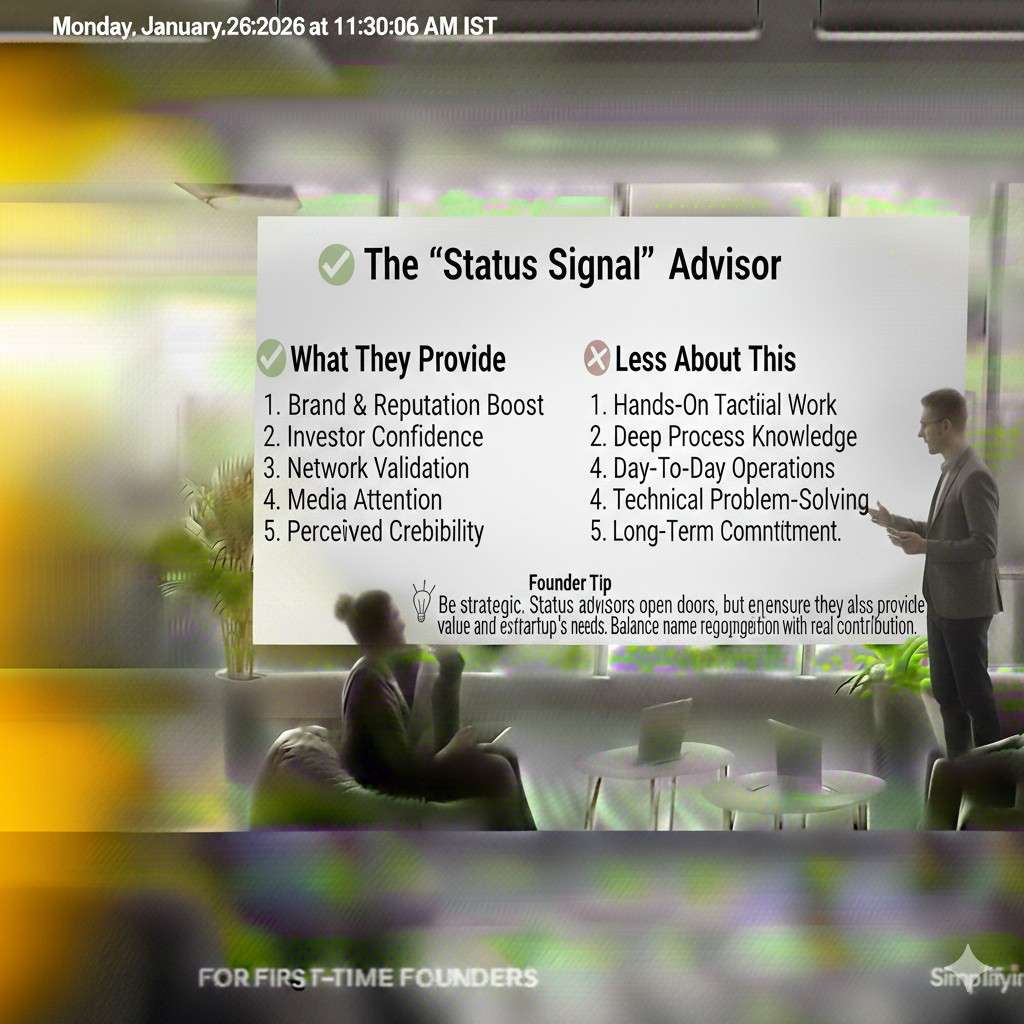

The “status signal” advisor

Some advisors mainly add credibility. Their name helps you get meetings. Their background helps investors take you seriously. Their presence can reduce perceived risk.

This can be real value. But it is also easy to overpay for it. A name on a slide does not build your product. It does not fix your hiring plan. It does not carry you through a tough quarter.

If you want a status signal advisor, you should be even stricter with terms. You want a short vesting schedule, a clear scope, and a strong understanding that the role is not a blank check. If their name is doing the work, that can be useful, but you still need to protect the company.

The “technical guide” advisor

This advisor helps with hard technical questions, architecture choices, safety constraints, data strategy, or research direction. For early AI and robotics teams, technical guidance can be priceless because one wrong path can cost months.

The risk is that technical advice can turn into design-by-committee. You do not want an advisor who “owns” your roadmap. You want someone who can pressure test your choices and help you spot blind spots.

Also, if this person is contributing actual inventions or key technical methods, you must treat IP carefully. If they create patentable ideas with you, you need clean invention assignment terms. Otherwise, you can end up with unclear ownership later, which can scare investors and buyers.

