A cap table is a simple sheet that shows who owns your startup. That is all. But in a seed-stage company, that “simple sheet” quietly controls your future. It decides how much of your company you still own after you bring in a co-founder, give equity to early hires, raise a pre-seed round, and later price your seed round. It affects how investors judge your deal, how your team feels about fairness, and how hard it is to fix mistakes when you are finally moving fast.

Most founders don’t mess up their cap table because they are careless. They mess it up because they are busy building. They sign a quick adviser grant without setting vesting. They promise an early engineer “a few points” without writing down what that means. They accept a small check with weird terms because they think it’s “too early” to worry. Then six months later, they are about to raise seed, and the cap table looks like a junk drawer.

This guide is here to prevent that. And since you’re building in robotics, AI, or deep tech, cap table clarity matters even more. These startups often need a longer runway, more talent up front, and stronger IP walls. That means you must plan ownership with care from day one.

If you want Tran.vc to help you build an IP-first foundation while you set up a clean, investor-ready cap table, you can apply any time here: https://www.tran.vc/apply-now-form/

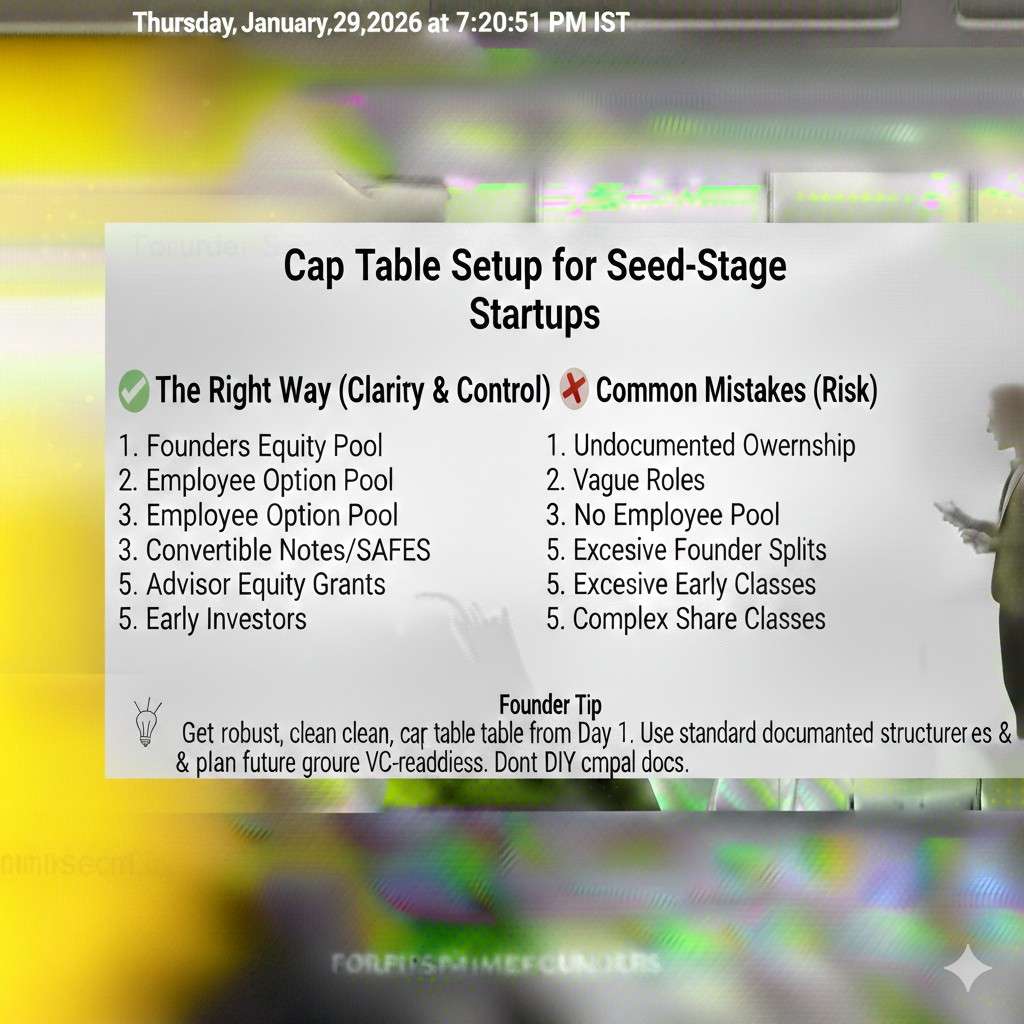

Cap Table Setup for Seed-Stage Startups

What a cap table really is (in plain words)

A cap table is a living record of ownership. It tells you who owns shares today, who can earn shares later, and who has the right to buy shares in the future. It also shows the price people paid, what type of shares they have, and what happens if the company sells or raises more money.

In seed-stage startups, the cap table is not just “paperwork.” It is the map that guides every funding talk, every hiring deal, and every hard founder conversation. If the map is messy, people lose trust. If the map is clear, the company moves faster with fewer fights.

