If you are building a startup, you will hear the word “vesting” very early. It often comes up right when things feel exciting—when you are forming the company, picking co-founders, and talking to your first investors. Then the mood shifts a bit, because vesting can feel personal. It touches ownership. It touches trust. It touches the fear of “What if someone leaves?”

Cliff vesting is one of those terms that sounds cold, but it exists for a simple reason: startups change fast, and people’s lives change too. Investors expect cliff vesting because they want the company to survive the hard parts. And they want to know the founding team is truly committed, not just present on day one.

In this article, I’ll explain cliff vesting in plain words, why investors push for it, what it protects, and how to set it up in a way that feels fair—especially if you are a technical founder building real tech like AI or robotics, where the work is deep and the timeline is long. I’ll also show you how to talk about it with co-founders without blowing up the relationship, and how to avoid common vesting mistakes that can quietly kill a funding round.

Before we go further: if you’re a founder building AI, robotics, or other hard tech, and you want help turning what you are building into strong patents and a real moat, Tran.vc can support you with up to $50,000 in in-kind IP and patent services. You can apply anytime here: https://www.tran.vc/apply-now-form/

Cliff Vesting: Why Investors Expect It

What cliff vesting means in simple words

Vesting is the rule that decides when you truly “earn” your shares over time. You may be a founder on paper from day one, but vesting says you only keep all your founder shares if you stay and keep doing the work long enough. This is not meant to punish anyone. It is meant to match ownership with real time and real effort.

A “cliff” is the first big checkpoint in that vesting schedule. The most common cliff is one year. That means if a founder leaves before one full year, they usually earn none of the shares that were set aside to vest. After that one-year mark, a chunk becomes earned, and the rest is earned bit by bit each month after.

Think of the cliff like a “prove it” period that protects the company from early breakups. Startups are stressful. Co-founder relationships are intense. Investors know this. The cliff exists because day-one optimism is not the same as day-365 commitment.

The simple math behind the most common setup

The most common setup is “four years with a one-year cliff.” In plain terms, that means a founder earns their shares over four years, but nothing is earned until the first year is completed. At the one-year mark, a large slice is earned at once, often 25%. After that, the remaining 75% is earned gradually, often monthly, over the next three years.

This structure is popular because it creates a fair balance. It gives founders enough time to show real commitment. It also gives the company protection if someone leaves very early, before they have made a lasting contribution.

Even when founders feel confident they will stay, investors still want the structure in place. They are not judging your character. They are managing risk, because risk is their job.

