Most startup fights do not start with the product. They start with the cap table.

Who owns what. Who can leave. Who stays. What happens if the co-founder who built the first version walks away six months in. What happens if a key hire quits right before a fundraise. And what happens if an investor looks at your equity setup and thinks, “This is risky.”

Reverse vesting is one of the cleanest ways to reduce that risk. It is not fancy. It is not new. But it is one of the first things many investors look for when they are deciding whether your team is “fundable.”

This article is about how reverse vesting actually works, why VCs like it, and how to set it up in a way that protects you, not just the investor. We will keep it simple, practical, and focused on what matters in the real world.

Before we go deeper, here is the core idea in plain words:

Reverse vesting means you get your founder shares now, but you earn the right to keep them over time.

So if you leave early, you do not keep all of them. The company can buy back the “unearned” shares. That protects the team that stays and keeps building. It also tells investors you are serious and not playing a short game.

And since Tran.vc works with technical founders to build real moats with patents and smart IP strategy, reverse vesting fits the same mindset: build the foundation early, so your next steps are easier.

If you want help thinking through your early setup—equity, IP, patents, and how to look fundable without giving up control too soon—you can apply anytime here: https://www.tran.vc/apply-now-form/

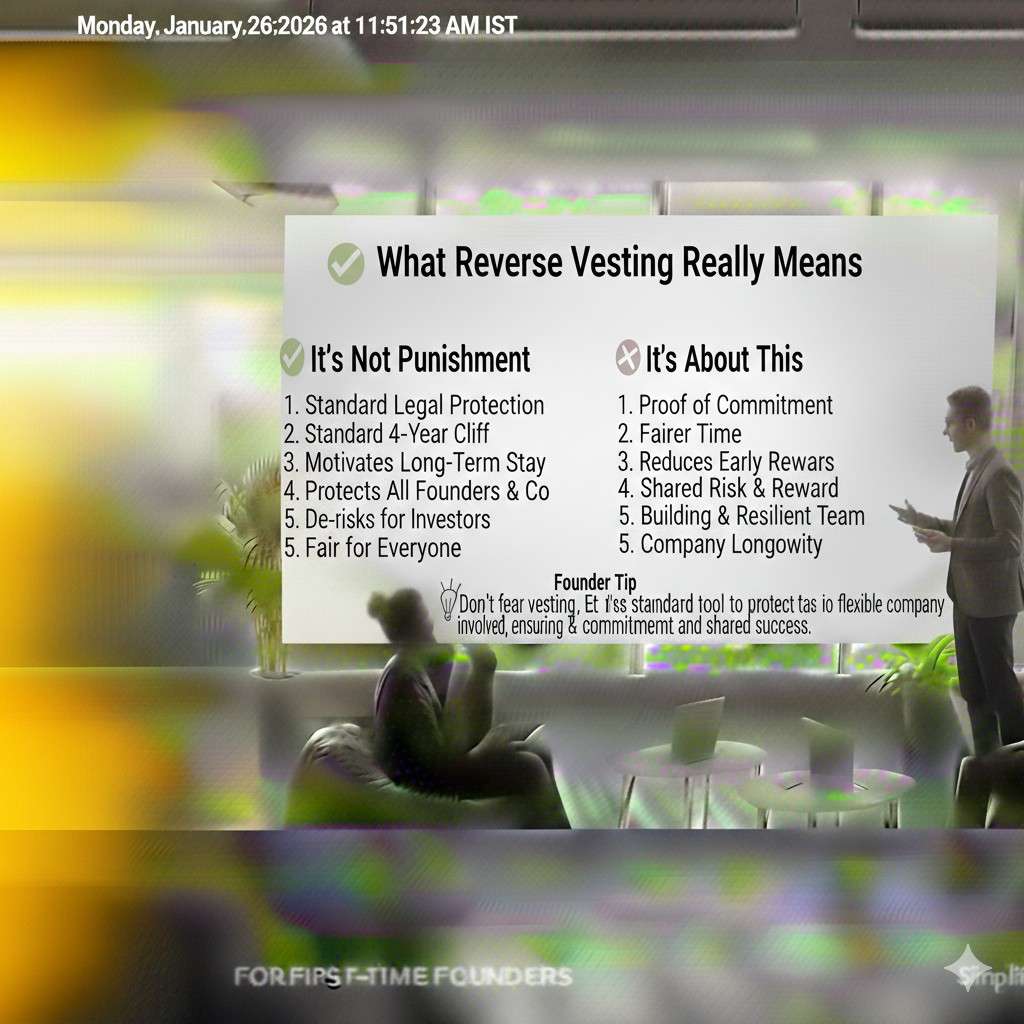

What Reverse Vesting Really Means

The simple idea behind reverse vesting

Reverse vesting looks complex on paper, but the idea is very simple. A founder is given their shares on day one, but those shares are not fully theirs yet. They earn them over time by staying and building the company.

