Founders move fast. You write code, talk to users, ship demos, and try to stay alive long enough to find traction. In that rush, it’s easy to treat founder agreements like “later paperwork.”

But a founder agreement is not paperwork. It is the rulebook for your company and your friendship.

If it is not in writing, it is not real. Not in a legal fight. Not in an investor meeting. Not when someone quits, gets sick, breaks trust, or wants more than they earned.

A clean founder agreement does one main thing: it prevents “memory wars.” It replaces “I thought we said…” with clear words everyone signed. It keeps the team focused on building, instead of arguing.

And because Tran.vc helps deep tech founders build real moats early, we see this pattern all the time: teams that treat IP seriously, but forget to lock in founder basics. They file patents, but they don’t lock down ownership, roles, and exit rules. That gap can kill a round. Or worse, it can kill the company.

This article is about what must be in writing between founders. Not theory. Not “best practice” fluff. Real parts you can put into a document, with plain language and real examples of what goes wrong when you skip them.

Before we begin: this is not legal advice. It is practical guidance. You should have a lawyer review your final agreement. If you are building in robotics, AI, or other deep tech, the stakes are even higher because your work can become patents, trade secrets, and real defensible assets. If you want help building that foundation, you can apply to Tran.vc anytime here: https://www.tran.vc/apply-now-form/

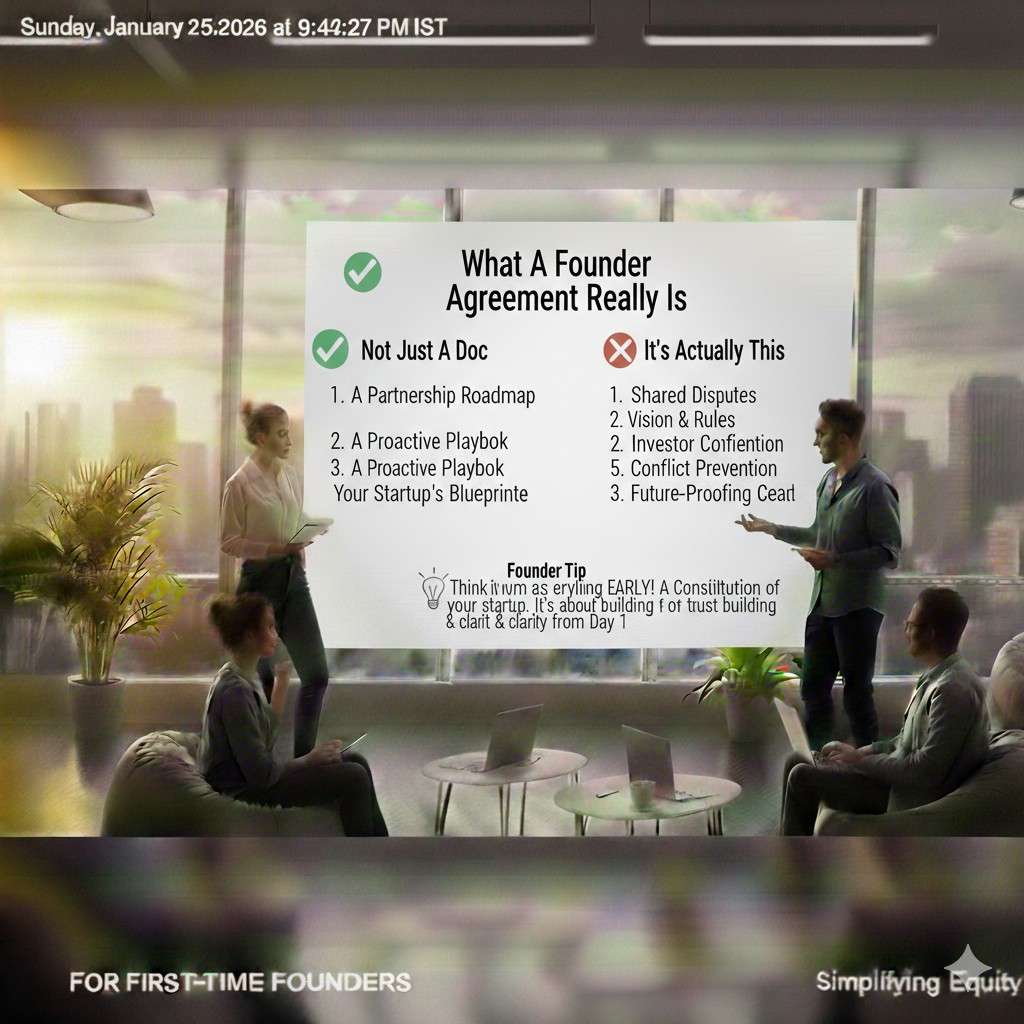

What a founder agreement really is

Most people think a founder agreement is one document. In real life, it is usually a small set of documents that work together. The goal is simple: define who owns what, who does what, how decisions happen, and what happens when things change.

