If you are building a deep tech, AI, or robotics startup, your first funding round will shape your company more than you think.

Before product-market fit.

Before revenue.

Before press.

The paper you sign at pre-seed can affect your control, your next round, and even your exit.

Two of the most common tools at this stage are the SAFE and the Convertible Note. Many founders hear these terms and nod. Few truly understand what they mean in practice.

This guide will explain both in plain language. No jargon. No fluff. Just what matters to you as a technical founder who wants to build something real, protect it well, and raise smart.

Let’s begin.

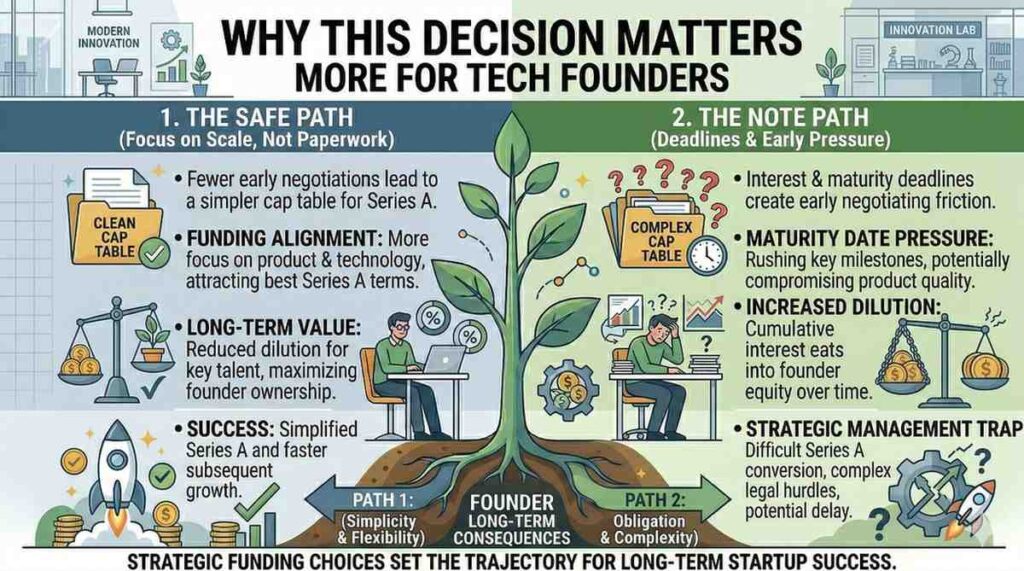

Why This Decision Matters More for Tech Founders

If you are building a SaaS tool, mistakes can be painful.

If you are building robotics, AI models, or deep infrastructure, mistakes can be fatal.

Your tech likely took years of study. It may involve complex algorithms, hardware, novel methods, or defensible systems. It can and should become intellectual property.

At the pre-seed stage, you are not just raising money. You are setting terms that future investors will look at closely. You are shaping how ownership flows. You are deciding how much leverage you will have when the real money comes in.

Many founders rush this step. They sign whatever their first angel sends. They focus only on getting cash in the bank.

That is understandable. But it is risky.

The better approach is simple: raise in a way that keeps you in control, protects your upside, and does not create hidden problems for your next round.

This is where SAFE and Convertible Notes come in.

