Most first-time founders pick an “authorized shares” number because they saw it in a template, or a friend said “just do 10 million.” Then, months later, they hit a weird problem: their cap table looks messy, their option pool math gets harder than it should, or they’re stuck paying extra fees in some states because the share count is too high.

Authorized shares sound like a small legal checkbox. In real life, they shape how clean your company feels to investors, employees, and future you.

In this guide, I’ll help you choose a number that is simple, flexible, and easy to live with. And if you want help building a real moat while you set this up, Tran.vc can support you with up to $50,000 in in-kind patent and IP services for deep tech, AI, and robotics startups. You can apply any time here: https://www.tran.vc/apply-now-form/

Before we get into the “how many,” let’s get very clear on what “authorized shares” actually means—because this is where most confusion starts.

Authorized shares are not the shares you “have.” They are the shares your company is allowed to issue under its charter. Think of it like a bucket. The bucket size is the authorized number. The water you pour in is the shares you actually issue to people.

On day one, you normally issue some shares to founders. You may also reserve shares for an employee option pool. Later, you might issue shares to advisors, early hires, angels, or a seed investor. Every time you do that, you are using shares from the bucket. If you run out, you can increase the authorized number, but that takes paperwork, board approval, stockholder approval, and legal time. It is not a disaster, but it is friction. And friction shows up at the worst time—when you’re hiring fast or raising money.

So the goal is simple: authorize enough shares so you will not run out at an awkward time, but not so many that you create extra cost, confusion, or a cap table that feels sloppy.

Now here is the part that surprises people: the exact number of authorized shares is not the same thing as ownership.

If your company authorizes 10,000,000 shares, that does not mean each founder “owns less” than if you authorize 1,000,000 shares. Ownership is about percentages, not raw share count. If two founders split 50/50, they can each hold 500,000 shares out of 1,000,000, or 5,000,000 out of 10,000,000. Same 50/50. Different share count.

So why do investors and lawyers still care about the number?

Because share count affects how clean everything feels:

A clean share count makes option grants easy to explain.

A clean share count makes price-per-share math easy in a financing.

A clean share count makes it easier to do splits, pools, and grants without tiny fractions.

A clean share count avoids running out when you least expect it.

There is also a second layer: authorized shares interact with par value and state filing fees in some places. This is where “just do 10 million” can become a quiet money leak depending on where you are incorporated and qualified to do business. Delaware is common for venture-backed startups. Delaware’s franchise tax is not simply “more shares = more tax,” but the authorized share count can still push you into a higher calculation path if you do not plan it well. The right setup can keep taxes reasonable without making the cap table weird.

This is why I like to treat authorized shares as a design choice, not a default.

Let’s talk about the decision in a very practical way, like you are sitting at your desk filling out incorporation docs.

You are trying to choose a number that supports four things:

- A simple founder split

- Enough room for an option pool

- Room for early advisors and small grants

- Room for at least one priced round or SAFE conversion without needing an emergency charter change

That’s the real target.

To get there, you need to understand the difference between three numbers that founders mix up:

Authorized shares: the maximum allowed to be issued.

Issued and outstanding shares: shares actually given out and currently owned.

Reserved shares: shares set aside for the option pool (not issued yet).

If you authorize 10,000,000 shares, and you issue 6,000,000 to founders, and you reserve 2,000,000 for an option pool, then you have 2,000,000 left unallocated for future use. Those “leftover” shares are not owned by anyone yet, but they are available for future grants, advisors, or financings.

Now, the reason people pick big numbers is to avoid decimals.

If you authorize only 1,000 shares and you want to grant an employee 0.25% of the company, you are stuck. 0.25% of 1,000 is 2.5 shares. You cannot grant half a share in most simple setups. So you either round and distort the grant, or you do a stock split and redo paperwork.

But if you authorize 10,000,000 shares, 0.25% is 25,000 shares. Easy, clean, no fractions. This is why you see large share counts early.

There is also psychology. Employees like seeing a big number in their offer letter. “25,000 options” feels bigger than “250 options,” even if the percent is exactly the same. Good founders do not play games, but they do understand how humans react to numbers. The key is to keep it honest and easy to explain: “This is the number of options. This is the percent on a fully diluted basis. Here is how vesting works.”

A good share count helps you do that without confusion.

Now let’s get tactical. How do you actually pick the number?

Start with your near future, not your fantasy future.

In the first 12–24 months, most startups will do some mix of:

Founder issuance

Advisor grants (small, but real)

Hiring 3–10 people (sometimes more)

Creating or increasing an option pool (often 10% to 15% early)

Raising pre-seed or seed (often with SAFEs first, then a priced round)

So you want a structure that can handle those without needing to rewrite your charter right away.

A very common pattern for a Delaware C-Corp is to authorize 10,000,000 shares of common stock at formation. That pattern exists for a reason: it gives room for founders, pool, and early grants with clean numbers.