If the founder leaves early, the company can take back the part that was not earned. If the founder stays long enough, they keep everything. That is the whole deal.

This structure is not about punishment. It is about fairness. The people who stay and do the hard work should own the company, not someone who left when things got hard or boring.

How it is different from normal vesting

Employees usually vest forward. They start with zero shares and earn them month by month. Founders usually vest in reverse. They start with all their shares, but risk losing some if they leave early.

This matters because founders are not like employees. Founders already took the risk of starting the company. Reverse vesting respects that while still protecting the business.

From an investor’s point of view, reverse vesting is cleaner. The shares already exist. There is no confusion later about who owns what or how much was earned.

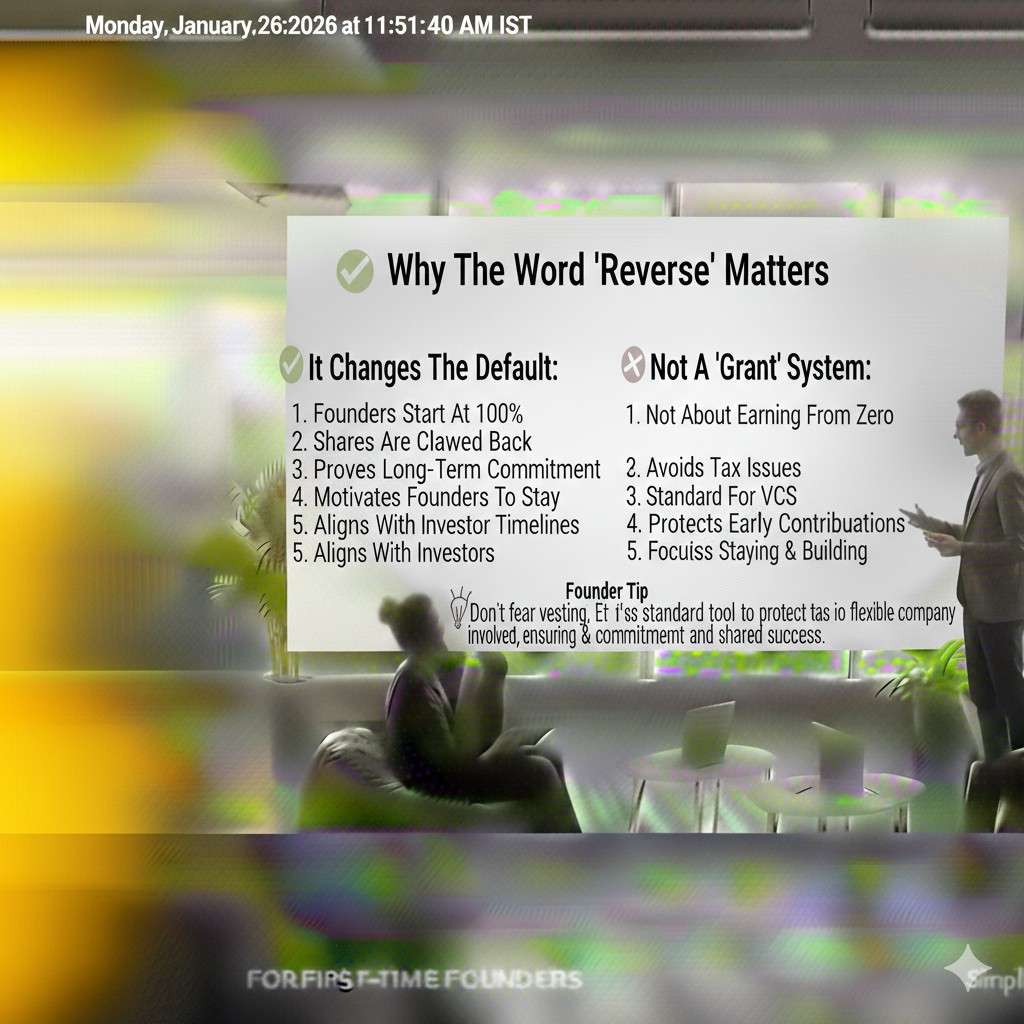

Why the word “reverse” matters

The word “reverse” confuses many first-time founders. It sounds negative. It is not. It just describes the direction.

Instead of earning shares over time, you are keeping shares over time. The end result is the same, but the legal structure is different.

VCs care about this detail because it affects control, taxes, and how clean your company looks during due diligence.