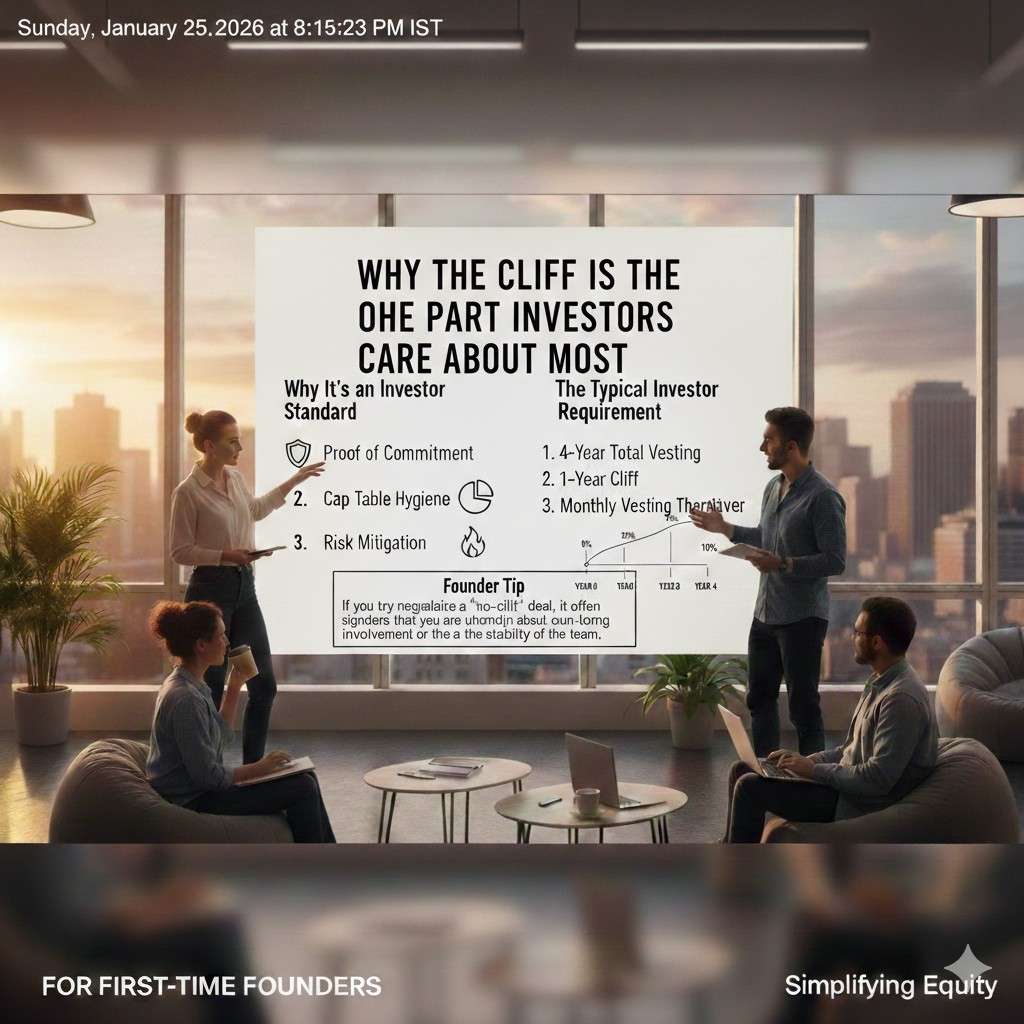

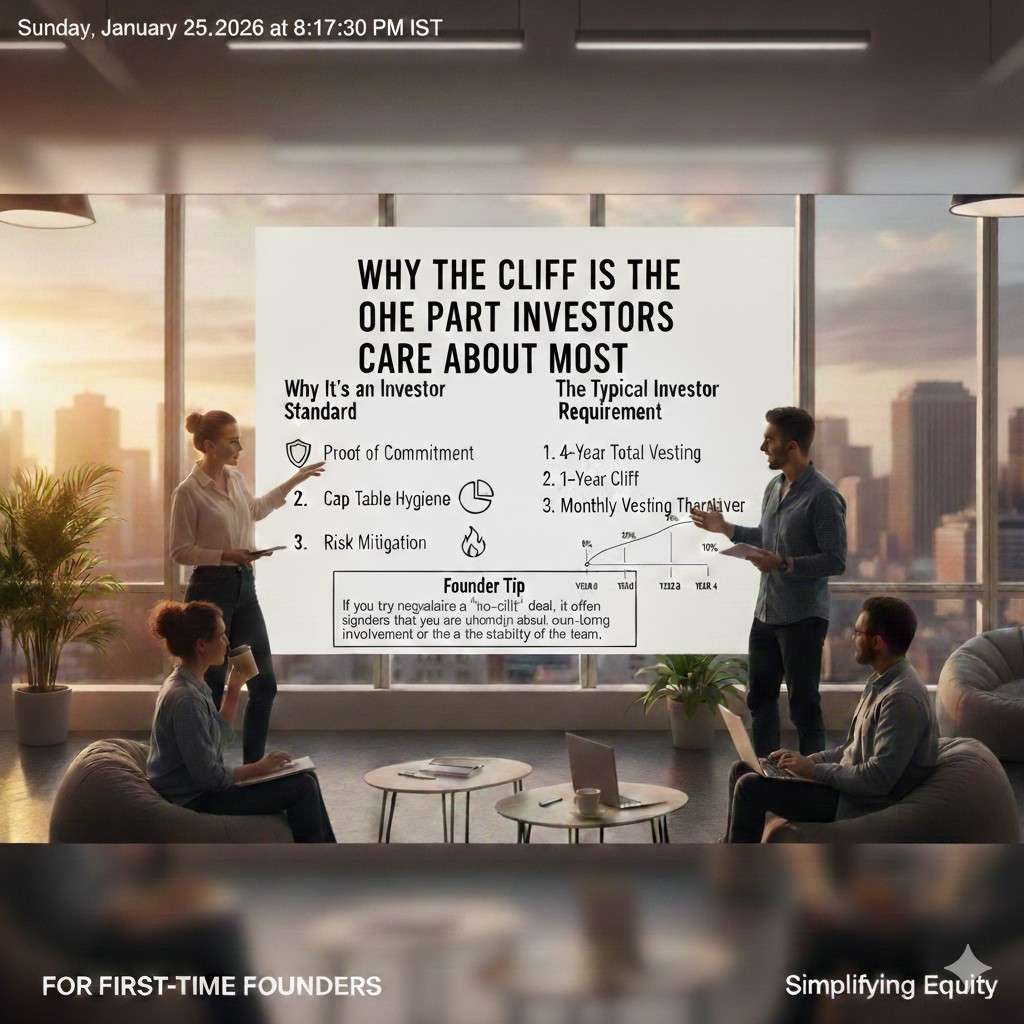

Why the cliff is the part investors care about most

Vesting without a cliff still gives some shares to someone who leaves quickly. Investors do not like that, because those shares are hard to recover. If an early co-founder walks away after three months with a meaningful stake, the company carries that weight forever. It can scare off new hires and future investors because too much ownership is tied up with someone no longer building.

The cliff is a clean line that avoids messy debates about “how much was done” in a short time. It prevents the company from being stuck with a cap table that feels unfair to the people who stayed and carried the hard work.

When investors say they “expect a cliff,” they are really saying they expect a company to be able to survive founder changes without falling apart. This is less about control and more about long-term stability.

What cliff vesting is not

Cliff vesting is not an investor trick to take founder equity. The shares are still yours if you stay and do the work. The cliff only matters if someone leaves before that first checkpoint. If everyone stays, the cliff is almost invisible. It is just a line in legal paperwork that never becomes an issue.

It is also not a sign that investors distrust you personally. Most serious investors ask for the same thing across almost every early-stage deal. They have seen many companies fail due to team splits. They try to reduce that risk early because later is too late.

If you treat cliff vesting like a normal seatbelt, it becomes easier to accept. You hope you never need it. But you are glad it is there when something unexpected happens.

Where cliff vesting shows up in a real startup life

In the real world, cliff vesting comes up in three moments. The first is at company formation, when founders divide equity. The second is when you bring in your first serious investor, who wants to confirm the equity is properly set up. The third is when you hire early employees and they ask, “Do the founders vest too?”

These moments matter because they set the tone for trust and fairness. If your early team sees founders with fully owned equity, but employees must vest, that can create resentment. Investors notice this too. They want to see one standard that applies to everyone, even if the details vary by role.

For deep tech startups, where progress can take longer than in simple software, vesting also signals patience. It tells investors the founders are in it for the long run, not just a quick sprint.

Why investors expect cliff vesting at the seed stage

Seed investors are not buying today’s results. They are buying the next two to five years of execution. They want to fund a team that will still be present when the company hits its hardest problems. Cliff vesting is one of the clearest signals that the team is locked in for that journey.

At seed, the company is fragile. The product can change. The market can change. The team must adapt quickly. If a key founder leaves early, the company can collapse. Investors protect against that by making sure the equity structure supports staying power.

This is especially true in AI and robotics, where a key technical founder is not easily replaced. If the person who understands the model, data pipeline, hardware design, or core algorithm walks away, progress can stop. Investors know that risk is real, so they insist on guardrails.

How cliff vesting protects the company, not just investors

It is easy to think cliff vesting is mainly for investors. In practice, it protects founders who stay. If you and a co-founder start together and that person leaves early, cliff vesting stops them from owning a large piece of your future work. Without it, you may spend years building value while a former teammate benefits without contributing.