The goal is not to build a “perfect” cap table. The goal is to build a clean one that stays clean as you grow. That means simple terms, clear vesting, and no hidden promises.

If you want hands-on support building a cap table that investors respect, while also building an IP wall that protects your tech, Tran.vc can help. You can apply any time here: https://www.tran.vc/apply-now-form/

Why seed-stage cap tables go wrong so often

Most cap table problems start with good intent. A founder wants to reward a friend who helped early. An early engineer takes a pay cut, so equity feels like the kind thing to do. A small investor offers quick cash, and the founder is tired and says yes.

The issue is timing and structure. Seed-stage decisions happen when you have the least context, the least legal support, and the most pressure. That is why “small” equity decisions can turn into big blocks later.

Another common reason is vague language. Words like “a few points,” “we’ll make you whole,” or “we’ll fix it later” are not terms. They are future conflicts. A cap table only stays healthy when everything is written in clear numbers and clear rules.

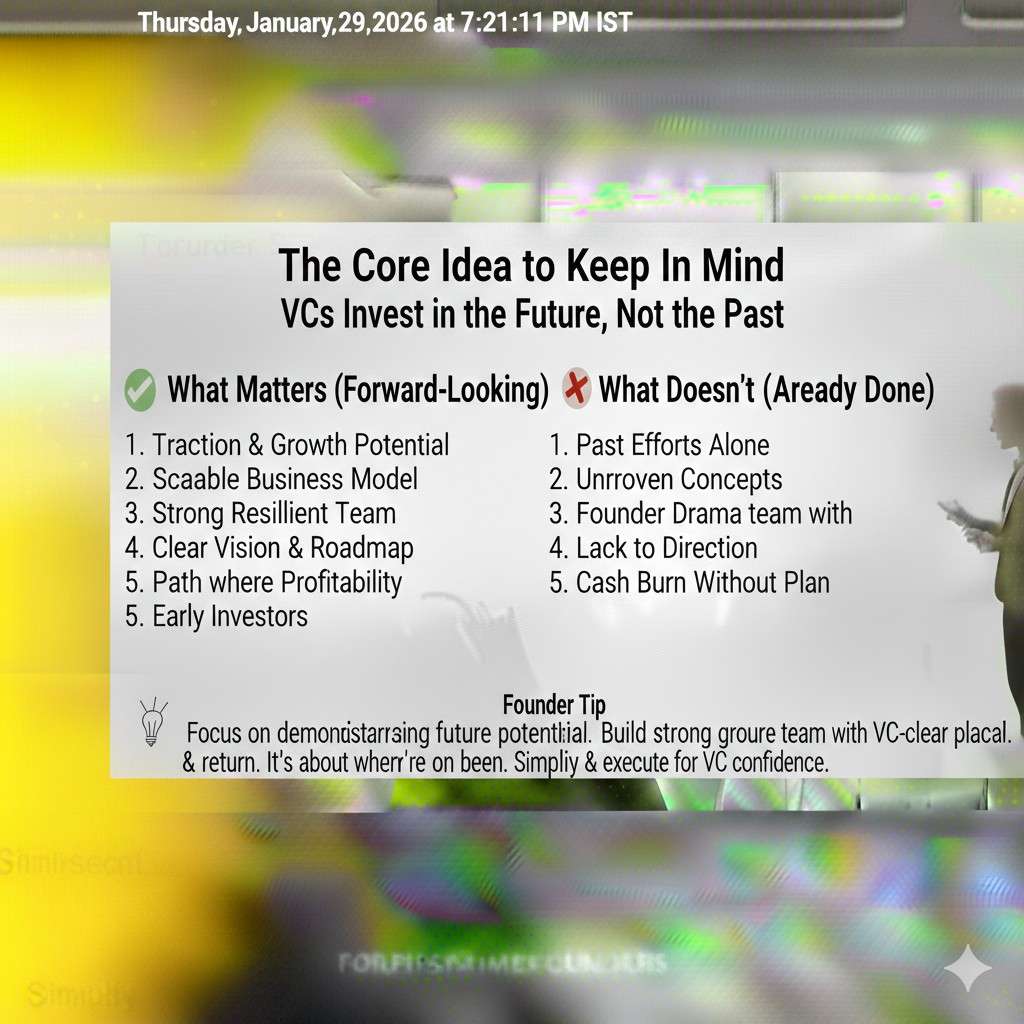

The core idea to keep in mind

At seed stage, your cap table should help you do three things at once. First, it should keep founders motivated and in control. Second, it should leave room to hire strong people. Third, it should be simple enough that new investors can understand it in minutes.

When these three are true, fundraising gets easier. Hiring gets easier. And when problems come up, you can fix them without breaking trust.

That is the standard you are aiming for. Not complicated. Not clever. Just clean and fair.