You can have a handshake partnership for a weekend hackathon. You cannot run a company on one.

A founder agreement should answer these questions with zero confusion:

Who owns the company, and how much?

What does each founder do, and what counts as doing the job?

Who owns the code, inventions, designs, and ideas?

How do we make decisions when we disagree?

What happens if someone leaves?

What happens if someone stops doing the work but keeps the equity?

How do we handle money, salaries, and expenses?

How do we protect the company’s secrets?

How do we settle disputes without burning the company down?

If your documents do not answer those clearly, they are not done.

The hard part is not writing the words. The hard part is saying the quiet parts out loud. The founder agreement forces honest talks early, when you still like each other.

If you skip the talk now, you will have it later. And later it will be expensive.

Start with the core: who owns what, and why

Equity is emotional. It is tied to ego, risk, and pride. This is why equity fights feel personal. A good agreement makes equity boring. Boring is good.

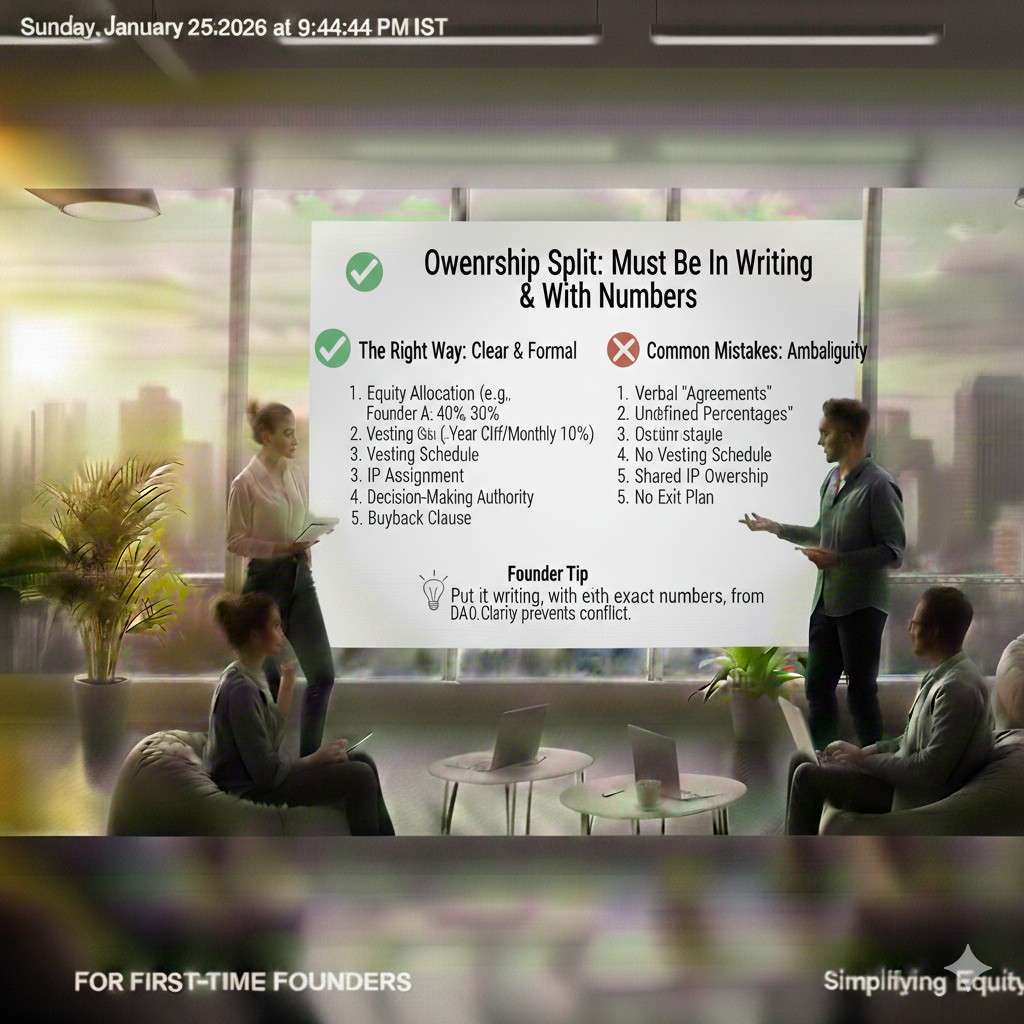

The ownership split must be in writing, with numbers

Do not write “we will split fairly.” Write exact shares or exact percentages.

You should also write why the split is what it is. Not because the law needs it, but because you will forget.

Many teams split 50/50 because it feels fair. Sometimes it is fair. Many times, it is a trap.

Here is the real test: if you had to replace one founder tomorrow, could you? If yes, that role may not deserve half. If no, and the company cannot exist without that person, then maybe half makes sense.

