Repatriation sounds like a big finance word, but the idea is simple: it’s how money moves back into a country, or out of a country, in a legal and well-documented way.

If you run a startup that touches more than one country—maybe you have a U.S. parent company with an India team, or you sell to customers in Europe, or you raised money from an overseas investor—this topic stops being “nice to know.” It becomes a real risk area. Not because you did anything wrong, but because banks, tax teams, and regulators care a lot about where money came from, why it moved, and whether the paperwork matches the story.

This guide is here to make that story clear.

When founders hear “getting money in and out,” they often think of only one moment: wiring funds from an investor, or paying an overseas contractor. But repatriation is bigger than that. It includes how you bring revenue home, how you move profits (if you have them), how you pay for tools and cloud services, how you send money to a related company you own, how you reimburse founders, how you handle dividends, and how you avoid the kind of sloppy records that create issues later during due diligence.

And this matters even more for deep tech founders.

If you build robotics or AI, your company value is often in what you created: your code, models, hardware designs, data work, and the inventions behind it. Money movement and IP usually connect in ways founders don’t expect. For example: who paid for the work that created the invention? Which entity owns the invention? Which country was the work done in? When investors ask these questions, they are not being picky. They are checking if your company can safely scale without future legal surprises.

At Tran.vc, we see this pattern all the time. A strong product is not enough. Clean structure and clean records make fundraising easier. They also make it easier to protect your edge with patents and solid IP ownership—especially when your team and customers are spread across borders. That’s why we invest up to $50,000 in in-kind patent and IP services for AI, robotics, and other technical startups—so you build a defensible base early, without giving up control too soon. If you want help building that base, you can apply anytime here: https://www.tran.vc/apply-now-form/

What “Repatriation” Really Means

The plain meaning founders can use

Repatriation is the lawful movement of money across borders, with a clear reason and a clean record. It can mean money coming into your home country, money going out, or money moving between companies you control in different places. The key is not the direction. The key is whether the “why” and the “paper trail” match.

A bank does not want poetry. It wants a simple story that can be proven fast. Where did the money come from, what is it for, who is receiving it, and what document supports it. If the story is clean, transfers feel routine. If the story is messy, even honest transfers can get stuck.

Why it becomes a startup risk, even early

Startups cross borders earlier than ever. You may have a Delaware company, a team in India, and cloud bills in Singapore. You may take payment from a customer in Germany and pay a contractor in Canada. None of this is wrong. But each move becomes a “case file” in the bank’s system.

When you later raise a priced round, investors and lawyers look back. They want to see that each transfer had a reason and a matching contract, invoice, or board approval. If they see confusion, they start asking if there is hidden tax or legal risk.

