Convertible notes feel simple when everyone is in the same country.

You agree on a cap, a discount, an interest rate, and a date. Money comes in. You keep building. Later, the note turns into shares.

But the moment the founder is in one country, the company is in another, and the investor is somewhere else… the “simple” note turns into a quiet mess.

Not a loud mess. A hidden one.

It shows up as a slow close. A surprise tax bill. A bank that freezes wires. A lawyer who says, “We need to redo the paperwork.” An investor who gets cold feet because they have seen cross-border notes go wrong before.

This article is about that hidden friction—what creates it, why it catches smart teams off guard, and how to reduce it early so you do not pay for it later.

And because Tran.vc works with technical founders who are building real tech moats, we will treat this like a real operating problem, not a legal lecture. The goal is not to scare you. The goal is to help you close faster, stay clean, and keep control.

If you are building AI, robotics, or deep tech and you want to raise with leverage (not panic), you can apply any time here: https://www.tran.vc/apply-now-form/

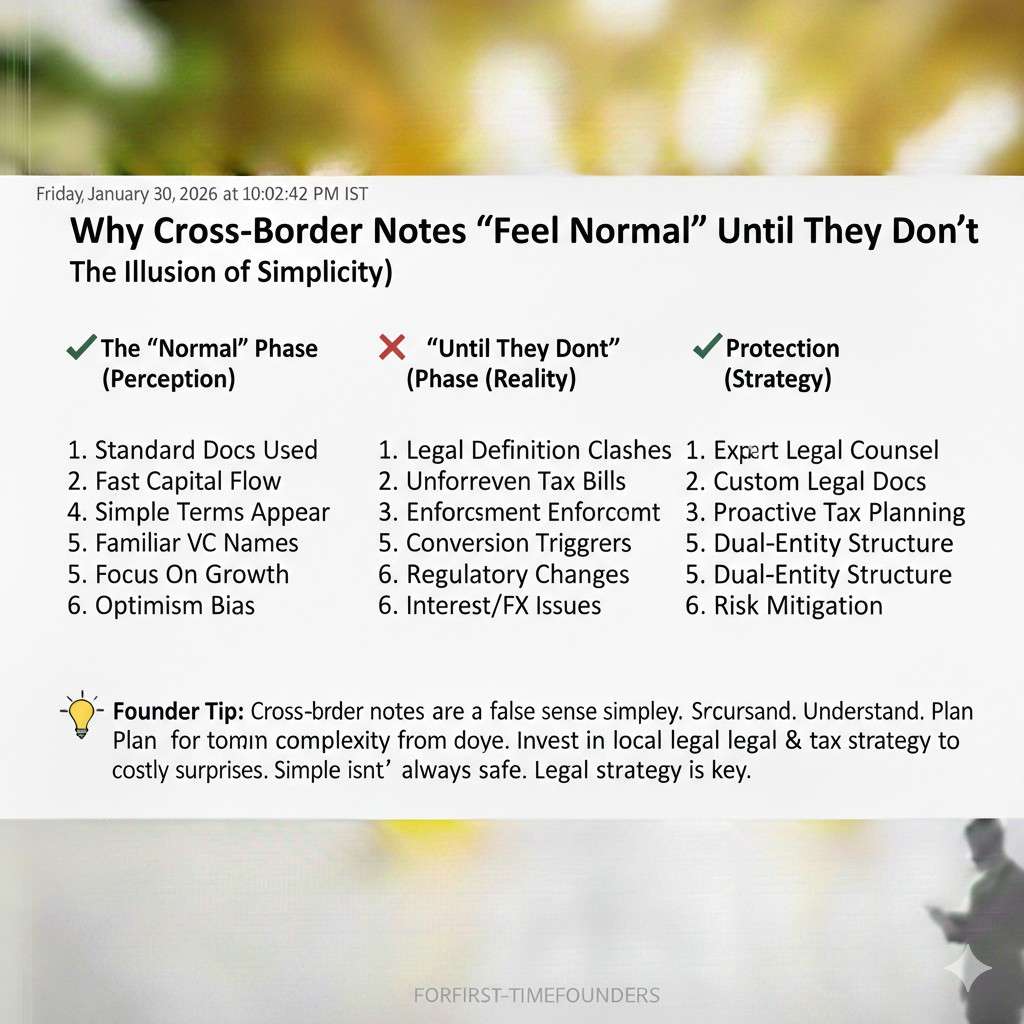

Why cross-border notes “feel normal” until they do not

A convertible note is a contract. The contract lives inside a legal system. It touches tax rules. It touches currency rules. It touches banking rules. It touches how your future equity round will work.

When all parties are inside one system, people already know the defaults.

In the US, many investors have seen thousands of notes. They know what “standard” looks like. They know what paperwork comes next. Their fund admin knows what to do. Their tax person knows what to expect.

Across borders, there are fewer shared defaults.

Founders often think the hard part is negotiating the cap. But the hard part is usually everything around the cap:

- Which country’s law controls the note.

- Whether the investor is even allowed to hold that kind of instrument.

- How interest is treated for tax.

- Whether the conversion is treated as a taxable event.

- How money moves in and out without breaking rules.

- Whether the note can be enforced if something goes wrong.

- Whether the next priced round can cleanly “pick up” the note.

Most founders only discover these issues when they are already trying to close. That is when friction becomes expensive—because you are tired, you need the money, and you start accepting bad compromises.