Another test: if one founder is full-time and one is part-time, the split should reflect that. If one founder brings the key invention and the other joins later, the split should reflect that too.

Also, the split is not just “today.” You need to plan for how the split behaves when time passes, work changes, or someone leaves. That is why vesting is not optional.

Vesting: the part that saves your company

Vesting means you earn your equity over time by staying and contributing. It exists because people leave. Even great people leave.

Without vesting, one founder can walk away after three months with a huge chunk of the company. That chunk can scare investors, block hiring, and block future fundraising. It can also create a bitter feeling for the people who stayed.

Most startups use four-year vesting with a one-year cliff. In simple words, that means: you earn equity over four years, and if you leave before one year, you get nothing. After the first year, you start earning monthly or quarterly.

You do not need to copy a template blindly, but you do need vesting that is normal enough that investors do not panic.

Also, make sure vesting applies to every founder. Not just the “newer” one. Exceptions are possible, but every exception should be written, explained, and agreed.

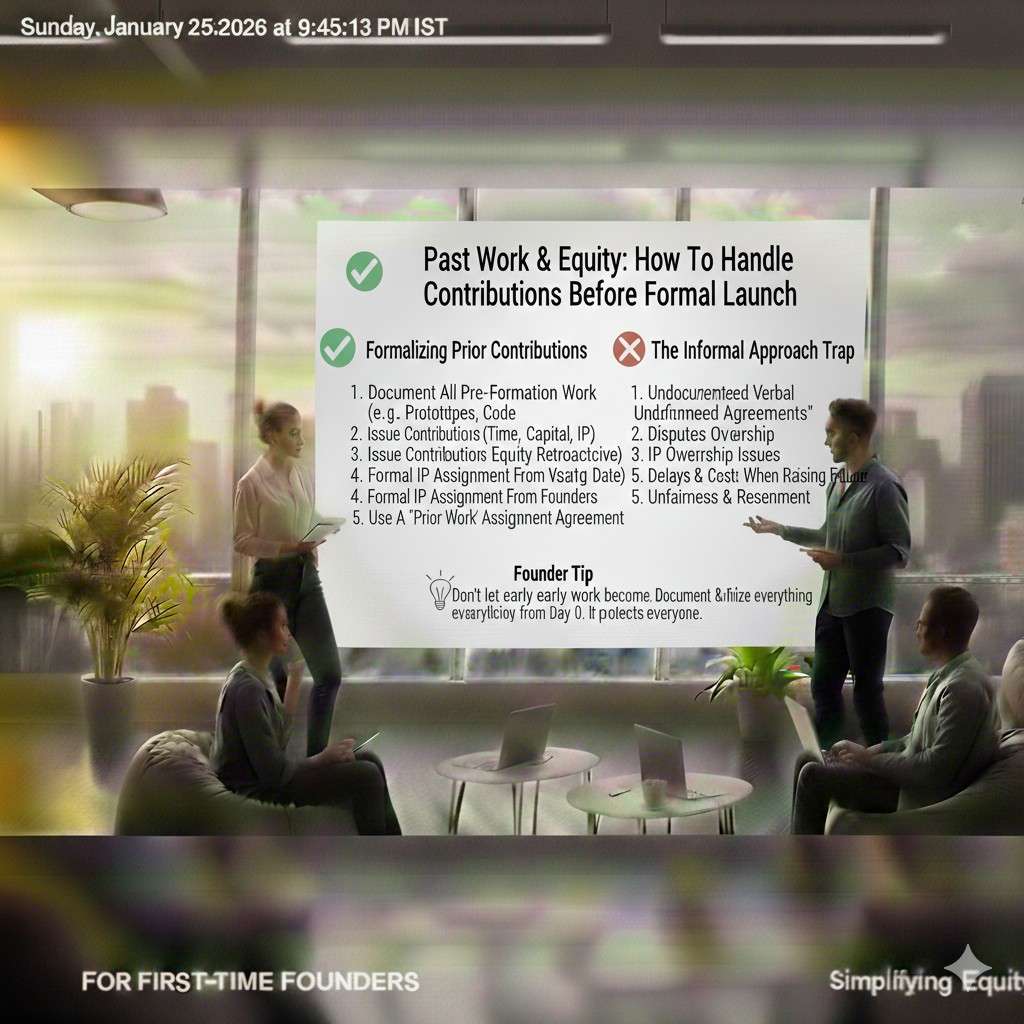

What about past work before the company formed?

This is where deep tech teams get burned.

Maybe someone built the first model, or wrote the first code, or designed the first hardware prototype before you formed the company. That work is valuable, but it can also become a legal mess if it was done under another employer, at a university lab, or using someone else’s tools and data.

In writing, you need to state:

What work existed before the company

Who created it

Whether the company now owns it

Whether it is being “assigned” to the company

Whether any outside party might claim it

If you are building patentable tech, this part matters even more. If the early invention is unclear, your patents can get messy. If you want to build a strong moat, you want clean invention ownership from day one.

