A SAFE is one of the fastest ways to raise early money in the US. It is short, it feels “standard,” and many founders have seen it close quickly.

But the moment you step outside the US, the SAFE stops being “plug and play.”

If you are building from India, Europe, the UK, the UAE, Singapore, or anywhere else, you can still raise on something people call a SAFE. The real question is: will it work the way you think it will, with your local company, your local tax rules, and your future investors?

This matters because the wrong early paper can slow your next round, create surprise taxes, or force a messy restructure right when you should be shipping product and protecting your edge. If you want to raise fast and still stay clean for the next round, you need to understand what a SAFE is in legal terms, what it is not, and what changes when your company is not US-based.

And as you figure this out, keep one thing in mind: if your startup is doing real AI, robotics, or deep tech, your early leverage is not hype. It is your IP. The strongest early “yes” from serious investors often comes when you can show that your core invention is being protected in a smart way. Tran.vc helps founders do exactly that by investing up to $50,000 in in-kind patent and IP services so you build a moat early, not later. You can apply anytime here: https://www.tran.vc/apply-now-form/

Now let’s get clear on the core issue.

A SAFE is not equity today. It is not debt either. It is a contract that says: “I give you money now, and later I get shares when a priced round happens, based on a discount or a valuation cap.”

That “later” part is where the outside-the-US problems start.

Because in many countries, regulators, tax offices, and even banks do not treat “later shares” the way Silicon Valley does. Some places want you to treat it like a loan. Some treat it like equity right now. Some do not like the idea of a security that has no maturity date. Some require you to set a clear valuation today. Some have rules about who can invest, how you can market the raise, and what filings you must do even for a small check.

So can you raise on a SAFE outside the US?

Yes—sometimes.

But the better way to think about it is this:

You can raise using a SAFE-style agreement if (1) your company structure supports it, (2) your investors will accept it, (3) your local rules do not create hidden pain, and (4) you have a clear plan for how it converts later without drama.

If you do not check those boxes, you can still raise fast—you just may need a different instrument that behaves like a SAFE but fits your country better.

Here is what I want you to take away from this intro before we go deeper:

Raising outside the US is not “SAFE vs not SAFE.” It is “clean future cap table vs messy future cap table.”

If you make the future clean, the money often comes faster.

If you want, I’ll continue into the next section where we break down, in plain words, the exact situations where a SAFE works well outside the US, when it backfires, and what to do instead—without turning this into a legal textbook.