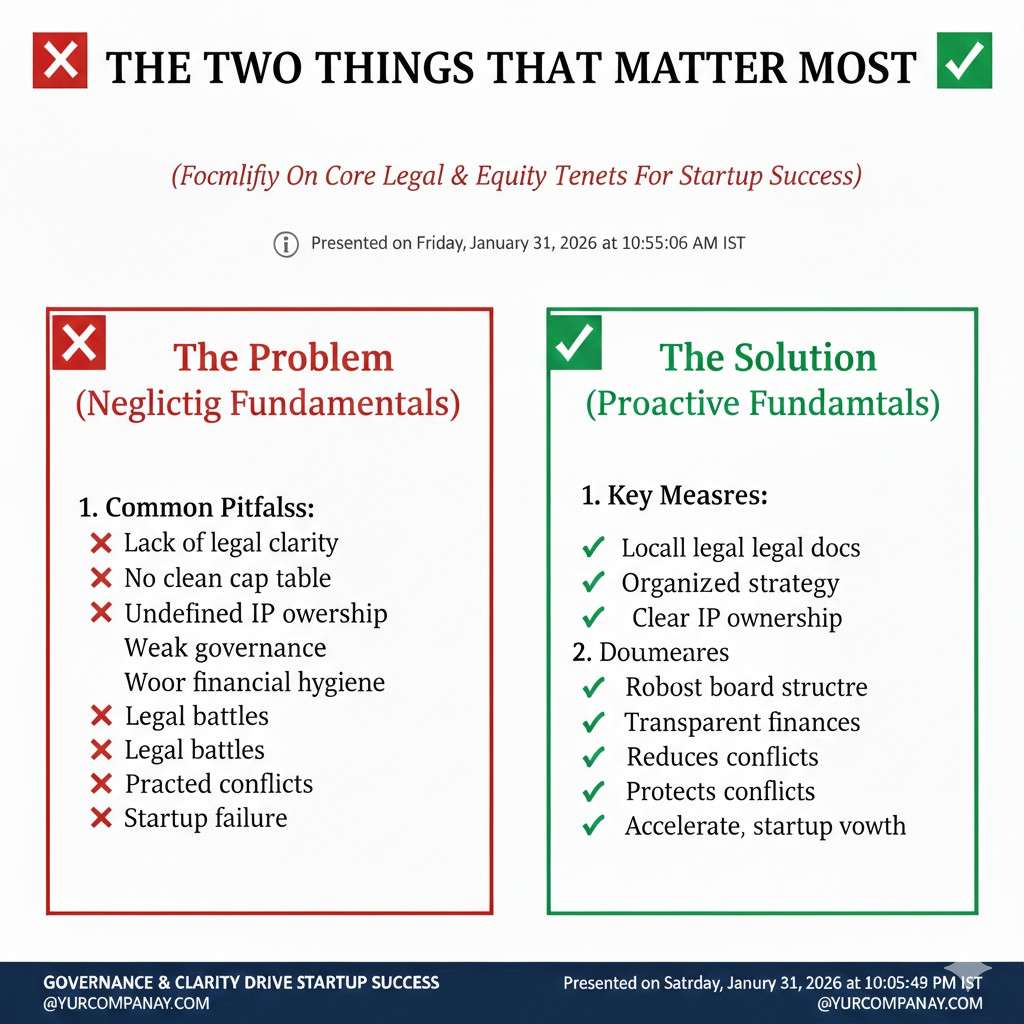

The two things that matter most

In real life, repatriation is less about the transfer and more about classification. The same wire can be treated very differently depending on what it is. A loan is not the same as revenue. A service payment is not the same as a dividend. A capital contribution is not the same as a reimbursement.

The second thing is proof. Regulators and banks are not reading your mind. They are reading your documents. If your documents are thin, they assume the worst. If your documents are clear, they assume the normal.

The Main Buckets: What Your Transfer Is “Called”

Capital coming in: equity and investor money

When an investor sends money, the clean way is to treat it as capital. That means you have a signed agreement, clear investor details, and proof of approval inside the company. In many places, the bank also wants a short note that explains the purpose, like “subscription for shares” or “equity investment.”

Founders sometimes take shortcuts here, like receiving money into a personal account and then forwarding it. That creates confusion right away. It also makes it harder to prove where the money came from and why it moved. If you want due diligence to feel smooth later, keep investor money inside the company path from day one.

Revenue coming in: customer payments and exports of services

If you sell software or services to a foreign customer, that inflow is usually treated as business income. Banks and tax teams often want to see invoices, a contract, and basic details about what was delivered. They also may want to match the payment to the invoice amount and date, or at least understand why it differs.

Founders get into trouble when they mix revenue with other inflows. For example, if a customer prepays for work, that is still revenue related, but your accounting treatment may differ. The bank does not need your accounting theory. It needs a clear business reason and supporting documents that look real.

Expenses going out: tools, cloud, contractors, and vendors

Money leaving the country is common and often normal for startups. You pay for cloud hosting, design, legal work, testing tools, and maybe manufacturing parts. These are usually “current account” style payments in many systems, meaning routine business expenses, but the bank still wants to know what the payment is for.

