Most founders think incorporation is a quick checkbox: pick a name, file a form, open a bank account, move on.

But to a VC, your incorporation choices are not “admin.” They are a signal of how you think, how you manage risk, and whether your company can safely take money.

And here’s the hard truth: some incorporation mistakes do not look like small mistakes. They look like hidden landmines. Even if your product is strong, these landmines can slow the deal, shrink the check, or kill the round.

This article will show you the incorporation mistakes that scare off VCs, why they matter, and how to fix them in a clean, calm way—before you are in a rushed fundraising sprint. I’ll keep it simple, practical, and focused on what investors actually worry about.

If you want Tran.vc to help you build a strong IP foundation while you set up your company the right way, you can apply anytime here: https://www.tran.vc/apply-now-form/

The first thing VCs look for: “Can we invest safely?”

When a VC invests, they are buying a slice of your company. But they are also buying peace of mind.

They want to know:

- the company owns its tech

- the cap table makes sense

- stock was issued correctly

- there are no surprise claims from past employers, contractors, or co-founders

- the company can issue new shares without drama

- the company can sign customer deals without legal fog

When your incorporation is messy, the investor has to assume you will be messy later too. That is not personal. It is pattern matching.

VCs have seen the same disasters again and again. So when they see the early warning signs, they do not “wait and see.” They protect their fund.

Mistake #1: Incorporating in the wrong place “because it was easy”

This is one of the most common early mistakes. A founder picks a country, state, or structure because:

- it was the cheapest

- their friend did it

- an online tool suggested it

- it felt faster

- they wanted to avoid paperwork

Then they raise money and learn: investors do not like it.

Here’s why it scares VCs.

VCs want clean, standard structures. They want a setup they have funded many times. They want legal terms that are known and predictable. They do not want to invent new process for a one-off structure.

A typical example: a startup targeting US customers incorporates outside the US to “save costs,” then tries to raise a US seed round. The investor sees extra tax complexity, cross-border paperwork, and possible trouble moving IP. Even if none of that becomes a real problem, it still increases time and risk.

Time and risk are the enemies of deals.

You may think, “But we can flip later.” Yes, sometimes you can. But VCs often think: If you did not get the basics right, what else is wrong?

What to do instead:

If you plan to raise VC money in the US, the most standard path is a Delaware C-Corp. It is not perfect, but it is familiar, and “familiar” is a big deal in venture.

If you are not in the US and you are not sure yet, you still want to plan for the most likely investor base. If your buyers and future investors will be US-based, it is wise to align early. If they will be in another region, align there.

The key is not “Delaware is best.” The key is “choose the structure your future capital expects.”

If you already incorporated somewhere else, do not panic. This is fixable. But fix it early, not the week you get a term sheet. The later you wait, the harder it becomes.

And if you want help thinking through the right path—especially if IP is a core asset—you can apply to Tran.vc anytime: https://www.tran.vc/apply-now-form/

Mistake #2: Using an LLC when you plan to raise VC

An LLC can be great for a small business. It can be fine for a consulting shop. It can also be fine for a company that will never raise venture capital.

But many VCs avoid LLCs for a simple reason: taxes and fund rules.

Many VC funds have investors like universities, endowments, and pension funds. Those investors often do not want “pass-through” tax exposure. LLC income can “flow through” to members. A VC does not want to hand their LPs extra tax forms and tax risk.

So even if your LLC is working well, you may hear: “Convert to a C-Corp, then we can proceed.”

That conversion may not be hard, but it is one more step, one more legal bill, and one more thing that can go wrong.

The deeper issue is this: when you raise venture, you want to remove friction. Every extra step is a chance for delay.

A founder will say, “But we can convert quickly.” Sometimes yes. But if you have:

- multiple members

- early revenue

- foreign owners

- messy bookkeeping

- unclear IP ownership

then “quickly” becomes “not quickly.”

What to do instead:

If you are building a robotics, AI, or deep tech startup and you think venture funding is likely, start as a C-Corp. It is simply the standard for VC-backed companies.

If you are already an LLC, the best move is to talk to a startup lawyer and map the cleanest conversion plan before fundraising.

Also, if your core value is your invention—your models, your hardware design, your data pipelines, your control system—treat that as an asset that must sit inside the right company shell. Do not let your IP float around outside the entity that investors will fund.