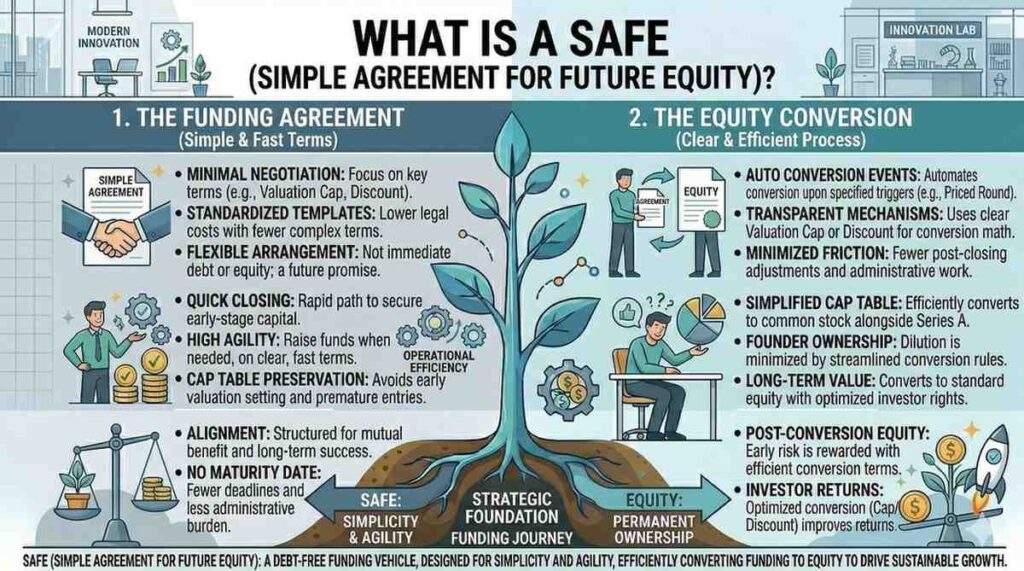

What Is a SAFE?

SAFE stands for Simple Agreement for Future Equity.

It was created by Y Combinator to make early fundraising easier. The idea was simple: instead of setting a valuation today, the investor gives you money now. Later, when you raise a priced round, that money converts into shares.

There is no interest. There is no maturity date. It does not act like a loan.

It is a promise that in the future, when you raise a real equity round, the investor will receive shares based on agreed terms.

At first glance, this sounds clean and founder-friendly.

No debt.

No ticking clock.

Fewer negotiations.

That is why SAFEs became popular, especially in Silicon Valley.

But simple does not always mean harmless.

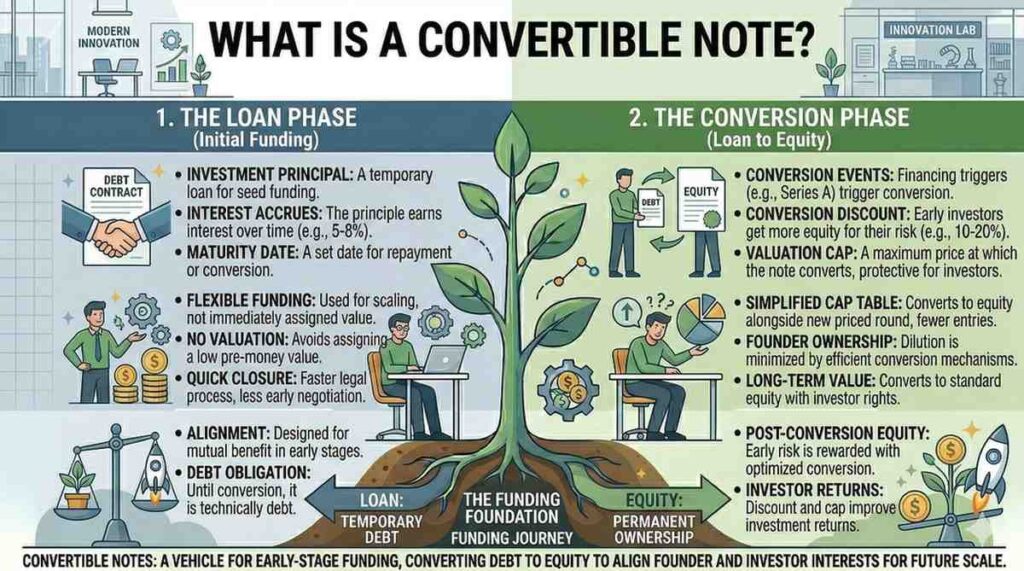

What Is a Convertible Note?

A Convertible Note is technically a loan.

The investor gives you money. That money accrues interest. It has a maturity date. At some point, usually when you raise your next round, the loan converts into equity.

So the big difference at the surface level is this:

A SAFE is not debt.

A Convertible Note is debt that converts into equity.

Both delay setting a valuation today. Both convert later. Both are used in pre-seed rounds.

But the details matter a lot.

The Core Terms You Must Understand

Whether you use a SAFE or a Convertible Note, you will usually see two important concepts: valuation cap and discount.

The valuation cap sets the maximum company value at which the investor will convert their money into shares.