But “common pattern” does not mean “always correct.”

Here are situations where 10,000,000 might be too high or not ideal:

If you are incorporating in a state that charges fees based on authorized shares, you might pay more than needed.

If your legal docs set a par value that creates odd accounting, you might add friction later.

If you are doing a structure that includes multiple classes early (rare, but sometimes), you may want a different plan.

If you are not Delaware, your state rules may make other counts simpler.

And here are situations where 10,000,000 may be too low:

If you plan to hire a lot before your first priced round and want a large pool early.

If you know you will do multiple SAFE rounds and want room for conversion plus pool refresh.

If you expect to grant meaningful equity to several early engineers or researchers and want clean math.

So, instead of giving you one magic number, I want to give you a method you can use.

Here is the method, explained in plain words.

Step one: decide what “one percent” should look like in shares.

If you authorize 10,000,000 shares and plan to issue about 8,000,000 early (founders plus pool), then 1% is about 80,000 shares on a fully diluted basis. That means a 0.10% grant is about 8,000 shares. Those are nice, round, easy numbers.

If you authorize only 1,000,000 and issue 800,000 early, then 1% is about 8,000 shares and 0.10% is 800 shares. Also workable. But once you get into smaller grants—like 0.03%—you start seeing numbers like 240 shares. That can still be fine. But the smaller the base, the faster you bump into rounding and explanation problems.

Step two: plan your initial issued shares.

Many startups issue something like 6,000,000 to founders out of 10,000,000 authorized, then reserve 2,000,000 for the option pool. That leaves 2,000,000 unused.

Why leave unused shares? Because they are your flexibility. Early advisors, small grants, and paperwork mistakes happen. Also, when you raise money, investors often want a pool increase before the round closes. Having unused authorized shares makes that process smooth.

Step three: stress test the “bucket.”

Imagine three hires, each with meaningful equity. Imagine two advisors. Imagine a pool increase from 10% to 15%. Imagine your SAFEs convert and you do a priced seed. Do you still have room in authorized shares to issue what is needed, or do you end up rushing to amend the charter?

This stress test is the whole game. If the stress test says you will run out, you authorize more at the start. If the stress test says you have way too much, you can choose a smaller number.

Now here is the part founders often miss: if you choose a smaller authorized number, you can always increase it later. That is allowed. The question is not “can I change it?” The question is “will it cause pain at a bad time?”

If you are raising a round, you do not want extra legal steps. If you are onboarding a key hire, you do not want to say, “We’ll grant your equity after we update our charter next month.” The cost is not only money. It is trust and speed.

Speed matters.

And if you are building a deep tech company—robotics, AI systems, new hardware, real research—you already have enough hard problems. Paperwork should not be one of them.

This is also where Tran.vc can help founders. A clean equity setup is important, but it is not your moat. Your moat is your inventions. Your code. Your method. Your unique edge. If you want to build that edge into real assets from day one, you can apply here: https://www.tran.vc/apply-now-form/

Let’s address a very common worry: “If I authorize a lot of shares, will it make investors think I’m not serious?”

No. Investors do not judge you on raw share count. They judge you on whether your documents are clean and your cap table makes sense.

What investors do not like is chaos:

Random founder grants with no vesting

Handshake advisor equity with no paperwork

Option grants promised but not approved

A cap table that does not match legal docs

Old templates with strange terms

Broken IP assignment agreements

Missing invention assignment language

No patent plan even though the tech is defensible

Notice what is missing from that list: “authorized shares are 10 million.”

So, do not overthink the number as a signal. Think of it as a tool.

Now let’s move from concept to numbers. In most standard cases, founders choose one of these ranges:

1,000,000 to 5,000,000 authorized shares: smaller base, still workable, sometimes preferred in certain states or for simpler early setups.

10,000,000 authorized shares: the most common “clean math” setup for Delaware startups.

15,000,000 to 20,000,000 authorized shares: used when founders want extra room for bigger pools, more early hiring, or multiple conversions before a priced round.

I am not going to turn this into a long list of rules. Instead, here is a simple way to decide which bucket you are in:

If you plan to stay tiny for a while and hire slowly, a smaller authorized number can work.

If you plan to hire engineers quickly, grant equity often, and raise within 12–18 months, 10,000,000 is usually easier.

If you know you will do a lot of early equity moves and want maximum flexibility, a bigger number might reduce future amendments.

But there is a hidden tradeoff.

A higher authorized number can increase costs in certain states and can complicate franchise tax if set up poorly. So you do not want to go large without reason. “Because a blog said so” is not a reason.

The best reason is: you have a clear plan for founder issuance, pool, and hiring—and you want room for predictable growth.

Now, one more important concept before we go deeper: par value.

When you authorize shares, you also set a par value. Par value is usually very small, like $0.00001 per share, but it affects the minimum price founders pay for their stock at formation (and some accounting entries). This is one of those topics that founders ignore until they accidentally set something awkward.