The fastest way to keep these payments smooth is to standardize your paperwork. Keep the vendor contract, invoice, and proof of delivery or service. When the bank asks, you should be able to show it in minutes, not days.

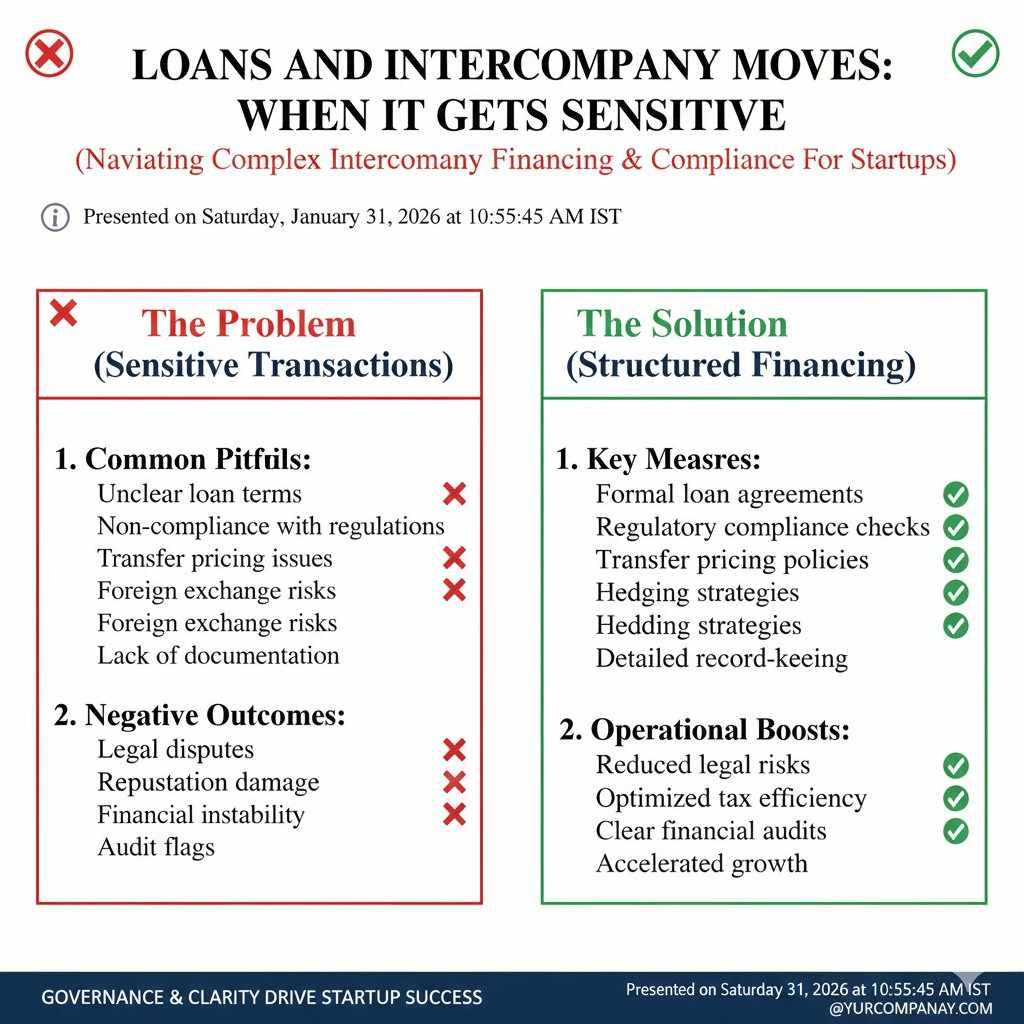

Loans and intercompany moves: when it gets sensitive

If money moves between two companies you own, you must decide what it is before you send it. Is it a loan? Is it a capital infusion? Is it a payment for services? Is it a reimbursement? Each choice has different rules, different tax impact, and different documents.

