Founder agreements can feel like a “we’ll clean it up later” problem.

You and your co-founder are building fast. You trust each other. You just need something signed so you can open a bank account, talk to customers, and get the product moving.

And yet, this is exactly where many startups quietly break.

Not because the founders were bad people. But because the agreement they signed had small legal gaps that later turned into big, expensive fights. The kind that kill momentum, scare off investors, and make good teams split up.

This article is about those gaps.

When people hear “legal red flags,” they often think of dramatic stuff: someone stealing code, someone committing fraud, someone doing something clearly wrong. In real founder disputes, it’s usually not that. It’s ordinary things that were never written down clearly:

Who owns the work you built before you incorporated?

What happens if one founder stops working but keeps their shares?

Who can sign contracts?

What if the company gets sued?

What if you disagree on the roadmap?

What if one founder wants to leave, but still wants access to the customer list?

Those questions sound simple. The problem is that many founder agreements answer them in vague ways. Or they don’t answer them at all. And when the company gets real—money, customers, traction, attention—vague turns into conflict.

At Tran.vc, we work with technical founders building AI, robotics, and other hard tech. These teams often move faster than their paperwork. That’s normal. But if your founder agreement has the wrong structure, it can also put your patents, your future funding, and even your ability to sell the company at risk.

So as you read, here’s the mindset that helps: your founder agreement is not about “trusting less.” It’s about protecting the friendship, protecting the company, and protecting the work you’re putting years of your life into.

If you want Tran.vc to review your founder setup through the lens of IP and fundability, you can apply anytime here: https://www.tran.vc/apply-now-form/

Common Legal Red Flags in Founder Agreements

Why this matters more than most founders think

Founder agreements sit in the background when things feel calm. But they become the main story when the company starts to win. The first customer, the first hire, the first investor call, the first big contract—these moments bring pressure. Under pressure, unclear terms turn into blame, and blame turns into gridlock.

A founder agreement is really a “decision map.” It tells you what happens when someone leaves, when someone slows down, when money comes in, when the company gets sued, or when two smart people see the future in different ways. If the map is missing roads, you do not feel it on day one. You feel it when you cannot afford confusion.

If you want help checking whether your founder setup is clean for patents and future funding, you can apply anytime at https://www.tran.vc/apply-now-form/

A quick note on what “red flag” means here

A red flag is not always “illegal.” Many red flags are simply weak language, missing terms, or default templates that do not match how startups actually work. They become dangerous when they collide with real life, like burnout, family emergencies, job changes, or a big pivot.

Also, a red flag often shows up as a small line that seems harmless. One phrase can change who owns the code, who controls the company, or who gets paid first. That is why founders should read agreements slowly, like they are reading a contract that decides their next five years. Because it does.

Ownership and Equity Red Flags

Splitting equity evenly without linking it to time and work

Many teams split equity 50/50 because it feels fair. It feels like trust. It feels like a clean start. But legal fairness is not the same as business safety. A clean split can become a trap if one founder later carries most of the load.

The real issue is not the number. The issue is whether equity is earned over time, based on continued effort. If equity is granted upfront with no “earn-in” structure, someone can stop working and still own a huge part of the company. That can make it hard to raise money, hard to hire leaders, and hard to keep morale.

A safer approach is to tie equity to continued service. This is not punishment. It is a basic rule that keeps the company aligned with reality. Investors expect this. Strong teams expect this. It protects both founders because it creates a shared standard that is not personal.

Missing or weak vesting terms

Vesting is a simple idea: you earn your shares by staying and working. But founder agreements often mess this up in two ways. The first is leaving vesting out completely. The second is adding vesting language that is vague or easy to work around.

If vesting is missing, the company can get stuck. Imagine a founder leaves in month six, takes 30% or 50%, and then becomes unreachable. Even if everyone stays polite, the cap table is now heavy. Future hires see fewer options. Investors see risk. Acquirers see problems.

If vesting is weak, you can face the same outcome. The agreement might say shares “vest monthly,” but it might not say what happens on departure. Or it might not give the company a clear right to buy back unvested shares. In practice, weak vesting is often the same as no vesting.

Good vesting language is specific. It explains timelines, cliff periods, what happens if someone leaves, and what the company can do to reclaim unearned equity. It also aligns with local law and your company structure, because sloppy wording can be hard to enforce.