Why VCs Care So Much About Reverse Vesting

The fear investors never say out loud

Most VCs have seen the same movie many times. Two or three founders start a company. One of them loses interest, gets another job, or burns out. They leave with a large chunk of equity and never look back.

The company keeps going, but now it is stuck. A big part of the cap table is dead weight. New hires want equity, but there is not much left. New investors worry about motivation and control.

Reverse vesting prevents this problem before it starts.

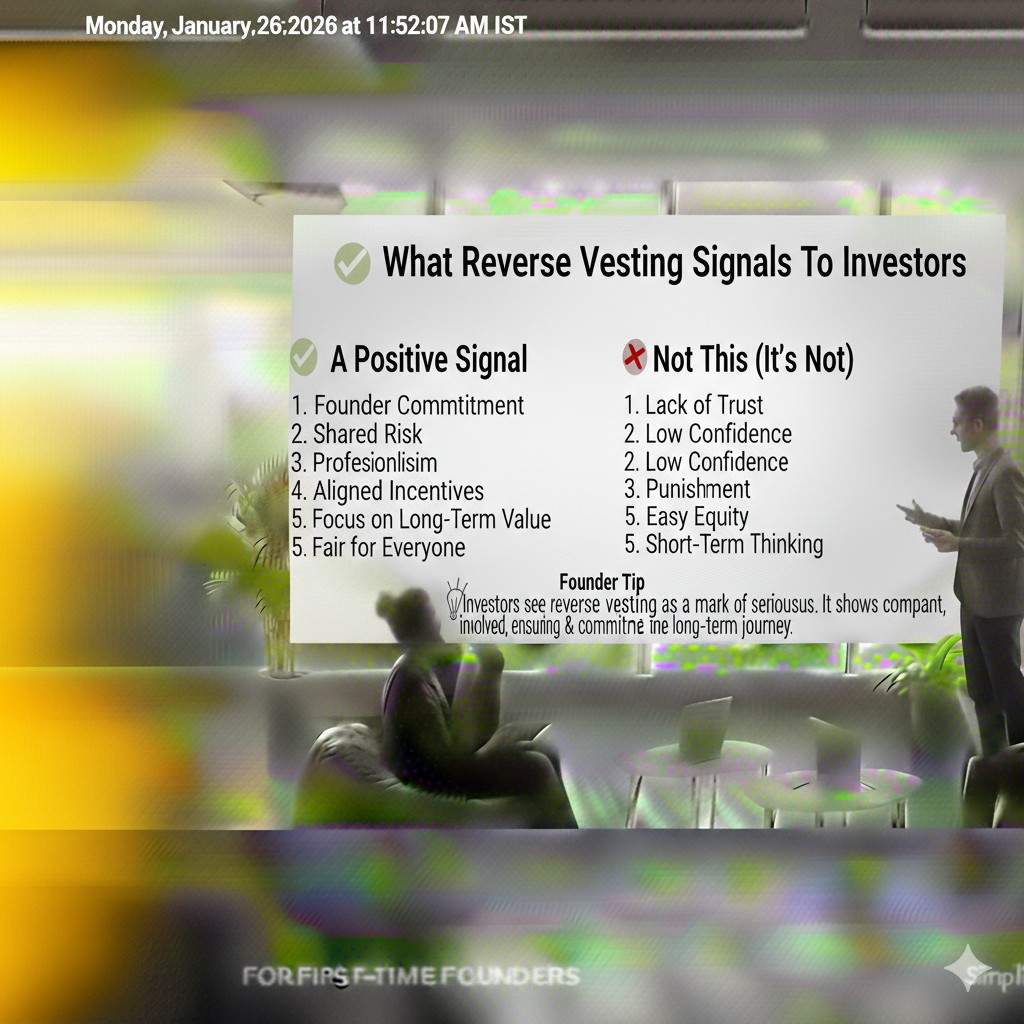

What reverse vesting signals to investors

When an investor sees reverse vesting, they see discipline. They see founders who planned ahead instead of hoping everything would work out.

It also shows alignment. Everyone on the founding team is committing time, not just ideas. Ownership matches effort over time, not just who showed up first.

For early-stage investors, this signal often matters more than revenue or polish.

Why VCs may require it anyway

Even if you do not set up reverse vesting early, many VCs will ask for it later. If you wait, it becomes harder.

Renegotiating equity after emotions, effort, and egos are involved is painful. It can break teams. It can delay funding. It can even kill deals.

Doing it early keeps things calm and professional.