This is where founders often guess, and guessing is expensive later. If you send money as a “loan” but never document terms or repayment, it starts to look like something else. If you send money as “services” but there is no services agreement, the payment can be questioned. Clear structure upfront is cheaper than cleanup later.

Profit going out: dividends and distributions

Dividends are not just “sending profit home.” They usually require that your company has profit under local rules, proper approvals, and sometimes proof that taxes were handled. Many early-stage startups do not pay dividends at all, but some founders try to pull money out this way without realizing how formal it is.

If you are at an early stage, it is often safer to treat founder cash-outs as salary, reimbursements, or approved expense payments, depending on what is true. Dividend planning belongs later, when your finance function is stronger and the company is stable.

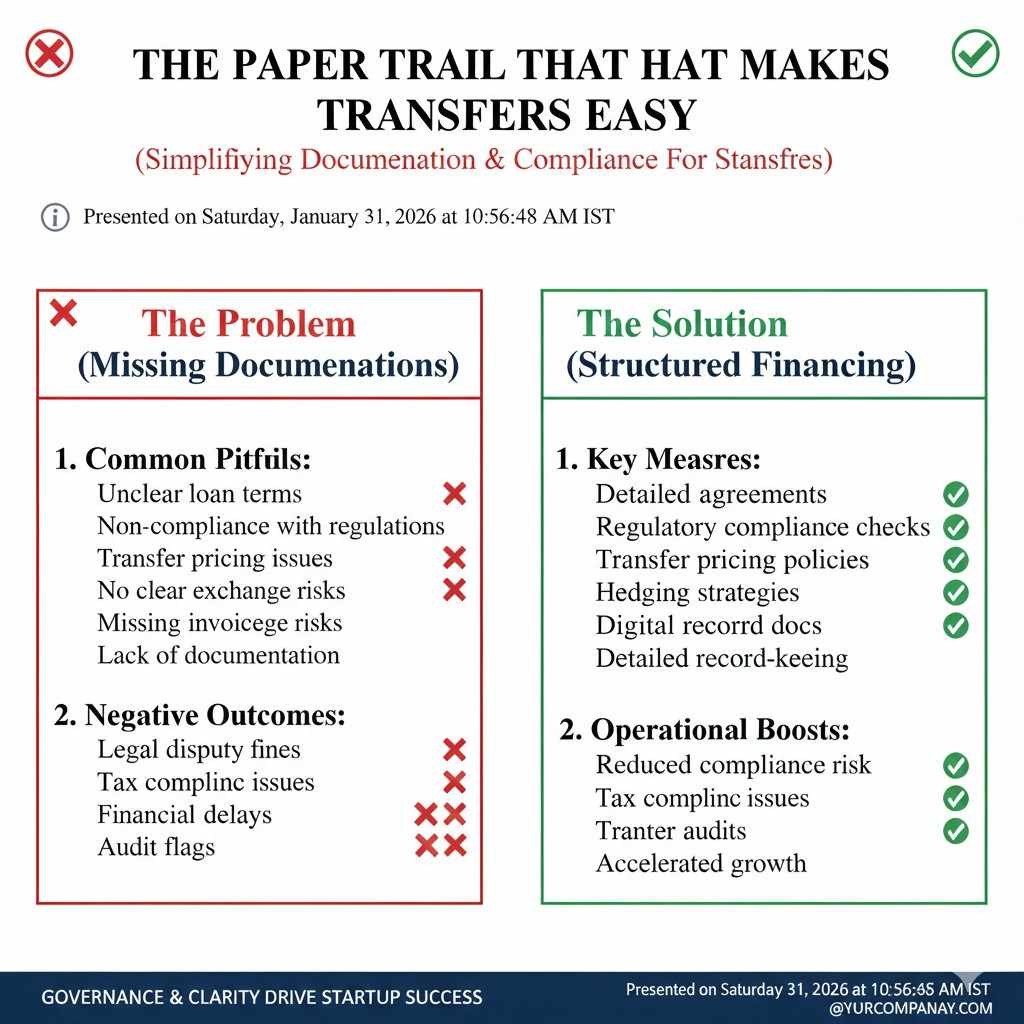

The Paper Trail That Makes Transfers Easy

The “transfer packet” mindset

A good habit is to treat every cross-border transfer like it needs a small packet of proof. Not a book. Just the few pages that answer the bank’s questions. Most banks are not trying to block you. They are trying to protect themselves, because they are audited and can be fined.

If you build a simple packet each time, your bank learns that your company is clean. That speeds up approvals. It also makes your records strong when investors ask questions.

What banks usually want to see, in plain terms

Banks usually want three basic items: who you are paying or receiving from, what the payment is for, and proof that the reason is real. Proof is often a contract and an invoice. For payroll-like payments, it might be an agreement and a payslip record. For capital, it is usually investor documents and company approvals.

The bank may also ask for a short purpose code or purpose description. This is not a trap. It is how banks label transactions for their own rules. If your description is vague, they will ask more questions. If it is specific and matches your documents, they move faster.