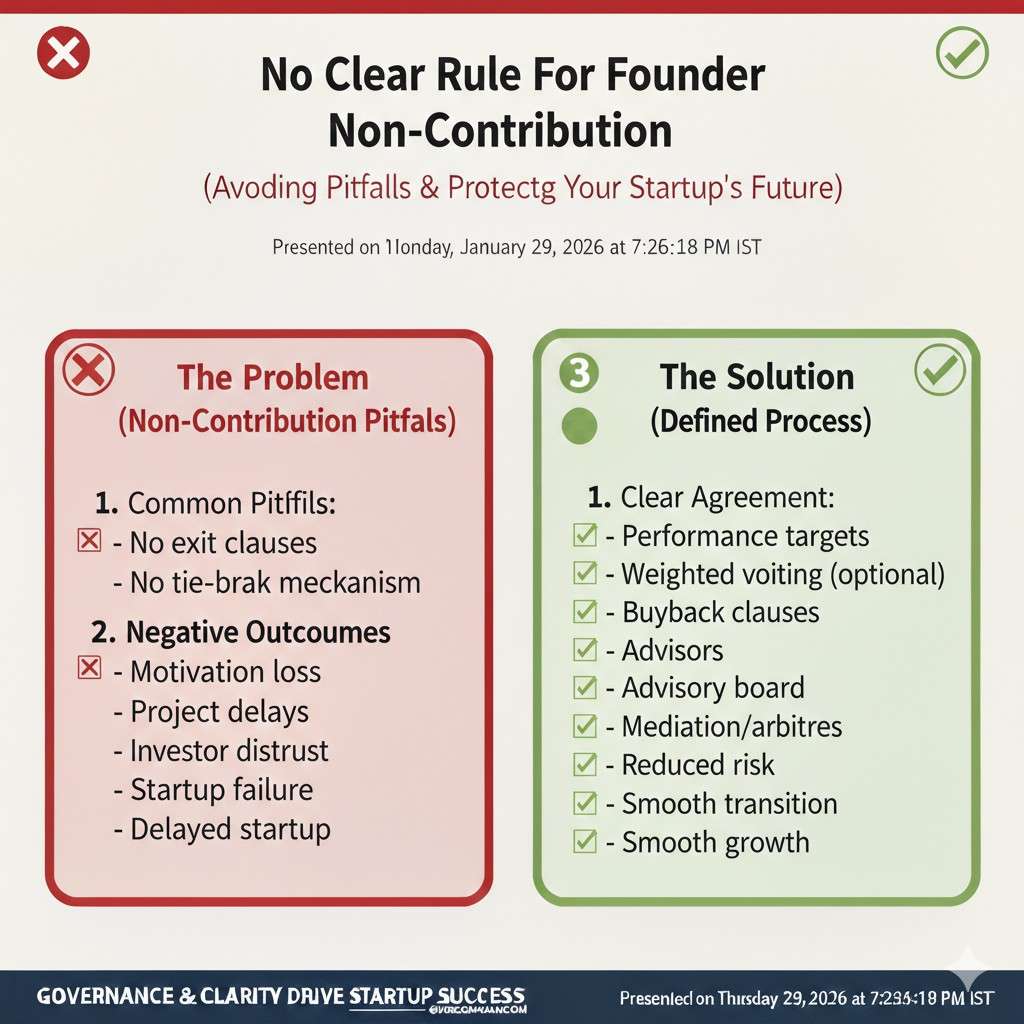

No clear rule for what happens if a founder stops contributing

This is one of the most common silent failures. A founder may not “quit,” but they also may not deliver. They might take another job, step back for months, or stop showing up to key meetings. The company keeps moving, but resentment builds.

A strong founder agreement should define expectations in a realistic way. Not as strict “hours,” but as duties, time commitment, and decision responsibility. It should also outline a process: what counts as stepping away, how it is documented, and what the consequences are.

Without that clarity, the team ends up negotiating in the middle of stress. That is the worst time to negotiate. People feel attacked. The conversation becomes emotional. The company loses speed. Legal rules should reduce drama, not create it.

Using informal promises instead of written terms

Founders often say, “If anything changes, we’ll talk.” That feels mature, but it is not a system. When money and control are on the table, memory becomes selective. People remember conversations differently, especially if their personal situation changes.

A founder agreement is where you lock in the key promises. This includes equity, roles, authority, and what happens during conflict. It also includes how major decisions are made and how deadlocks get resolved.