Tran.vc’s model is built around helping founders do this right early, because investors look closely at IP ownership. If you want support on that side, you can apply here: https://www.tran.vc/apply-now-form/

Roles and expectations: stop guessing, start writing

A founder agreement should not read like a job offer, but it should define roles in a clear way.

This is not about control. It is about reducing resentment.

Many founder fights start like this:

One founder feels they are doing more.

The other feels unappreciated.

Neither has a shared definition of “enough.”

So write it down.

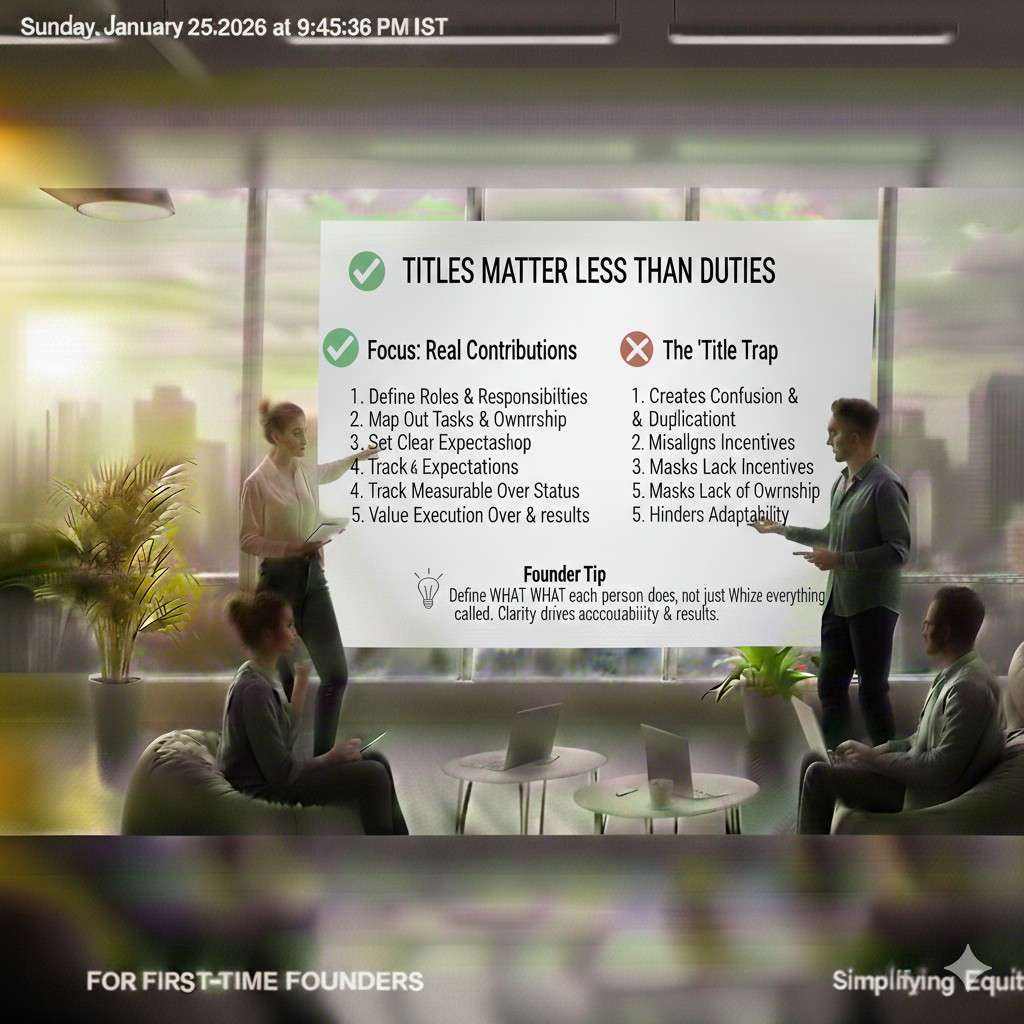

Titles matter less than duties

You can call someone CEO, CTO, or whatever. The title does not protect you. The duties do.

Write what each founder is responsible for in plain words. Not long lists. Just clear areas.

For example: “Product and customer discovery” is a real responsibility. “Operations and finance setup” is real. “Core model training and deployment” is real. “Hardware design and supply chain” is real.

Then add a simple standard: what does “doing the job” look like?

This is where people get uncomfortable, but it helps later. You can write things like:

Founder A will work full-time, with startup as the main job.

Founder B will work at least X hours per week until date Y, then transition full-time.

Both founders will join weekly planning and investor calls unless traveling or sick.

Both founders will share progress weekly in writing.

Keep it simple. You are not trying to police each other. You are trying to avoid “I didn’t know you expected that.”

Time commitment must be stated

If someone is part-time, say it clearly. If someone is still employed elsewhere, say it clearly. If someone is in school, say it clearly.