If you authorize 10,000,000 shares at $0.00001 par value, the “legal minimum” value of all authorized shares is $100. That is usually fine. If you authorize 100,000,000 shares at $0.0001 par value, now the math changes in ways that can create small but annoying side effects. Not always a problem, but it is the kind of thing you want to choose on purpose.

Again: clean and intentional beats default.

So, in the next section, I’ll walk you through real example setups:

A two-founder company with a standard option pool

A solo founder who will hire fast

A team doing deep tech research with advisors and early lab hires

How SAFEs and conversion impact your share planning

When it is smart to amend your authorized shares later

How investors look at these choices in diligence

And I’ll do it without making it feel like a law textbook.

Also, quick reminder: if you are building robotics, AI, or other serious tech and you want to protect what you are building early, Tran.vc can invest up to $50,000 in in-kind patent and IP work. You can apply any time at https://www.tran.vc/apply-now-form/

Common share setups that stay clean

A simple baseline that works in most cases

A large share count is popular because it makes the math easy to explain and easy to use. That is why many Delaware startups choose 10,000,000 authorized shares at formation. It gives you room for founders, a reasonable option pool, and a few early grants without forcing you to amend your charter right away.

The goal is not to pick the “correct” number for all startups. The goal is to pick a number that keeps your early paperwork smooth. When your paperwork is smooth, you move faster on hiring, closing advisors, and raising capital.

If you are building robotics or AI, speed matters even more. You already have long technical cycles. You do not want “we ran out of shares” to be the reason an offer letter gets delayed.

Why startups rarely issue all authorized shares on day one

Authorized shares are only the size of the bucket. Most startups issue only part of them at formation. The rest stays unused so you can issue shares later without needing extra approvals.

This unused space is not waste. It is flexibility. It is what lets you add an advisor, extend an offer to a key engineer, or expand your pool without a rush legal project.

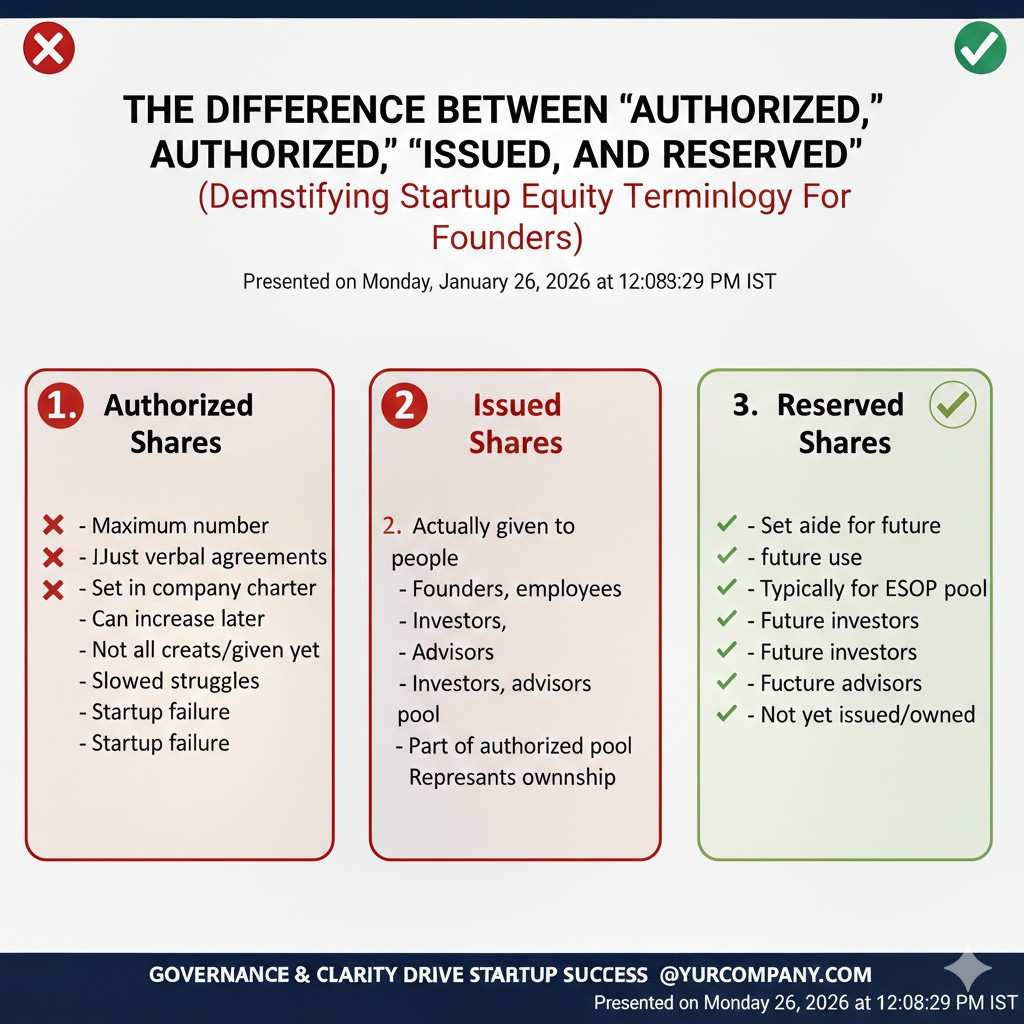

The difference between “authorized,” “issued,” and “reserved”

Authorized shares are the maximum you are allowed to issue. Issued shares are the shares that are already owned by someone. Reserved shares are the shares set aside for options, even though no one owns them yet.