How Reverse Vesting Usually Works in Practice

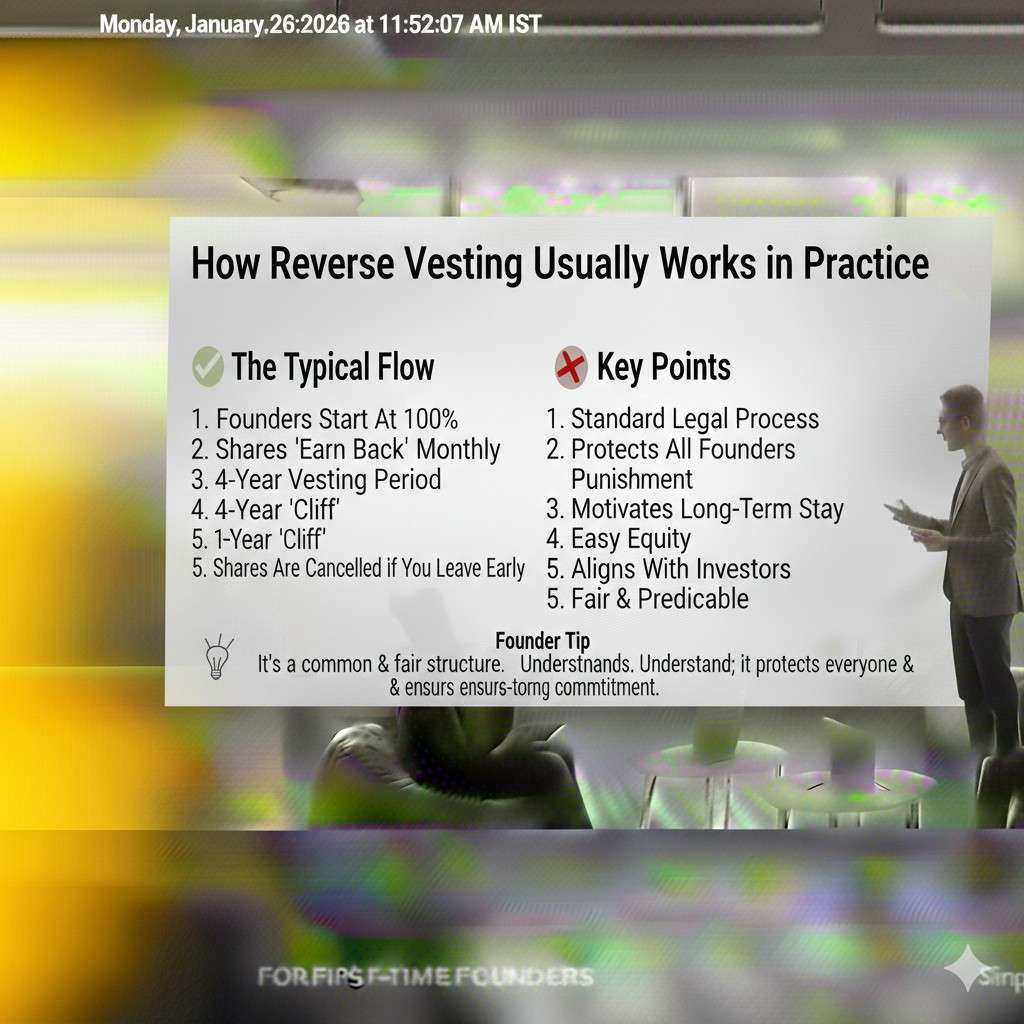

The typical time frame

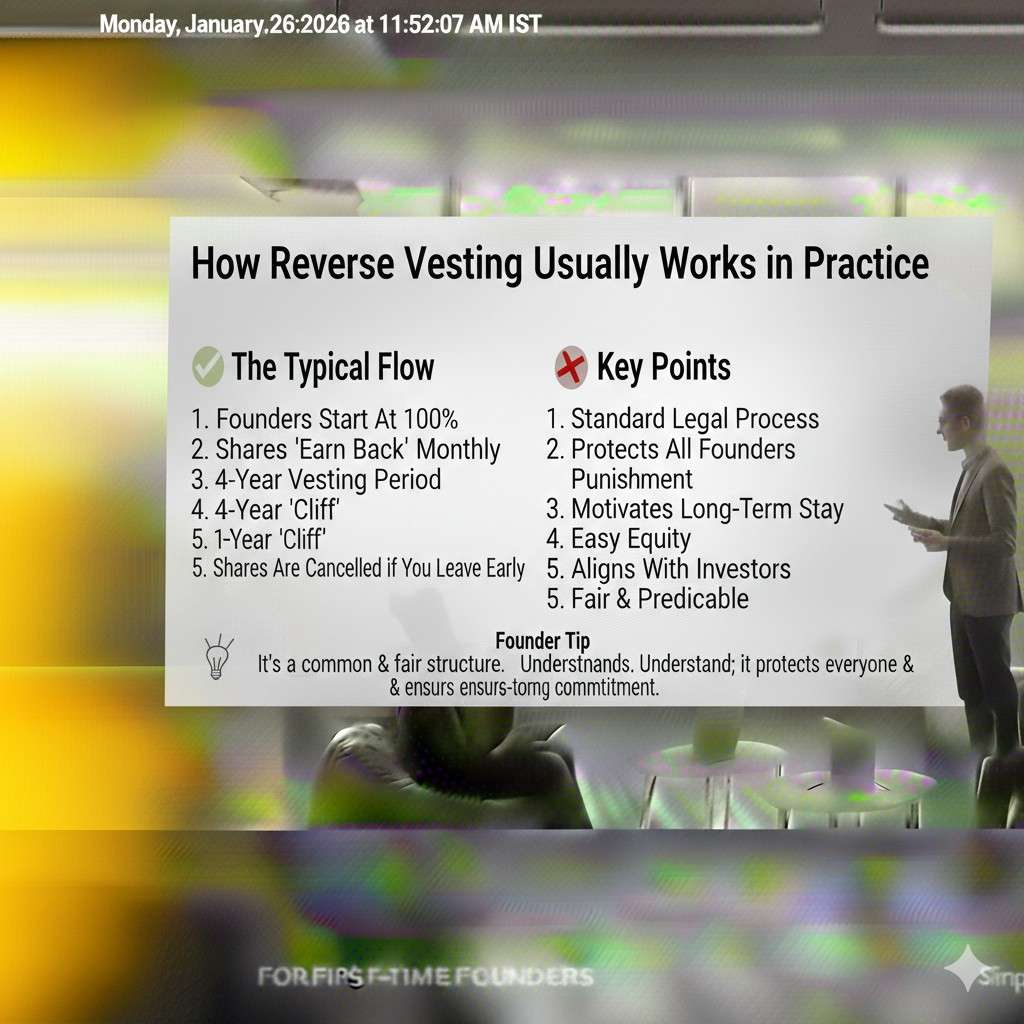

Most reverse vesting schedules last four years. This has become a standard, not because it is perfect, but because everyone understands it.

Often there is a one-year cliff. This means that if a founder leaves before one year, they keep nothing beyond what they already earned outside the vesting plan.

After the first year, shares usually vest monthly or quarterly.

What happens if a founder leaves early

If a founder leaves before fully vesting, the company can buy back the unvested shares. The price is usually very low, often the original price paid.

This is important. The goal is not to punish the founder who leaves. The goal is to return unused ownership back to the company so it can be reused.

Those reclaimed shares often go to new hires or future founders who actually do the work.