Tran.vc is built for founders like this. We invest up to $50,000 in in-kind patent and IP services, so you can turn your tech into assets investors respect. Apply anytime: https://www.tran.vc/apply-now-form/

Mistake #3: Not papering the founder relationship early

This one looks small until it explodes.

Two friends start building. They trust each other. They do not want to “make it weird.” So they skip the hard talk:

- Who owns what percent?

- What happens if someone leaves?

- Who decides what?

- What if one person stops working?

Then six months later, a VC asks for the cap table and founder docs.

Now the company has a problem.

VCs want to see that founders have signed proper stock purchase agreements, that shares vest over time, and that there is a clear story if someone leaves. They do not want to invest into a situation where a non-working founder owns a big chunk forever.

If you do not have vesting, investors worry you will have “dead equity.” Dead equity is a company killer. It makes it harder to hire, harder to motivate the team, and harder to raise later rounds.

It also signals something else: founders might avoid hard conversations. Investors fear that pattern because startups are made of hard conversations.

What to do instead:

Handle founder equity the right way from day one.

In simple terms: vesting protects the company. It does not punish anyone. It says: “You earn your shares by staying and building.”

The common structure is four-year vesting with a one-year cliff. That means if a founder leaves before one year, they do not keep unearned shares. After that, shares vest monthly or quarterly.

Also, clarify roles and decision rights early. This does not require a long document. It requires clear thinking and clean signatures.

If you already split shares with no vesting, you can still fix it. But it requires careful handling because you are changing something people already “feel” they own. Again: fix it before fundraising, not during it.

Mistake #4: Issuing stock incorrectly (or not issuing it at all)

You would be shocked how many “incorporated” startups never actually issued founder stock properly.

They filed the company. They started building. They even put “CEO” on LinkedIn. But the paperwork for stock issuance was skipped, delayed, or done wrong.

This scares VCs for one reason: if ownership is unclear, everything is unclear.

Common messy situations include:

- founders never bought shares, so they do not legally own them

- stock was promised in emails but not documented

- shares were issued without board approval

- the company did not file required tax forms on time

- the price per share was set in a way that creates tax trouble later

When an investor sees this, they think: “If we invest, are we really buying what we think we are buying?”

What to do instead:

Make sure founder stock is issued with:

- board consent

- signed stock purchase agreements

- vesting terms

- the right early tax filings

One particular trap: the 83(b) election in the US. If you miss it, you can create painful tax outcomes later. Many founders do not know it exists until it is too late.

I am not giving legal advice here, but the practical advice is: treat stock issuance as a real event with real steps. Do not treat it like a “later” task.

If you are not sure whether you did this right, ask your startup lawyer to do a quick “corporate hygiene” check. It is much cheaper before a priced round than during one.

Mistake #5: Mixing personal and company money

Early on, money feels informal. A founder pays for cloud credits on a personal card. Someone buys parts for the robot with their own money. Another founder wires money from their personal account “just to cover payroll.”

This can be normal early behavior. But if it stays messy, it becomes scary.

Investors want to see clean separation:

- company has its own bank account

- expenses are tracked

- reimbursements are documented

- founder loans are documented

- revenue is booked properly

Why? Because messy money can hide legal and tax risk. It can also hide real cap table risk. For example, if a founder thinks they “put in more money,” they may later demand extra equity. That can blow up a round.

What to do instead:

Open a company bank account as soon as you incorporate. Use it. Track spending. If founders pay for something personally, reimburse them and keep receipts.

If a founder is lending money, write it down as a simple promissory note. If a founder is investing, document it clearly.

Clean books are not just for accountants. They help you raise money faster.

Mistake #6: Hiring contractors without clear IP assignment

This one is a silent deal killer, especially for AI, robotics, and deep tech.

Founders hire a contractor to help with:

- model training

- data labeling

- firmware

- CAD design

- UX

- app development

They pay them. Work gets done. Everyone moves on.

Then a VC asks: “Do you have signed invention assignment agreements?”

If the answer is “no,” the VC hears: “You might not own your own product.”

That is terrifying for an investor.

Even if you think you own it because you paid for it, in many places payment does not automatically transfer IP rights. You need clear agreements.

What to do instead:

Every contractor should sign an agreement that says:

- work product belongs to the company

- any inventions are assigned to the company

- they will help sign future paperwork if needed

Also, if contractors used open source or third-party assets, track it. Investors do not expect perfection, but they want honesty and awareness.