If you confuse these three, you will make bad choices and feel stuck later. If you separate them clearly, share planning becomes simple.

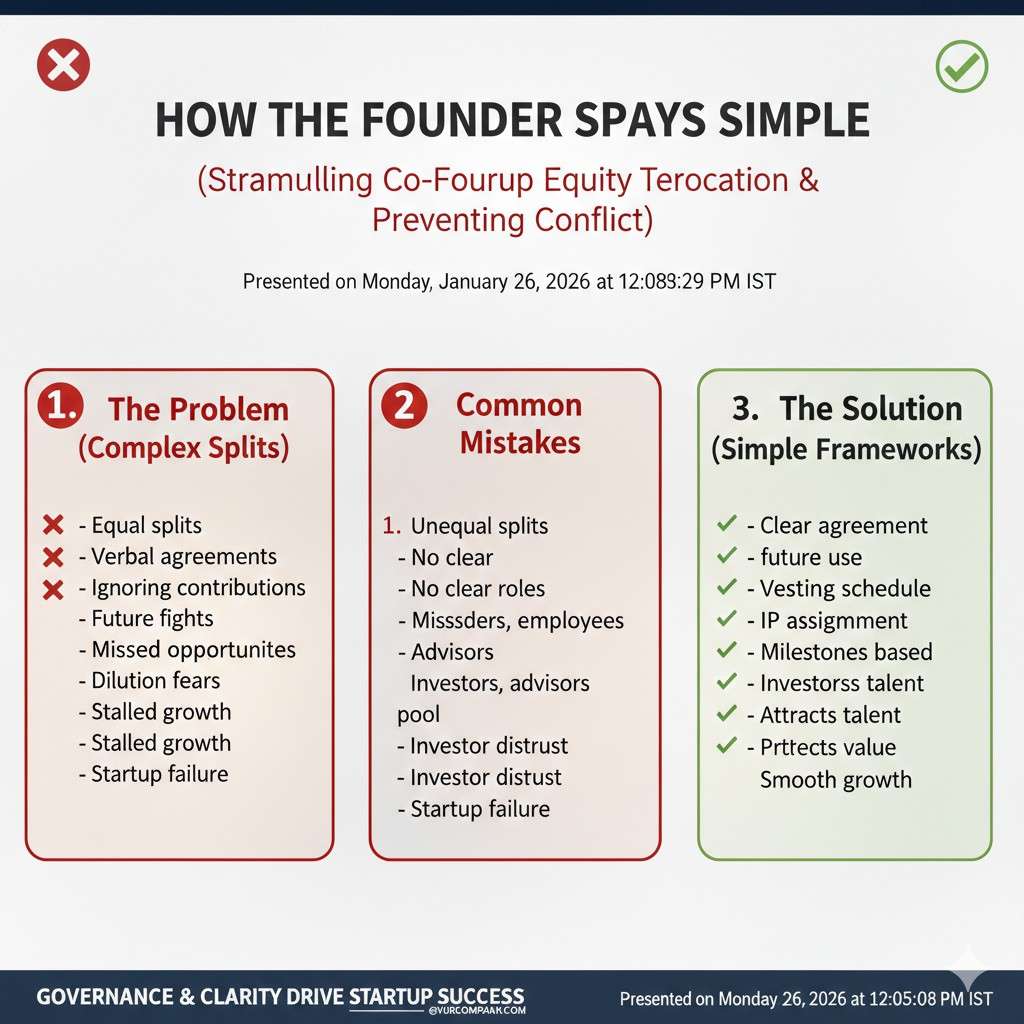

A practical example: two founders and a standard option pool

The most common early split pattern

A very normal early structure is 10,000,000 authorized shares of common stock. Then the company issues 6,000,000 total to the founders and reserves 2,000,000 for an option pool. That leaves 2,000,000 shares unused.

Those numbers are not sacred. They are common because they keep the cap table easy to read. They also give you room to adjust without paperwork when real life happens.

How the founder split stays simple

If two founders split the company 50/50, they might each get 3,000,000 shares in this structure. That looks large, but the percent is what matters. Each still owns half.

This is why a high share count does not reduce ownership by itself. Share count changes the unit size, not the percentage.