Start with the building blocks

Authorized shares and why they matter

Before anyone can own anything, the company must decide how many shares exist in total. This is called authorized shares. It is like choosing the size of the pie pan before you cut slices.

Founders often pick a large number, like 10,000,000 shares, because it makes grants feel “normal” and avoids odd decimals. The exact number matters less than consistency and simplicity. What matters is that you have enough shares to issue founder shares, set aside an option pool, and still have room for future rounds.

If you set the number too low, you will need to increase it later, which adds paperwork and cost. If you set it high, that is usually fine, as long as everyone understands that percentages are what matter, not raw share counts.

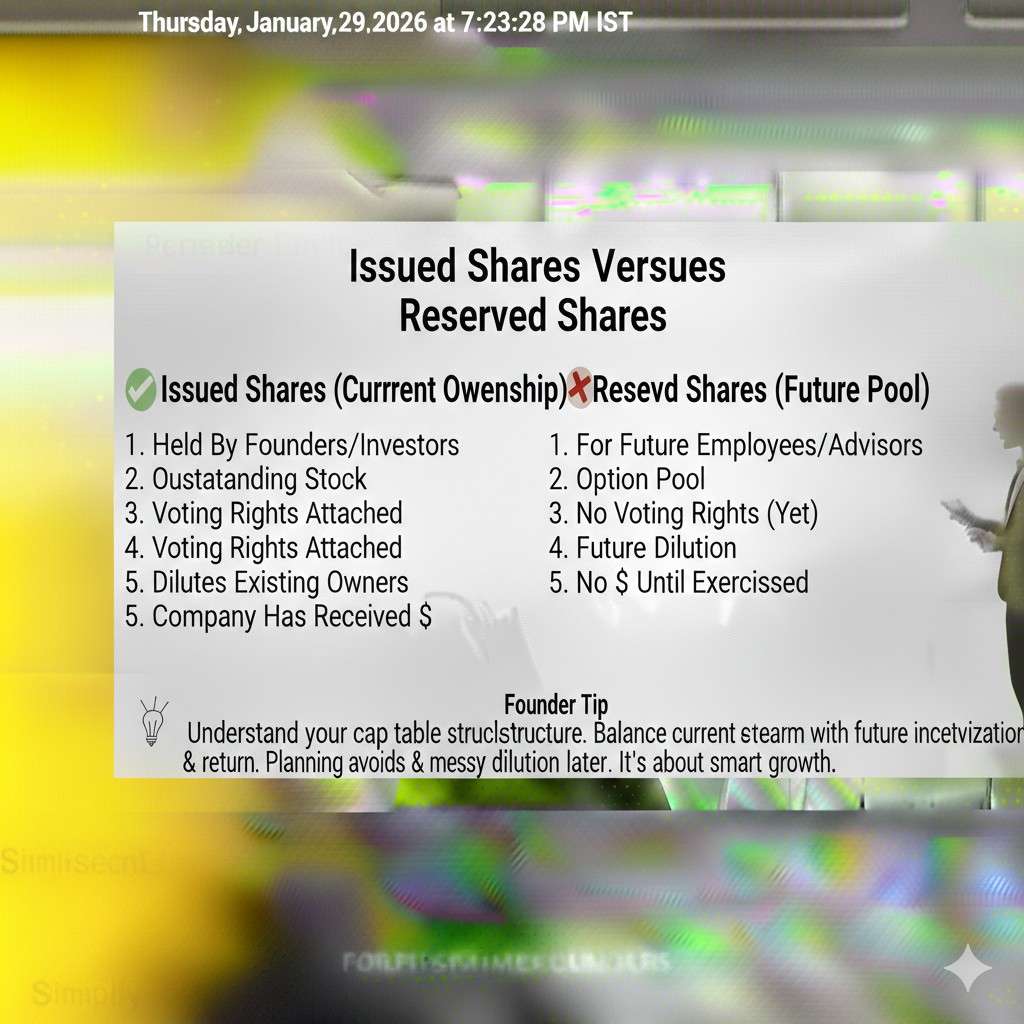

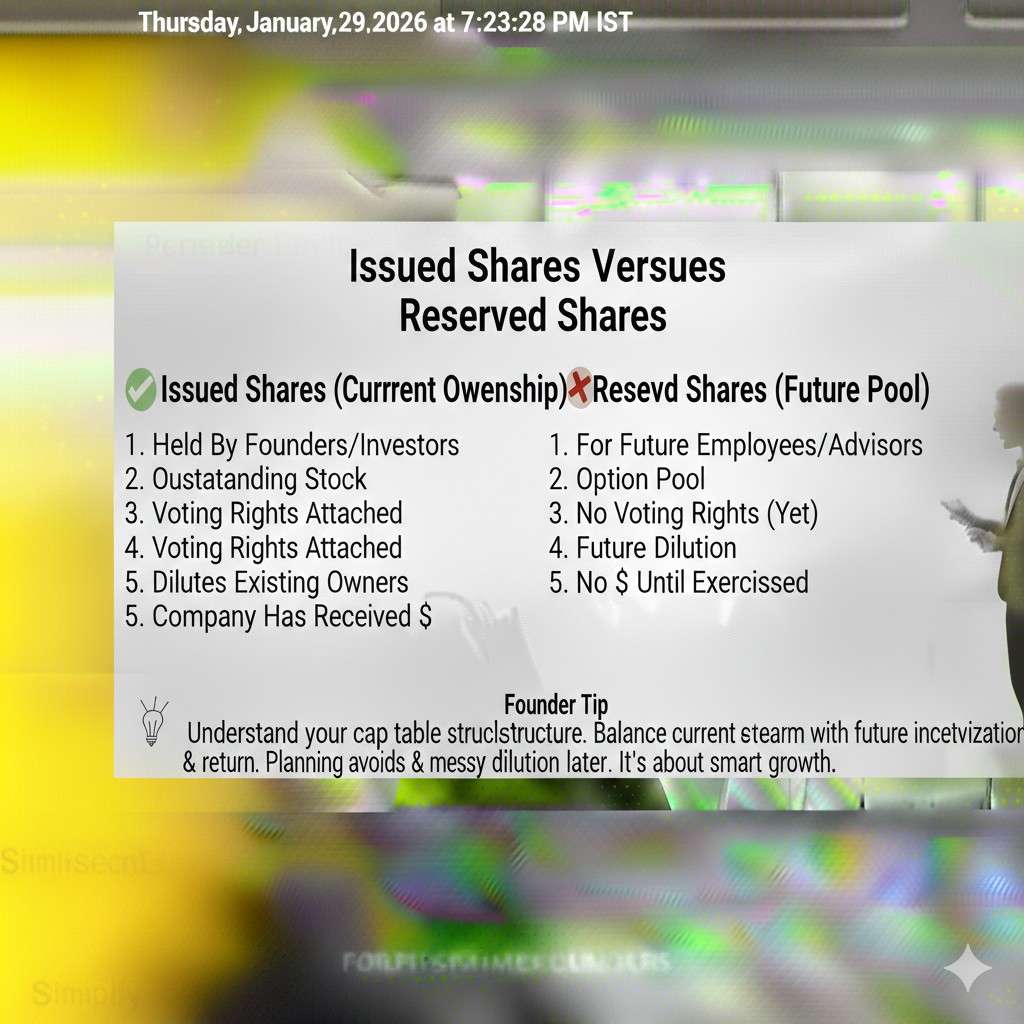

Issued shares versus reserved shares

Authorized shares are the maximum the company can issue. Issued shares are what you have actually given out. Reserved shares are shares you plan to issue later, often for an employee option pool.

This difference matters because founders sometimes think the cap table is only what is “issued.” But investors look at “fully diluted” ownership. That includes issued shares plus the reserved option pool, and often includes other rights to buy shares later.

If you do not plan for the reserved part early, you can accidentally corner yourself. Then when you need to hire, you will dilute founders more than expected.

Common stock and preferred stock

At the beginning, founders and employees usually hold common stock. Investors in priced rounds usually buy preferred stock. Preferred stock often comes with extra rights, like liquidation preferences, board rights, and protective provisions.

At seed stage, many startups do not start with preferred stock right away. They might use SAFEs or convertible notes first. Even then, you should understand that those instruments are designed to convert into preferred stock later.

The key is to keep your early structure simple, so that when preferred stock arrives, it fits cleanly.