There is a simple mental model that helps: a cross-border note is not one deal. It is four deals happening at once.

- The funding deal (cap, discount, etc.)

- The legal deal (jurisdiction, enforceability, signatures)

- The tax deal (withholding, reporting, classification)

- The money-move deal (banking, FX, controls, compliance)

If any one of those fails, the whole thing slows down.

And here is the part investors do not always say out loud: slowness is risk. Risk makes investors cautious. Caution kills momentum. Momentum is your most valuable resource in an early round.

If you are reading this before you start sending the note out, you are already ahead.

The first hidden friction: “Where is the company really?”

Founders say, “We are a Delaware C-Corp.”

That helps, but it is not the full picture.

Investors and lawyers will quietly ask:

- Where are the founders physically located?

- Where is the real work being done?

- Where are key decisions made?

- Where are contractors and employees?

- Where are the bank accounts?

- Where is the IP actually created?

Those questions matter because many countries look at “management and control,” not just incorporation papers, when deciding tax residency. Some also look at “permanent establishment” risk—meaning your company could be treated as doing business in a country even if it is not incorporated there.

Why does this matter for a convertible note?

Because a note is often treated like debt until it converts. Debt has tax rules. Debt also has rules around payments, interest, and sometimes withholding. If your company is accidentally treated as tax-resident somewhere else, you might inherit rules you did not plan for.

This is also where many deep tech teams get hit: the founders are in one country, building the core product there, but the “fundraising entity” is in the US. It can be perfectly workable. But it must be structured cleanly, and the story must match the facts.

If there is a mismatch, your investor’s counsel will find it. And when they do, they will slow the deal down until it is clarified.

A practical way to think about it: your note investor is not only investing in your future. They are investing in your paperwork being boring.

Boring paperwork closes faster.

If you want help making your IP and your structure line up in a way investors trust, that is a big part of what Tran.vc does. You can apply here: https://www.tran.vc/apply-now-form/