This is one area where Tran.vc teams often get the most leverage: building a clear IP plan early and filing smart patents before the story gets complicated. If you want that kind of foundation, you can apply anytime at https://www.tran.vc/apply-now-form/

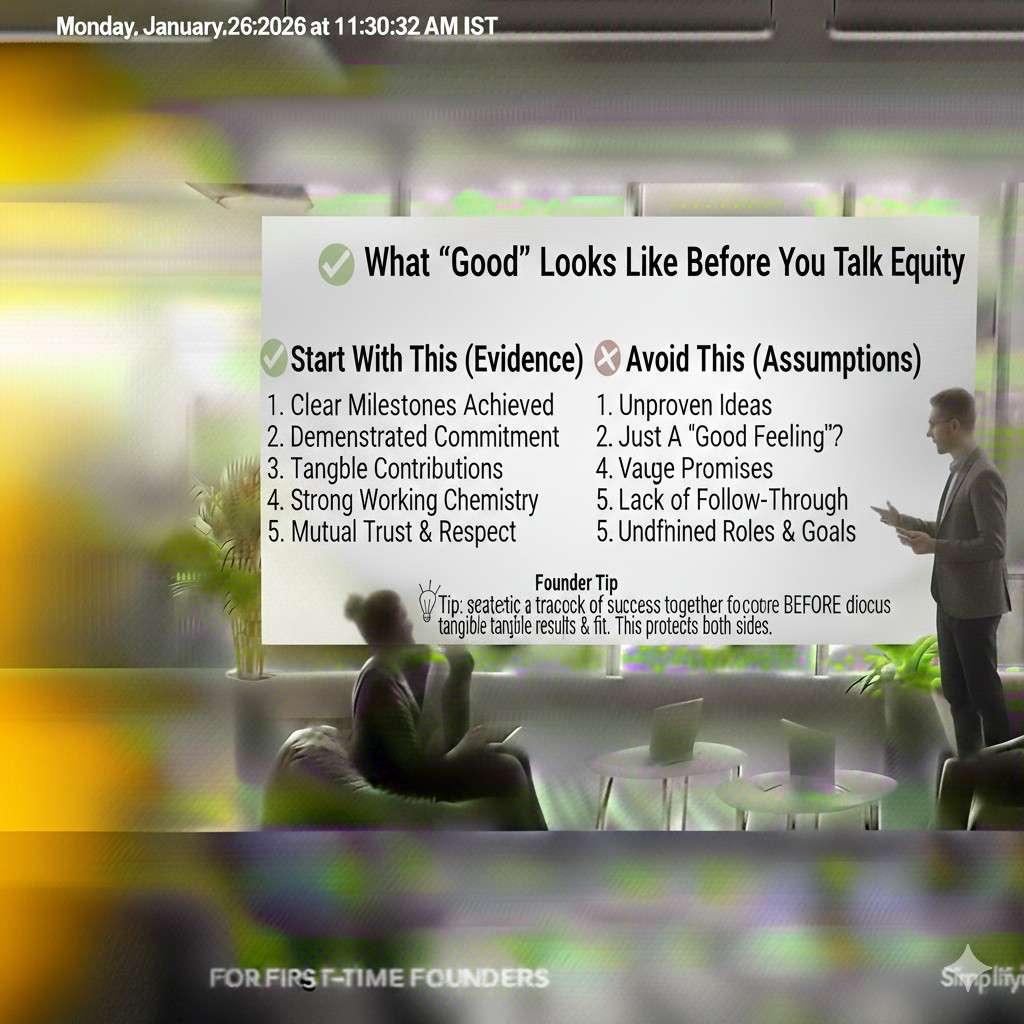

What “Good” Looks Like Before You Talk Equity

Start with a single, clear outcome

A good advisor relationship begins with clarity. You should be able to say, in plain words, what will be different because this person is involved. Not a vague promise. Not a hope. A real change.

For example, you might say: “We will land three serious customer discovery calls in the next six weeks.” Or, “We will make a clear choice on which market we start with, and why.” Or, “We will pressure test our pricing so we stop guessing.”

When you can name an outcome, you can structure the relationship around it. Without that, the relationship becomes a friendly chat that slowly turns into equity drift.

Define the lane so you do not create confusion

Advisors can help a lot, but they can also confuse your team if they are not in a lane. If an advisor is giving product direction, sales advice, hiring advice, and investor advice all at once, you may end up with too many voices and no clear owner.

A lane does not have to be narrow, but it must be real. It could be “enterprise sales motion,” or “robotics deployment risks,” or “pricing and packaging,” or “patent and moat strategy.” When the lane is clear, you know when to pull them in and when to ignore the noise.