If you already used contractors without these agreements, fix it now. Ask them to sign proper assignment documents. Most will, if the relationship is good. The longer you wait, the harder it gets.

And if your tech is patentable, you also want to align patents with correct inventors and correct assignment. This is exactly where founders get stuck.

Tran.vc helps early founders build clean IP foundations and patent strategy from day one. You can apply anytime: https://www.tran.vc/apply-now-form/

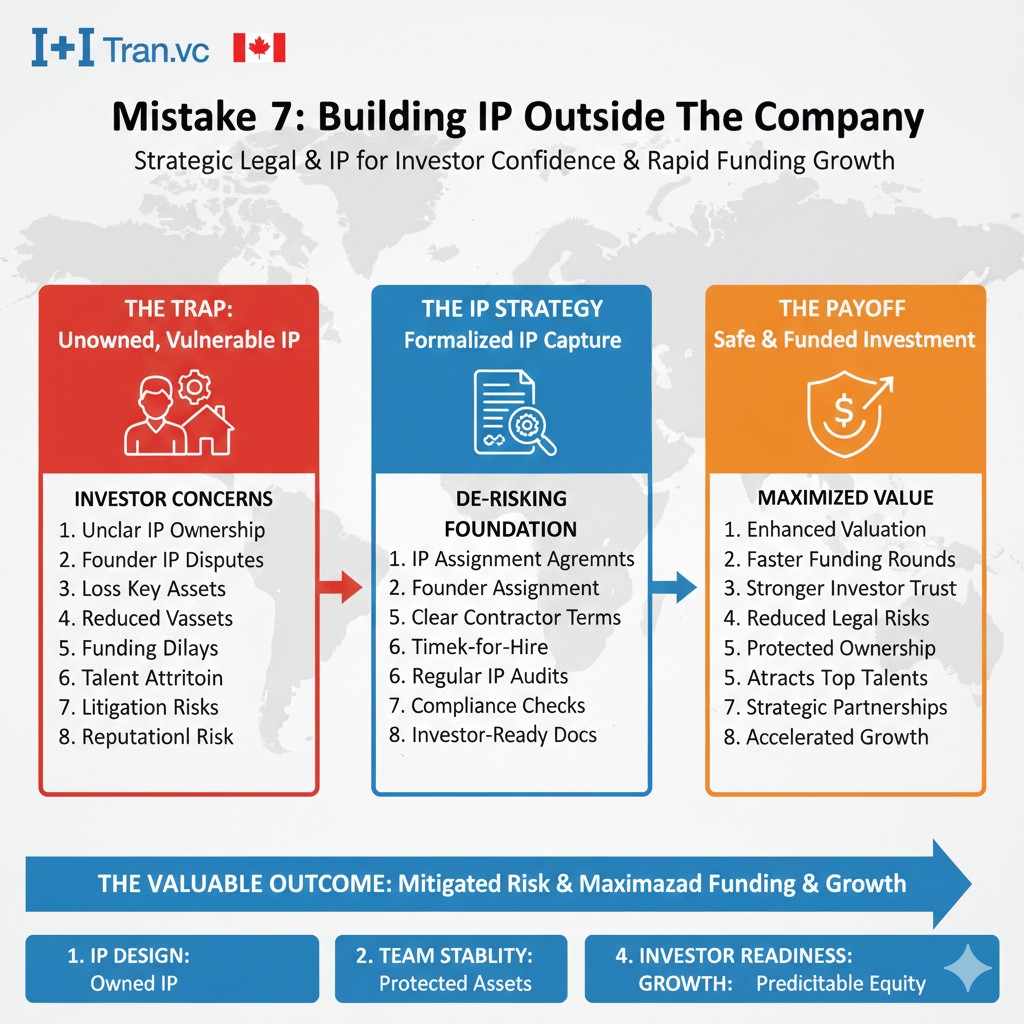

Mistake #7: Building IP outside the company

This happens in many ways:

- you built the first version before you incorporated

- you wrote core code in a personal repo

- the lab work was done under a university agreement

- your co-founder built key parts while employed elsewhere

- you used your old employer’s equipment or time

- you and a friend “owned it together” before forming the entity

To you, it might feel like the same thing: “We made it, so it’s ours.”

To a VC, it is not that simple. They are thinking about claims:

- Could your employer claim the invention?

- Could a university claim it under a sponsored research rule?

- Could a past collaborator claim co-ownership?

- Could a founder who leaves claim they personally own a key part?