The discount gives the investor a lower price per share compared to new investors in the next round.

These two tools reward early risk. Investors get better terms because they invested early.

That makes sense.

But the way these tools interact with your next round can change your cap table more than you expect.

Many founders do not model this properly. They accept a low cap because they want quick money. Later, when they raise a priced round, they realize early investors now own a much larger percentage than expected.

This can reduce founder ownership fast.

And if you are building long-term deep tech, ownership matters.

SAFE: The Advantages

Let us talk about why many founders like SAFEs.

First, they are fast.

There is usually less negotiation. Investors are used to them. Lawyers are familiar with them. You can close quickly.

Second, there is no interest. The amount invested does not grow over time.

Third, there is no maturity date. There is no legal deadline forcing conversion or repayment.

For founders who want speed and simplicity, this feels comfortable.

If you are raising a small round from angels and plan to raise a priced seed round within a year, a SAFE can be efficient.

But that is only part of the story.

SAFE: The Hidden Risks

The biggest issue with SAFEs is not obvious at first.

Because there is no maturity date, SAFEs can stack up.

You might raise $200,000 from one angel. Then another $150,000. Then another $250,000.

Each one on a different SAFE. Each with a different cap.

On paper, it feels harmless. No debt. No pressure.

But when you finally raise your seed round, all of those SAFEs convert at once.

Suddenly, your cap table shifts more than expected.

In some cases, founders discover they gave away 25 to 35 percent of their company before even closing their first priced round.

This becomes painful when VCs start negotiating.

They will look at your fully diluted ownership. If it is already tight, they may push for more aggressive terms.

Now your control shrinks even faster.

Another risk is psychological. Because SAFEs feel light, founders sometimes delay raising a proper priced round. They keep stacking SAFEs instead of building toward a clear milestone.

This can create a messy structure.

If you are building robotics or AI, where capital needs are higher and timelines are longer, this risk is even greater.

Convertible Note: The Advantages

Now let us look at Convertible Notes.

Because they are debt, they feel more serious. There is interest. There is a maturity date.

This can actually be healthy.

The maturity date creates discipline. It forces you to think about when you will raise your next round.

The interest component slightly increases what converts, but it is usually small compared to ownership impact.

Some institutional investors prefer notes because they are older and more traditional.

In certain markets outside Silicon Valley, Convertible Notes are still more common than SAFEs.

Another subtle benefit is negotiation clarity.

Because notes are more structured, discussions around terms are sometimes more direct. There is less ambiguity around edge cases.

Convertible Note: The Risks

The main risk is the maturity date.

If you do not raise a new round before the note matures, the investor technically has the right to demand repayment.

In reality, this rarely happens with good investors. Most will extend the note.

But legally, that pressure exists.

For a hardware-heavy robotics startup with longer build cycles, that clock can feel stressful.

Also, interest accrues. While it is usually small, it does increase dilution slightly.

Convertible Notes can also stack, just like SAFEs. If you raise multiple notes with different caps, your future dilution can still surprise you.

The tool itself is not the problem. Lack of planning is the problem.