Writing things down is not about distrust. It is about removing the need to guess. It gives both founders a shared reference point. And it makes it easier to stay friends, because you are not trying to “win” a debate about what was said a year ago.

Company Control and Decision-Making Red Flags

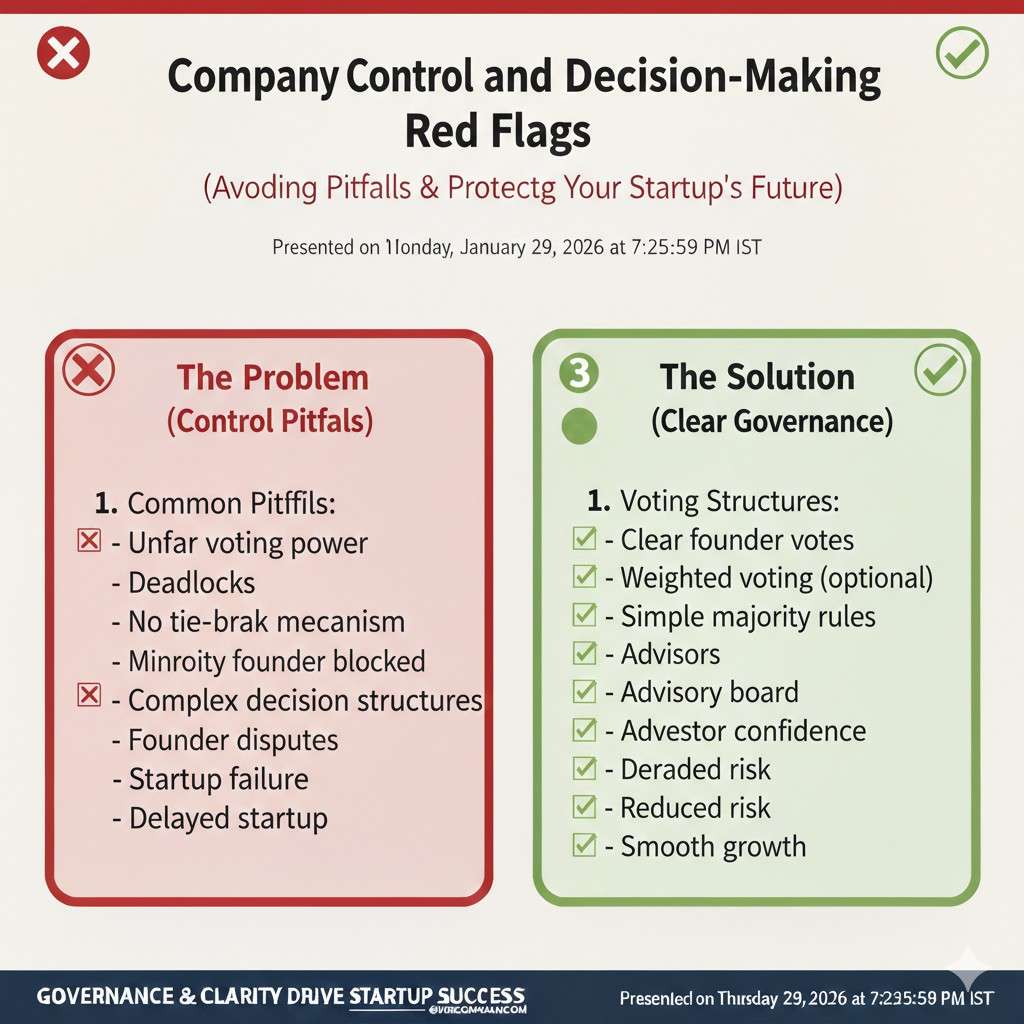

No clear voting rules for key decisions

Some founder agreements assume that founders will “figure it out” when it comes to decisions. But companies do not run on hope. They run on clear authority. If you do not define voting rules early, small disagreements can freeze the company later.

Key decisions include raising money, taking on debt, signing large contracts, selling the company, changing the cap table, hiring executives, and approving budgets. The agreement should say which decisions need a vote, and what vote threshold is required.

If everything requires unanimous consent, one person can block progress. If everything requires a simple majority, a founder can get pushed out of core decisions too easily. There is a balance that depends on the team, but the worst option is leaving it undefined.

No plan for founder deadlock

Deadlock is when founders cannot agree and the company cannot move. It happens more than people think, even in good teams. Sometimes it is about strategy. Sometimes it is about risk tolerance. Sometimes it is about burnout and fear showing up as “logic.”