It also protects your hiring plan. Early hires often take lower pay in exchange for equity. If too much equity is stuck with an early leaver, you may not have enough left to attract great people later. That hurts the company, and it hurts every founder who remains.

Cliff vesting also protects morale. When everyone knows equity is earned through time and effort, trust is easier to keep. People feel the system is fair, even when outcomes are tough.

What happens when you do not have a cliff

When there is no cliff, you create a hidden problem that may not show up until you try to raise money. Investors will look at your cap table and ask hard questions. They may slow down the deal, ask you to renegotiate equity, or require legal fixes that cost time and money.

If a founder already left and owns meaningful shares outright, you may not be able to “fix” it easily. That person may not want to give anything back. Even if they are reasonable, renegotiating can turn emotional and ugly. It can also create legal risk if handled poorly.

In the worst case, a missing cliff can block the round. Investors do not want to step into a situation where ownership is misaligned. They would rather pass than inherit a cap table that can cause conflict later.

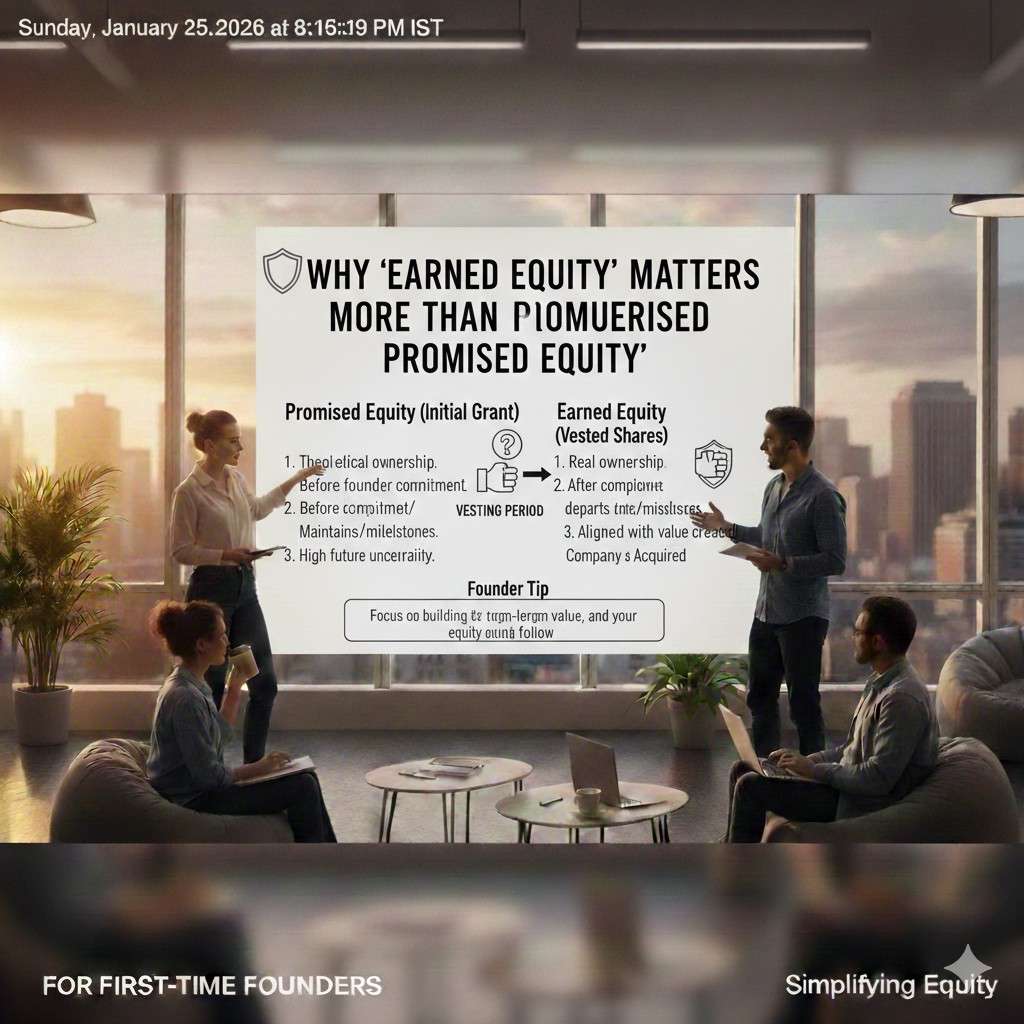

Why “earned equity” matters more than “promised equity”

In a startup, equity is not just a reward. It is a tool. It pulls people through hard weeks, missed deadlines, product pivots, and stress that outsiders do not see. If equity is given fully upfront, it stops being a tool. It becomes a sunk cost the company carries, even if the person is gone.