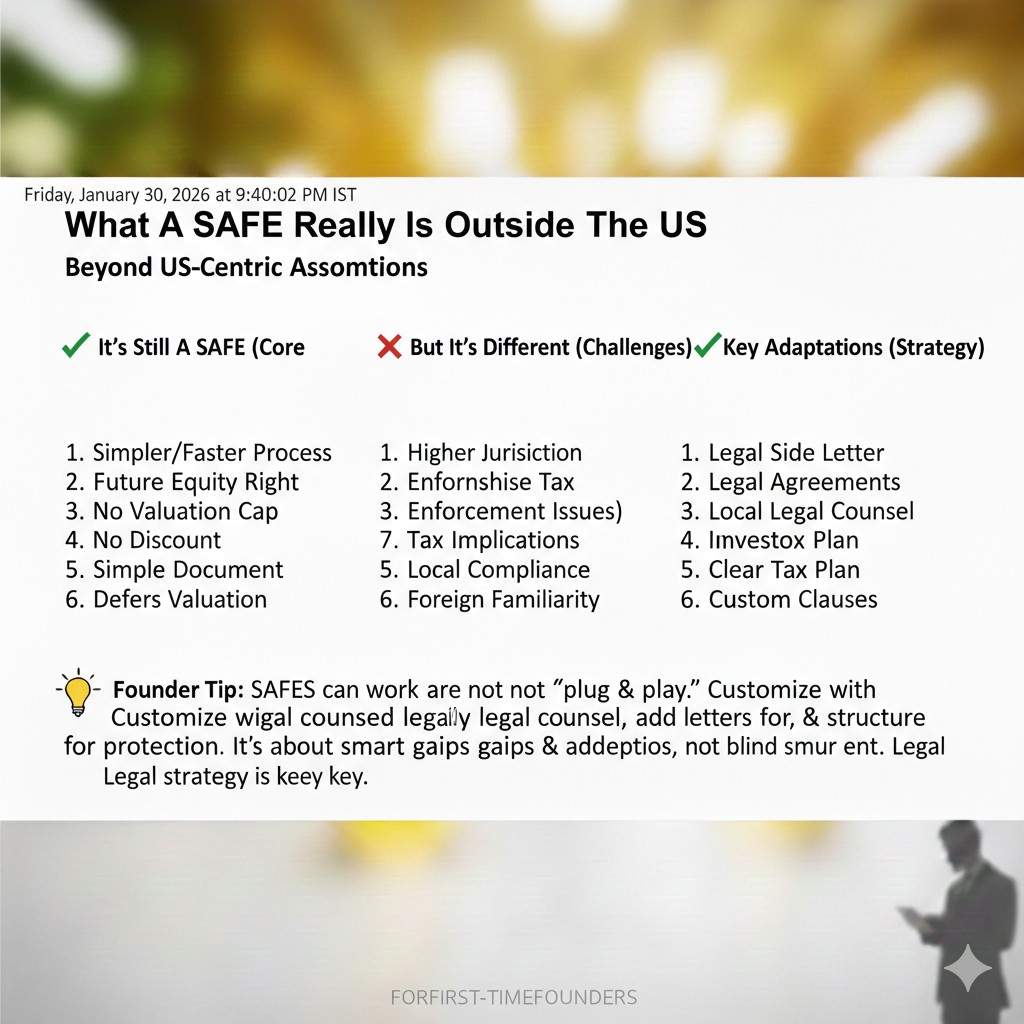

What a SAFE Really Is Outside the US

A SAFE is a promise, not shares today

A SAFE is a contract that sits in between “money now” and “shares later.”

The investor wires funds today, and the company agrees to issue shares later.

Those shares usually come when you raise a priced round, like a Seed or Series A.

That sounds simple, but many countries do not have a common box for this kind of promise.

Some systems want every investment to look like equity right away, with shares issued now.

Other systems want it to look like a loan, with interest, a due date, and repayment terms.

Why US founders say “SAFE” like it is universal

In the US, SAFEs became popular because many investors and lawyers already know how they work.

They also sit inside a bigger system that supports fast private fundraising.

That system includes common startup structures, clear market practice, and a deep pool of repeat investors.

Outside the US, you can still use a SAFE-style deal, but you lose the “everyone knows this” benefit.

That means your speed now depends on how well you explain the instrument and how clean it is later.

If you want fast money, you must make it easy for the investor to say yes.

The key distinction: “What is this instrument treated as in your country?”

This is the core question most founders miss.

It is not only “can I sign a SAFE,” because anyone can sign a document.

It is “how will regulators, tax offices, auditors, and future investors treat this document?”

If the local view is “this is debt,” you may trigger loan rules, interest rules, and repayment questions.

If the local view is “this is equity,” you may need to issue shares now, not later.

If the local view is “this is a security offer,” you may need filings and investor limits.

When a SAFE Works Well Outside the US

It works best when the next priced round is very likely

A SAFE depends on a future priced round to convert cleanly.

If you are already in active talks with seed funds, or you have strong traction, it can work well.

Your investors can see a clear path: today money, tomorrow shares.

It tends to work poorly when the company might stay bootstrapped for a long time.

If there is no priced round for years, investors may get nervous.

In some countries, that “open-ended” timeline can also create legal discomfort.

