Liquidation preference sounds like a hard, legal phrase. In real life, it is simple: it is the rule that decides who gets paid first if your company sells or shuts down. That one rule can either protect you—or quietly trap you.

If you are a founder, you do not want to learn this rule at the exit. You want to set it up early, in a way that is fair, clear, and founder-friendly, so you do not lose years of work in one line of a term sheet.

Tran.vc helps technical founders build leverage early, before big money shows up. One strong way to do that is to build real assets—like patents and strong IP—so you can negotiate better terms later. If you want support building your IP moat while staying in control early, you can apply anytime at https://www.tran.vc/apply-now-form/.

Liquidation Preferences: The Founder-Friendly Setup

Why this matters more than most founders think

Liquidation preference is one of those terms that sounds like legal housekeeping. Many founders treat it like a small footnote, something the lawyers will “handle.” That is a costly mistake. This single clause often decides whether your team walks away proud after a sale, or feels shocked and empty even after years of building.

A liquidation preference is not about “if you win, you win.” It is about what happens when the outcome is messy, medium, or just not perfect. Most exits are not blockbuster outcomes. Many are decent sales, early acquisitions, or hard pivots that end with a soft landing. In those common scenarios, liquidation preference becomes the rulebook that decides who gets paid first and how much.

If you are building in AI, robotics, or deep tech, your path can be longer. Hardware cycles, safety testing, and customer trust can take time. That means you may raise more rounds, and more rounds mean more preference stacking risk. You should treat this topic like a core founder skill, not a legal detail.

Tran.vc works with technical founders early, when you still have room to shape your future leverage. If you want to build strong IP and patents that help you raise on better terms later, you can apply anytime at https://www.tran.vc/apply-now-form/.

The founder-friendly goal in one sentence

A founder-friendly liquidation setup is not about “beating investors.” It is about setting clear, fair rules so that investors get a reasonable downside shield, and founders still have a real path to earn meaningful outcomes in normal exits.

When the setup is fair, everyone stays aligned. Investors want you to take smart risks, hire well, and build long-term value. You want to feel that a decent exit still rewards your time, your stress, and your team’s sacrifice. The right preference structure keeps both of those truths alive.

A founder-friendly setup also reduces drama later. When terms are clean, future investors worry less, acquisitions go smoother, and your board discussions are less tense. You end up spending time on product and customers instead of fighting math.

What we will cover in this guide

This article will help you understand liquidation preference in plain words, without hiding behind finance talk. You will learn the common versions of preference, what each version does to your payout, and where founders often get tricked without noticing.

You will also learn how to negotiate in a way that keeps trust intact. The best founders do not start fights. They ask sharp questions and set clean boundaries early. That is what this guide is designed to help you do.

Finally, we will connect this to a bigger point: leverage. The best way to get founder-friendly terms is to be less desperate. Strong IP can make you less desperate, because it makes your company harder to copy and easier to believe in. If you want Tran.vc to help you build that moat through in-kind patent and IP work, apply anytime at https://www.tran.vc/apply-now-form/.

The plain-English definition of liquidation preference

The simple rule: who gets paid first

Liquidation preference is a promise written into the investment deal. It says that if the company has a “liquidation event,” the investor gets paid before common shareholders. A liquidation event usually includes a sale, a merger, or a shutdown.

Think of it like a line at a checkout counter. Investors with preference stand in front. Founders and employees holding common stock stand behind. If the money runs out before it reaches the back of the line, the people behind may get little or nothing.

This is not automatically evil. Investors take risk, and preference is meant to protect them if things go poorly. The problem starts when the preference is too big, too complex, or paired with extra rights that let investors get paid twice.

Why it exists in the first place

Early-stage investing is risky. Many startups fail. Investors use liquidation preference to reduce the impact of losses, especially when a company sells for less than expected. It is a form of downside protection, like a seatbelt.

A reasonable seatbelt makes sense. But founders sometimes sign a deal where the seatbelt becomes a cage. That happens when preference terms turn a normal exit into a founder-zero outcome, even though the company created real value.

A fair system recognizes that both sides are taking risk. Investors risk money. Founders risk time, career, reputation, and health. The best deals protect investors without removing founder incentives.