Investors want equity to stay connected to contribution. Vesting does that in a clear, measurable way. It does not depend on opinions about who did what. It depends on time served and continued involvement.

For founders, this is also a healthy mindset. It shifts the question from “What do I deserve?” to “What will I build over the next few years?” That is the mindset that creates strong companies.

How to talk about cliff vesting with co-founders without damaging trust

The best time to talk about vesting is before you split equity, not after. If you wait until someone feels ownership is “final,” the conversation becomes tense. If you bring it up early as a normal part of building a fair company, it feels less personal.

The way you frame it matters. You can say, “We are doing this because we respect each other and want to protect the company if life changes.” That feels different from “We need this in case you quit.” Use language that focuses on mutual protection, not suspicion.

Also be honest that investors will ask for it anyway. That truth can reduce emotional pushback. It is easier to accept something when it is part of the standard startup playbook, not a special rule one founder invented.

The common cliff length and why one year became standard

One year became standard because it is long enough to see real commitment, but not so long that it feels like punishment. In many startups, the first year includes the hardest identity work: choosing the market, building the first version, talking to users, finding early traction, and learning how you work together under pressure.

If someone leaves before one year, it often means the match was not right. The cliff ensures the company can recover and move forward without giving away permanent ownership too early.

That said, “standard” does not mean “perfect for everyone.” Some deep tech teams choose slightly different terms based on the timeline of the work. But one year is the default because it has worked well across many situations.

How vesting terms connect to fundraising readiness

Investors often view vesting as a sign of maturity. It shows you are building for the long term, not just hacking something together. It also signals you have gotten real legal and business guidance, which reduces the chance of messy surprises later.

If your vesting is clean, investors move faster. Your due diligence feels lighter. Your term sheet negotiations have fewer bumps. That can matter a lot when you are trying to close a round and keep momentum.

This is one reason Tran.vc focuses so much on strong foundations. For technical founders, strong foundations are not only code and prototypes. They are also ownership, IP, and the legal structure that makes future funding smoother. If you want help building that kind of foundation, you can apply anytime here: https://www.tran.vc/apply-now-form/

Cliff Vesting: Why Investors Expect It

The investor’s real fear: “dead equity” that blocks the company

When investors look at your cap table, they are not only asking, “Who owns what today?” They are asking, “Will this ownership still make sense two years from now?” The biggest problem they worry about is dead equity. That is equity held by someone who is no longer working on the company, but still owns a meaningful slice.

Dead equity creates quiet damage. It reduces the share pool you can use to hire strong people. It can make future rounds harder because new investors want enough room for themselves, and they want the team still building to stay motivated. If too much is locked with someone who left, everyone else gets squeezed.

Cliff vesting is the simplest way to prevent dead equity from being created in the first place. Investors expect it because they have seen what happens when it is missing, and they do not want to fund a problem that could have been avoided with one clean clause.

Why early-stage investing is mostly “team risk,” not product risk

At seed, many startups do not have stable revenue. Some do not even have a finished product. Even if you have a prototype, it may change. So investors spend a lot of time thinking about team risk. Team risk means the company may fail because the people building it cannot stay aligned, cannot keep going, or cannot handle the stress.

Cliff vesting is one of the few tools that reduces team risk without slowing the company down. It does not change what you build. It changes incentives and outcomes if someone leaves.

This is why investors bring it up so early. They are not trying to distract you. They are trying to remove one of the most common causes of early startup failure: the founding team breaking apart and leaving the company with a broken ownership structure.