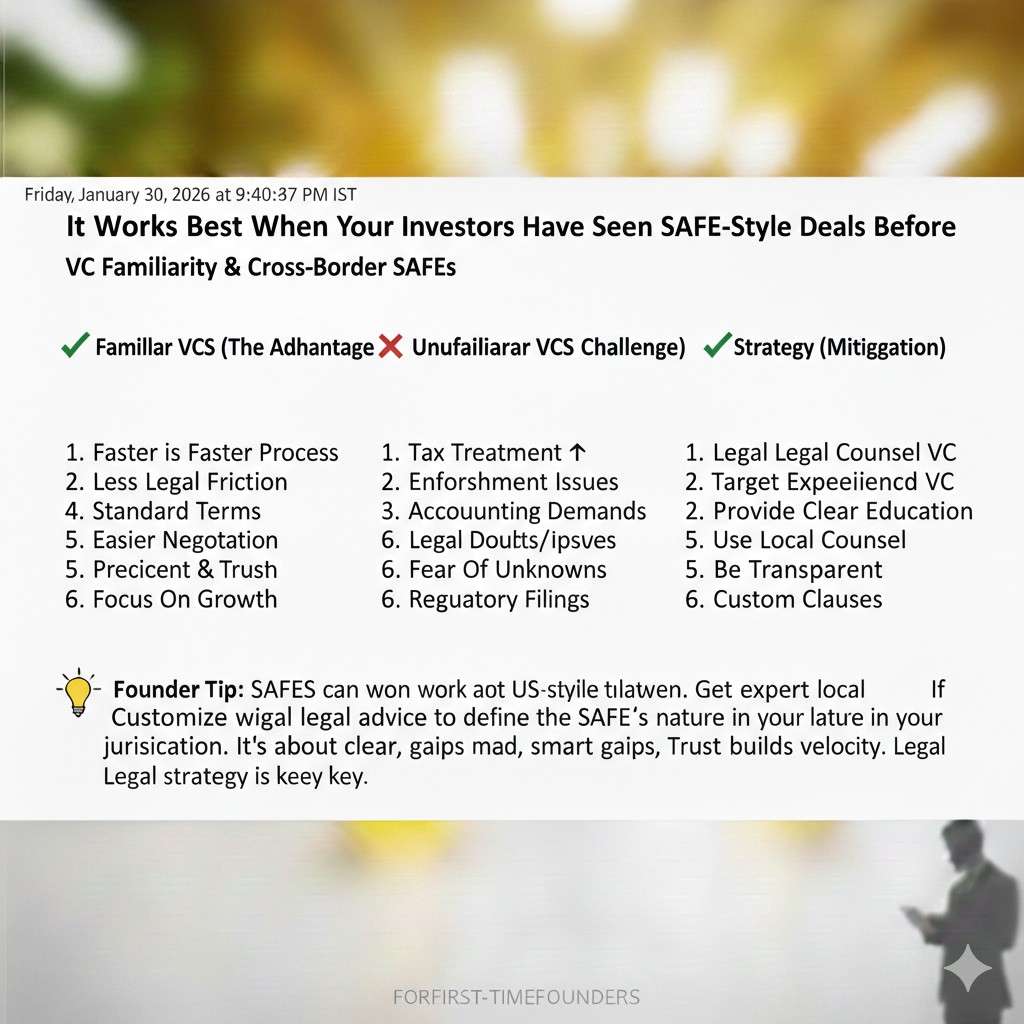

It works best when your investors have seen SAFE-style deals before

A founder raising from global angels, US angels, or funds that invest cross-border will have an easier time.

These investors often accept the concept as long as the conversion terms are fair and clear.

They mainly care about two things: cap table cleanliness and enforceable rights.

If your investors are local and used to “shares now,” a SAFE can create friction.

They may ask, “What do I own today?” or “How do I report this?”

You can still close, but you will spend time teaching instead of building.

It works best when your company structure can issue shares later without chaos

Even if your country allows a SAFE-style promise, your company must be able to convert it later.

That means your charter documents, share classes, and corporate approvals must support conversion.

If conversion requires special approvals each time, it turns into a slow process at the worst moment.

Many founders only discover this problem when a priced round is already moving.

Then the new lead investor asks for proof that every SAFE converts cleanly.

If you cannot show that, the round slows down or the terms get worse.