Why the unused shares matter more than most founders think

The unused shares are what protect you from surprise events. Early hiring often triggers a pool increase request. Advisors show up when you least expect them. Sometimes you want to make a small grant to close a partnership.

When you have unused authorized shares, those moves stay simple. When you do not, everything turns into a legal task at the worst time.

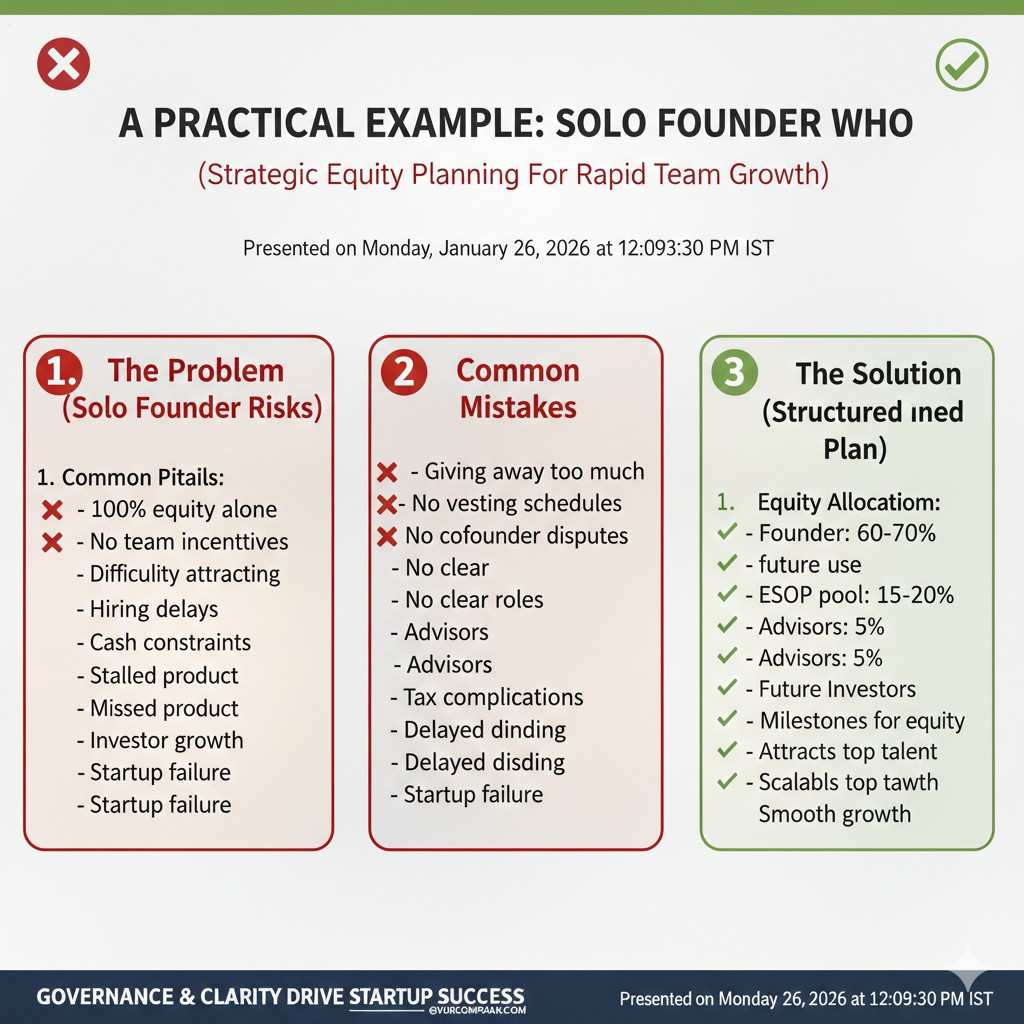

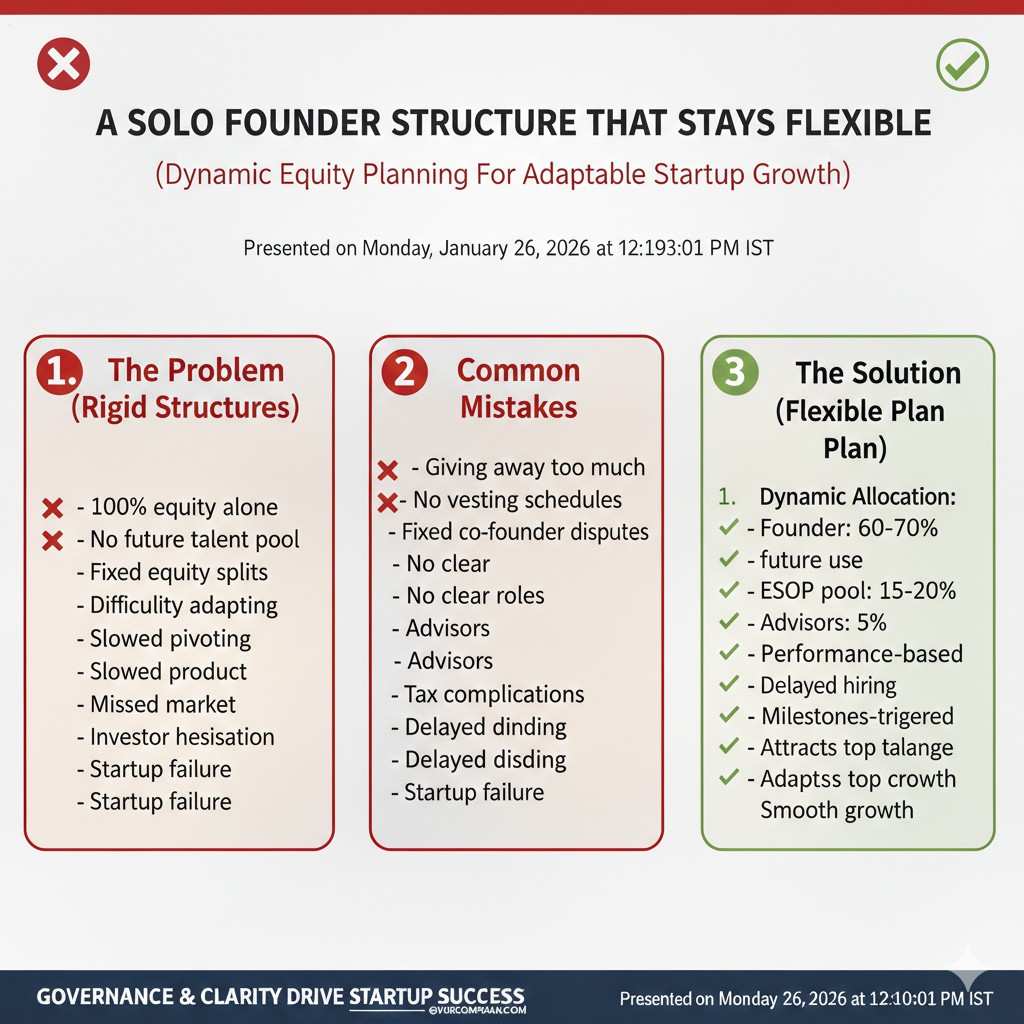

A practical example: solo founder who plans to hire fast

The main risk for solo founders

Solo founders often underestimate how much equity they will grant in year one. Even if you do not plan to hire a large team, the first few hires are usually expensive in equity because they take early risk.

If you plan to hire a senior engineer, a product leader, or a research lead early, you will likely need a healthy option pool. You want to plan for that before you start making offers.

How to think about your first option pool

Many startups reserve somewhere around 10% to 15% for a pool early. The exact percent depends on hiring plans and market conditions, but the logic is the same. Your pool is the fuel for hiring.

If you set the pool too small, you will be renegotiating grants constantly. If you set it too large with no plan, you may create unnecessary dilution conversations with future investors.

A solo founder structure that stays flexible

With 10,000,000 authorized shares, a solo founder might issue something like 7,000,000 to themselves, reserve 2,000,000 for the pool, and keep 1,000,000 unused.

This leaves enough room to make early grants without rushing into a charter amendment. It also keeps the “one percent” math easy to explain to candidates.