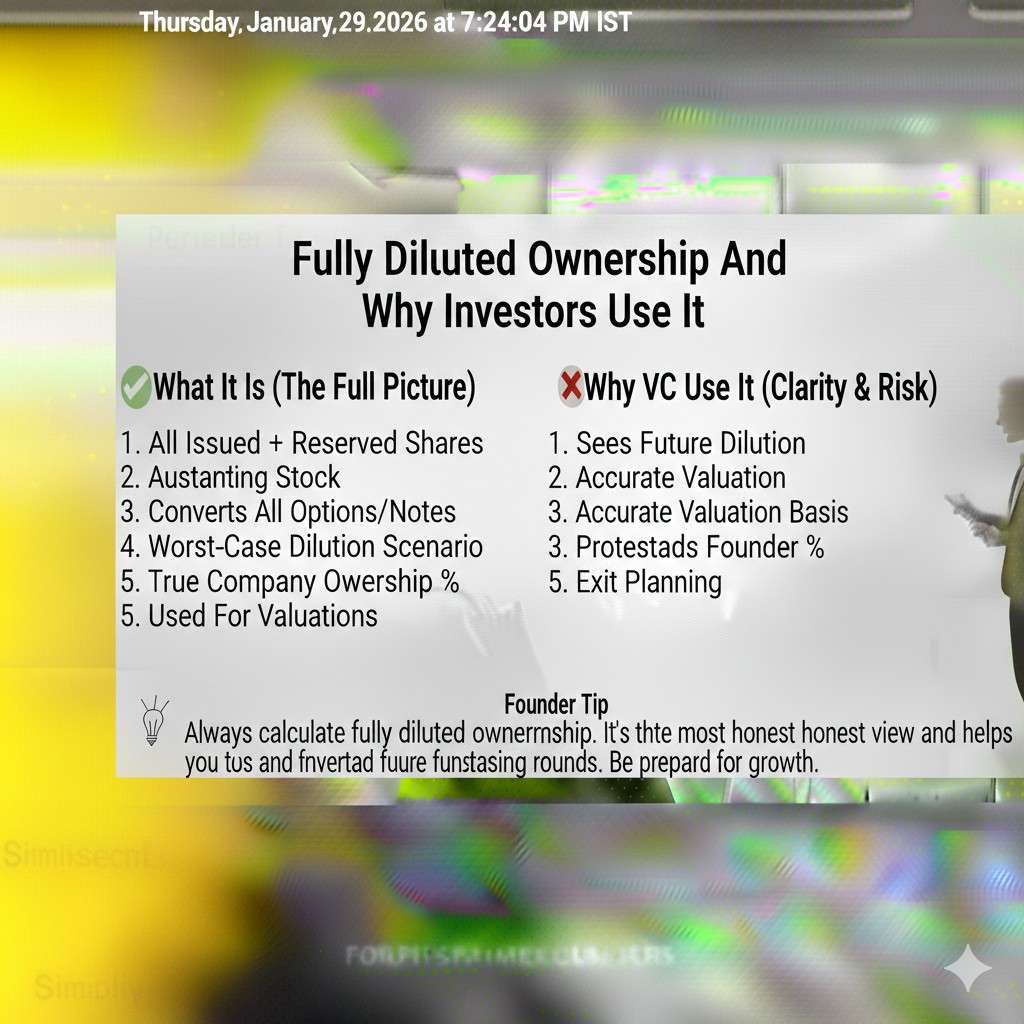

Fully diluted ownership and why investors use it

When an investor asks, “How much of the company do the founders own?” they usually mean on a fully diluted basis. That means assuming the option pool is filled and all convertibles convert.

Founders sometimes feel surprised by this, because the option pool might not be granted yet. But investors treat it as real dilution because it will be used to hire people. A cap table that ignores the pool is not realistic.

So when you model ownership, always look at the fully diluted picture. It will save you from false confidence and painful surprises.

If you want Tran.vc to help you think through this early, and pair it with a strong patent plan that makes your company more fundable, you can apply any time here: https://www.tran.vc/apply-now-form/

Founder equity: the first and most important decision

How to split equity without breaking trust

Founder splits are emotional because they are about more than work. They are about identity, risk, and fairness. The trap is to treat it like a one-time handshake deal. The healthier approach is to treat it like a clear agreement that can survive stress.

A fair split usually reflects three things: who is taking the most risk, who is doing the most core work, and who is hardest to replace. But even when you get the split “right,” it still needs vesting to keep it fair over time.

Without vesting, you can end up with a founder who leaves early but keeps a huge stake. That is the kind of cap table problem that scares off future investors and weakens the team.

Vesting is not a punishment, it is insurance

Vesting is the rule that equity is earned over time. The common approach is four years of vesting with a one-year cliff. That means if someone leaves before one year, they earn nothing. After the first year, they start earning monthly.

This protects everyone. It protects the company from dead equity. It protects co-founders from carrying someone who is no longer contributing. And it protects the departing founder from being treated unfairly if they put in real time and effort.

When founders avoid vesting because it feels awkward, they usually regret it later. It is easier to set the rule at the beginning than to negotiate it during conflict.