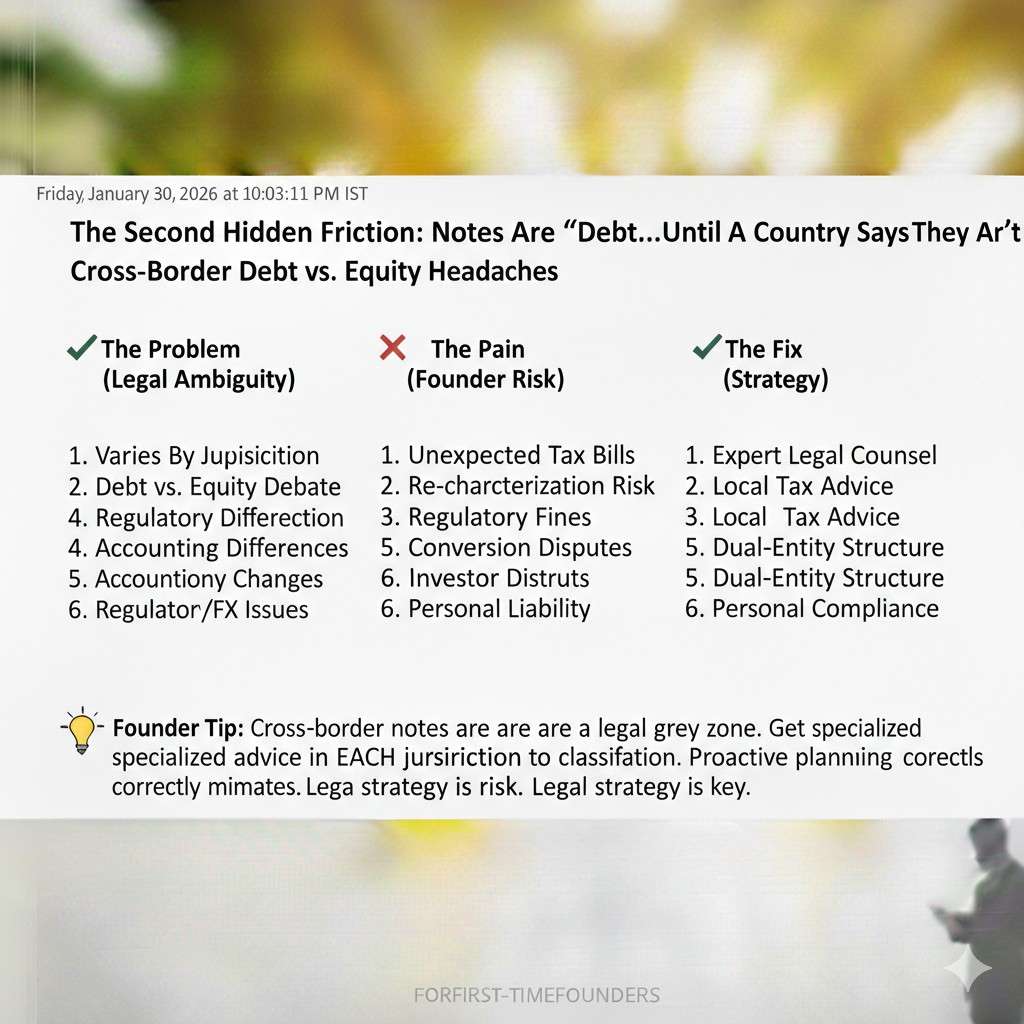

The second hidden friction: notes are “debt”… until a country says they are not

In one country, a convertible note may be treated like a loan.

In another, it may be treated like equity from day one.

In another, it may be treated like a derivative or a “security” with extra rules.

This classification changes everything:

- How interest is taxed.

- Whether interest must be withheld.

- Whether the company must file forms for the investor.

- Whether conversion is a taxable event.

- Whether the investor must report holdings in a special way.

This is not just theory. It shows up as real emails like:

“Our tax team says the interest is subject to withholding.”

Or:

“Our compliance team cannot hold this instrument.”

Or:

“We can invest, but only if you use a different doc set.”

Now you are rewriting documents mid-round. That is where friction becomes very real.

The founders often ask: “But we are not even paying interest in cash. It just accrues.”

That does not always matter.

Many tax systems do not care whether you paid interest in cash. They care that interest exists on paper. They treat it as income to the investor. And once it is “income,” they ask whether your company is required to withhold tax before paying it, even if you never pay it.