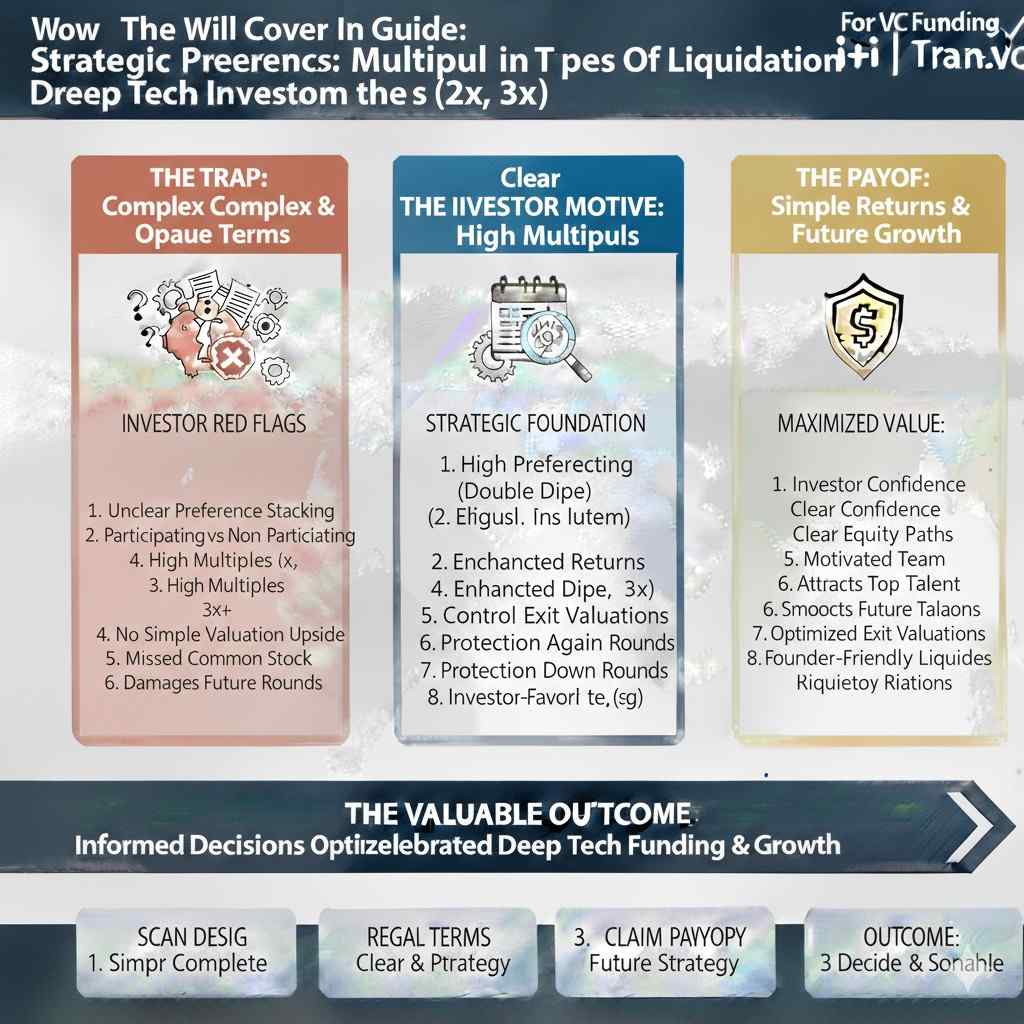

The key word most founders miss: “preference stack”

The first time you raise a priced round, you may take a standard 1x liquidation preference and move on. The danger is that this clause can stack across rounds. If you raise multiple rounds with preference, the total “first-pay” amount can become huge.

This is why founders should not look at preference in isolation. You must look at how it will behave after the next round, and the round after that. Deep tech founders are especially exposed, because their capital needs may be higher, and their timeline may be longer.

A clean structure early can save you later. So can strong IP. When you have patents and a clear IP story, you can often push for cleaner terms because investors view your downside as less scary. If you want help building that foundation, apply anytime at https://www.tran.vc/apply-now-form/.