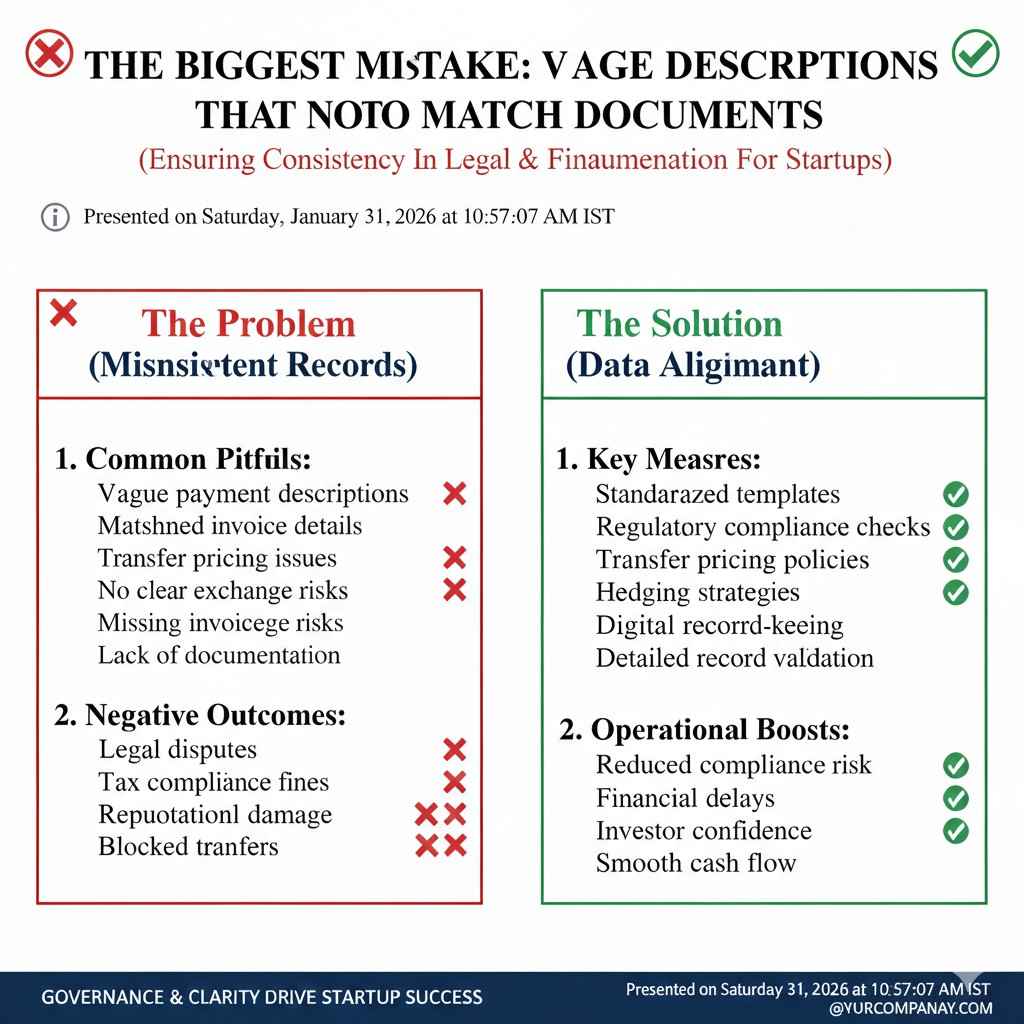

The biggest mistake: vague descriptions that do not match documents

Founders sometimes write “consulting” for everything. Or they write “services” without saying what. When a bank sees the same broad word repeated across many payments, it looks like someone is hiding details. You may not be hiding anything, but the bank cannot assume that.

A better approach is to use simple, true descriptions. “Monthly cloud hosting invoice,” “prototype design services per SOW,” “patent filing fees,” “software development milestone payment.” Clear words reduce follow-up questions.

Getting Money Into the Country Legally

Start with the reason, not the wire

Before you bring money in, decide the correct category. Is it investor money, customer revenue, a grant, a refund, or a loan? If you do this first, your documents will match your story. If you wire first and decide later, your records start with confusion.

For startups, the most common inflows are investment and revenue. Each needs its own clean lane. Keep them separate in your accounting, and do not mix them in emails or internal notes.