That sounds odd, but it is a common trap.

This trap grows sharper across borders because withholding is a cross-border tool. Countries use it to make sure they get their share when money goes to a foreign person.

So even if your investor is friendly, their tax counsel may say, “We need a withholding clause,” or “We need treaty language,” or “We need a tax form before we can fund.”

And if you do not have it ready, the wire waits.

The third hidden friction: your investor may be blocked by their own rules

This surprises founders most.

You think: “The investor wants to invest. They have money. We are good.”

But investors are not just people. They are entities with rulebooks.

A US venture fund may have limits in its LP agreement about what it can hold. A family office may have internal compliance rules. A corporation may have strict sign-off steps for cross-border deals. An angel in one country may face reporting requirements or currency rules that make it hard to wire funds out.

So the question is not only: “Can we issue a note?”

It is also: “Can the investor legally and practically buy it?”

Some investors do not like holding debt in foreign companies. Some do not like instruments that are not standard in their home system. Some require local counsel to review anything that crosses borders.

Even if they love your product, this can slow or kill the check.

The best founders reduce this risk by doing something unglamorous early: they make the round easy to buy.

That means:

- Using documents investors already know.

- Having clean cap tables and board approvals.

- Having a bank that can receive wires quickly.

- Having a clear story for where the company operates.

- Having basic tax forms ready when needed.

Not because you enjoy paperwork. Because paperwork is a sales tool.