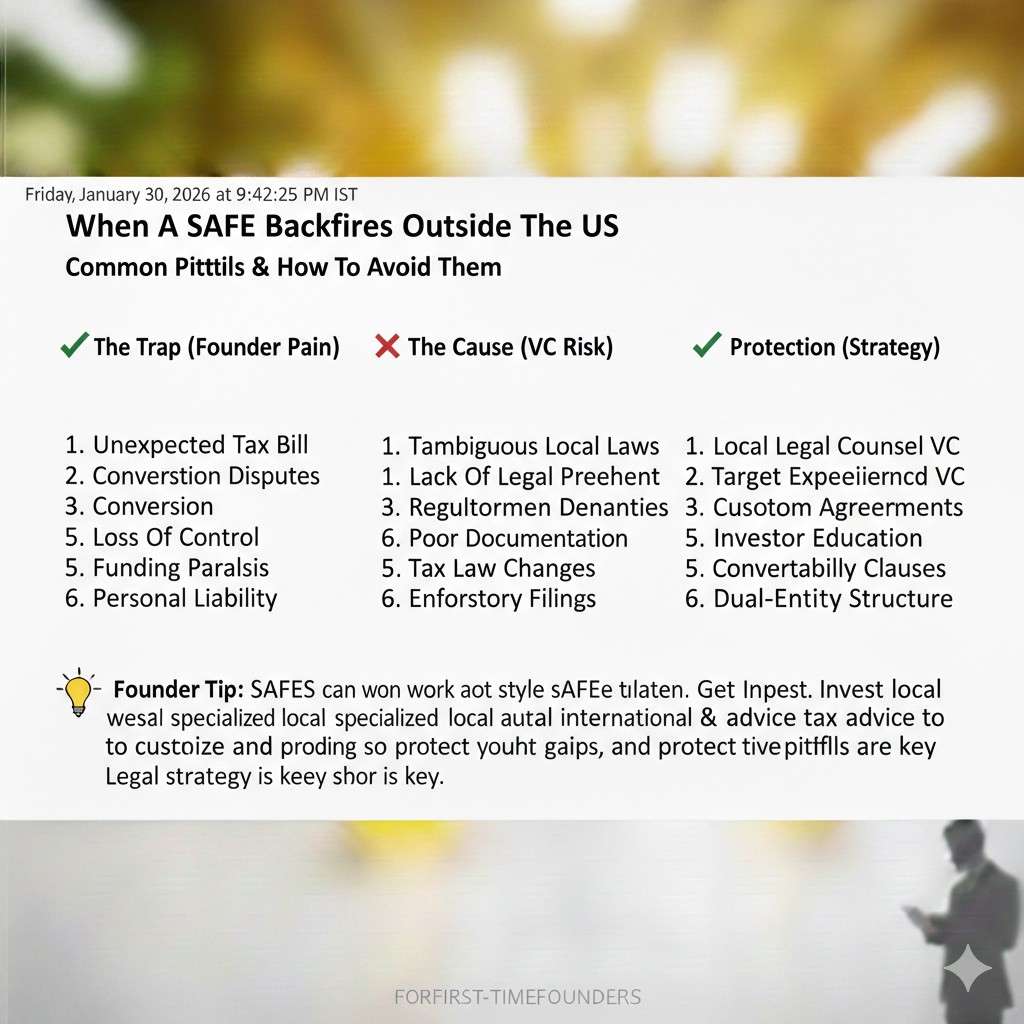

When a SAFE Backfires Outside the US

The “paper is signed” trap

A common mistake is thinking the job is done once the document is signed and the money lands.

In reality, early paper is judged later, when serious money comes in.

Your Seed lead or Series A lead will read everything you signed.

If they see unclear conversion terms, missing local compliance, or strange side letters, they worry.

Investors do not like surprises because surprises turn into legal risk.

And legal risk can become price cuts, delays, or demands that you restructure before they fund.

The “local tax surprise” trap

In some places, a SAFE-style instrument can trigger tax confusion.

For example, if it is treated like debt, questions can come up about “imputed interest.”

If it is treated like equity, questions can come up about valuation and when value is recognized.

You do not need to become a tax expert, but you must respect that taxes follow classification.

A document that looks simple can create messy tax reporting for both the company and the investor.

That mess can scare off the very investors you want to attract next.