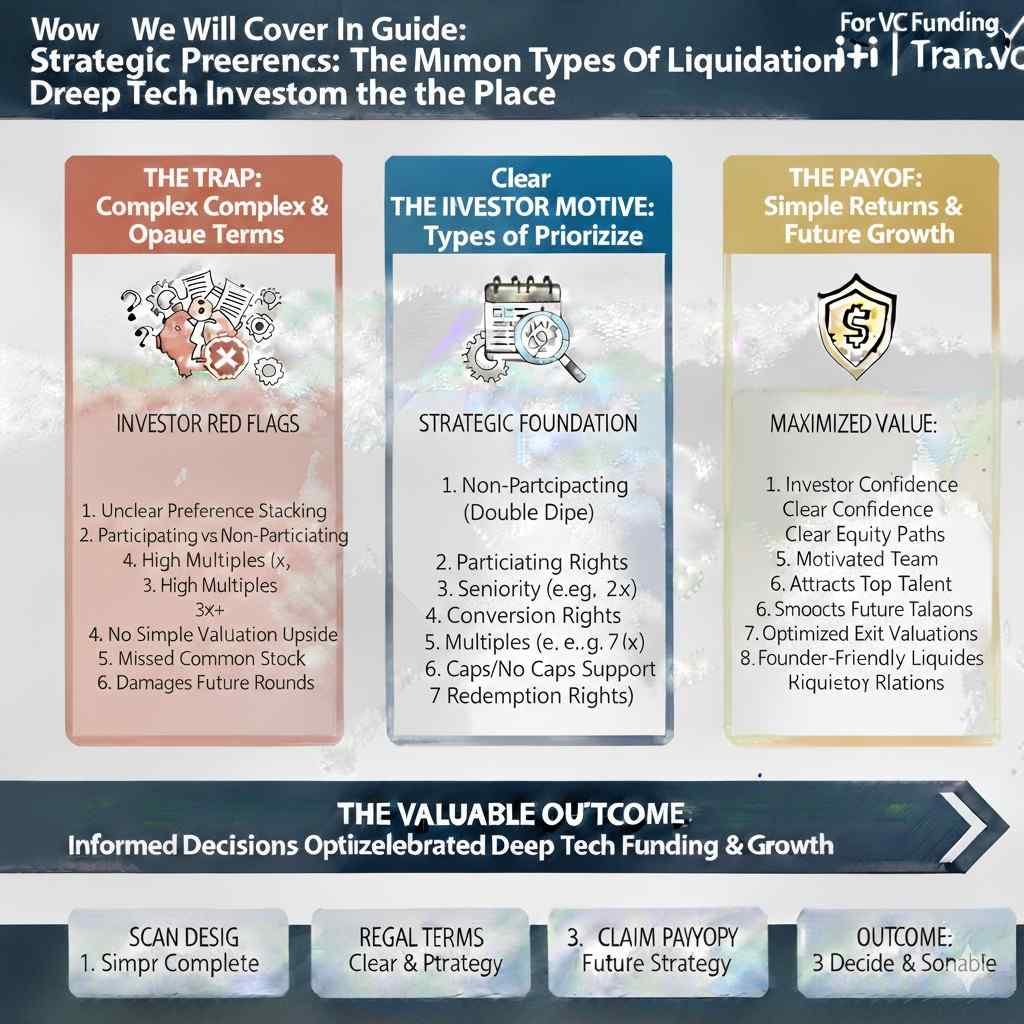

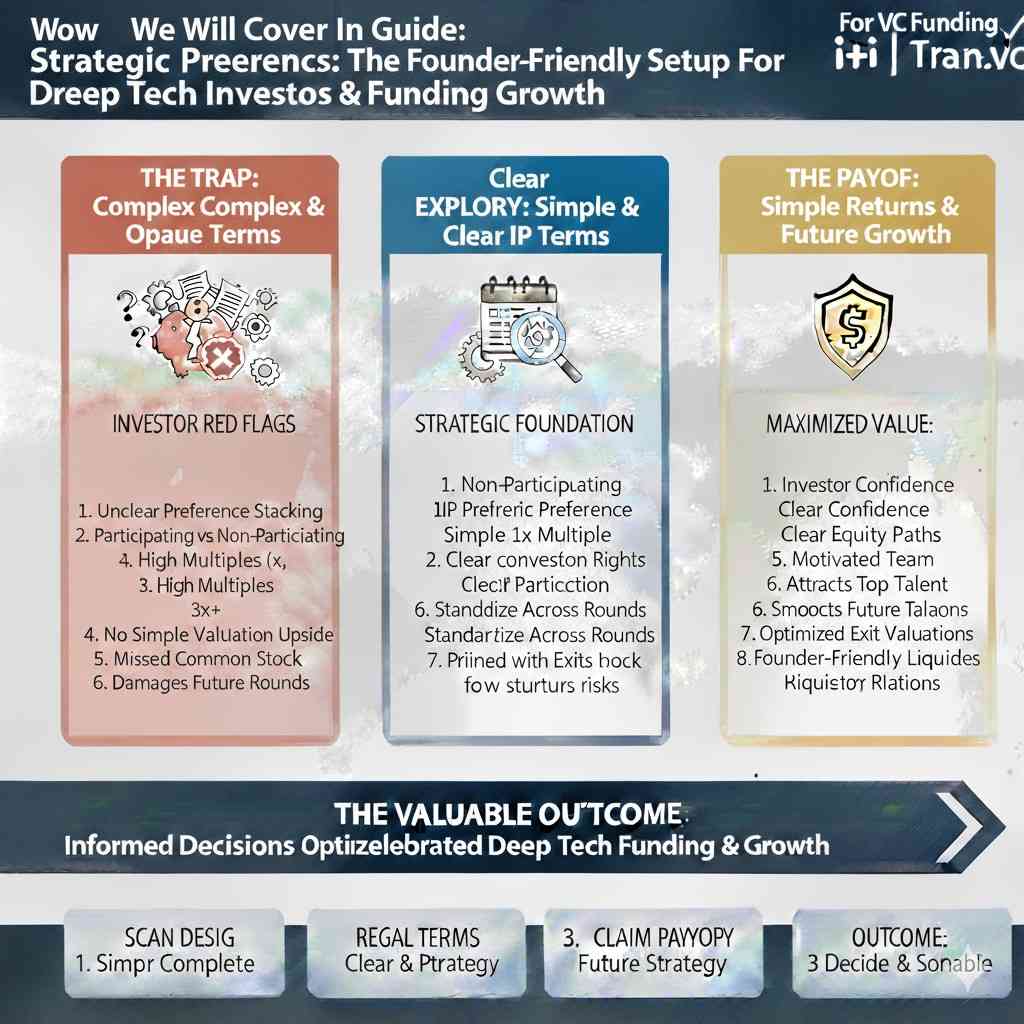

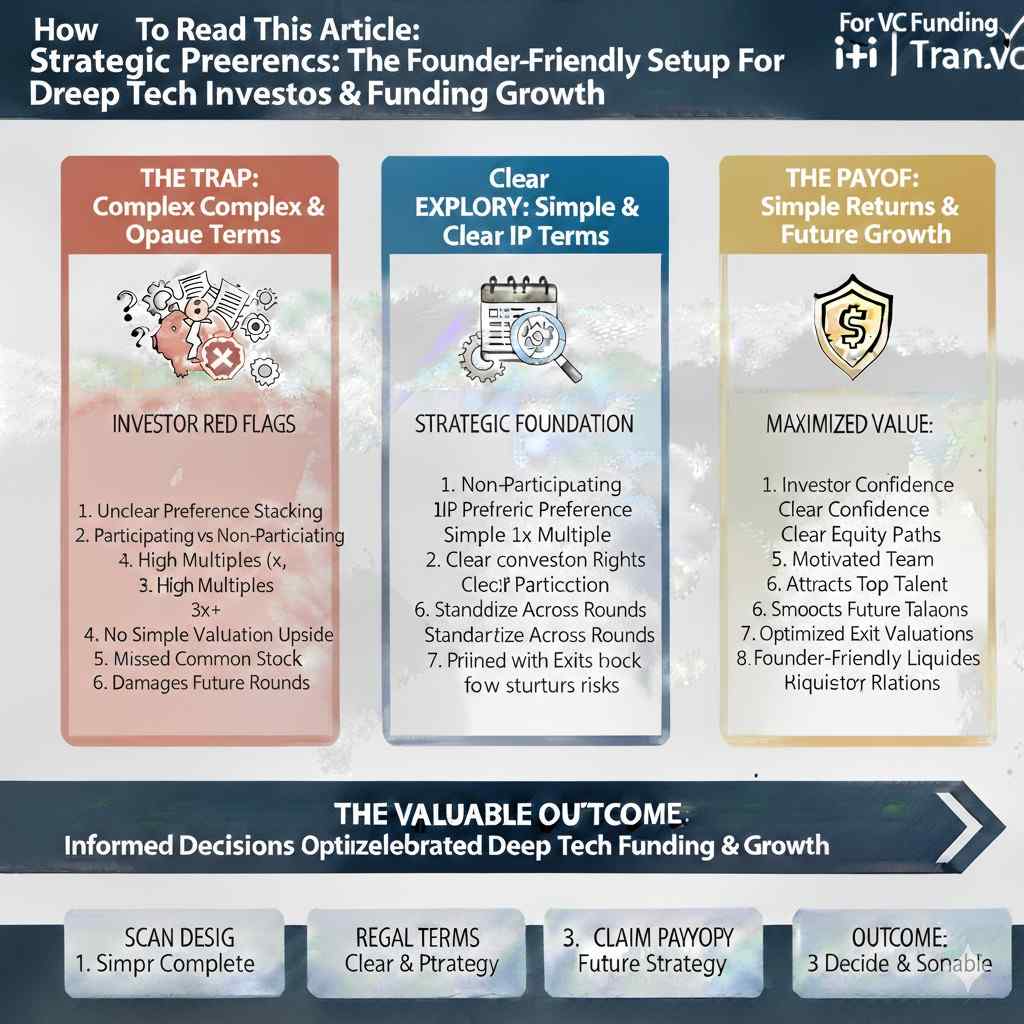

The most common types of liquidation preference

The baseline: 1x non-participating

This is the most founder-friendly version that is still widely accepted. “1x” means the investor gets an amount equal to what they invested, before common shareholders get anything. “Non-participating” means the investor must choose one path: either take their 1x back, or convert to common and take their percentage like everyone else.

This is fair because it creates a simple choice. If the exit is small, the investor takes their money back first. If the exit is big, they convert and share in the upside. They do not get to do both at once.

In many healthy seed and Series A deals, 1x non-participating is considered clean and standard. It is also easy to explain to future investors and potential acquirers. Clean terms reduce friction later, and friction kills deals.

The tricky one: participating preference

Participating preference is where founders often get surprised. It means the investor gets their preference amount first, and then also participates again in the remaining proceeds based on their ownership. This is why people call it “double dip.”

In a moderate exit, participating preference can pull a lot of money toward investors, even when founders and employees did most of the heavy lifting. It can turn what looks like a decent outcome into something that feels unfair.

Some investors justify participating preference by saying the risk is high. Sometimes they offer it with a “cap,” meaning the double dip stops after they reach a certain return. A cap is better than uncapped participation, but it can still be painful. The key is understanding the math before you sign.

The pressure move: multiple liquidation preference (2x, 3x)

A “2x” preference means the investor gets two times what they invested before common sees anything. A “3x” means three times. This is a strong downside shield for the investor, and it can crush founder outcomes in many realistic exit ranges.

Multiples sometimes appear in distressed situations, or in deals where the company has very weak leverage. Founders accept them when they feel they have no other path. This is why your job is to build leverage before you need the money.

If you can show defensible IP, clear differentiation, and real technical barriers, you can often avoid these harsh terms. Tran.vc’s model is designed to help you build that defensibility early through in-kind patent and IP services. You can apply anytime at https://www.tran.vc/apply-now-form/.