If your agreement does not address deadlock, your only options may be messy: lawsuits, forced buyouts, or one founder walking away angry. A better path is to define a process ahead of time.

A deadlock process can include steps like a structured discussion period, a neutral advisor vote, mediation, or a “buy-sell” mechanism where one founder offers terms and the other chooses to buy or sell at that price. The right method depends on your values and legal setup, but having a process matters more than the exact method.

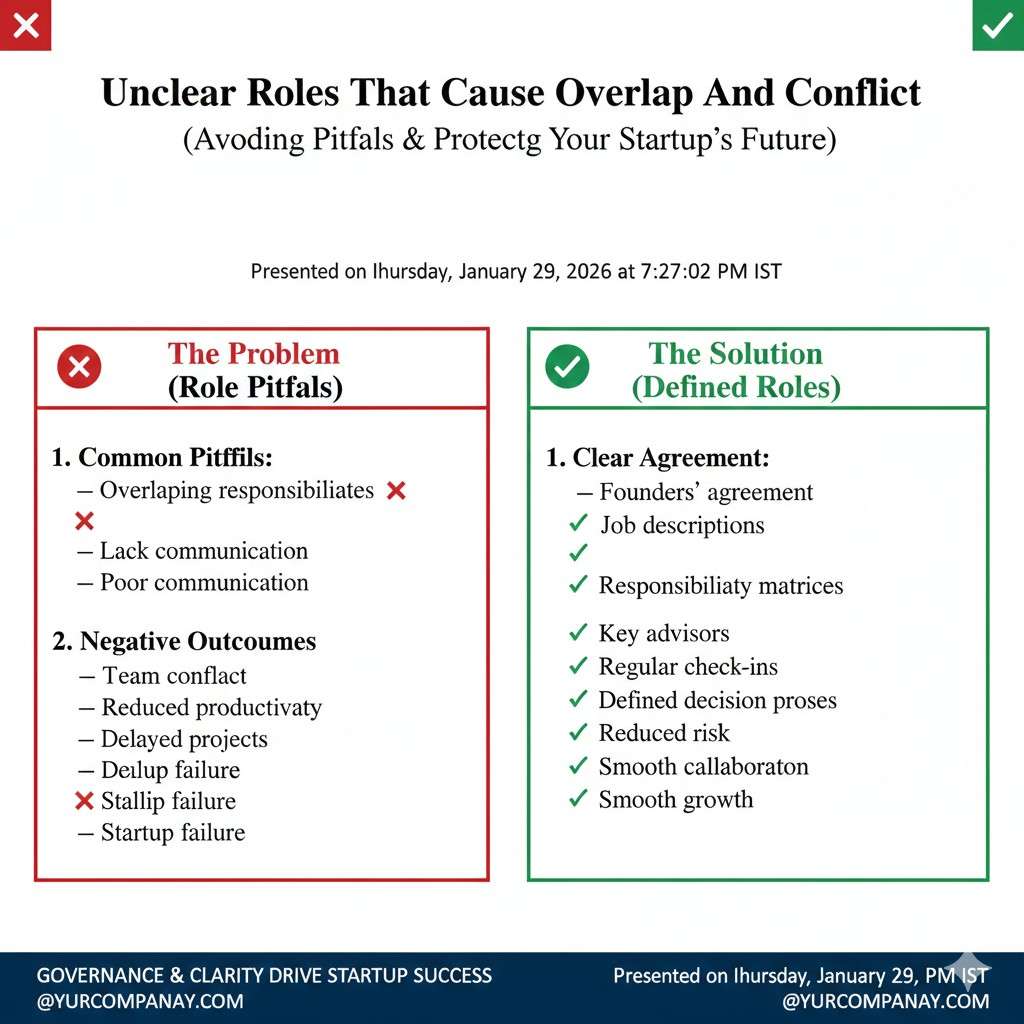

Unclear roles that cause overlap and conflict

Early on, everyone does everything. That is normal. But you still need clarity on final responsibility. If both founders think they “own” product decisions, or both think they “own” hiring, you will collide as soon as the team grows.

The founder agreement should state roles in a way that matches real work. It should not be a title-only document. It should explain areas of authority, expected duties, and how responsibilities can change over time.