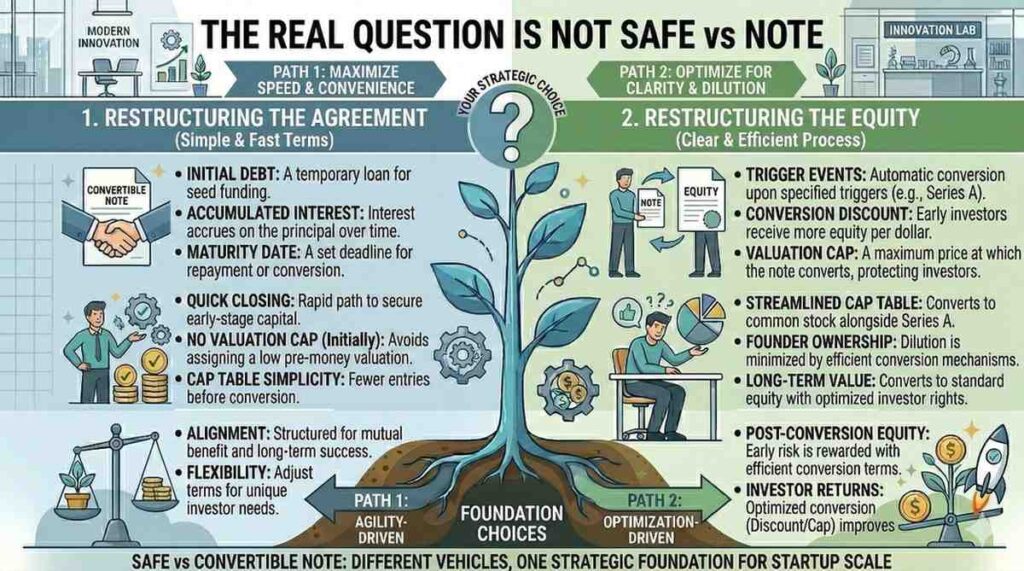

The Real Question Is Not SAFE vs Note

Here is the truth most founders miss.

The instrument matters less than the strategy.

What matters most is:

How much are you raising?

At what cap?

From whom?

And what milestone will this money help you reach?

If you raise $500,000 on a SAFE at a $5 million cap and hit strong traction, that can be fine.

If you raise $1.5 million in scattered SAFEs at a $3 million cap before even proving your tech works, that can hurt you later.

The same logic applies to Convertible Notes.

The document is not magic. It is a container.

The real issue is whether you are raising with intention.

This is especially important for deep tech founders. Your company’s value is not just traction. It is your intellectual property.

If your core algorithm, hardware design, or system architecture is not protected, your leverage in the next round is weak.

When investors know your IP is secured, your position improves. Your valuation discussions change. Your negotiating power grows.

That is why pre-seed should not only be about cash.

It should be about building defensible assets.

At Tran.vc, this is exactly what we focus on. We invest up to $50,000 in in-kind patent and IP services. Not just money, but real strategy. We help founders turn code and inventions into protected assets before the big round.

If you are thinking about raising pre-seed, you can apply anytime at https://www.tran.vc/apply-now-form/

The right structure combined with strong IP can change everything.

SAFE vs Convertible Note: The Real Structural Differences

How Each Instrument Is Legally Built

A SAFE is not a loan. It is a contract that promises future equity when a priced round happens. There is no debt on your balance sheet. There is no interest growing over time. There is also no fixed deadline by which conversion must happen.

A Convertible Note, on the other hand, begins its life as debt. It sits on your books as a loan. It earns interest. It carries a maturity date. Even though most notes are designed to convert into equity, they still start as borrowed money.

This legal difference may seem small, but it changes how investors view risk and how lawyers structure your documents. It also shapes how much pressure exists if your next round takes longer than expected.

For a deep tech founder building complex systems, timelines are rarely predictable. That legal foundation can either give you breathing room or create silent stress in the background.