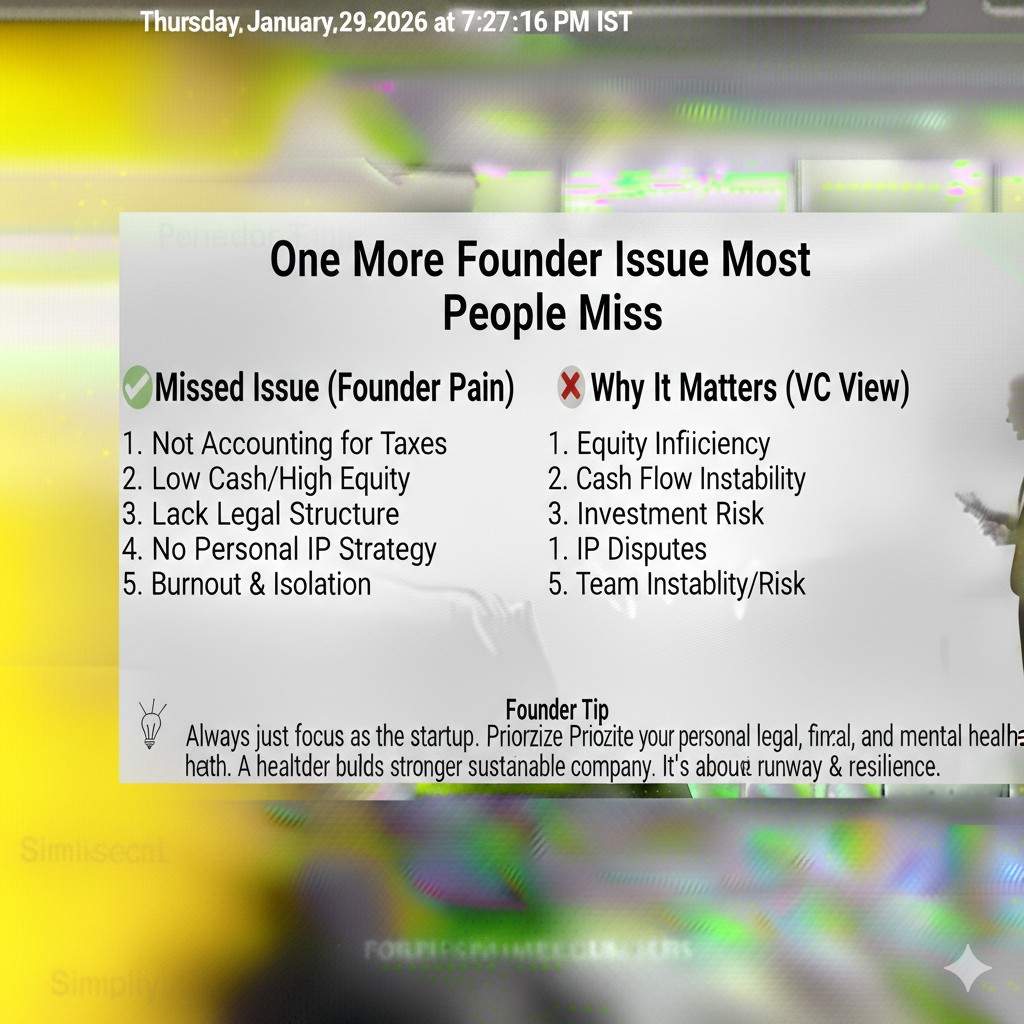

Founder stock and early tax steps

When founders buy common stock early at a very low price, there can be tax advantages. In the US, many founders consider filing an 83(b) election within a short window after receiving restricted stock. This is not legal or tax advice, but it is a common step founders discuss with counsel because it can affect how future gains are taxed.

The main point is practical: if you issue founder stock with vesting, you must handle the paperwork correctly. If you do not, you can create tax problems and legal confusion.

This is one reason many founders work with experienced startup counsel early. The cost of fixing it later can be higher than doing it right now.

One more founder issue most people miss

Many deep tech teams have a “technical founder” and a “commercial founder.” Sometimes the technical founder builds the core invention, while the commercial founder drives partnerships, pilots, and fundraising.

The risk is that the company becomes dependent on the technical founder’s invention but does not lock down the IP assignment correctly. If the IP is not properly assigned to the company, your cap table might be clean, but your company is still fragile.

That is why cap table setup and IP setup should happen together. Tran.vc focuses on that exact gap. You can apply any time here: https://www.tran.vc/apply-now-form/

Option pool: how to hire without panicking later

What an option pool is used for

An option pool is a set of shares reserved to reward future hires. At seed stage, this is how you recruit strong engineers, product leaders, and early operators without paying full market cash.

The option pool is also one of the most negotiated parts of a seed round. Investors often want to see a pool large enough to cover key hiring needs after the round.

If you do not plan the pool early, you may be forced to create it at the worst time, right before pricing a round. That can dilute founders more than expected.

