Most founders know they “need an ESOP pool.” Fewer founders understand the math behind it—and how that math quietly changes who owns what after the next fundraise.

Here’s the simple truth: the ESOP pool is not just a hiring tool. It is a dilution tool. And the way it is set up can move real ownership away from founders, earlier than you think, often without anyone saying it out loud.

If you are building in robotics, AI, or deep tech, this matters even more. You usually need senior talent sooner. You also tend to raise in stages. That means your ESOP decisions today can ripple through several rounds.

In this guide, I’ll show you how ESOP pool math works in plain words, why investors care so much, and how to protect your future ownership while still hiring great people. And if you want help building leverage early—before you raise a priced round—Tran.vc can help you build real defensibility with patents and IP strategy as in-kind support (up to $50,000). You can apply anytime here: https://www.tran.vc/apply-now-form/

Before we go deeper, one quick note: this article is about understanding the math and the deal mechanics. It is not legal advice. The best outcome is when you understand enough to ask the right questions, then you get your lawyer to paper it cleanly.

ESOP Pool Math: How It Impacts Future Dilution

Why the ESOP pool feels simple, but is not

An ESOP pool is a set of shares kept aside for your team. On the surface, it sounds like a clean and fair idea. You create a pool, you grant options, and you bring in strong people who help you build. Most founders stop thinking right there.

The hard part is that the pool is also a math problem that changes your ownership. It changes it in ways that are easy to miss if you are focused on product, hiring, and fundraising at the same time.

This is why ESOP planning is not “admin work.” It is a core money topic. If you get it wrong, you still may raise money, but you might give away more than you needed to.

If you want to build leverage early, Tran.vc helps technical founders create strong IP and patent plans as in-kind support, so you can raise with more confidence later. You can apply anytime at: https://www.tran.vc/apply-now-form/

What dilution really means in plain words

Dilution means your slice of the company gets smaller when new shares are created. It does not mean your company is worse. It just means more people now share the same pie.