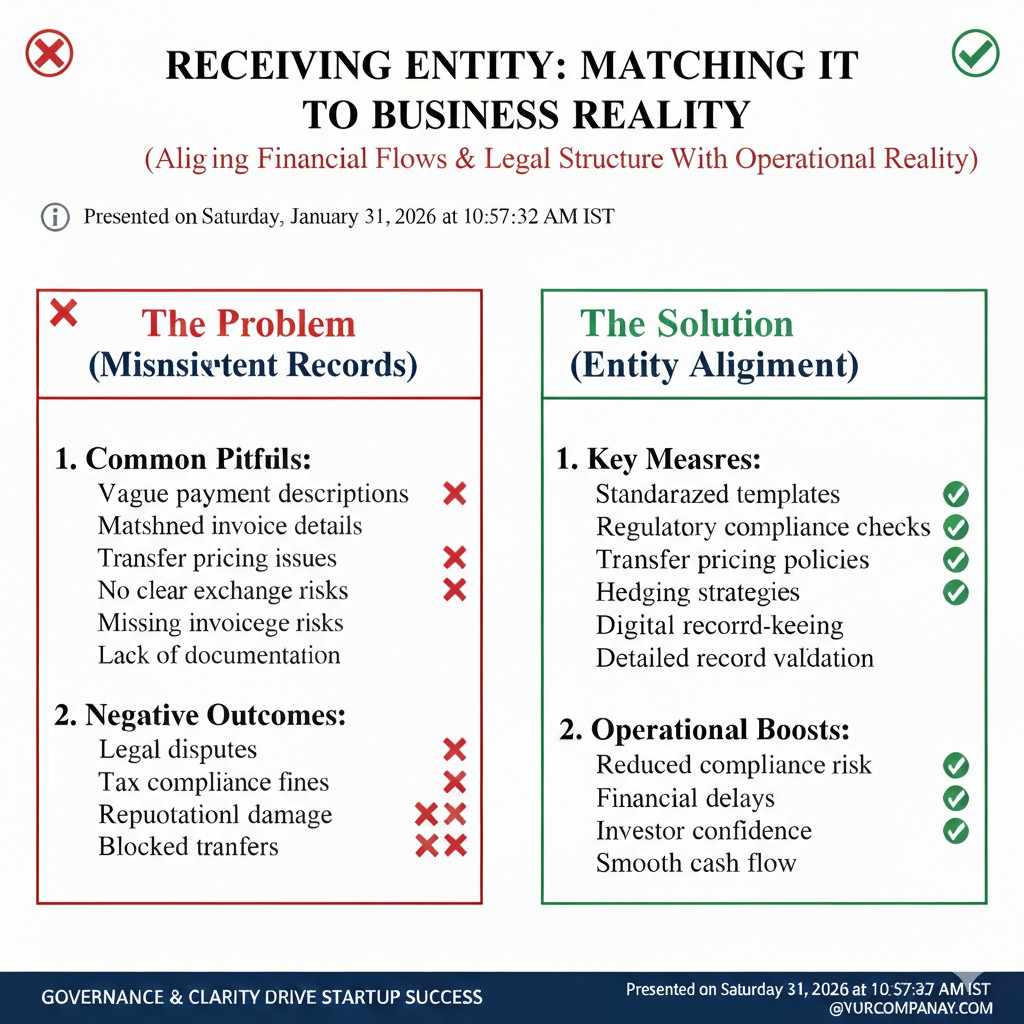

Make the receiving entity match the business reality

If your U.S. company sells to customers, customer payments should usually go to the U.S. company. If your India entity is the seller of record, then payments should go there. Problems begin when the money lands in an entity that is not the one providing the service or holding the contract.

This is not only about banking. It links to tax, transfer pricing, and IP ownership. If the wrong entity is paid, you may later need to explain why. Simple structure today saves legal work later.

Bring money in with records ready for audits and fundraising

Even if you are small, act like you will be audited, because one day you will be. A seed investor may not audit you, but their lawyers will still ask for clean trails. A bank may also review past transfers if something triggers a review.

If you want to raise with leverage, you want your money flows to look boring. Boring is good here. Boring means clear documents, stable patterns, and no odd detours through personal accounts.

Sending Money Out Without Creating Trouble

Paying vendors and service providers the clean way

When money leaves your company, the safest path is to treat every payment as if someone will ask about it later. Most payments are normal business expenses, but banks still want to understand them. The clearer your records, the less friction you face.

A proper vendor payment usually starts with a contract or at least a written agreement. It explains what the vendor is doing and how much they are paid. The invoice then matches that agreement. When the money moves, the description in the bank transfer should match both. When all three line up, the payment feels routine to the bank.

Problems start when founders rush. A vendor asks to be paid quickly, and the founder wires money with a vague note. Later, when the bank asks for proof, the founder scrambles to recreate documents. That scramble is what creates delays and stress, not the payment itself.