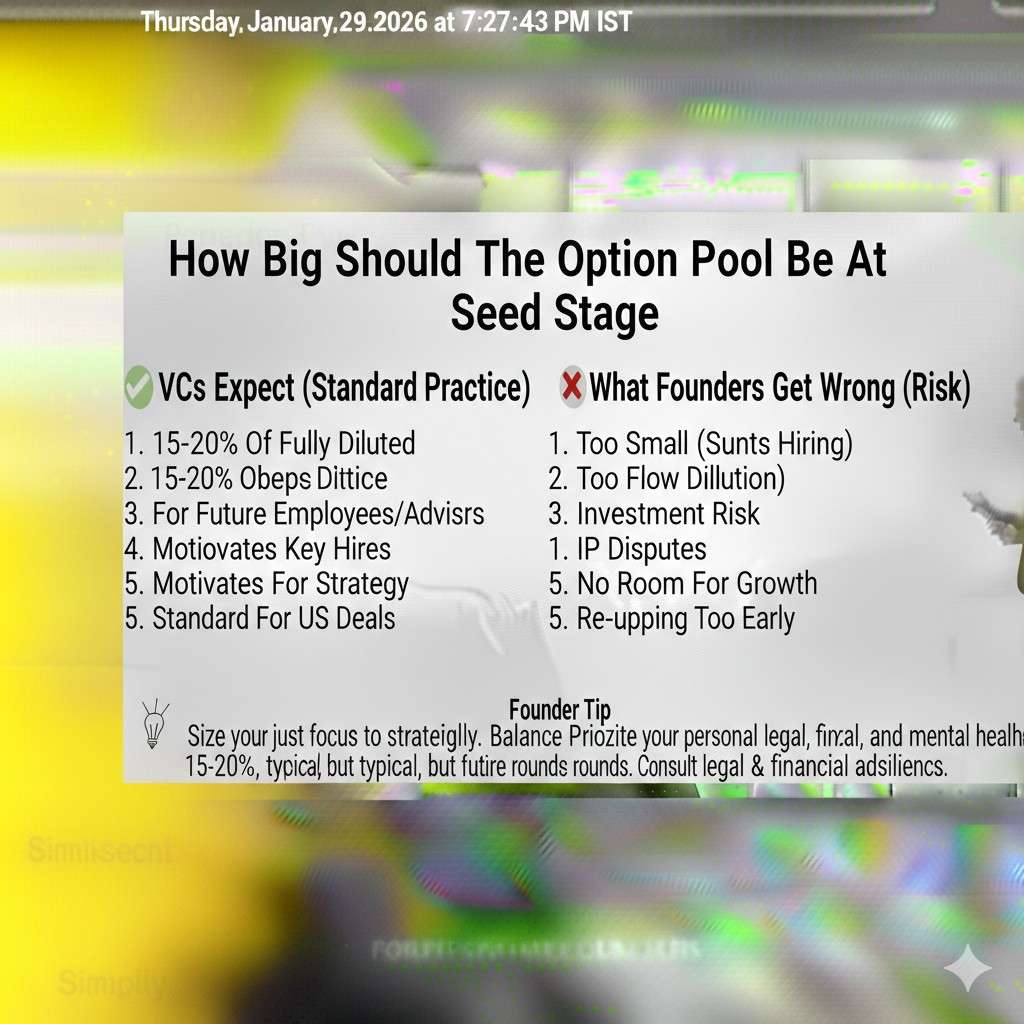

How big should the pool be at seed stage

There is no one right size. The “right” size depends on your hiring plan, the seniority of roles you need, and how competitive the market is for your talent.

In robotics and AI, hiring can be expensive and equity expectations can be higher, especially for key technical leaders. If you know you will need specialized talent, you should model that reality early.

A simple way to stay grounded is to map the next 12–18 months of hires and estimate equity ranges for each. Then you size the pool based on your real plan, not a guess.

Why the pool changes negotiation leverage

Many investors push for a “pre-money” option pool increase. This means the pool expansion happens before the investor money comes in. In practice, that pushes more dilution onto founders.

Founders who understand this can negotiate smarter. Sometimes the best move is not to fight the pool itself, but to align on a realistic hiring plan and avoid an oversized pool that just sits unused.

If your cap table is clean and your plan is credible, you can often keep this discussion calm and rational. If your cap table is messy, it becomes a power game.

Making equity grants without creating future chaos

When you grant options, use standard terms, clear vesting, and a clear exercise window. Avoid custom side deals that create special rights for one person. Those special rights almost always come back to haunt you.

Also, keep a clear record of board approvals and grant documents. If you later raise seed, investors will review this. Missing approvals and informal promises can slow down your round.

A cap table is not just numbers. It is proof that your company runs with discipline.

SAFEs and convertible notes

Why these tools exist in the first place

Most seed-stage startups are not ready to price the company. You may not have enough revenue, enough traction, or enough proof to pick a fair valuation and defend it. That is where SAFEs and convertible notes come in.

They let you raise money now, without locking in a priced valuation today. Later, when you do a priced seed round, these early instruments convert into shares, usually into preferred stock, under the rules written in the document.

Founders like them because they can be fast. Investors like them because they still get a deal that rewards early risk. But “fast” can hide landmines if you stack too many of them or accept terms you do not fully understand.

SAFE versus note, in simple language

A SAFE is a contract that says the investor will get shares later. It is not debt. There is usually no interest rate and no maturity date that forces repayment. It is meant to convert when you raise a priced round or hit another trigger.

A convertible note is debt that can convert into shares later. It usually has interest, and it usually has a maturity date. If you hit that date without converting, the company may need to renegotiate or repay, which can be stressful when you are still early.

Both tools can work. The best choice often depends on what is normal in your market and what your lead investor expects. The deeper point is that you should not treat either as “free money.” Both affect the cap table later.

Valuation cap, discount, and why they matter

A valuation cap sets the maximum price the SAFE or note converts at. If your priced round valuation is higher than the cap, the early investor converts at the cap, meaning they get more shares for the same dollars. That rewards them for taking early risk.

A discount gives the early investor a lower price than the priced round, often something like 10% to 25% off. If both a cap and a discount exist, the investor usually gets the better of the two outcomes.