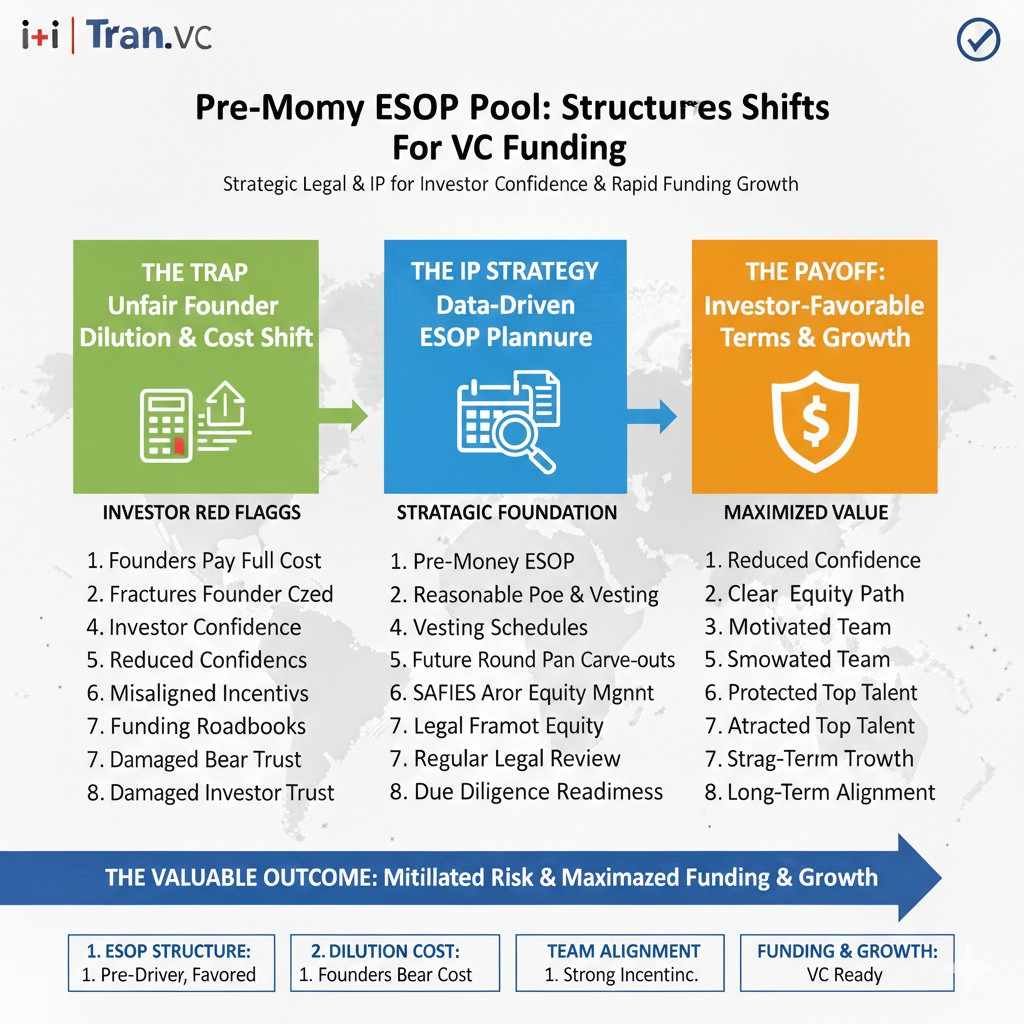

The key point is that dilution is not only caused by investors buying shares. It is also caused by creating shares for an ESOP pool. That pool usually gets created or expanded right before a priced round.

So when you hear “we need to refresh the pool,” you should hear “we are about to change the cap table.” Cap table is just the table that shows who owns what.

The part founders miss: who pays for the ESOP pool

In many startups, investors ask the company to have a certain ESOP pool size right after the round closes. That sounds like the pool is part of the deal, and the cost is shared by everyone.

But in practice, the pool is often created before the investor money comes in. When that happens, the dilution hits the existing holders first. That usually means founders and early employees take the hit.

This is not always “bad.” It can be normal. The problem is when you do not see it, do not model it, and do not negotiate it.

A quick promise for the rest of this guide

We will keep this simple. We will not hide behind complex terms. We will walk through the math in a way you can use during a real term sheet conversation.

You will learn how to spot the “pool shuffle,” how to model it in minutes, and how to choose a pool size that matches your hiring plan instead of someone else’s assumptions.

And if you want help turning your technology into assets investors respect, Tran.vc supports founders with patents and IP strategy as in-kind funding support. Apply anytime at: https://www.tran.vc/apply-now-form/

ESOP pool basics you must get right

Options are not shares, until they are exercised

Employee options are a promise. They give someone the right to buy shares later at a set price. That set price is called the strike price.

Until someone exercises options, they do not own shares. But the pool still matters because investors and acquirers look at the “fully diluted” picture. That means they count the pool as if it will be used.

So even though options are not shares yet, the pool still reduces your percentage on paper. In fundraising, “on paper” is what sets the deal terms.

Authorized shares vs issued shares vs the option pool

Most startups create a large number of authorized shares early, like 10 million. This number is often chosen for convenience, not because it has deep meaning.

Issued shares are the shares already given to founders and any early holders. The option pool sits in the middle. It is authorized and reserved, but not issued to a person yet.

When people talk about “increasing the pool,” they usually mean reserving more shares. That reservation changes the fully diluted cap table. That is what impacts dilution discussions.

The ESOP pool is a planning tool, not a guess

A pool should exist for a reason. That reason is hiring over a planned window, usually 12 to 18 months.

If you do not have a hiring plan, you end up picking a pool size based on fear. Founders fear they will not be able to hire. Investors fear the company will have to expand the pool later, which could reduce their ownership.

The best pool size is the one that matches the hires you truly plan to make before the next round, with some buffer for real-world surprises.

The two ways ESOP pool math shows up in a round

Post-money pool: the clean story people tell

Sometimes you will hear, “The pool is part of the post-money.” This means, after the investor money comes in, everyone is diluted together, including the new investor.

In that setup, the investor effectively shares the cost of the pool. It is not always how deals are structured, but it is the cleanest way to think about fairness.