This is especially important for technical teams. If one founder owns the core architecture and another owns go-to-market, those boundaries should be clear. Otherwise, even small choices become political, and politics is a slow poison in early-stage companies.

One founder can bind the company without limits

Some agreements allow any founder to sign contracts on behalf of the company. That sounds efficient. But it can be risky if there is no limit. One founder could sign a lease, a loan, or a long-term vendor deal without the other founder knowing.

This is not just about bad intent. It is about speed and stress. A founder might sign something quickly to close a deal, not realizing the long-term cost. Later, the company is stuck with obligations it cannot afford.

Strong agreements clarify who can sign, what needs approval, and what dollar amount triggers a second signature. This protects the company, and it protects the founder who signs, because they are not carrying the blame alone later.

IP and Confidentiality Red Flags

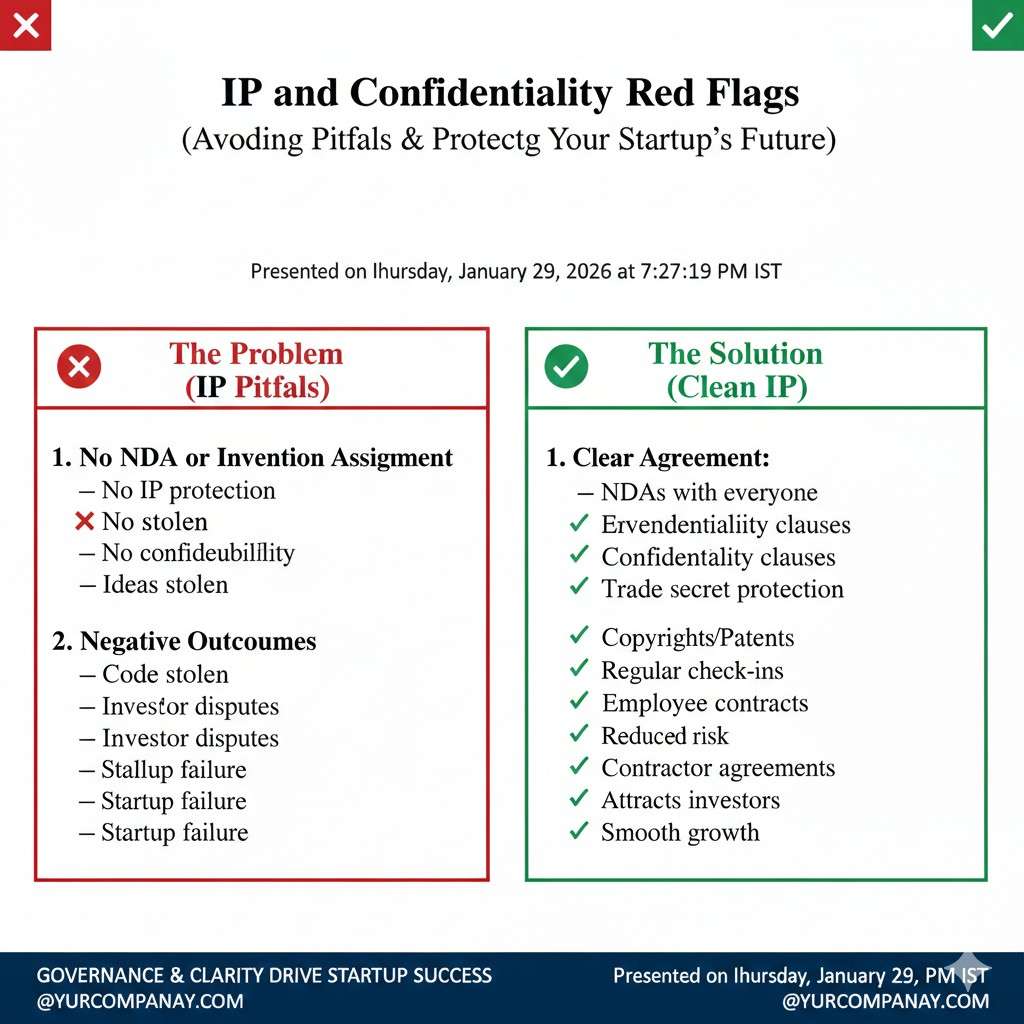

No clean IP assignment from founders to the company

For AI, robotics, and deep tech teams, this is a huge deal. If the founder agreement does not clearly assign inventions, code, designs, and other work to the company, you may not truly own your own product.