Investors will ask. And even if you never raise money, your future team will feel the impact.

Also, write what happens when time commitment changes. For example, if someone stays part-time longer than expected, does their vesting slow down? Does their role change? Does the equity change?

Some teams avoid this talk because it feels harsh. But the harsh part is later, when someone feels tricked.

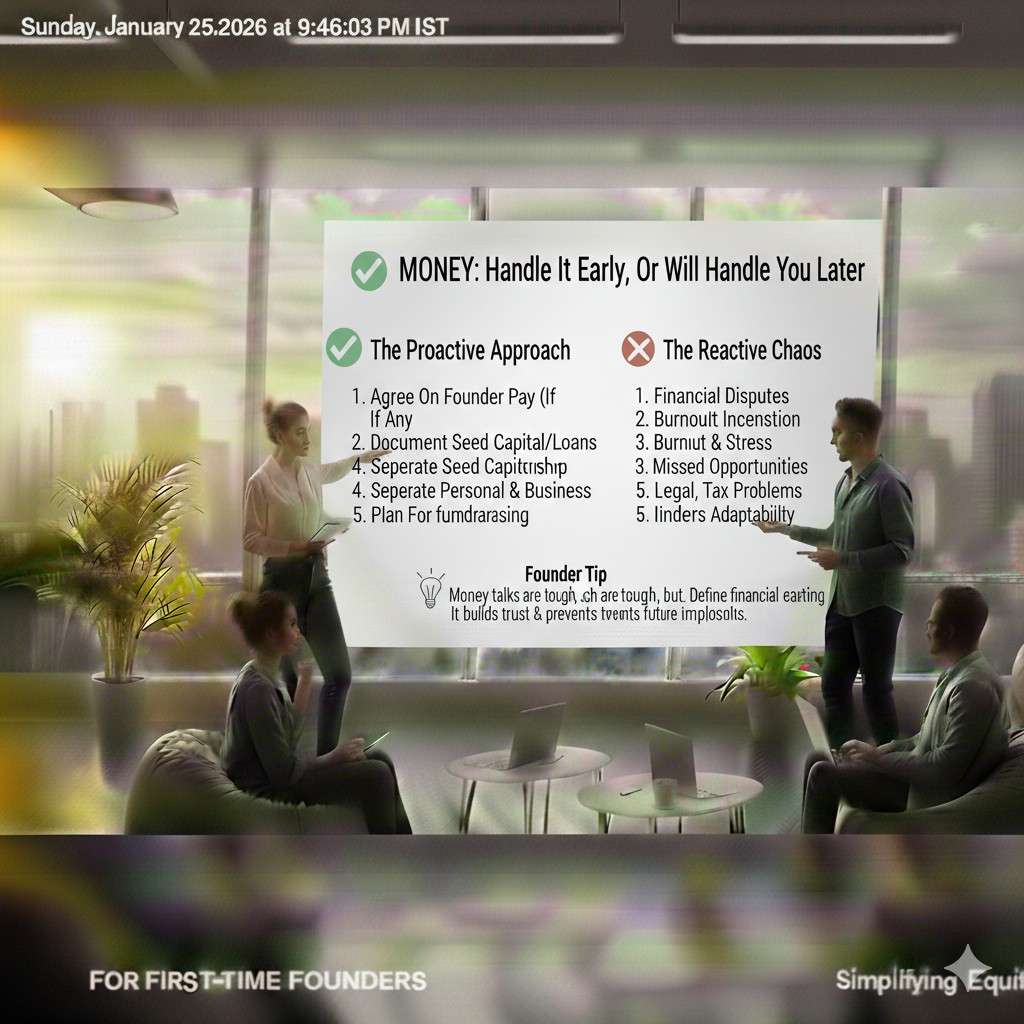

Money: handle it early, or it will handle you later

Money issues do not always mean greed. Often they mean survival.

One founder may have savings. Another may have rent due. If you do not talk about it early, you create silent pressure that turns into anger.

Salaries: when, how much, and who decides

In most early startups, founders do not pay themselves at first. But you should still write rules for when you can.

For example: “No founder salary until we raise outside funding” is clear. Or: “Founder salaries can start after revenue hits X per month” is clear. Or: “Founder salary requires approval by the board” is clear.

If you do not write this, one founder may start paying themselves from the bank account and claim it was fine. Even if they meant no harm, that can destroy trust.

Also write how salary levels are set. You do not need to pick a number now. You just need a rule for who decides and what standard you use.