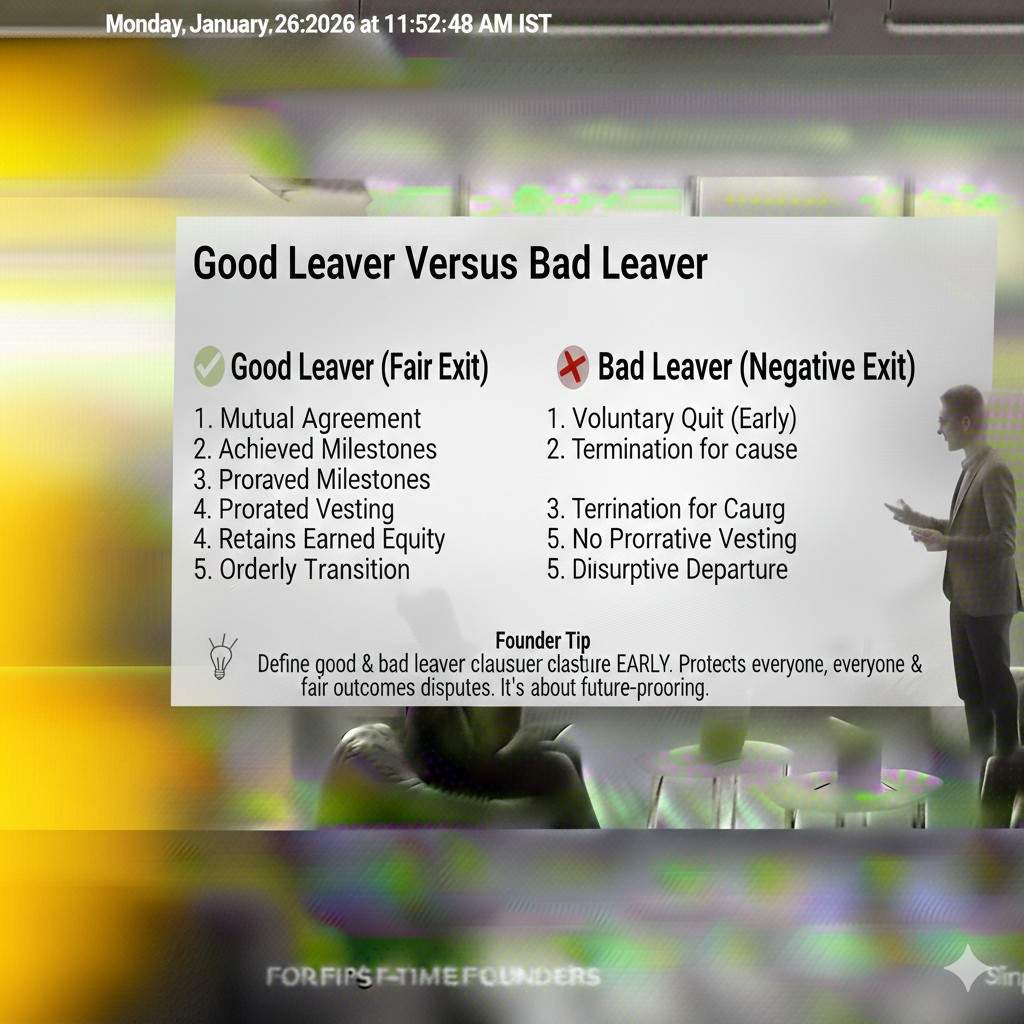

Good leaver versus bad leaver

Some agreements treat all departures the same. Others make a distinction.

If a founder leaves for reasons outside their control, like health issues, they may be allowed to keep more shares. If they leave to join a competitor or break trust, they may lose more.

This is where good legal advice matters. Simple does not mean careless.

Reverse Vesting and Founder Psychology

Why founders resist it at first

Many founders hear “reverse vesting” and feel insulted. They think it means investors do not trust them.

In reality, it is the opposite. It means investors trust the process, not just promises.

Founders who resist reverse vesting often do so because they are afraid of uncertainty. Ironically, avoiding it creates more uncertainty later.

How reverse vesting protects founders too

Reverse vesting is not just for investors. It protects founders from each other.

If one founder stops contributing but still owns a large stake, resentment builds fast. Reverse vesting sets expectations early, when everyone is still aligned.

It also makes tough conversations easier later because the rules were clear from the start.

The confidence it creates inside the team

Teams with reverse vesting often operate with more trust. Everyone knows that ownership is earned through action, not words.

This reduces quiet tension. It keeps focus on building instead of counting shares.

That kind of culture shows up during investor meetings, even if no one says it out loud.