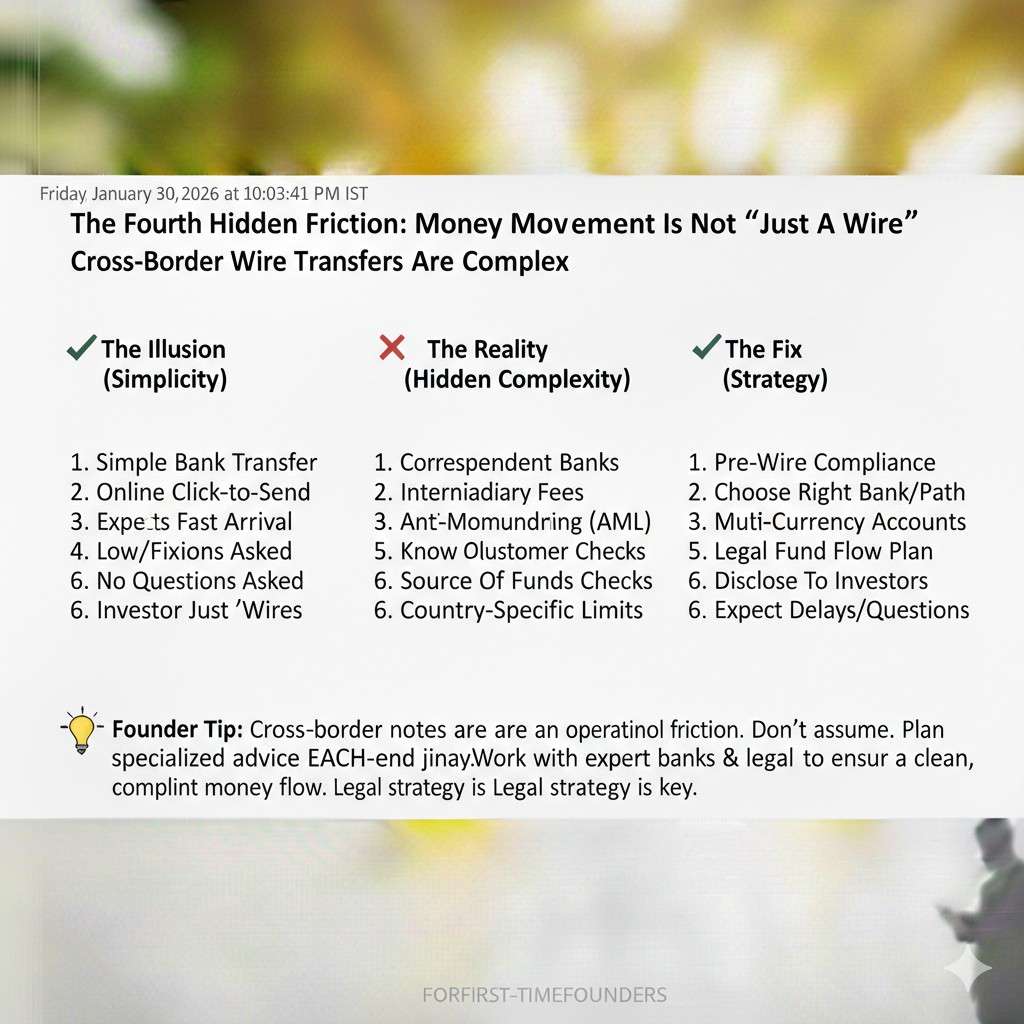

The fourth hidden friction: money movement is not “just a wire”

If you have only raised from investors in one country, you might think wiring money is a solved problem.

Across borders, wires can get stuck for reasons that have nothing to do with you:

- A bank asks for extra proof of source of funds.

- A bank asks for proof of services or an invoice.

- A bank asks for a board resolution.

- A bank flags the transaction for compliance review.

- The investor’s bank requires beneficiary details that do not match your account.

- The transfer triggers currency control thresholds.

Sometimes the wire bounces. Sometimes it sits in limbo. Sometimes the bank freezes the receiving account until you provide more documents.

Founders often treat this as a random event. It is not random. It is predictable when you know the patterns.

The key pattern is this: banks become strict when they do not understand the transaction.

A convertible note is not a normal consumer transfer. It is not a product payment. It is not a salary. It is an investment into a startup.

If the bank staff does not have a clear category for it, they ask questions. If the answers are unclear, they escalate. Escalation means delay.

This is why many experienced founders keep a “wire pack” ready: a simple set of documents that explain what the money is and why it is allowed.

You do not need to overbuild it. You just need enough to make compliance feel safe.

What hidden friction does to your company when you are not watching

There are three quiet costs.

First, it lengthens your round. You lose momentum. You waste time. Your build speed drops.

Second, it changes your power. When you need cash and you are stuck in delays, you are more likely to accept worse terms.

Third, it leaves residue. Badly drafted cross-border notes can create weird cap table problems later. And weird cap table problems show up at the worst possible time: during a priced seed round.

Seed investors want a clean story. If they see messy notes with unclear tax treatment, unclear conversion mechanics, or jurisdiction problems, they push for clean-up. Clean-up can mean legal fees, forced amendments, or investors refusing to sign.

So the goal is not “perfect.” The goal is “clean enough that the next round is easy.”