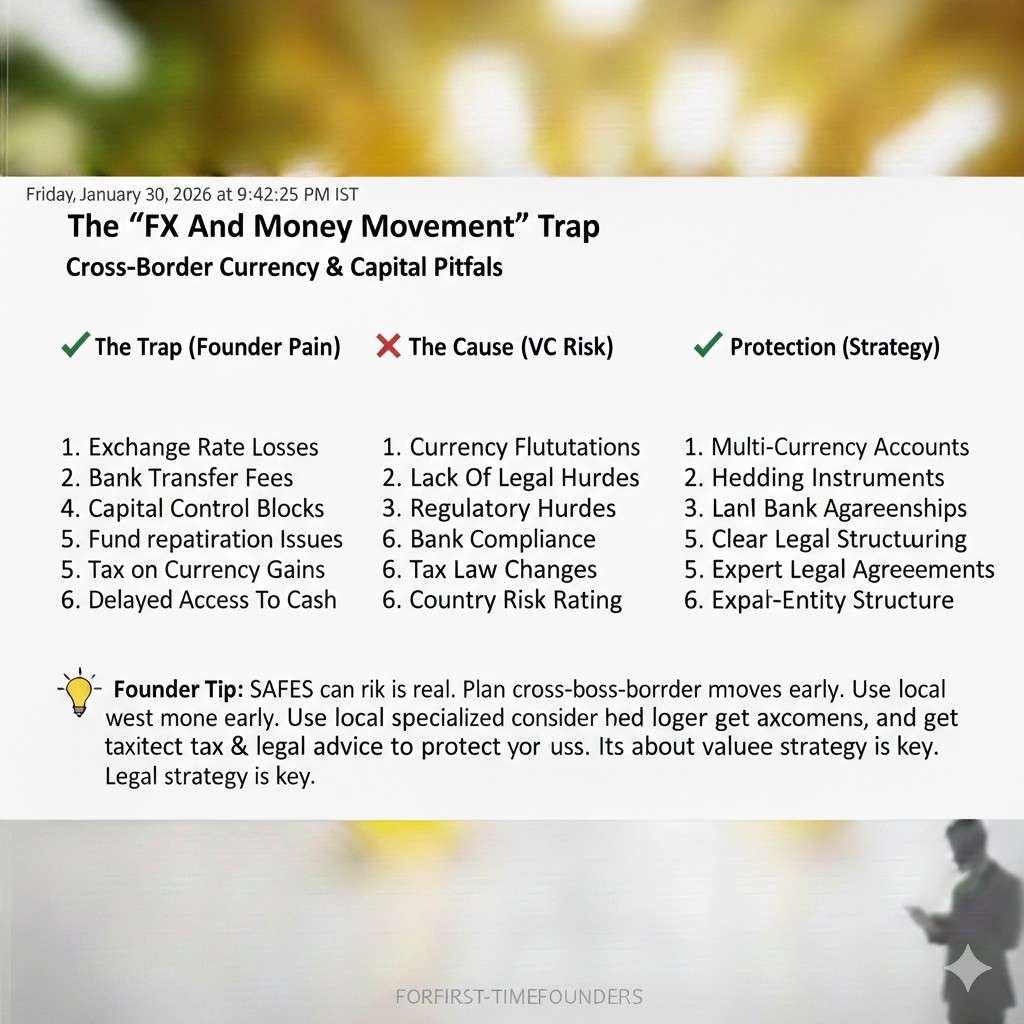

The “FX and money movement” trap

Cross-border raises often create extra steps around banking, reporting, and money movement.

Even when everything is legal, it can still take longer than a founder expects.

A SAFE does not remove these steps, because those steps sit outside the contract.

If you plan to raise from outside your home country, you should plan the path of funds early.

Know where the money lands, what approvals you need, and what records you must keep.

This is not glamorous work, but it protects you from last-minute panic.

The Most Important Distinction: Local Company vs US Holding Company

A local operating company can raise, but the investor base may be smaller

If you are incorporated in your home country, you can often raise from local angels and funds.

Some will accept SAFE-like instruments, but many will prefer local standard notes or equity.

The investor base you can access depends a lot on what your market is used to.

If your long-term plan is to raise from top-tier global funds, they may prefer a US parent company.

That does not mean you must do it now, but you should understand the path.

Your early fundraising choice should not block your future fundraising choice.

A US parent can make SAFE fundraising easier, but it is not “free”

A Delaware C-Corp is familiar to many global investors.

US SAFEs are designed for that world, which makes legal review faster for many investors.

That speed can be real, especially when you are raising from US angels or US seed funds.

But creating a US parent company can add ongoing work and cost.

You may have two entities, two sets of filings, and more accounting complexity.

You also must handle the relationship between the US parent and the local operating company carefully.

A practical way to think about it

If your next investors are likely US-based, a US-friendly structure can reduce friction.

If your early capital is local and your operations are local, a local structure can be fine.

The best answer is the one that keeps your next round simple, not the one that sounds trendy.

This is also where IP strategy becomes a real lever.

When your patents and core invention story are strong, investors tolerate more structure complexity.