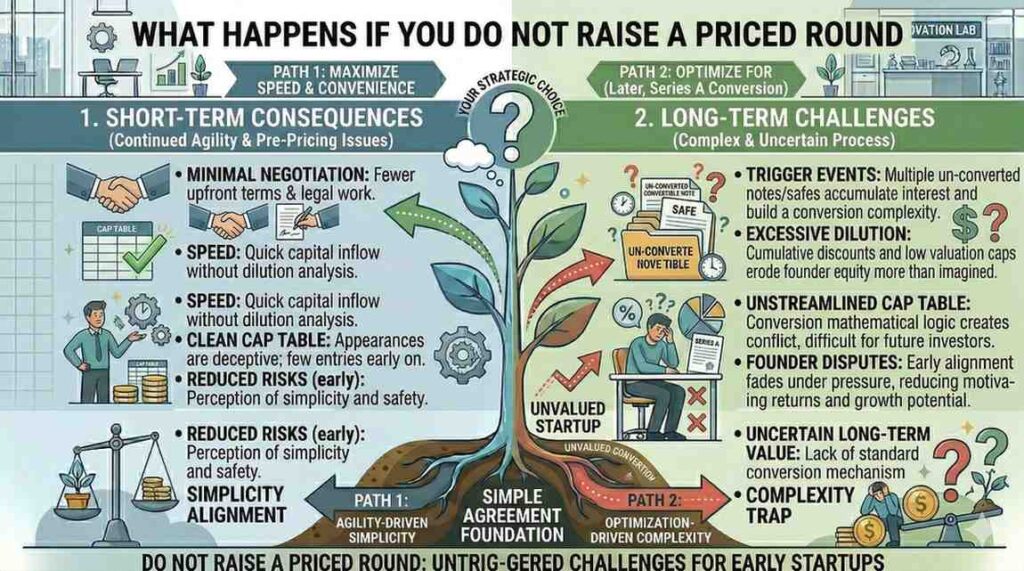

What Happens If You Do Not Raise a Priced Round

With a SAFE, nothing dramatic happens if you do not raise a priced round quickly. There is no repayment clause triggered by time alone. The agreement simply waits until a qualifying event occurs.

With a Convertible Note, the maturity date eventually arrives. At that point, the investor technically has the right to request repayment. In practice, many investors extend the note. Still, the power balance shifts slightly when that date approaches.

If your robotics product takes 24 months instead of 12, that maturity date can become a real negotiation moment. You may be forced to renegotiate terms at a time when you do not yet have strong leverage.

Understanding this difference is critical before you sign. It is not about fear. It is about knowing how future scenarios play out.

How Interest Changes the Math

A SAFE does not accrue interest. If an investor puts in $250,000, that exact amount converts later based on the agreed cap or discount. The number stays clean and simple.

A Convertible Note accrues interest over time. If the interest rate is five percent and you take two years to raise your next round, the total amount converting will be higher than the original investment.

While the increase is usually not massive, it still means slightly more dilution. Over several notes and multiple years, those increments add up.

For founders who are careful about ownership, even small percentage shifts matter. That is why modeling both scenarios before signing is essential.

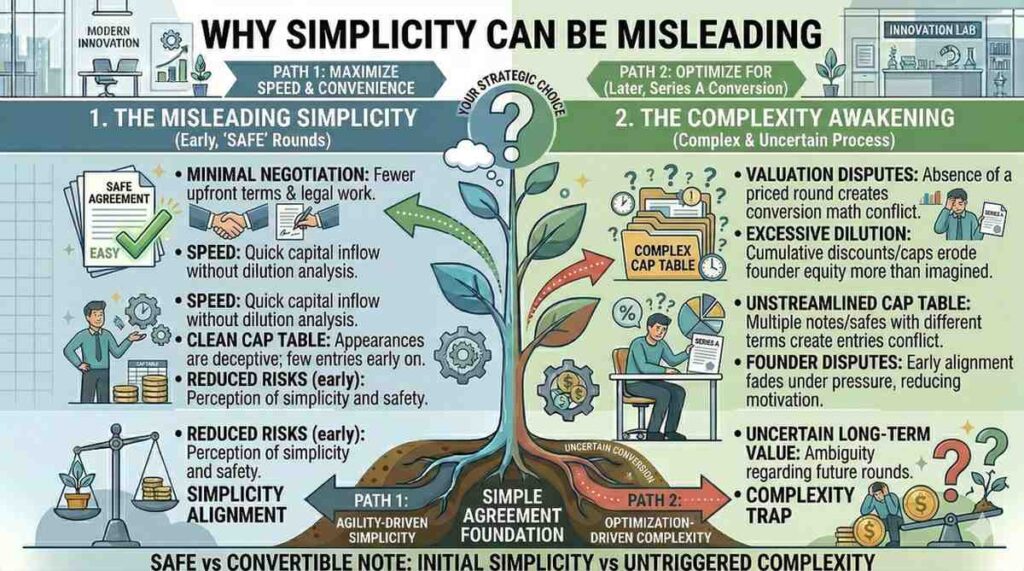

Why Simplicity Can Be Misleading

Many founders choose SAFEs because they appear simple. Fewer moving parts. No interest calculations. No ticking maturity clock.

But simplicity on the surface can hide complexity later. When you raise multiple SAFEs at different valuation caps, the conversion math becomes layered. Each investor may convert at a different effective price.

When the priced round finally happens, the cap table can change quickly. You may find that your ownership dropped more than you expected.

The instrument itself is not dangerous. Lack of planning is what creates surprises.