If the company does not clearly own the IP, investors worry the whole business can be challenged later.

What to do instead:

Do a simple IP inventory:

- What did we build before incorporation?

- Who worked on it?

- Under what employment or school terms?

- What parts are truly core to the product?

Then assign what should be assigned into the company, with clear documents.

If there are employer issues, handle them with counsel. Sometimes the fix is simple. Sometimes you need a clean rewrite of certain components. But either way, you want to know early.

Mistake #8: Promising equity without documents

A founder tells an early helper: “We’ll give you 2% when we raise.”

Or: “You can have 0.5% for helping with sales.”

Or: “We’ll figure it out later.”

These promises feel harmless. But they create expectations. And expectations become conflict.

Investors hate unclear equity promises because they can turn into disputes right when the company is trying to raise.

They also hate it because it suggests weak process. A startup can move fast without being sloppy.

What to do instead:

If you want to give equity, do it through a clear tool:

- a proper option grant plan

- a written advisor agreement

- clear vesting terms

- clear board approval

If you are not ready, do not promise equity. Offer cash if you can. Or offer a small, written advisor arrangement. But avoid “handshake equity.”

Mistake #9: Not setting up an option pool early (or setting it up the wrong way)

When VCs invest, they often expect the company to have room to hire. That means an option pool.

If you have no pool, you may be forced to create one as part of the round. If it is created “pre-money,” it effectively dilutes founders before the investor’s money comes in. Many founders are surprised by this.

The mistake that scares VCs is not “no option pool.” It is “the founders do not understand dilution, and they will panic later.”

Deals fall apart when founders feel tricked. Even if the investor is being standard, founder shock creates tension.

What to do instead:

Learn the basics of dilution early. Model your cap table with a few simple scenarios:

- hiring 5 key roles

- raising a seed round

- raising a Series A later

You do not need to become a finance expert. You need to understand the shape of the future.

A good startup lawyer can help you set the pool at the right stage. And you can also ask investors what they typically expect.

Mistake #10: Forgetting basic governance and records

Investors will ask for:

- charter and bylaws

- board consents

- stock ledger

- option plan docs

- signed agreements

If you do not have them, the investor starts to wonder what else is missing.

This is not about being “corporate.” It is about being investable.

What to do instead:

Keep a simple, organized folder with signed PDFs. Use a cap table tool if you can. Store board consents. Document major actions. It is boring, but it saves your round.

Mistake #1: Incorporating in the wrong place “because it was easy”

Why investors care about your state or country

A VC is not only judging your product. They are also judging how hard it will be to invest in you. If your company is set up in a place they do not often fund, they may expect extra legal work, extra tax work, and extra delays.

That extra work does not always kill a deal, but it often slows it down. Slower deals create more chances for things to break. In venture, speed matters because markets move, teams change, and terms can shift fast.

The hidden cost of “we will flip later”

Many founders assume they can do a simple “flip” into a new structure right before raising. Sometimes that works. But it can also turn into a long clean-up project, especially if you already have revenue, contractors, or early investors.

The bigger risk is trust. If an investor sees a major early choice that created avoidable friction, they may wonder what other choices were made the same way. They will not say this out loud, but it shows up as slower replies and more caution.

How to choose a structure that matches your funding plan

If you expect US venture funding, the standard path is a Delaware C-Corp because it is familiar to lawyers and investors. If you plan to raise mostly in another region, you want the structure that funds in that region understand best.

The goal is simple: reduce surprise. When investors see a familiar setup, they can focus on your team and traction instead of paperwork. That alone can change the speed of your round.

What to do if you already incorporated in a non-standard place

This is fixable, but do it early. When a term sheet arrives, you want the only “work” to be the deal terms, not a major company rebuild. A clean plan with the right counsel can often solve this without drama, but waiting almost always makes it more painful.

If your moat depends on invention, also think about where your IP lives. Tran.vc helps founders make their tech defensible through patents and strong IP structure. You can apply anytime: https://www.tran.vc/apply-now-form/

Mistake #2: Using an LLC when you plan to raise VC

Why many VC funds avoid LLCs

Many VC funds have their own rules and limits. They also have investors behind them, like endowments and pension funds, that want simple tax reporting. LLCs can create pass-through tax issues that these groups do not want to deal with.

Even if your LLC is well run, a VC may still say no because it does not fit their fund structure. That can feel unfair, but it is common. The result is you being asked to convert before they can move forward.