Investors look for clean ownership. Patent attorneys need clear ownership to file properly. Acquirers require it to reduce risk. If IP ownership is unclear, deals slow down or fall apart.

The agreement should clearly state that any work created for the company belongs to the company. It should also cover work created before incorporation, because many founders build prototypes early. If pre-company work is not properly transferred, you can end up with a split ownership mess.

If Tran.vc is a fit, this is exactly where we help: we support early IP structure and patent strategy so your foundation is defensible. You can apply anytime at https://www.tran.vc/apply-now-form/

Founders keeping side projects that overlap with the startup

Side projects are common, especially for technical founders. The risk is overlap. If one founder is building something “on the side” that touches the same space, the company can face a conflict of interest and an IP ownership problem.

A good founder agreement defines what is allowed and what is not. It sets rules for disclosure. It clarifies whether side projects must be approved, and it protects the company from founders quietly developing competing work using shared learning.

This is not about banning hobbies. It is about protecting focus and protecting ownership. Even a small overlap can later become a dispute when the company becomes valuable.

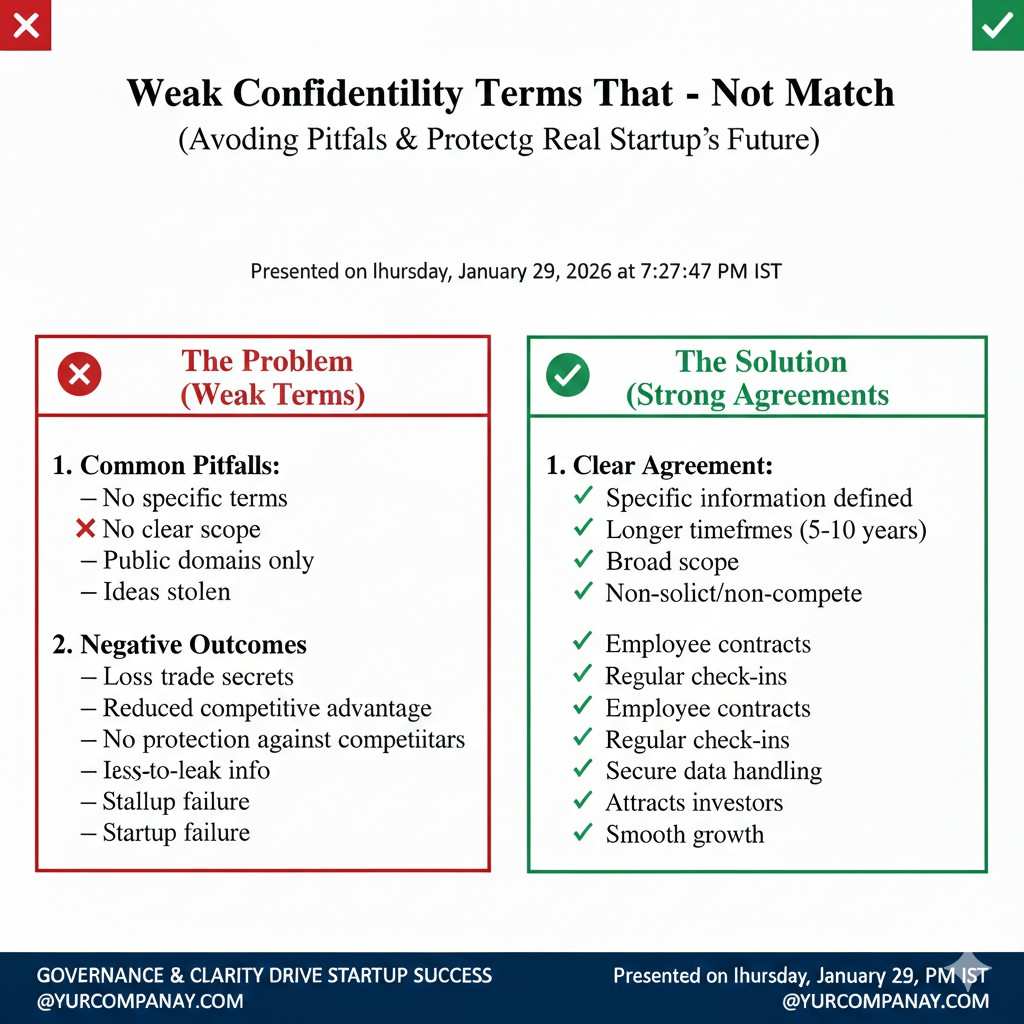

Weak confidentiality terms that do not match real startup needs

Many templates have a generic confidentiality clause. It might not cover what matters most: training data, model weights, customer lists, pricing, design docs, prototypes, vendor terms, and investor conversations.