If you can push the deal closer to this structure, it often protects founders. But what matters is not the words. It is the numbers in the cap table model.

Pre-money pool: the common structure that shifts dilution

More often, the investor will say something like, “We need a 10% option pool included in the pre-money.”

What that often means is the pool must be created before the new money is counted. So the pool reduces the founder percentage first, then the investor buys into the company at that new lower founder ownership level.

This is the core reason founders feel surprised after signing a term sheet. They thought the valuation was one thing, but the pool moved the real ownership math behind the scenes.

Why investors push for a pre-money pool

Investors want the company to be able to hire without coming back to them soon asking for another pool increase. They also want their ownership target to remain stable.

If the pool is created pre-money, it helps them hit that target. In their eyes, they are paying for the company, not for your future hires.

This can be a reasonable viewpoint. The founder viewpoint is also reasonable: you are building the company, and hiring benefits everyone, including investors. That is why this is a negotiation topic.

A simple example that shows how dilution shifts

Start with a clean cap table

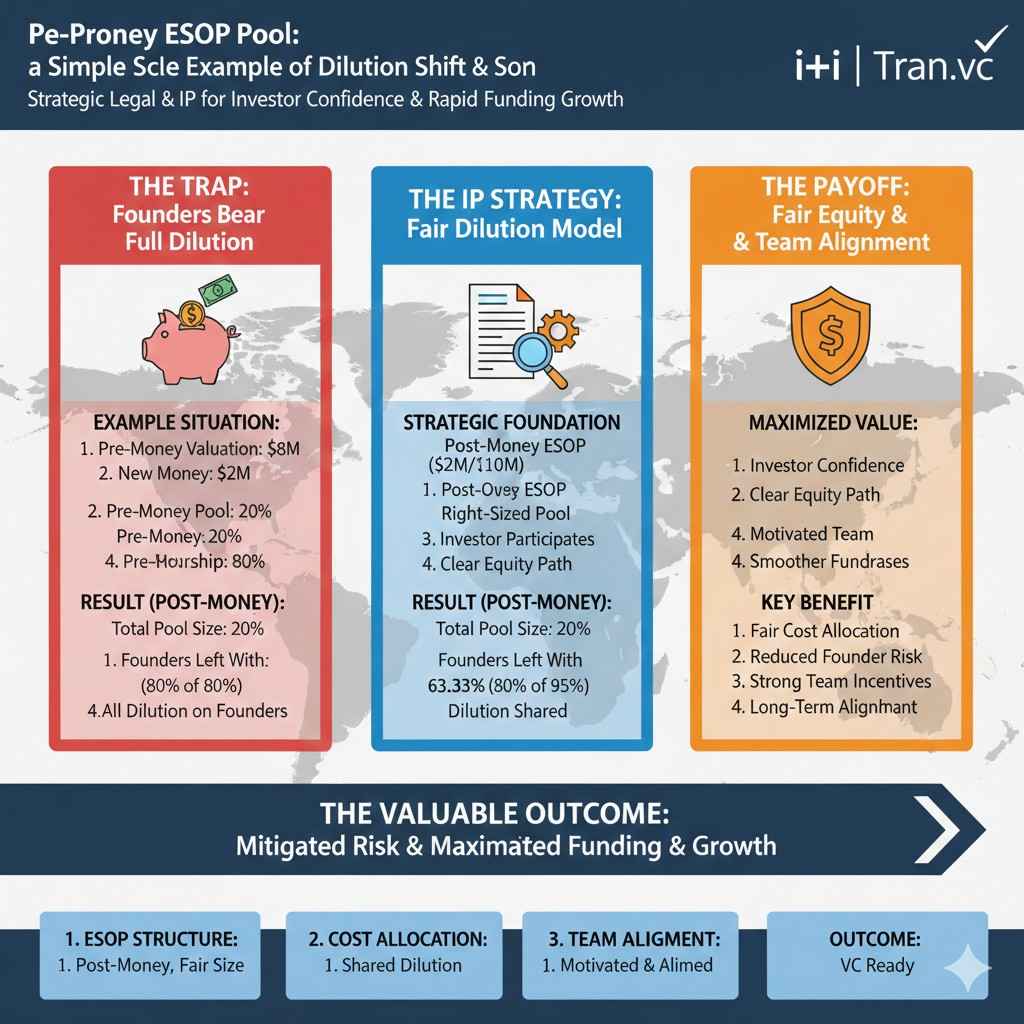

Let’s say you and your co-founder own 100% of the company today. You have 8,000,000 shares issued between you.

