A priced round sounds simple: you and an investor agree on a company value, you sell a set percent of shares, and you move on to building.

In real life, it is rarely that clean—especially if you are building from outside the biggest startup hubs, raising across borders, or running a company with deep tech risk (AI, robotics, hardware, biotech-adjacent software). The term sheet may look “standard,” but small wording choices can quietly shape who controls the company, how hard it is to raise again, and whether your best work becomes a defensible asset or an easy copy.

This is why founders often feel shocked later. Not because they were careless. Because priced rounds reward people who understand the hidden levers: how terms stack, how investor rights travel into the next round, how board control shifts, how legal systems differ, how your cap table tells a story, and how your IP either strengthens your hand—or leaves you negotiating from fear.

At Tran.vc, we see the same pattern across global founders: they build something real, they get interest, they rush to “lock the round,” and they treat the priced round like a finish line. It is not. It is the start of a longer game. A priced round is a permanent decision. Every round after it will measure you against it.

So this article is about the common pitfalls we see in priced rounds for global startups—and what to do instead. Not theory. Not big words. Just the places founders get trapped, even when the valuation looks good on paper.

One important note before we go deeper: if you are building something technical, your negotiating power is not only your growth. It is also your ownership of what you built. Clean IP, clear invention records, smart patent choices, and a strong filing plan can change the tone of a priced round. It turns “please fund us” into “here is why this is defensible.” That shift matters. If you want help building that kind of leverage early, you can apply anytime at https://www.tran.vc/apply-now-form/.

Pitfall 1: Treating “valuation” like the only number that matters

The price can look great while the deal is still bad

Many founders focus on the headline valuation because it is the easiest thing to talk about. It feels like the scorecard. But a priced round is a bundle of terms, and the valuation is only one piece of it.

If the other terms are heavy, you may end up giving away more control than you think. You can also block your next round, even if your product is growing. A “high price” does not protect you from that.

Why global startups feel this pain more

If you are raising across borders, investors often worry about what they cannot see. Legal systems, enforcement, hiring, banking, and local market risk all sit in their head. Some investors try to cover that fear with stronger rights.

That is not always evil. It is often just how they manage risk. But if you accept those rights without understanding them, the valuation becomes a distraction. The true cost shows up later.

The quick check you should do before you celebrate

Ask yourself one simple question: “If we execute well for 12 months, will this round make the next round easier or harder?” If you cannot answer that clearly, the valuation number is not doing its job.

This is also where ip can quietly change the whole discussion. If you can show that the core work is protectable and properly owned, the investor’s fear drops. You negotiate from strength, not from pressure. If you want help building that leverage early, you can apply anytime at https://www.tran.vc/apply-now-form/.

Pitfall 2: Signing terms you do not fully understand because they look “standard”

“Market terms” can still hurt you

Founders hear phrases like “this is standard” or “this is what everyone does.” Sometimes that is true. Many terms are common. But a common term used in the wrong place, at the wrong stage, can still be a problem.

A priced round sets the tone for future governance and economics. If you lock in strong investor protections too early, they may become permanent features of your company. Later investors may expect the same or ask for more.

Where misunderstandings happen most

The biggest confusion usually comes from terms that sound harmless. Words like “preference,” “participation,” “protective provisions,” “drag-along,” “pay-to-play,” and “anti-dilution” can look like legal noise.

In reality, those words decide who gets paid first, who can block decisions, and what happens when things do not go perfectly. Founders often learn what they signed only when the next round forces the issue.

What to do instead of guessing

You do not need to become a lawyer. But you do need to be able to explain the business impact in plain words. If you cannot describe a term without reading it out loud, pause the process.

A clean way to pressure-test is to walk through two stories: a great outcome and a tough outcome. If the term shifts power heavily in the tough outcome, you need to decide if that risk is worth it.

Pitfall 3: Building a cap table that scares the next investor

The cap table is not a spreadsheet, it is a signal

Investors read your cap table the way a good engineer reads logs. It tells them what happened before they arrived. If it looks messy, they assume decision-making was messy too.

This is where global startups often get trapped. Early money comes from many places: friends, small angels, local funds, sometimes even service providers. Each one may have different paperwork and different expectations.

The most common cap table issues in priced rounds

One issue is giving away too much too early, which leaves founders with thin ownership. Another is stacking too many small investors who each want updates and rights. A third is unclear option pools, where hiring later becomes hard.

There is also the problem of “shadow terms.” These are promises made in side emails or old documents that never got cleaned up. In the next round, those promises become surprises, and surprises kill deals.

How to keep the cap table simple without slowing down

Think of your cap table like your product roadmap. You want clarity, not chaos. Before you price a round, map out where you want founder ownership to be after this round and after the next one.

If you already have complexity, do not hide it. Clean it. That may mean consolidating small checks, fixing missing signatures, or rewriting early notes into clear equity terms. The goal is to make the next investor feel safe, fast.

Pitfall 4: Accepting control terms that quietly move the company away from the founders

Control is not only about voting shares

Founders think control means owning more than 50%. In venture deals, control usually moves through board seats, veto rights, and approval rules.

You can own a lot of shares and still be unable to make key decisions. You can also lose speed. In early-stage startups, speed is life. Control terms that slow decisions are a hidden tax.