Tran.vc helps founders build that strength early with up to $50,000 in in-kind patent and IP services. Apply anytime here: https://www.tran.vc/apply-now-form/

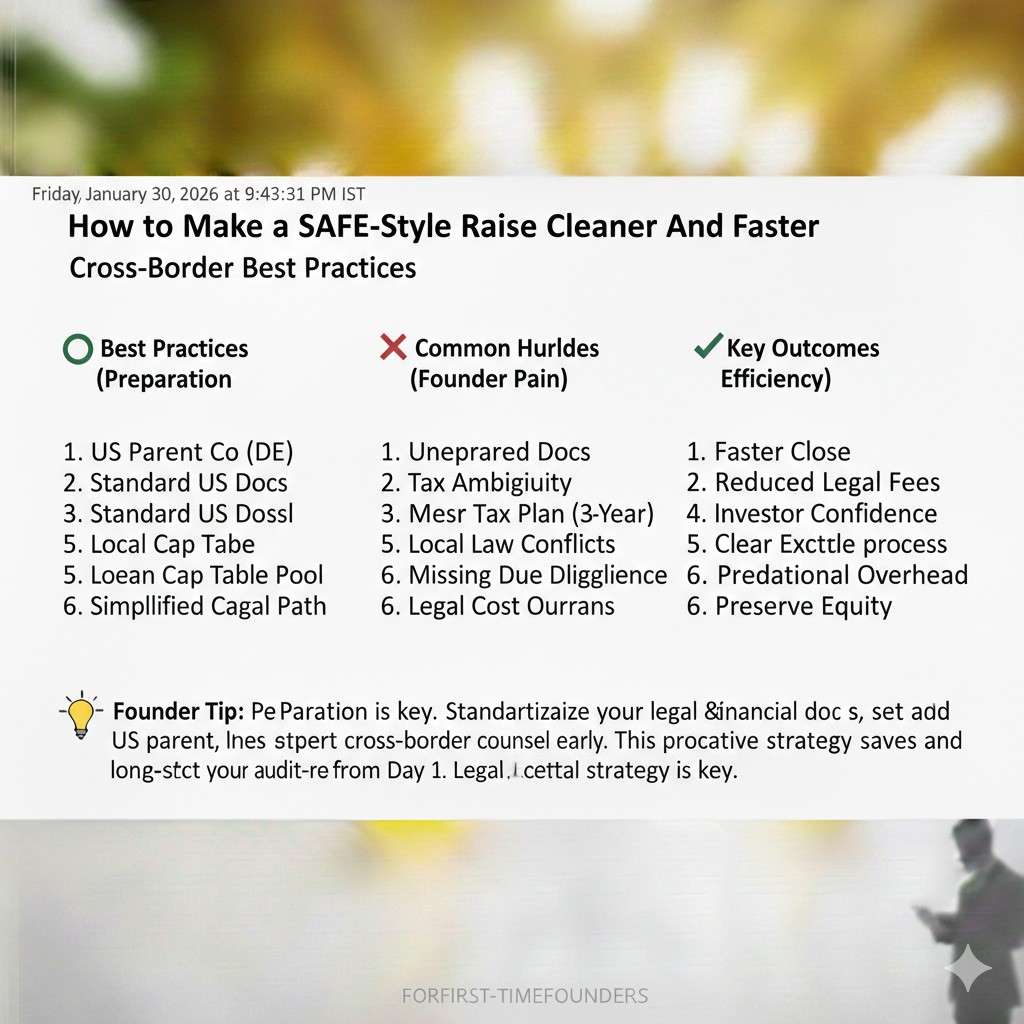

How to Make a SAFE-Style Raise Cleaner and Faster

Start by writing down your “conversion story” in plain words

Before you send any document, write one short explanation for yourself:

“When will this convert, into what shares, at what price logic, and what happens if we never raise?”

If you cannot explain it simply, the investor will not feel safe signing it.

If you can explain it simply, the document becomes a formality instead of a negotiation.

Clarity is speed in early fundraising.

Use terms that future investors will accept

Future leads care deeply about valuation caps, discounts, and most-favored terms.

They also care about whether too much money came in on too generous caps.

If your early cap is very low, you may lock in painful dilution later.

This is not about trying to “win” against your early angels.

It is about staying fair to them while keeping the company fundable later.

If you want to raise with leverage, your early terms must be reasonable and easy to defend.

Keep your early IP story tight, because it reduces negotiation

When a startup has no moat story, investors push harder on price and control.

When the startup can show real defensibility, investors often relax on terms.

That is why early IP work is not paperwork, it is fundraising support.

If your product is based on core algorithms, robotics designs, or unique training methods, protect it early.

It makes your SAFE conversation simpler because the investor sees substance behind the pitch.

Tran.vc is built for this stage, and you can apply anytime here: https://www.tran.vc/apply-now-form/