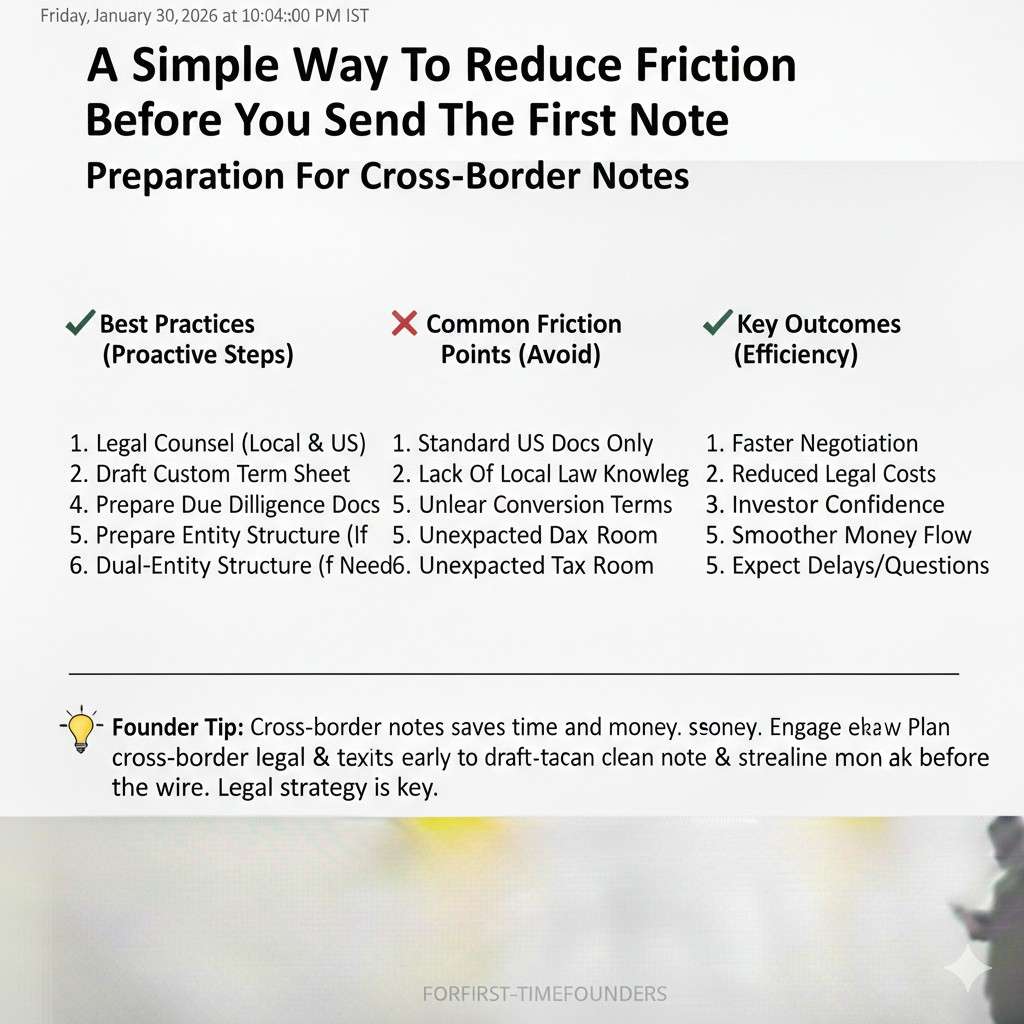

A simple way to reduce friction before you send the first note

Think in terms of pre-work, not fixes.

When founders do pre-work, the round often feels smooth.

When founders skip pre-work, the round becomes a series of emergencies.

The pre-work usually includes:

- Picking one clear governing law and forum for disputes.

- Making sure the note fits your jurisdiction and your investor’s common expectations.

- Setting up a bank path that can handle international wires.

- Making your IP story and your company structure match reality.

- Ensuring your conversion mechanics will not break the next priced round.

For Tran.vc founders, the IP piece is not a side note. In deep tech, your note investors often want to know that the key inventions will end up owned by the right entity, with clean assignments, and that the patent plan is real.

That is part of why Tran.vc invests up to $50,000 in-kind in patent and IP services. Not as “nice to have,” but because it reduces risk and raises your leverage.

If you want to build an IP-backed foundation before you raise your seed, apply here: https://www.tran.vc/apply-now-form/

The term sheet illusion in cross-border notes

Why the same words behave differently in different countries

A convertible note looks familiar on the surface. Cap, discount, interest, maturity. Most founders feel relief when they see those words because they think the rules are known. The illusion is that these words mean the same thing everywhere. They do not. Each country wraps these terms in its own legal and tax logic, which changes how they behave in practice.

What feels like a small wording choice can shift how a regulator, a tax authority, or a future investor reads the instrument. This is where cross-border friction hides best—inside language that looks standard but is not treated as standard once it crosses a border.

Why “market standard” often stops at the border

Founders often hear, “This is market standard.” What is usually meant is “market standard in my country, for my fund, under my rules.” Once the note crosses into another system, those standards fade.