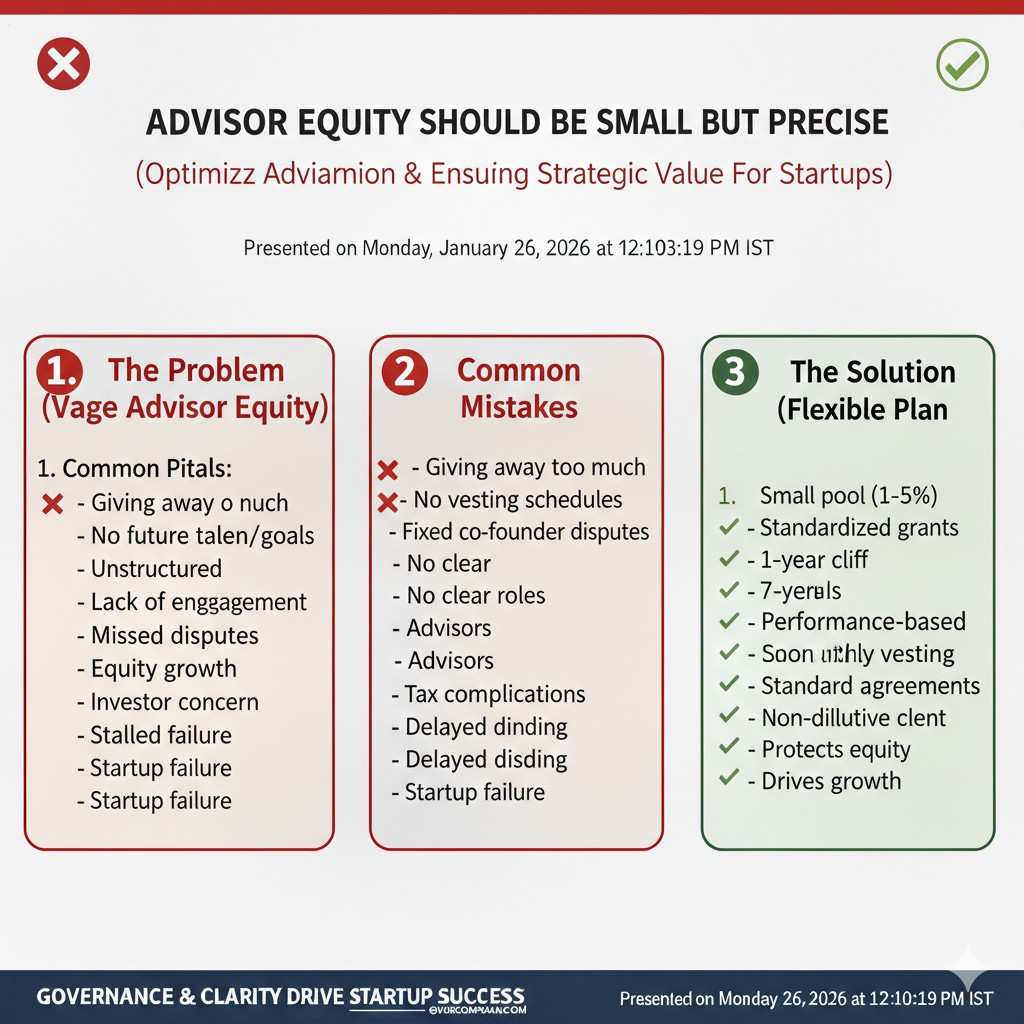

A practical example: deep tech teams with advisors and early research hires

Why deep tech cap tables get messy faster

Deep tech companies often involve research advisors, lab collaborators, and early technical contributors. The people involved can be different from a typical software startup.

That is not bad. But it does mean you can issue equity in more directions early. If you do not plan your authorized shares with this in mind, you can run out faster than expected.

Advisor equity should be small but precise

Advisor grants tend to be small in percent but important in impact. The challenge is not usually the size of the grant. The challenge is the paperwork and the clarity.

A higher share count helps you keep advisor grants clean in share numbers. It prevents awkward rounding and avoids the feeling that you made up the numbers on the spot.

Where Tran.vc fits for deep tech founders

If your edge is real technical invention, your moat is not your pitch deck. It is your IP. This is where Tran.vc is designed to help. We invest up to $50,000 in in-kind patent and IP services so you can protect what matters while you build.

If you want to turn your work into defensible assets early, you can apply any time here: https://www.tran.vc/apply-now-form/