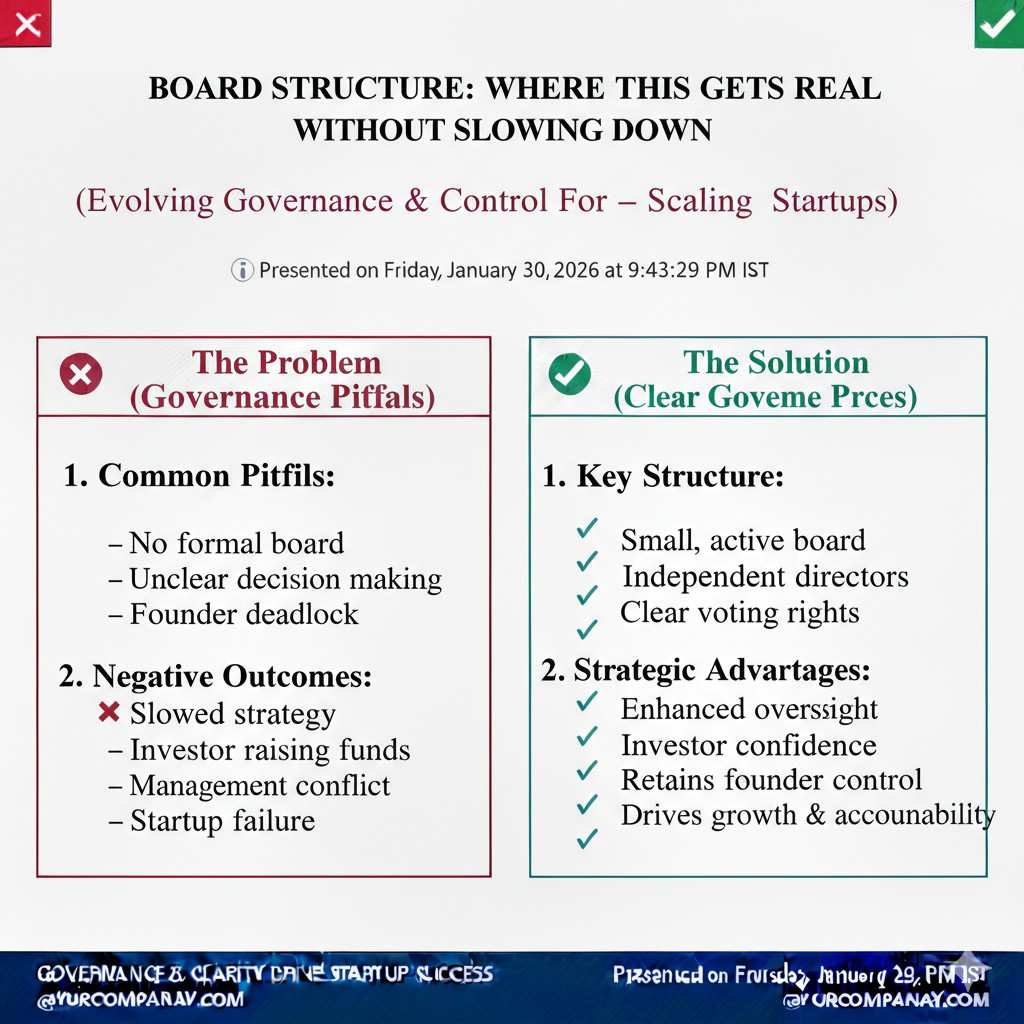

Board structure is where this gets real

A board is not just a formality. A board decides hiring and firing at the top, approves budgets, and guides major moves like acquisitions and new financings.

In global startups, board issues can get worse because of time zones and travel. If your board has people who are not aligned, every key decision becomes a meeting, then another meeting, then another.

The practical way to protect founder control

A healthy early board is small and balanced. It should help you make better decisions faster, not make you ask permission to build.

If an investor asks for strong veto rights, ask why. Sometimes the concern is real and you can solve it with reporting, milestones, or a clear IP plan. When you solve the real fear, the term often softens.

Pitfall 5: Leaving IP and ownership questions “for later”

This is the pitfall that shows up at the worst time

For technical founders, IP is not a nice-to-have. It is the thing you are selling. Yet many teams wait until diligence to organize it, and diligence is when you have the least time and the most pressure.

If your core code was built by contractors without clean assignments, if founders built parts before incorporation, or if university work overlaps, investors get nervous fast. Some will walk. Others will use it to push tougher terms.

Cross-border teams add extra risk

When your team is spread across countries, ownership paperwork matters even more. Different labor laws can affect who owns what. Some countries have strict rules about invention assignments and employee rights.

This does not mean you cannot build globally. It means you must be disciplined. Clear contracts, clear invention records, and a clear filing plan reduce the “unknowns” that make investors demand extra protection.

How IP can improve your priced round, not just “protect you”

Strong IP does two things in a priced round. First, it reduces risk in the investor’s mind. Second, it increases your leverage, because your work becomes harder to copy.

At Tran.vc, we invest up to $50,000 in-kind in patent and IP services so founders can build that leverage early—before the priced round terms get locked in. If you are raising soon and want to build a stronger position, apply anytime at https://www.tran.vc/apply-now-form/.

Pitfall 6: Pricing a round before you have the proof the market expects

A priced round raises the bar for the next round

When you set a price, you set a benchmark. The next investor will ask, “What changed since that price?” If the answer is not clear, you risk a flat round or a down round.

Many founders choose a priced round because they want to “look serious.” But seriousness is not the price. It is the proof behind it. If you price too early, you may lock yourself into expectations you cannot meet yet.

Global founders often face uneven traction signals

In some regions, early revenue may be harder to get, or sales cycles may be slower. Sometimes your customers need compliance steps. Sometimes buyers want to see local presence.

These are real challenges, but they do not change investor math. If your round is priced like you are already past those hurdles, you may create a gap between story and reality.

The better question than “Can we price it?”

Ask, “What milestones will make the next round easy?” Then price the round in a way that gives you room to hit those milestones without panic.

If you want, I can also explain when it may be smarter to use a SAFE or a note instead of a priced round, and how to avoid the common traps there too.