Reverse Vesting and IP Ownership

Why IP and vesting are connected

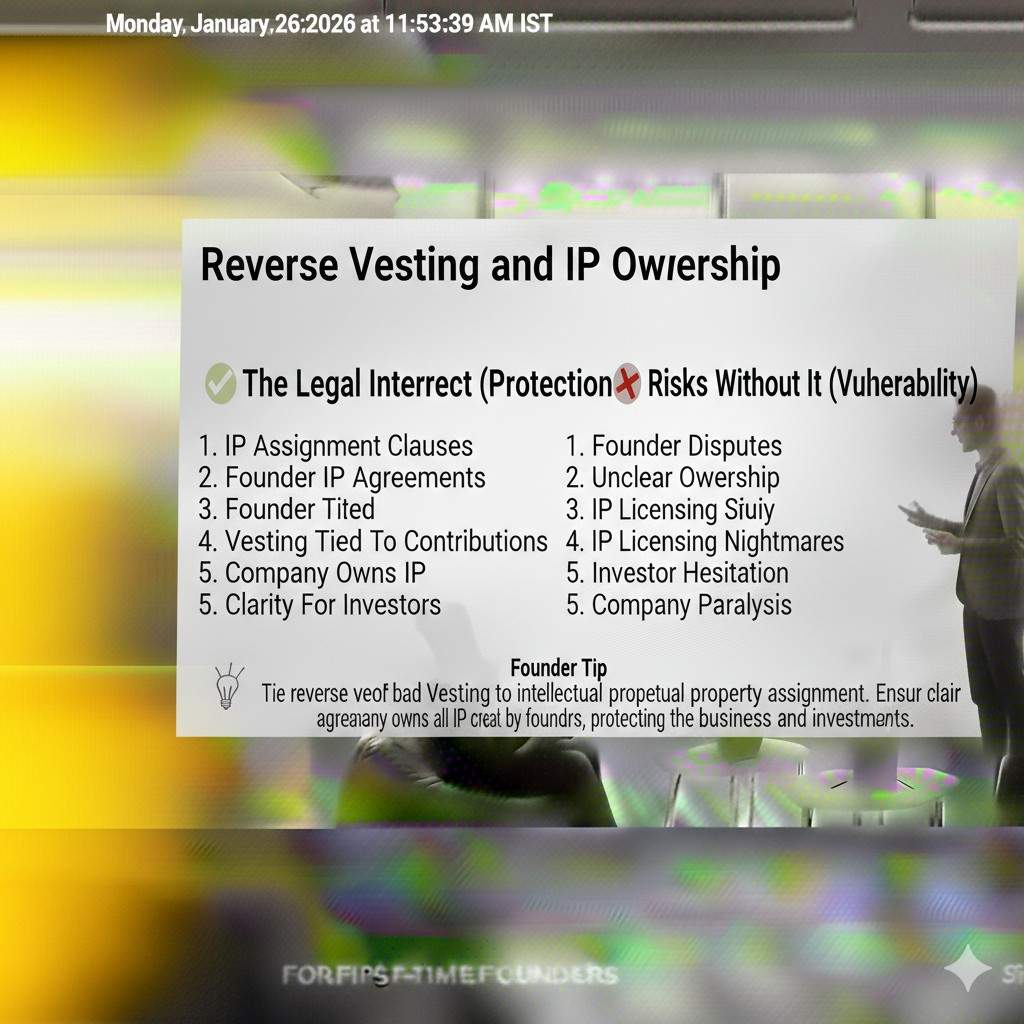

Equity is only one side of ownership. Intellectual property is the other.

If a founder leaves but still owns a large stake and contributed core IP, things get messy fast. Investors worry about control, licensing, and future lawsuits.

Reverse vesting works best when paired with clear IP assignment from day one.

How Tran.vc looks at this differently

At Tran.vc, the focus is not just on equity. It is on turning technical work into defensible assets.

That means making sure patents, code, and inventions belong to the company, not individuals who might leave.

Reverse vesting supports this by keeping ownership aligned with long-term contribution.

If you are building in AI, robotics, or deep tech, this alignment matters even more. Your IP is your moat.

You can apply anytime to work with Tran.vc on this kind of early setup here: https://www.tran.vc/apply-now-form/

Common Mistakes Founders Make With Reverse Vesting

Waiting too long to set it up

The biggest mistake is delay. Founders say they will “fix it later.” Later almost never comes at a good time.

Once money is involved, lawyers get louder. Once emotions are involved, logic gets weaker.

Early is always easier.

Copying templates without thinking

Another mistake is blindly copying a template without understanding it.

Not all founders contribute equally. Not all roles are the same. Vesting should reflect reality, not symmetry for its own sake.

A good setup is simple, but it is also thoughtful.

Forgetting tax and legal details

Reverse vesting has tax implications, especially around elections and share pricing.

Ignoring these details can create surprise bills or legal headaches later.

This is not the place to cut corners.

How To Structure Reverse Vesting The Right Way

Start with roles, not titles

Before you touch numbers, get clear on who is doing what. Not the job title on LinkedIn, but the real work that will happen in the next 18 months.

One founder may lead product and ship weekly. Another may handle sales and partnerships. A third may be deep in research and patents. If you pretend these are equal just to avoid a hard talk, reverse vesting will not save you. It will only delay the conflict.

A strong reverse vesting plan starts by matching ownership to effort, risk, and time. If one founder is quitting a stable job and moving cities, that is real risk. If another is “helping nights and weekends,” that is different. You can still be fair, but fairness requires honesty.

Choose a schedule that fits your reality

Four years is common, but “common” is not the same as “correct.” The right schedule depends on how fast your company needs to grow and how long it takes to reach key milestones.

If you are building deep tech, progress may be slower at first. Research, prototypes, testing, patents, and regulatory steps can take time. In that case, a longer view can be helpful because it keeps the team committed through the long early stretch.

If you are building a fast-moving software product, a standard four-year schedule with monthly vesting may fit well. The key is that the schedule should feel logical when you imagine the hard months ahead. If the plan feels unfair in your gut, it will cause problems later.

Use a cliff for real commitment

A one-year cliff is common for a reason. It creates a clear “trial period” without constant renegotiation. If someone leaves before a year, it is usually because the fit was not real or the commitment was not there.

The cliff protects the company from giving away a large stake to someone who did not stay long enough to carry the hard part. It also protects the founder who stays, because they are not stuck explaining to future investors why a former teammate owns a big chunk of the cap table.

If the idea of a cliff feels harsh, that is often a sign that the team is not fully aligned yet. The cliff forces clarity.

Decide what the company can buy back and at what price

Reverse vesting usually works through a repurchase right. That means the company has the right to buy back unvested shares if a founder leaves.

The buyback price is often the original price paid for the shares, which is usually very low early on. This is not meant to be a cheap trick. It is meant to return unused ownership back to the company so the company can keep functioning.