Now an investor wants to put in money for 20% ownership. You might think, “Okay, we will end up with 80% and they will have 20%.”

That can be true only if nothing else changes. But in real deals, something else almost always changes: the option pool.

Add a pool and watch the math change

Now imagine the investor says, “We need a 10% option pool after the round.” The wording sounds small, but it changes the share counts.

If that pool is set up pre-money, the company issues new shares into the pool before the investor invests. Your percentage drops because you now own 8,000,000 shares out of a larger fully diluted number.

Then the investor buys shares to reach 20% of that larger number. Your final percentage ends up lower than the simple 80% you expected.

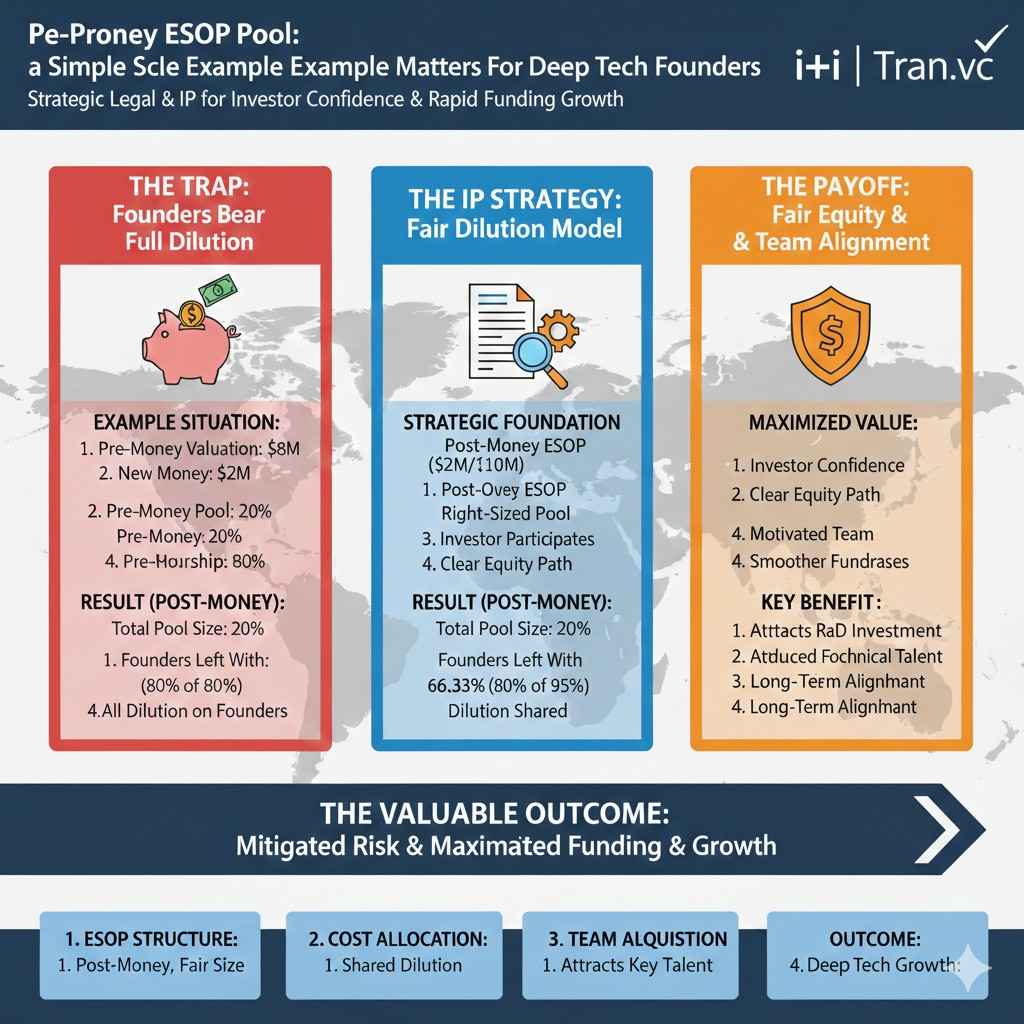

Why this example matters for deep tech founders

In robotics and AI, you often need a strong team early: a senior engineer, a product lead, maybe someone who understands safety, hardware, or enterprise sales.