Contractors, advisors, and overseas talent

Many startups rely on global talent. This is common and accepted, but it needs structure. If you pay an individual overseas, you should have a clear agreement that states the scope of work and payment terms. This is not about legal perfection. It is about clarity.

Banks and tax teams often want to know whether the person is an employee or a contractor. They may also want to know if taxes were withheld locally. If your documents are vague, they may pause payments until they understand the setup.

For technical founders, this is also where IP risk shows up. If a contractor builds part of your core system, your agreement should clearly state that the company owns the work. This is not just an IP issue. It also supports the logic of why the company paid for that work in the first place.

Intercompany payments and shared costs

If you have more than one entity, money often moves between them. One company may pay salaries. Another may own the product. A third may handle sales. These setups are common, but the money movement between them needs a reason that makes sense.

Shared cost payments should reflect real activity. If one entity uses engineers employed by another, there should be a services agreement. The amount paid should roughly match the work done. It does not need to be perfect, but it needs to be defensible.

Random transfers with no explanation are a red flag later. They raise questions about hidden profit shifts or tax avoidance, even if that was never your intent. Clear agreements reduce those questions.

Repatriating Profits, Founder Pay, and Personal Transfers

The difference between company money and personal money

One of the hardest habits for early founders to build is keeping company money separate from personal needs. In the early days, everything feels informal. You paid for things yourself. You worked without salary. You just want some cash back.