In cross-border deals, there is no single market. There are overlapping systems with different defaults. If you rely on “standard” without asking “standard where,” you are handing control to whoever notices the mismatch first. That is rarely the founder.

Valuation caps and the geography problem

How caps feel simple but create hidden pressure

Valuation caps are emotional. They anchor expectations. Founders focus on keeping them high. Investors focus on keeping them reasonable. Across borders, caps quietly take on another role. They become signals to tax authorities and future investors about how the company was valued at an early stage.

In some countries, a low cap can be used as evidence that the company itself believed it was worth very little. That can later affect transfer pricing discussions, option pricing, or even questions around whether value was shifted across borders.

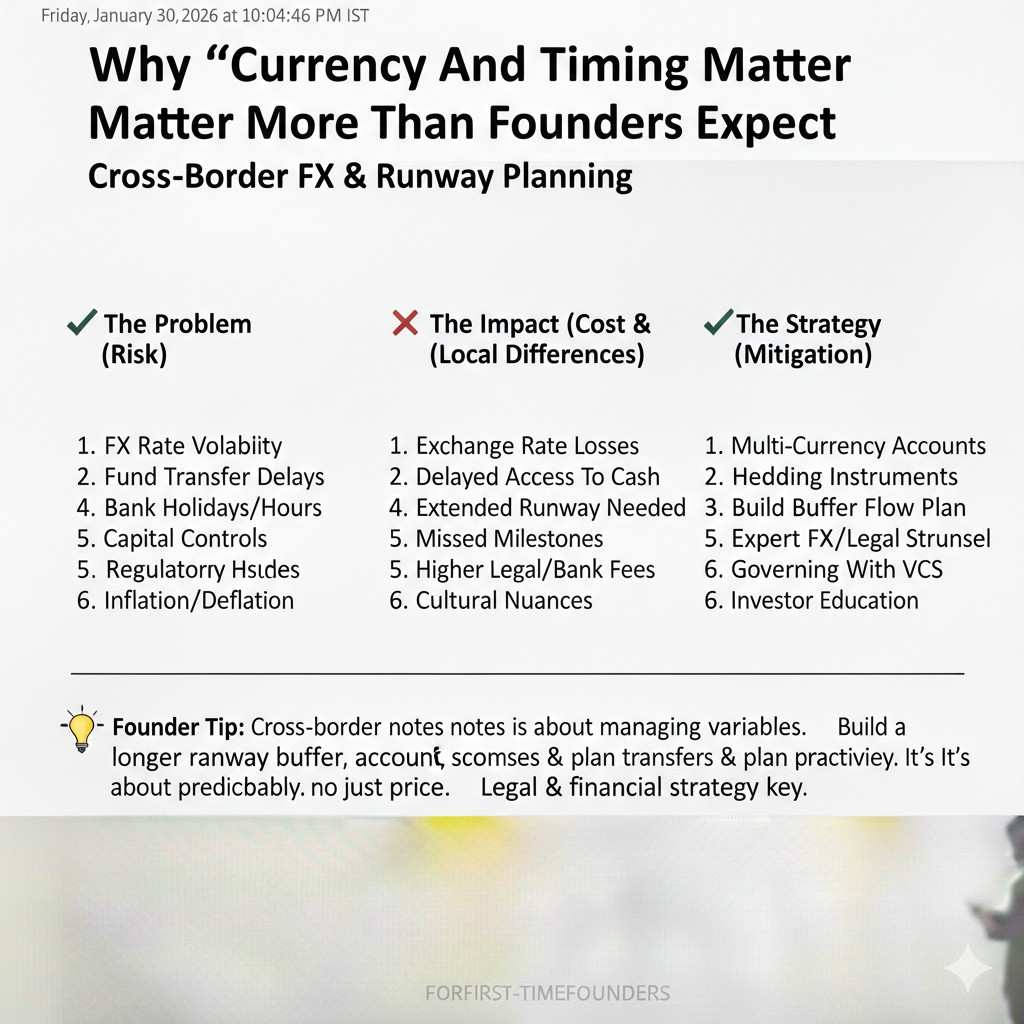

Why currency and timing matter more than founders expect

Caps are often written in one currency. The company may operate in another. The next priced round may be negotiated in a third. Currency movement alone can change the real economic meaning of a cap over time.