The quiet risk: seniority and stacking

Even with 1x non-participating, seniority matters. Seniority answers a basic question: when there are multiple rounds, who is first in line? “Senior” means paid first. “Pari passu” means they share the preference payout together.

If each new round is senior to the last, the stack becomes heavy. In a mid-range exit, later investors may take most of the proceeds, and earlier investors and common may get squeezed. This can make earlier investors unhappy and can also distort board decisions.

Pari passu structures can reduce these conflicts, because rounds share the payout rather than pushing earlier money to the back of the line. It is not always possible, but it is worth understanding because it can shape your long-term exit reality.

How the math really works in real exits

A simple story with simple numbers

Imagine an investor puts in $5 million at a 1x non-participating preference. Later, the company sells for $6 million. Under 1x non-participating, the investor can take their $5 million first, leaving $1 million for everyone else.

If the investor owns, say, 25% of the company, they could also choose to convert to common and take 25% of $6 million, which is $1.5 million. In this case, the investor would not convert because the preference payout is larger. They take the $5 million.

Notice what happened here. A $6 million exit might sound like a win from the outside. But it can still be a low outcome for founders if preference eats most of the proceeds. That is not a rare situation. It is one of the most common situations.

What changes under participating preference

Now imagine the same $5 million investment, but it is 1x participating. If the company sells for $6 million, the investor takes $5 million first. There is $1 million left. Then the investor also takes 25% of the remaining $1 million, which is $250,000.

That extra $250,000 came out of the pool that could have gone to common shareholders. If the exit were $10 million, the investor might take $5 million first, leaving $5 million, and then also take 25% of that $5 million, which is $1.25 million. Total payout becomes $6.25 million.

This is why participating preference is so sensitive. In mid exits, it can change the founder’s lived experience dramatically, even though the term sheet looked “close to standard” in other areas.

Why multiple rounds make everything sharper

Now add a second round. Suppose you raise another $10 million later, also with 1x preference, and that later round is senior. If you sell for $15 million, the later investor may take $10 million first, leaving $5 million. Then the earlier investor may take their $5 million, leaving zero for common.

From the founder’s point of view, that exit may feel like a failure even if the company built something valuable and the team worked hard for years. This is why founders must model outcomes. Not with fancy spreadsheets, but with honest scenarios: small, medium, and big exits.

A founder-friendly setup aims to protect normal outcomes, not just unicorn outcomes. If your terms only reward you in a huge exit, you are taking a dangerous bet with your life and your team’s time.

How investors really think about liquidation preference

What most investors are actually trying to protect

Most good investors are not trying to trick founders. They are trying to manage risk across a portfolio. They know many companies will fail or return little. Liquidation preference helps them survive those losses so they can keep backing new teams.

From their side of the table, preference is a safety net. It gives them comfort that if things go sideways, they are not wiped out completely. When founders understand this, negotiations become calmer and more productive. You stop reacting with fear and start responding with logic.

Problems usually arise when the safety net becomes too thick. When the downside protection is so strong that it removes upside motivation for founders, the deal stops being healthy. Smart investors know this, even if they do not say it out loud.

Why early leverage shapes investor behavior

Investors ask for tougher terms when they feel uncertain. Uncertainty about the market, the tech, the team, or defensibility makes them reach for more control and more downside protection.

This is where leverage quietly matters. When your technology is easy to copy, preference becomes the investor’s shield. When your technology is protected by patents, clear claims, and strong IP strategy, the fear level drops. Lower fear leads to cleaner terms.

This is one reason Tran.vc focuses so heavily on IP early. Patents do not just protect your future product. They change how investors behave today. If you want help building that leverage before a priced round, you can apply anytime at https://www.tran.vc/apply-now-form/.

The emotional side most founders overlook

Founders often assume liquidation preference is only math. It is not. It shapes boardroom dynamics. It shapes how investors feel about exit options. It shapes whether a “good enough” acquisition is supported or blocked.

If investors are deep in the preference stack, they may push for higher-risk moves late in the game, because a modest exit does not change their outcome. That can hurt the company, the team, and even customers.

A founder-friendly setup keeps incentives aligned. It makes reasonable exits feel reasonable for everyone. That alignment reduces pressure, conflict, and second-guessing when hard decisions appear.