This also helps you avoid the awkward moment where your advisor starts acting like they are leading, while your team is unsure who is in charge. You can prevent that with clear boundaries from day one.

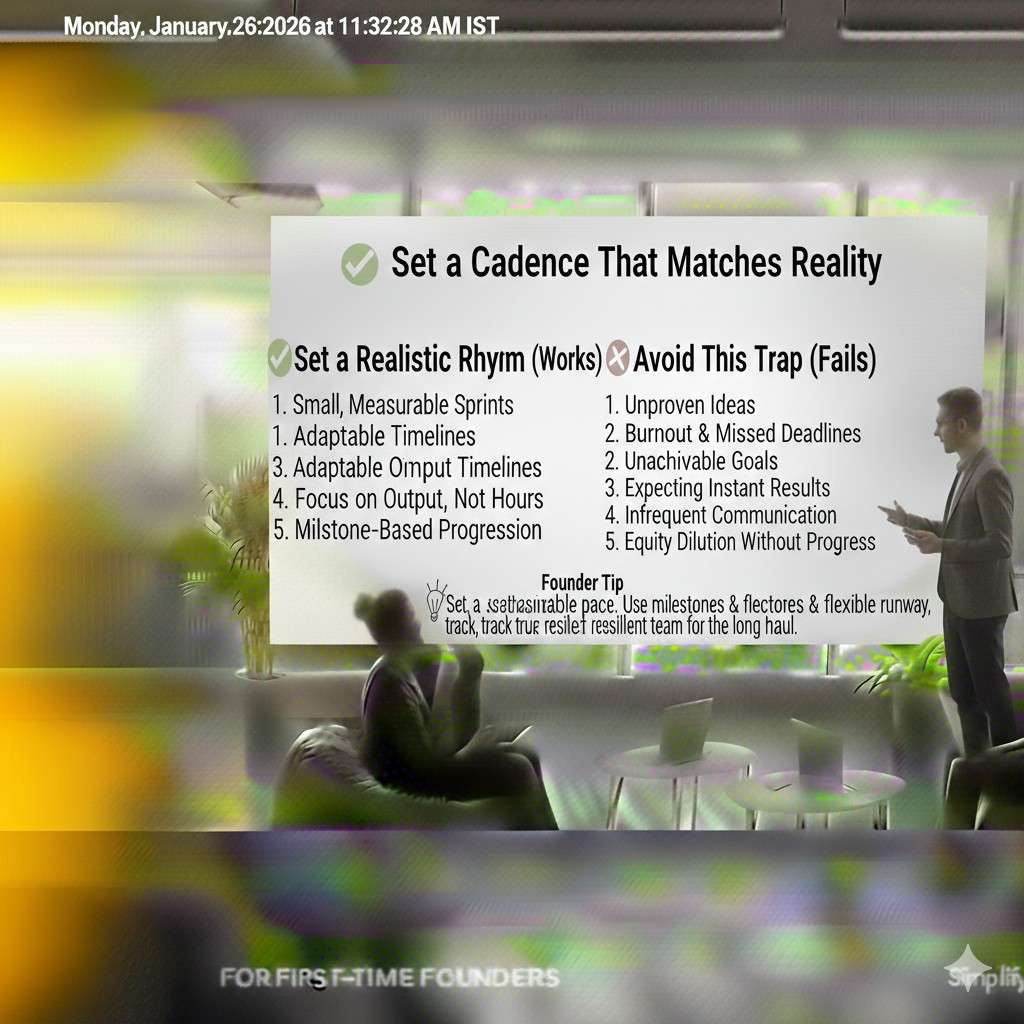

Set a cadence that matches reality

Many advisor relationships fail because the cadence is not real. Founders say, “Let’s talk once a month,” but then months go by. Or the advisor says yes, but they are too busy and keep rescheduling.

You want a cadence that fits the advisor’s actual schedule and your actual needs. Early stage companies benefit from shorter, more frequent touchpoints because things change quickly. If you only speak once every six weeks, the conversation can feel outdated before it starts.

This is why starting with a trial period is useful. You can test if the cadence works without locking in equity. You can also see if the advisor will show up when things are messy, not only when you have good news.

Decide what “work” means in your relationship

Advisors often think their job is to give advice. Founders often think the advisor’s job is to create results. The gap between those two views causes most conflicts.

You can fix this by agreeing on what “work” means. Does it mean introductions, and if so, how many and to whom? Does it mean reviewing materials and giving feedback within a set time? Does it mean joining key calls? Does it mean helping you recruit one hire?

When “work” is clear, equity becomes easier to price. When it is vague, you will either underpay and lose a great advisor, or overpay and regret it.