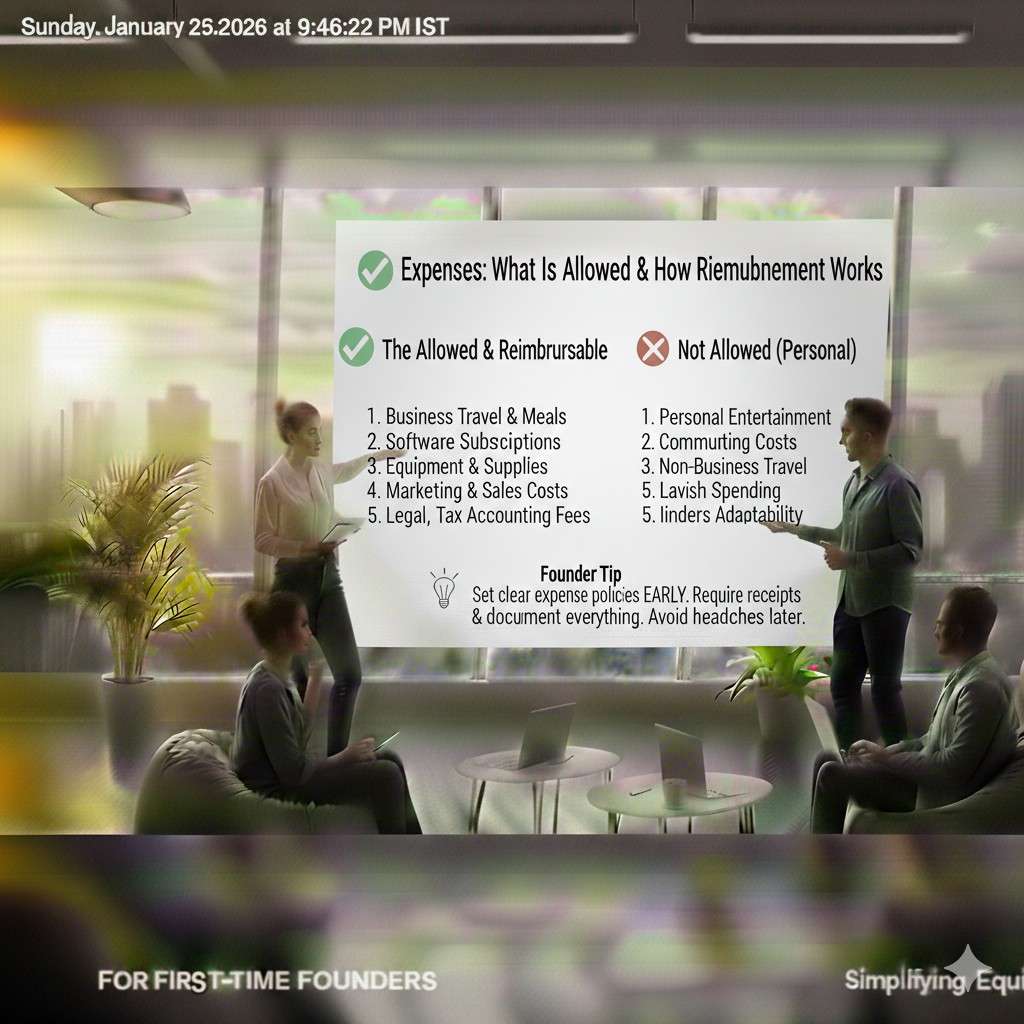

Expenses: what is allowed and how reimbursement works

Early teams buy tools, cloud credits, parts, travel, and random stuff. Without rules, people spend differently and get mad.

Write:

What expenses require approval

How approvals happen

How fast reimbursements happen

What proof is needed

It can be simple. But it should exist.

Also, if a founder is personally paying for early costs, write whether that is a loan to the company or a gift. If it is a loan, write when it is repaid and whether it has interest.

If you do not, later someone will say “you owe me” and another will say “I thought you offered.”

The most ignored section: who owns the IP

If you are building in AI, robotics, software, biotech tools, or any deep tech area, IP is not a side issue. It is the product moat. It is often the main reason an investor believes the company can win.

And yet many founder teams do not put clear IP ownership in writing.

This is where things get dangerous.