That hiring need can make a larger pool reasonable. But the right move is to plan it, not accept a number because it sounds “standard.”

Tran.vc helps founders create leverage by turning technical work into protectable assets through patents and IP strategy. When you have real defensibility, you can often negotiate from a stronger place. Apply anytime at: https://www.tran.vc/apply-now-form/

The ESOP pool is not just “10%”—it is a timeline

Pool size should match the next 12–18 months

A good pool is tied to a specific hiring plan. It asks, “Who are we hiring before the next fundraise, and what option grants will we need?”

If you raise seed today and plan a Series A in 15 months, your pool should cover those 15 months. You do not need to fully stock the company for the next five years right now.

Over-sizing the pool “just in case” can create dilution today for hires you may never make.

Unused pool still dilutes you in negotiations

Even if you never grant a single option, an unused pool still counts in the fully diluted cap table.

That means if you accept a very large pool, you are giving away ownership on paper. That paper ownership drives investor math. It also drives how future rounds stack up.

So a pool that sits unused is not harmless. It is quiet dilution that did not even help you hire.

A small buffer is wise, but a huge buffer is costly

Hiring is messy. People decline offers. You might need a different role than you planned. Having some extra room helps you move fast.

But there is a difference between a buffer and a vague guess. When the pool is too big, you are paying today for uncertainty.

A better approach is to right-size now and refresh later when there is a real need, ideally with a clear reason and clear math.

The “pool shuffle” that founders should spot early

How it shows up in term sheet language

Sometimes the term sheet will list a valuation, then include a line that says something like, “The pre-money valuation includes an unallocated option pool equal to X% of the post-money.”

That one sentence can change your outcome more than the valuation number.

It can be confusing on purpose or confusing by habit. Either way, you should translate that sentence into actual share counts and founder percentage.

Why the valuation headline can be misleading

A founder might hear “$10M pre-money” and assume the math is straightforward. But if the pool is increased pre-money, the effective valuation for founders is lower.

This is not about anyone tricking you every time. It is about the deal having multiple moving parts.

Your job is to convert the headline into, “After this round, what percent do we own, and what percent is left for our next hires?”

The easiest way to protect yourself is to model it

You do not need fancy software to model it. You need a simple cap table.

When you can model it, you can negotiate it. When you cannot model it, you are negotiating blind, and the other side will naturally steer toward what helps them.

How to do ESOP pool math without getting lost

Start with one number that matters most

When you are modeling dilution, the cleanest starting point is the fully diluted share count before the round. Fully diluted means you count founder shares plus any shares already reserved for options, plus any other convertibles that are treated as shares in the model.

If you do not know this number, you will keep guessing. If you do know it, you can test any pool size and see the impact in seconds. Many founders only look at valuation and forget share count. That is where confusion starts.

A simple habit helps here. Before you negotiate, open your cap table and write down the current fully diluted shares as a single line. That becomes your “baseline.” Every change in the deal becomes visible because you can see what has to be added and why.

Use ownership targets, not feelings

Most early-stage rounds are driven by ownership targets. Investors often aim for a certain percent after they invest. Founders want to stay above a certain percent so they feel motivated and still have room for future rounds.

When you treat dilution like a feeling, you react too late. When you treat it like a target, you can plan. A founder can say, “I want to stay above X% after seed so I am not crushed after Series A.” That is a rational goal.

Once you choose targets, your job is to connect them to share math. That means you will stop arguing about what is “standard” and start discussing what is needed to build the company and stay healthy through the next two rounds.