Founders sometimes pick a cap without thinking about future dilution. A cap that feels harmless today can become a large ownership chunk later, especially if you raise multiple SAFEs at different caps. This is why you should model the outcomes before you sign.

The quiet risk of stacking SAFEs

One SAFE is easy to understand. Five SAFEs, raised at different times with different caps, can create a conversion math puzzle that surprises everyone.

The biggest problem is not the math itself. The biggest problem is founder shock at the moment of conversion. You think you are giving away a small slice, but when the priced round happens, the slice is bigger than expected, and you are forced to accept it because you already signed.

Another problem is investor trust. New seed investors want a cap table they can read quickly. If the SAFE stack is complex, you will spend time explaining it, and that time can slow down a round.

A smart goal is to raise early capital in a small number of clean instruments with terms that fit together. That way, conversion is predictable.

If you want support designing an early raise that keeps your cap table simple and also strengthens your IP moat for seed investors, Tran.vc can help. Apply any time here: https://www.tran.vc/apply-now-form/

How to model dilution before you sign anything

Why “I’ll figure it out later” is expensive

At seed stage, the biggest cap table mistakes come from delaying basic math. It feels reasonable to say, “We’ll do the numbers when we raise seed.” But the documents you sign now decide what the numbers will be later.

The simplest way to protect yourself is to run a dilution model every time you add a new money instrument. You do not need a fancy spreadsheet. You need a clear view of what happens if your next priced round is at a low valuation, a mid valuation, or a high valuation.

When you do this, you stop making emotional choices. You start making choices that protect founder control and future hiring room.

Three future scenarios you should always test

A useful model checks three cases. First, what happens if the seed valuation is lower than you hope. Second, what happens if it is right around your target. Third, what happens if it is higher than expected.

This matters because a valuation cap bites hardest when the priced valuation is high. Many founders assume dilution is worse when valuation is low, but with caps, the opposite can happen.

The point is not to predict the future perfectly. The point is to stop being surprised. If you can see the range, you can pick terms you can live with.

Pre-money and post-money SAFE language

Some SAFE templates are “post-money” SAFEs. That language can make it clearer how much of the company the SAFE buyer will own after the conversion, because it anchors ownership math in a defined way.

Some older styles can be harder to model because the ownership outcome depends on what else is in the round.

This is not about one being “good” and the other “bad.” It is about understanding what you are signing. When founders do not realize how the SAFE calculates ownership, they can sell more of the company than they intended.

Pro rata rights and why they can crowd your round

Some early investors ask for pro rata rights, meaning they have the right to invest more in later rounds to keep their ownership percentage.

This can be reasonable. But if you hand pro rata rights to too many small investors, you can create a crowding problem later. When you raise seed, the new lead investor wants a meaningful allocation. If your round is already filled by many early investors exercising pro rata, you lose flexibility.

That can force you to raise more than you planned, or it can force you to cut out a new investor you wanted. Both are avoidable if you are careful early.

Seed round mechanics that shape your cap table

What changes when you price the round

A priced seed round is different from SAFEs because it sets an actual valuation and issues preferred stock. That preferred stock often comes with rights that common stock does not have.

When you price a round, investors will look at the cap table and ask if it is “standard.” They want to see clean founder stock, a clear option pool, clean SAFE or note conversions, and no random grants with odd terms.

If anything looks strange, they will either ask you to fix it or price it into the deal. Either way, it costs you.

The option pool shuffle during seed

Many seed term sheets include a requirement that the option pool be increased before the money goes in. This is a very common point of tension.

The investor’s view is simple. They want you to have enough equity set aside to hire after the round, so their investment is not immediately diluted by a pool increase later.

The founder’s view is also simple. If the pool is increased pre-money, it feels like the founders are paying for it alone.

A practical way to handle this is to bring a real hiring plan to the conversation. If you can show exactly which roles you plan to hire and why, the pool size becomes a rational number rather than a negotiation trick.

Price per share and why it matters for everything else

In a priced round, the price per share becomes the anchor for many other actions. It affects how SAFEs convert. It affects how option grants are valued. It affects future 409A valuations and tax conversations.

That is why having clean documentation before the round matters. If the company has sloppy records, counsel will spend time correcting it, and that can delay closing.

Seed investors prefer teams that move with discipline. A clean cap table signals that discipline right away.

Liquidation preference and how it shows up later

Preferred stock often includes a liquidation preference, which affects who gets paid first if the company sells. Many seed deals have a “1x” liquidation preference, meaning investors get their money back before common stock holders get paid, depending on the structure.

This is not always a problem. It is often standard. The danger is when preferences stack in later rounds or when special terms are added that compound.

Even if you are focused on ownership percentages, you should also understand that payout rights can matter as much as percentage ownership in an exit.

If you want Tran.vc’s help building an investor-ready cap table while also building patents that make your seed round stronger, you can apply any time here: https://www.tran.vc/apply-now-form/