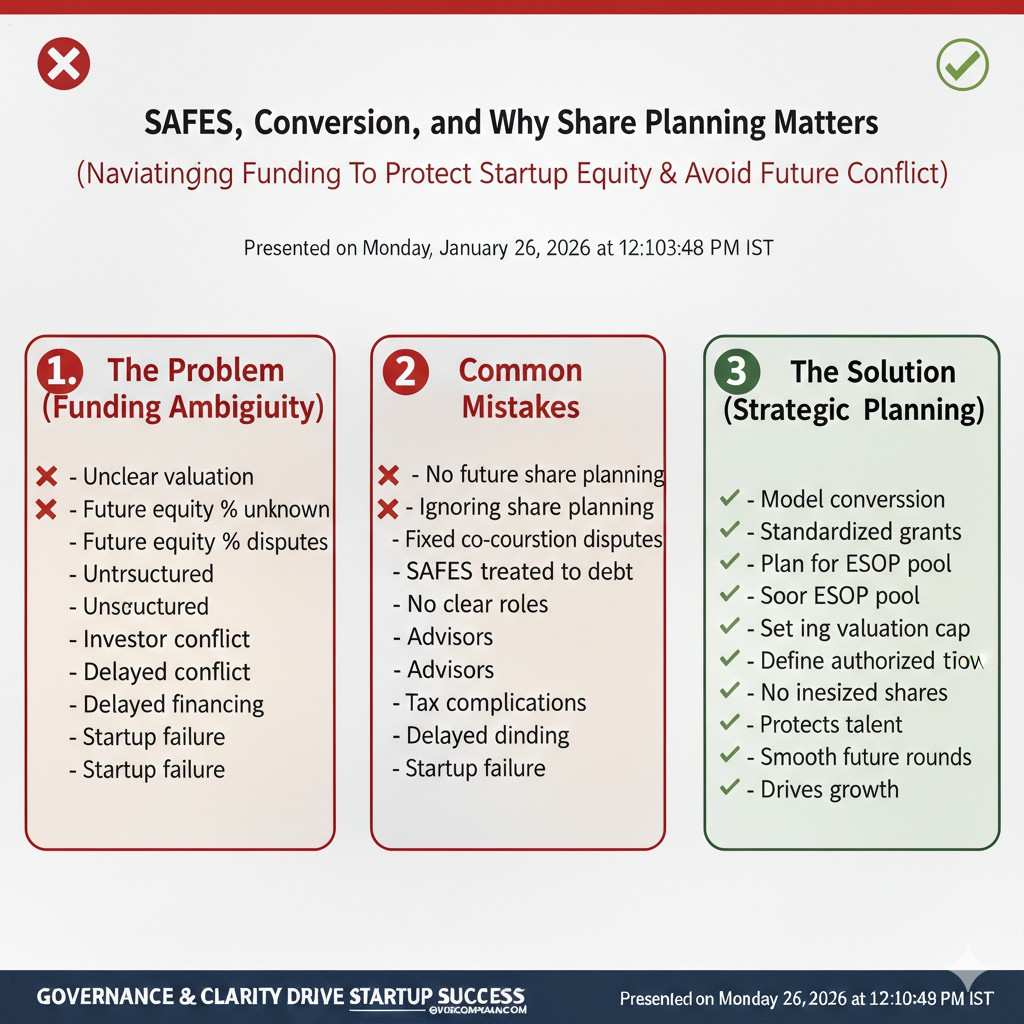

SAFEs, conversion, and why share planning matters

SAFEs do not issue shares right away

A SAFE is a contract today that may convert into shares later. That means your cap table can look simple at first, and then change quickly at conversion.

Founders sometimes forget that conversions can require new shares to be issued. If you do not have enough authorized shares available, you may need to amend your charter right when you are closing a priced round.

The “option pool increase before the round” effect

Investors often ask for the option pool to be topped up before the financing closes. This is common. The reason is simple: they want the company to have hiring fuel after the round without immediately going back to expand the pool.

If you do not plan for a pool increase, you can get squeezed. The squeeze shows up as legal work, delays, and last-minute cap table stress.

A clean way to avoid last-minute share shortages

The simple approach is to keep meaningful unused authorized shares available. That way, when your SAFEs convert and your pool is adjusted, you are not scrambling to change your charter.

This does not mean you should authorize a wild number. It means you should plan for the most common financing path for your stage.

When you should increase authorized shares later

Increasing authorized shares is normal

Many startups increase authorized shares at some point. It is not a failure. It is a normal corporate action as the company grows.

The only real question is timing. You want to do it when you are not under pressure, not in the middle of a funding close or a hiring sprint.

Signals you will need an increase soon

If your unused authorized shares are getting low and you still have hiring plans, that is a sign. If you are about to convert SAFEs and add a refreshed pool, that is a sign.

The moment you start making “we will grant this later” promises, you are already in the danger zone. Equity delays create distrust fast.

How to make the process feel painless

The easiest time to increase authorized shares is when you already have your board organized and your stockholder approvals are straightforward. Doing it early keeps it boring.

Boring is good in corporate paperwork. Boring means your energy stays focused on building.

How investors look at authorized shares in diligence

What investors actually care about

Investors care that your cap table is correct, your documents match, and your equity issuances were approved properly. They want to see clean founder vesting, clean option grants, and clear board and stockholder consents.

They do not usually care whether you authorized 5 million or 10 million shares. They care whether your structure creates friction.

What makes investors nervous

Investors get nervous when equity promises were made without approvals. They get nervous when the option pool is unclear, or when the company has issued equity with missing IP assignment terms.

They also get nervous when your company’s technical moat is not protected. If you have valuable inventions but no patent plan, they may worry competitors can copy your work.

Building leverage with IP, not just equity paperwork

Cap table hygiene helps. But deep tech leverage comes from protecting the invention. Tran.vc exists for this exact moment, when you are early and need to build real defensibility without giving up control too soon.

If you want to lock in a serious IP strategy early, apply any time at: https://www.tran.vc/apply-now-form/

A clear recommendation you can use today

If you are a typical Delaware startup at formation

In many standard cases, 10,000,000 authorized shares is a clean and flexible starting point. It supports normal founder issuances, a reasonable option pool, and early grants without rounding problems.

It also makes it easier to speak in clean numbers when you are hiring, because small percentages turn into understandable share counts.

If you are not Delaware or you operate in states with share-based fees

If your state charges fees based on authorized shares, you may prefer a lower number to avoid unnecessary cost. This is not about being cheap. It is about avoiding a recurring cost that does not help you build.

In that case, the method stays the same. You still plan for founders, pool, and early grants. You just choose a base count that fits your state’s fee structure.

If you are a deep tech company that will grant equity in more directions

If you expect early advisors, research partners, or a larger early team, you may want more room than the “standard software startup.” You do not need extreme numbers, but you should leave enough unused authorized shares to avoid forced amendments.

This is especially true if you expect multiple SAFEs before a priced round and want to keep everything smooth at conversion.