But from a legal and banking view, the company is its own person. When money moves from the company to you, it needs a label that fits reality. That label determines taxes, approvals, and future questions.

Salary, reimbursements, and other common paths

Salary is usually the simplest way to pay founders once the company can afford it. It is regular, documented, and understood by banks. Reimbursements are also normal, but they should match real expenses and include receipts or records.

Where founders get stuck is when they move money without calling it anything. A transfer with no label looks suspicious later. Even if the amount is small, it creates noise in your records.

If you are unsure how to structure founder pay early on, it is better to ask once and set a standard than to fix many small mistakes later.

Dividends and distributions need extra care

Dividends are often misunderstood. They are not just “taking money out.” They usually require profits under local rules, board approvals, and sometimes proof that taxes were handled. For early-stage startups, dividends are rare for a reason.

If you try to repatriate money as dividends too early, you may trigger reviews or tax costs that were avoidable. In most cases, founders are better off using salary or reimbursements until the company is stable and well advised.

Repatriation and Taxes: The Quiet Risk

Why tax teams care about money movement

Every cross-border transfer has a tax angle, even if no tax is due. Tax teams care about where value is created and where money ends up. If the two do not line up, questions follow.

For example, if most development happens in one country but most money flows to another, tax authorities may ask why. They are looking for profit shifting, even if your goal was just convenience.

Transfer pricing in simple terms

Transfer pricing sounds complex, but the idea is basic. When related companies trade with each other, the price should look reasonable, as if they were independent. You do not need perfect math. You need logic that can be explained.

If your India entity provides engineering services to a U.S. parent, the fee should roughly reflect market rates for that work. If the fee is too low or too high, it invites questions. Clear agreements and simple benchmarking help here.

Planning early avoids painful fixes

Founders often delay tax planning because it feels premature. The truth is that early planning is cheaper and easier. Once money has moved for years without structure, fixing it can involve amended filings, penalties, and long explanations.

Even a short conversation early can help you choose paths that scale cleanly. This is part of building with intention, not rushing toward growth without a base.

How Clean Repatriation Supports IP and Fundraising

Investors look at money flow as a trust signal

When investors review a company, they do not just look at product and traction. They look at how the company behaves. Clean money movement tells them the founders are disciplined and aware of risk.

Messy transfers tell a different story. They suggest future clean-up work, hidden liabilities, and delays. Even strong technology can lose value if the structure around it is weak.

IP ownership often follows the money

Who paid for the work often influences who owns the result. If your U.S. company claims to own an invention, but your overseas entity paid for most of the development without clear agreements, that claim can be questioned.

This is why repatriation and ip risk connect. Clean payment records support clean ownership stories. That matters for patents, acquisitions, and future funding.

At Tran.vc, this connection is central to how we help founders. We invest up to $50,000 in in-kind patent and IP services so that your structure, ownership, and records support each other. This helps you raise with leverage and build a moat that lasts. You can apply anytime at https://www.tran.vc/apply-now-form/

A Practical Way to Stay Out of Trouble

Build habits, not heroics

The goal is not perfection. The goal is repeatable habits. Use the same descriptions. Store documents in one place. Decide categories before sending money. These small habits compound into clarity.

When something new comes up, pause and label it correctly. That pause often saves weeks of cleanup later.

Get help before pressure hits

Most repatriation problems surface under pressure. A bank review, a funding round, or a tax notice forces you to explain years of activity at once. That is the worst time to start thinking about structure.

A short review now, while things are calm, gives you options. It lets you fix issues quietly and design flows that support growth.

If you want support building a clean, defensible base—covering IP, structure, and the money paths that tie them together—Tran.vc works hands-on with technical founders at the earliest stage. You do not need hype. You need clarity. Apply anytime here: https://www.tran.vc/apply-now-form/