More importantly, the timing of when a cap is “tested” matters. In some systems, the moment of conversion can trigger scrutiny. If the cap is far from reality by then, questions follow. None of this kills a company, but all of it adds friction when you least want it.

Discounts and their quiet tax shadows

Why discounts are not always neutral

A discount feels harmless. It rewards early risk. In one country, it is just a pricing mechanic. In another, it may be viewed as a form of compensation or benefit. That framing matters for tax.

If a discount is treated as value transferred at conversion, some authorities may view it as taxable to the investor or even to the company. Founders rarely plan for this because it is not obvious from the document itself.

How future investors read early discounts

Seed investors read early notes closely. Heavy discounts can signal desperation or poor leverage, even if that was not the reality. In cross-border contexts, they also raise questions about whether early investors received special treatment that needs to be cleaned up.

This does not mean discounts are bad. It means they should be chosen with awareness of how they will be read later, not just how they feel now.

Interest: the smallest number with the biggest confusion

Accrued interest is still interest

Many founders dismiss interest because it is small and often never paid in cash. That is a mistake in cross-border notes. Interest exists even when it is only on paper.

Some tax systems treat accrued interest as income every year. That can trigger reporting or withholding duties, even if no money moves. When founders discover this late, they are forced into awkward fixes or explanations.

Why zero interest is sometimes cleaner

In some cross-border cases, setting interest at zero is not laziness. It is strategy. It removes an entire class of questions.

This is not always possible or desirable, but it is worth considering early. Reducing complexity is often more valuable than squeezing a small economic edge.

Maturity dates and enforcement reality

The myth of “we will just extend it”

Founders often treat maturity dates as symbolic. Everyone assumes the note will convert. Across borders, maturity is more serious. Once a note technically matures, it becomes enforceable debt.

In some countries, that changes how it must be reported or treated. In others, it gives investors rights that neither side actually wants to exercise. Extending maturity later may require formal steps that are slow and visible.

How enforcement risk changes investor behavior

Even friendly investors think about worst cases. If enforcement across borders is unclear, they may push for stronger terms upfront. That increases friction before money even arrives.

Clear maturity mechanics and realistic extension language reduce this fear. They tell investors that the founders have thought about outcomes, not just hopes.

Most-favored-nation clauses and cross-border spillover

When MFN sounds fair but spreads complexity

MFN clauses promise fairness. If later investors get better terms, early ones match them. In a single jurisdiction, this is manageable. Across borders, MFN can become a mess.

Later notes may be structured differently to satisfy local rules. An MFN can unintentionally pull those differences into earlier notes, creating conflicts or obligations no one intended.

Why simplicity protects you later

Many experienced founders limit MFN scope or avoid it entirely in cross-border rounds. This is not about being unfriendly. It is about containment.

The simpler each note is, the easier it is to explain, convert, and clean up when the priced round arrives.

Conversion mechanics and the seed round test

The moment everything comes due

Conversion is where all assumptions are tested at once. If the note language does not line up with the seed round structure, delays follow. Lawyers step in. Investors ask for changes.

In cross-border cases, conversion can also trigger tax or reporting events that were invisible at signing. This is why clean mechanics matter more than clever ones.

Why future investors care more than current ones

Your current note investors already said yes. Your future seed investors have not. They will review every note as if they might inherit its problems.

If they see friction, they price it in. Sometimes that means lower valuation. Sometimes it means more control terms. Sometimes it means walking away.

This is why thinking one round ahead is not optional in cross-border notes. It is survival.