Convert every term into shares

Valuation is a money number. Ownership is a percent number. Your cap table is a shares number. The bridge between them is new shares issued in the round.

So whenever you see a term sheet, translate it into share counts. Ask, “How many new shares are issued to the investor?” Then ask, “How many new shares are added to the pool?”

If you can answer those two questions, you can compute everyone’s final percent. If you cannot, then you only have a story, not a model. Investors will always have a model. You should too.

Step-by-step example with real numbers you can reuse

Set the starting cap table

Assume you have 8,000,000 founder shares issued today. There is no pool yet because you have been scrappy and only hired contractors. That means your fully diluted shares are also 8,000,000.

Now you are raising a seed round. An investor wants to invest and end up with 20% ownership after the round. The investor also asks for a 10% option pool to be available after the round.

This is the exact moment where founders can accidentally agree to extra dilution without noticing. The trick is to make the pool timing explicit. Is that 10% created before the money comes in, or after?

Model the post-money pool case first

In a post-money pool setup, the investor and the founders share the dilution from the pool. The pool is treated like it is created as part of the final post-round cap table.

The end state is: founders + investor + option pool = 100%. The investor wants 20%. The pool wants 10%. That leaves 70% for founders.

In this simplified view, founders go from 100% to 70% in one round. That 30% drop is made of 20% for the investor and 10% reserved for team options. The numbers are direct, and the story matches the math.

This is why post-money pool language often feels “fair” to founders. Everyone pays for the ability to hire.

How to do ESOP pool math without getting lost

Start with one number that matters most

When you are modeling dilution, the cleanest starting point is the fully diluted share count before the round. Fully diluted means you count founder shares plus any shares already reserved for options, plus any other convertibles that are treated as shares in the model.

If you do not know this number, you will keep guessing. If you do know it, you can test any pool size and see the impact in seconds. Many founders only look at valuation and forget share count. That is where confusion starts.

A simple habit helps here. Before you negotiate, open your cap table and write down the current fully diluted shares as a single line. That becomes your “baseline.” Every change in the deal becomes visible because you can see what has to be added and why.

Use ownership targets, not feelings

Most early-stage rounds are driven by ownership targets. Investors often aim for a certain percent after they invest. Founders want to stay above a certain percent so they feel motivated and still have room for future rounds.

When you treat dilution like a feeling, you react too late. When you treat it like a target, you can plan. A founder can say, “I want to stay above X% after seed so I am not crushed after Series A.” That is a rational goal.

Once you choose targets, your job is to connect them to share math. That means you will stop arguing about what is “standard” and start discussing what is needed to build the company and stay healthy through the next two rounds.

Convert every term into shares

Valuation is a money number. Ownership is a percent number. Your cap table is a shares number. The bridge between them is new shares issued in the round.

So whenever you see a term sheet, translate it into share counts. Ask, “How many new shares are issued to the investor?” Then ask, “How many new shares are added to the pool?”

If you can answer those two questions, you can compute everyone’s final percent. If you cannot, then you only have a story, not a model. Investors will always have a model. You should too.

Step-by-step example with real numbers you can reuse

Set the starting cap table

Assume you have 8,000,000 founder shares issued today. There is no pool yet because you have been scrappy and only hired contractors. That means your fully diluted shares are also 8,000,000.

Now you are raising a seed round. An investor wants to invest and end up with 20% ownership after the round. The investor also asks for a 10% option pool to be available after the round.

This is the exact moment where founders can accidentally agree to extra dilution without noticing. The trick is to make the pool timing explicit. Is that 10% created before the money comes in, or after?

Model the post-money pool case first

In a post-money pool setup, the investor and the founders share the dilution from the pool. The pool is treated like it is created as part of the final post-round cap table.

The end state is: founders + investor + option pool = 100%. The investor wants 20%. The pool wants 10%. That leaves 70% for founders.

In this simplified view, founders go from 100% to 70% in one round. That 30% drop is made of 20% for the investor and 10% reserved for team options. The numbers are direct, and the story matches the math.

This is why post-money pool language often feels “fair” to founders. Everyone pays for the ability to hire.