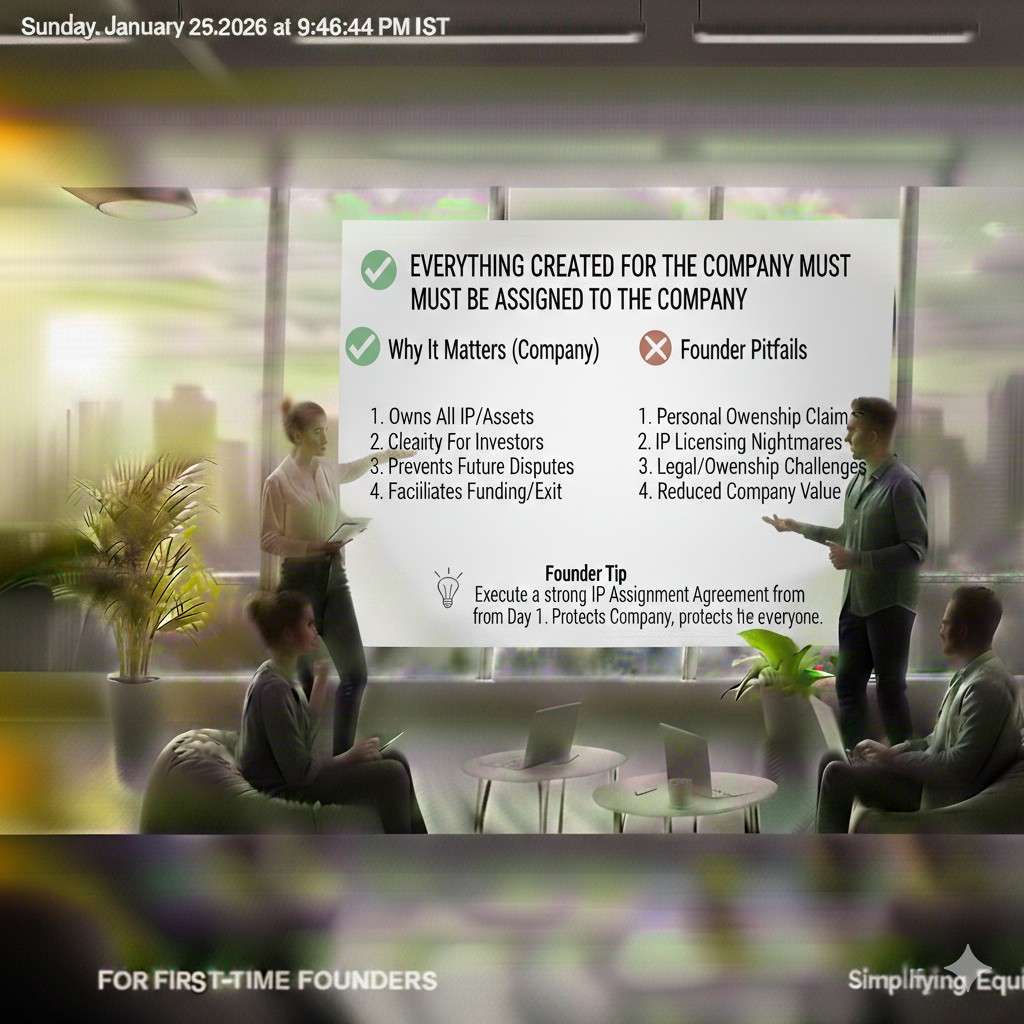

Everything created for the company must be assigned to the company

You need a written invention assignment. The idea is simple: any code, design, model, dataset work, patentable idea, or improvement that a founder creates for the company belongs to the company.

Not to the founder personally.

This sounds obvious, but it is not automatic. The law depends on where you are, who created what, and under what relationship.

If you want to file patents, you need clean assignment. Patent rights start with inventors. The company needs written transfer.

Also, if you ever sell the company, buyers will check this. If it is missing, deals slow down or die.

Watch out for employer and university claims

Many technical founders start while still employed. Many are at universities. Both situations can create outside claims.

Some employers have broad invention policies. Some universities claim rights in inventions made using their resources, labs, or funding.

This does not mean you cannot build. It means you must be careful and honest, and you must get proper clearance.

Your founder agreement should include a representation that each founder has the right to contribute what they contribute, and that they are not violating another agreement.

If someone is not sure, get clarity before pushing further. This is not fear. This is risk management.

Confidentiality: what must stay inside

Write a simple confidentiality promise: founders will not share company secrets, code, designs, customer lists, pricing, or plans outside the company.

Also define what happens when someone leaves: they return devices, delete copies, and stop using the company’s private info.

For deep tech, add a clear rule about research notes, lab notebooks, and model weights. These are often as valuable as the code.

This is also where trade secrets live. Patents are one part. Trade secrets are another. A good agreement supports both.

If you want Tran.vc’s help building a strong IP foundation early, including strategy around patents versus trade secrets, you can apply anytime here: https://www.tran.vc/apply-now-form/

Founder Agreements: What Must Be in Writing

Why this topic matters more than most founders think

Most founders do not ignore founder agreements on purpose. They delay them. They tell themselves they will handle it after the product ships, after the demo day, after the first customer, or after funding. It feels like paperwork that can wait.

In reality, founder agreements shape everything that comes after. They decide who owns the company, who controls the work, who benefits from success, and who carries risk when things go wrong. When these rules are unclear, progress slows. Trust cracks. Focus breaks.

For technical founders building AI, robotics, or deep tech, this matters even more. The value of your company often sits in code, models, designs, and inventions that are hard to explain and easy to fight over. If ownership and responsibility are not clear in writing, even strong technology can become unusable.

Founder agreements are not about planning failure. They are about protecting momentum. They let you build without fear that a future argument will undo years of work.

The real purpose of a founder agreement

A founder agreement is not there to predict every possible problem. Its real job is to remove guesswork. It replaces memory with clarity and emotion with structure.