If founders want a different approach, like a higher buyback price after a certain time, that can be discussed. But be careful. Complex buyback rules often create confusion during a fundraise, and confusion is expensive.

The Conversation Founders Avoid, But Need To Have

Put the hard topics on the table early

Reverse vesting forces a simple question: “What happens if you leave?”

This feels awkward, but it is one of the most respectful conversations you can have. It shows you care about the company more than your ego, and you care about the relationship enough to protect it.

When founders avoid this talk, they are not being kind. They are being unclear. Unclear agreements break friendships faster than clear agreements ever will.

Talk about effort changes, not just quitting

Leaving is not always a clean exit. Sometimes a founder stays but stops contributing. They are still around, still in meetings, still “helping,” but the real work is being done by others.

Reverse vesting does not automatically solve this, because vesting is time-based. But it gives you a framework for accountability. It also makes it easier to add performance expectations and decision rules, if you choose.

A team that talks about this early is a team that can handle stress later.

Agree on decision power before money shows up

Equity and control are related, but they are not the same thing. Reverse vesting helps protect equity, but you also need to be clear about control.

Who can fire a founder? Who decides salary? Who signs contracts? Who can raise money and on what terms?

Investors look for governance clarity. If you do not set this early, you may end up making rushed decisions during a fundraise, and rushed decisions often favor the loudest voice, not the best outcome.

Reverse Vesting During A Fundraise

Why it shows up in due diligence

When you raise money, investors run a basic check: “Can this team stay together long enough to win?”

They look at founder history, team dynamics, and the cap table. Reverse vesting is one of the cleanest signals that your cap table will not become a mess.

It also reduces investor fear about a “free rider” founder who can leave and still own a huge stake. That fear is more common than most founders think, and it can quietly kill a deal.

How it affects valuation and leverage

Reverse vesting does not directly increase your valuation, but it can improve your leverage because it reduces friction.

Fewer red flags means fewer special terms. Fewer special terms means faster closes. Faster closes means less distraction and more time building.

It also helps you negotiate from strength. If your cap table is clean and your founder commitments are clear, you do not have to accept bad terms just to keep the deal alive.

What happens if you do not have it

If you do not have reverse vesting, some investors will ask you to add it as a closing condition. This creates tension right when you need focus.

If the founding team is already tired, adding vesting under pressure can feel like betrayal. Even if everyone agrees, it can slow legal work and create extra costs.

If one founder refuses, the investor may walk away. Not because they hate your product, but because they see a future problem that will drain the company.

Negotiation Points That Matter

The start date and credit for past work

A common question is whether vesting should start from company formation or from when a founder joined.

If you built the prototype before incorporation, you may feel that effort should count. That is fair. The simple way to handle it is to start vesting from a date that reflects when real work began, not just when paperwork was filed.

But do not over-engineer it. Investors like clean stories. If you spend weeks fighting about credit, you are already losing speed.

Acceleration in special cases

Some agreements include acceleration. This means vesting speeds up if certain events happen.

For example, if the company is acquired, some founders want full vesting right away. Investors sometimes accept partial acceleration, like a portion vesting at acquisition and the rest vesting over time if the founder stays with the buyer.

Acceleration is a real topic, but it should not be your first priority. Early-stage founders often focus too much on exit scenarios and not enough on building something worth buying.

Handling a founder who becomes part-time

Sometimes life happens. A founder may need to step back for family, health, or another reason. The team needs a plan for that.

You can keep it simple by agreeing that part-time work should match part-time ownership going forward. The goal is not to punish someone. The goal is to protect fairness for the people who carry the load.

If you do not handle this, resentment grows quietly. Resentment destroys execution.

How Reverse Vesting Fits A “Build Moat First” Strategy

Investors want more than speed now

Many founders think investors only care about growth. In deep tech, investors also care about defensibility.

If you are building AI, robotics, or hard engineering products, your moat often comes from how you protect what you build. Patents, trade secrets, and clear ownership are part of that protection.

Reverse vesting is a piece of the same puzzle. It is one way of saying, “This company is being built for the long haul.”

Why Tran.vc pushes for clean early foundations

Tran.vc does not just talk about long-term value. The firm invests up to $50,000 in-kind in patenting and IP services to help technical founders turn real inventions into assets.

That work is much easier when the founder setup is clean. If ownership is unclear, IP ownership can become unclear too. If a founder leaves and still controls a big stake, it can scare investors who would otherwise be excited.

When reverse vesting and IP strategy work together, your company looks more investable and feels more stable.

If you want help setting up the right foundation early, you can apply anytime here: https://www.tran.vc/apply-now-form/