The hidden rule investors follow: “equity must match effort”

Many founders think equity is a reward for being first. Investors think equity is payment for future work. Both ideas matter, but investors prioritize the second. They want the people doing the next hard years to hold the largest share of the upside.

This is not about being harsh. It is about building a company where incentives stay aligned. If someone leaves early but keeps a big stake, the people still working feel cheated. That can lead to burnout and conflict, which can kill execution. Investors want to avoid that chain reaction.

Cliff vesting supports the idea that ownership is earned. That idea makes the company easier to lead, easier to hire for, and easier to fund again.

How cliff vesting protects the next investor, not just the first one

It is easy to focus on the seed investor sitting in front of you. But investors think ahead. They know you will need more money later. They know other investors will look at your cap table and ask, “Is this healthy?” If it is not healthy, they may offer worse terms or walk away.

So when an early investor asks for cliff vesting, they are also trying to protect your Series A path. They want your future fundraise to be smoother. They want the next investor to feel confident that the team is still intact and properly motivated.

A clean vesting setup is like clean accounting. You may not care on day one, but later it becomes a big reason deals move fast or slow.

What investors expect to see in a “normal” founder vesting setup

In many seed deals, investors expect founders to be on a four-year vesting plan with a one-year cliff. They often expect it to start either at company formation or at the financing event, depending on what happened before. They also expect acceleration terms to be handled carefully, because acceleration can change the incentive structure in ways people do not see at first.

Founders sometimes ask, “But I already worked on this for a year before we formed the company.” That may be true. Investors can respect that, but they still want clarity. If you have a long pre-company build phase, there are ways to reflect that in a fair way, but the structure still needs to be clean and understandable.

If you are unsure, this is the place where good legal guidance matters. You do not want to “wing it” because small wording differences can have big outcomes later.

The cliff is also a test of co-founder fit

Founders often avoid talking about hard topics early. Vesting forces the conversation. It makes you discuss commitment, roles, time, and what happens if life changes. That feels uncomfortable, but it is healthy.

If a co-founder strongly refuses any vesting, that is a signal to pay attention to. It does not always mean they are bad. It may mean they feel insecure, or they have been burned before. But it can also mean they want upside without full commitment.

Cliff vesting is one of the cleanest ways to create real alignment. It is not only about protecting the company if someone leaves. It is also about setting a standard of fairness for everyone who joins later.

How cliff vesting interacts with roles: CEO, CTO, and “part-time founders”

Investors care about who is full-time and who is not. If one founder is all-in and another is part-time, but both own the same shares with no vesting, that is a problem. Even if you are friends, the imbalance can build resentment.

Cliff vesting creates a baseline that makes these differences easier to handle. If someone is part-time now but plans to go full-time later, vesting can be structured to match that path. The key is to be honest. Investors do not like fuzzy promises. They like clear timelines and clear responsibilities.

In AI and robotics, this comes up a lot. You may have a technical founder finishing a PhD, or someone who is still employed while building the first version. Investors can work with this, but they will want the vesting terms to reflect the reality. Cliff vesting is one way to keep the company safe while the team transitions.

The IP angle: why investors link vesting to invention and patents

For deep tech startups, the core value is often intellectual property. That can mean novel algorithms, unique model training methods, special hardware designs, control systems, edge deployment techniques, sensor fusion stacks, or proprietary data pipelines. Investors care not only that the tech is good, but also that the company truly owns it.

This is where vesting and IP can touch each other in subtle ways. If a founder leaves early, investors want to know the company still has rights to the inventions that founder created. If those rights are unclear, the company can lose its most valuable assets.

Cliff vesting does not automatically solve IP ownership. But it often comes together with agreements that do: invention assignment, confidentiality, and proper patent filing strategy. Investors expect these to be clean because a single missing signature can create a big legal hole.

This is exactly why Tran.vc exists. Many technical teams build something real, but they do not lock down the IP early. Tran.vc supports founders with up to $50,000 in in-kind IP and patent services so your inventions become company assets that investors respect. If you want that support, you can apply anytime here: https://www.tran.vc/apply-now-form/