The founder-friendly negotiation mindset

Start with clarity, not confrontation

Negotiating liquidation preference does not mean acting defensive or combative. The strongest founders ask calm, clear questions. They seek understanding before pushing back.

A simple question like, “Can we walk through how this plays out in a $30 million exit?” can reveal a lot. If the answer is vague or rushed, that is a signal. Clean deals survive daylight.

Founders who model scenarios together with investors often earn more trust. You are not rejecting the term. You are stress-testing it. That behavior signals maturity, not weakness.

Know what is standard for your stage

At seed and early Series A, 1x non-participating preference is widely seen as founder-friendly and reasonable. Asking for this is not aggressive. It is normal.

Participating preference and multiple preference are less common early unless the deal is unusual. If these terms appear, you should understand why. Is the company distressed? Is the round overpriced? Is there unusual risk?

When you know what is normal, you can ask better questions. You stop feeling grateful for bad terms and start evaluating whether the trade-off is worth it.

Trade, do not just say no

Sometimes an investor will push for stronger preference. Saying “no” without context can stall a deal. A better approach is to trade.

For example, you might accept a standard 1x preference but push back hard on participation. Or you might accept participation only if there is a low, clear cap. Or you might accept seniority but ask for pari passu in later rounds.

These trades work best when you bring value to the table. Strong IP, real traction, and clear technical depth all make it easier to ask for fairness. Tran.vc’s in-kind IP investment is designed to strengthen exactly this position. You can apply anytime at https://www.tran.vc/apply-now-form/.

Red flags founders should never ignore

“It’s standard, don’t worry about it”

This phrase should slow you down, not speed you up. Truly standard terms are easy to explain. They do not require trust. They survive explanation and modeling.

If someone dismisses your questions instead of answering them, that is a process red flag. You are not being difficult. You are being responsible. This is your company and your future.

Founder-friendly investors welcome clarity. They know confusion later causes damage.

Complex language hiding simple outcomes

Sometimes liquidation preference is wrapped in dense legal language. Do not be embarrassed to ask for plain-English explanations. If you cannot explain the outcome to a co-founder in five minutes, the term is too complex.

Complexity usually benefits the party with more lawyers and more experience. Simplicity protects everyone. Clean structures close faster and break less often.

Ask for examples. Ask for numbers. Ask for best case, middle case, and worst case.

Preference that removes motivation

If you look at a realistic exit and realize that founders and employees get very little, that is a serious warning. Incentives matter.

A company where the team has no meaningful upside left becomes fragile. People disengage. Risk-taking changes. Talent leaves. That hurts investors too, even if they do not see it immediately.

Founder-friendly setups preserve motivation across a wide range of outcomes, not just the extreme top end.

How IP strength connects directly to better liquidation terms

Why defensibility lowers investor fear

Investors worry about one thing more than most founders realize: copy risk. If a competitor can replicate your product quickly, the downside risk feels higher. Higher risk leads to harsher terms.

Strong IP reduces that fear. It signals that even if execution is bumpy, the core idea has value and protection. That makes investors more comfortable offering clean liquidation preference terms.

This is especially true in AI, robotics, and deep tech, where the line between research and product can blur. Clear patent strategy draws that line sharply.

IP as negotiation leverage, not just legal protection

Patents are not just for lawsuits. They are negotiation tools. They help you say, “This company is not just code and hope. It is protected work with long-term value.”

When investors believe that, they are more willing to share downside risk instead of pushing it all onto founders. This changes the tone of the entire term sheet, not just liquidation preference.

Tran.vc was built around this idea. Instead of pushing founders to raise fast, they help founders build IP-backed leverage early through in-kind services worth up to $50,000. If that sounds aligned with how you want to build, you can apply anytime at https://www.tran.vc/apply-now-form/.

Founder confidence changes outcomes

Founders who understand their leverage negotiate differently. They are calmer. They are clearer. They are harder to pressure.

When you know your technology is protected, you do not feel rushed into bad terms. You can walk away if needed. That quiet confidence often leads to better offers without confrontation.

Liquidation preference becomes a discussion, not a demand.