Confidentiality also needs practical enforcement. For example, what happens when a founder leaves? Do they return devices? Do they delete data? Do they keep access to GitHub, cloud accounts, and shared docs? If the agreement is silent, offboarding becomes chaotic.

Strong terms are specific about what is confidential, how it should be handled, and what obligations survive after someone leaves. It reduces the chance of accidental leaks and makes separation cleaner.

Compensation, Expenses, and Founder Duty Red Flags

No clarity on whether founders are paid or unpaid

In the early days, many founders work without salary. That is normal. The problem starts when the agreement does not clearly say this, or when it does not say when and how compensation can begin. Silence creates assumptions, and assumptions break under stress.

One founder may assume payment starts after funding. Another may assume payment starts after revenue. A third may quietly expect reimbursement for time or lost income. When cash finally appears, these different expectations collide.

A strong agreement states the truth clearly. It explains whether founders are unpaid, under what conditions pay can start, who decides, and how changes are approved. This removes quiet pressure and prevents money from becoming personal.

Unclear rules around expense reimbursement

Founders often pay for tools, travel, legal fees, and services out of pocket. That is part of building. But without clear rules, expense reimbursement can turn into resentment. One founder may spend freely, assuming repayment later. Another may be careful and feel taken advantage of.

The agreement should explain what counts as a company expense, what needs approval, and how reimbursement works. It should also clarify timing, because early-stage companies often cannot repay immediately.

Clear rules protect both sides. They protect the founder who spends money in good faith, and they protect the company from surprise obligations it cannot afford.

No definition of full-time commitment

“Full-time” can mean different things. For some founders, it means 40 hours a week. For others, it means mental priority. Without a shared definition, disappointment grows quietly.

If one founder is juggling consulting work or another startup, the agreement should reflect that reality. If full focus is required, that should be stated plainly. Ambiguity makes it hard to address performance issues without emotion.

This is not about policing hours. It is about alignment. When expectations are written down, conversations stay factual instead of personal.

Founder duties described in vague or symbolic terms

Some agreements describe roles in very high-level language that sounds nice but means little. Titles without duties create confusion. When something goes wrong, no one knows who was responsible.

Clear duties do not limit creativity. They create ownership. They also help when the company grows and hires its first employees, because leadership boundaries are already set.

Duties can evolve, but the agreement should explain how changes happen. Otherwise, role changes feel like power grabs instead of natural growth.

Exit, Departure, and Breakup Red Flags

No clear process if a founder wants to leave

Founders leave for many reasons. Health issues, family needs, burnout, better opportunities. Leaving is not failure. But leaving without rules can damage the company badly.

The agreement should explain how a founder can resign, what notice is required, and what happens next. It should cover equity treatment, access removal, and communication expectations.

Without this, departures become emotional events. The company pauses. Lawyers get involved. Momentum dies at the worst time.

Equity treatment on departure is unclear or unfair

This is where many disputes start. If a founder leaves, do they keep all their shares? Only vested shares? Are unvested shares returned to the company? At what price?

If the agreement does not spell this out, people argue later based on feelings instead of rules. Someone may feel entitled. Someone else may feel betrayed. Neither side feels safe.

Clear equity treatment protects the company and the departing founder. It sets expectations early, when everyone is calm and aligned.

No distinction between good leaver and bad leaver

Not all departures are the same. Someone leaving due to illness is different from someone leaving to start a competing company. Treating all exits the same can be unfair and risky.

Many strong agreements distinguish between types of departure and adjust equity or obligations accordingly. This is not about punishment. It is about matching outcomes to behavior.

Without this distinction, companies either become too harsh or too soft. Both extremes scare investors and future hires.

No non-compete or non-solicit protection

In many places, non-competes are limited or unenforceable. But non-solicit clauses often still matter. These prevent a departing founder from taking customers, employees, or partners immediately.

If the agreement ignores this, a founder can leave and quietly pull value out of the company. Even if they do not mean harm, relationships often follow people, not entities.

Clear limits protect the company during a vulnerable transition. They also set fair boundaries for the departing founder.