When nothing is written, every hard moment turns into a debate about the past. People remember conversations differently. Tone gets lost. Assumptions fill the gaps. This is where small disagreements turn into company-ending fights.

When things are written clearly, decisions become easier. Disagreements stay contained. You can point to the document and move forward instead of circling the same argument again and again.

This is especially important when investors enter the picture. Investors do not want to mediate founder disputes. They want proof that the team can operate like adults. A clean founder agreement signals discipline and maturity long before revenue exists.

Why early trust is not enough

Many founders skip written agreements because they trust each other. Often, they are friends, former classmates, or coworkers. That trust is real, and it is valuable. But trust alone does not scale.

People change. Life changes. Pressure changes behavior. What feels obvious today may feel unfair a year from now when workloads shift, money runs low, or one founder carries more stress than another.

A written agreement does not replace trust. It protects it. It removes the need to constantly renegotiate expectations. It gives everyone the same reference point, even when emotions run high.

Strong teams do not avoid structure. They use structure to stay strong.

Why “we’ll figure it out later” is risky

Later is when the company is more valuable, more complex, and more fragile. Later is when outside money, customers, and employees depend on decisions made by the founders.

At that point, changing terms feels personal. Every edit feels like a loss. What could have been a calm discussion early becomes a tense negotiation.

This is why experienced founders lock things down early. Not because they expect conflict, but because they want to remove it as a risk.

At Tran.vc, this pattern shows up again and again. Teams that treat IP, ownership, and responsibility seriously from day one move faster and raise with more leverage. Teams that delay often pay for it in time, legal fees, or lost deals.

If you are building something defensible and long-term, structure is part of the product.

What this article will help you do

This article walks through what must be in writing between founders. Not theory. Not generic advice. Real areas that cause real problems when ignored.

It explains how ownership should be handled, how roles should be defined, how IP should be protected, and how exits and disputes should be planned before they happen. The goal is not to scare you. The goal is to help you build with confidence.

You do not need perfect documenOwnership and Equity

Put the split in writing, with exact numbers

If the ownership split is not written down, it is not real. It is only a story each person tells themselves. That story will change over time, especially when the company becomes valuable.

You want a single, clear statement that shows who owns what. Not “roughly equal.” Not “we’ll make it fair.” Exact percentages or exact share counts. This one detail removes a surprising amount of stress.

It also forces the first hard talk: what each person is really bringing to the table. Time, skills, money, networks, reputation, and the core invention all matter. The agreement should reflect reality, not guilt or politeness.

When a split is vague, people fill the gaps with feelings. When it is clear, people can focus on building.

Avoid “fair” and choose “earned”

Many teams pick 50/50 because it sounds fair. Sometimes it is fair, but many times it is just easy. Easy choices can become expensive later.

A better way to think is “earned.” Who is taking the bigger risk? Who is going full-time first? Who carries the key technical work that cannot be replaced quickly? Who is handling customers, hiring, fundraising, and operations? If one founder carries more of the load, the agreement should reflect that.

This is not about ranking people. It is about reducing future resentment. Resentment grows when the split and the effort do not match.

A split that feels slightly uncomfortable now often prevents a blowup later. A split that feels “nice” now can become a silent problem that poisons the team.

Use vesting so equity matches commitment over time

Vesting is one of the most important parts of any founder agreement. It exists because life is unpredictable. People leave. People burn out. People get pulled back into other jobs. Sometimes people simply stop contributing.

Without vesting, someone can walk away early and keep a large part of the company forever. That is not only unfair. It can also block your future.

Investors dislike messy cap tables. Future hires dislike them too. If a non-working founder owns a large piece, it becomes harder to motivate the people who are actually building. Over time, that dead equity can weaken the company.

Vesting fixes this by tying ownership to time and continued work. It keeps equity aligned with real commitment, not early excitement.

Understand the cliff, because it changes behavior

A cliff is a rule that says equity does not start vesting until a certain point. A common pattern is one year. That means if a founder leaves before a year, they do not keep any of the equity that was meant to vest.

This is not a punishment. It is a test of seriousness. It protects the company from short-term participation and long-term claims.

A cliff also helps founders feel safer. It reduces the fear that someone will “try it out” for a few months and then walk away with a lifetime stake.

When founders know the rules are firm, they are more likely to commit fully or step away early. Both outcomes are healthy.

Decide what happens if a founder leaves

People often avoid this topic because it feels negative. But planning for exits is part of building a stable company. It is also an act of respect.

The agreement should explain what happens to unvested shares when someone leaves. In most structures, unvested shares return to the company. That is what makes the vesting meaningful.

You should also decide what happens to vested shares. In many cases, the founder keeps what is vested. In some cases, the company has the option to buy them back under certain terms. The details depend on your setup, your jurisdiction, and what is normal for your stage.

The key is not choosing the “perfect” model. The key is having a clear model, so nobody is surprised in the worst moment.