Valuation Caps and Discounts: Where Founders Lose Control

Understanding the Valuation Cap in Plain Terms

The valuation cap sets the maximum company value used to calculate how much equity early investors receive. If your SAFE has a $5 million cap and your next round values the company at $10 million, the SAFE converts as if the valuation were $5 million.

This rewards early risk. Investors who believed in you before traction get better pricing. That part is fair and reasonable.

The problem begins when founders agree to caps that are too low for the level of risk they are taking. If your technology is complex and years in the making, a very low cap may not reflect real value.

When the next round closes at a higher valuation, that early low cap can result in significant dilution. You gave up a large piece of your company before it had the chance to mature.

The Discount and Its Long-Term Effect

A discount gives early investors a reduced price per share compared to new investors in the next round. For example, a twenty percent discount means they pay less per share than the incoming seed investors.

If both a cap and a discount exist, the investor typically receives whichever term is more favorable. That means your dilution will follow the path that gives them the better deal.

Many founders accept both terms without modeling outcomes. They focus on closing the round quickly instead of understanding conversion math.

Before signing, you should simulate several future valuations and see exactly how much ownership converts under each case. This simple exercise can prevent painful surprises later.

How Caps Influence Your Seed Round Negotiation

When institutional seed investors review your company, they will examine your fully diluted cap table. They will calculate how much ownership remains available after all SAFEs or notes convert.

If too much equity is already spoken for, new investors may demand stronger terms. They may request more ownership to compensate for perceived risk.

This creates a compounding effect. Early dilution from low caps makes later dilution more aggressive. Over time, founder ownership shrinks faster than planned.

If you are building AI or robotics infrastructure that may require multiple rounds of capital, protecting early ownership is not optional. It is strategic survival.

Timing and Milestones: Raising With Intention

Raise for a Clear Technical Milestone

Pre-seed money should have one job. It should help you reach a clear milestone that increases company value. For deep tech founders, that milestone is often technical proof, prototype validation, or protected intellectual property.

If you raise without a defined milestone, you risk drifting. You spend money but do not increase leverage. When it is time to raise again, investors see limited progress and push for tougher terms.

Before choosing SAFE or Convertible Note, define what this round must accomplish. Be precise. Is it filing core patents, building a working prototype, or securing a key pilot customer?

When your milestone is clear, your funding instrument becomes a tool instead of a lifeline.

Avoid Endless Rolling Rounds

Some founders treat pre-seed as an open door. They raise small checks over a long period, often through multiple SAFEs. Each new investor joins at a slightly different cap.

This rolling approach can stretch for years. It delays the moment when you face a true priced round. It also complicates your cap table.

When the seed round finally comes, conversion math becomes messy. Investors must untangle different caps, discounts, and interest calculations. Complexity rarely helps you in negotiations.

A better approach is to raise a defined amount, hit a defined milestone, and then move decisively to a priced round when ready.

Align the Instrument With Your Development Cycle

If your development cycle is short and you expect to raise a seed round within twelve months, a SAFE may provide enough flexibility.

If your build cycle is long and uncertain, the maturity date on a Convertible Note must be realistic. You should negotiate enough runway so you are not forced into extension talks at a weak moment.

Neither instrument is universally superior. The right choice depends on your timeline, capital needs, and investor mix.

What remains constant is the need for foresight. Technical founders often focus deeply on product and ignore financial structure. That imbalance can be costly.

How IP Strategy Changes the SAFE vs Note Decision

Why Deep Tech Is Not Like SaaS

If you are building a simple app, speed may matter more than protection. But if you are creating new algorithms, hardware systems, or machine learning architecture, intellectual property becomes your leverage.

When your patents are filed and your IP strategy is clear, investors see defensibility. They see barriers that competitors cannot easily cross.

That defensibility affects valuation. It changes how confidently you negotiate caps and discounts.

Raising on a low cap without protected IP is risky. Raising after securing key filings puts you in a stronger position, regardless of whether you use a SAFE or a Convertible Note.

Turning Code Into Assets Before the Big Round

Many founders wait until after raising seed to think about patents. By then, dilution has already occurred. Negotiation power has already shifted.

A smarter approach is to build your moat early. File strategically. Document inventions properly. Structure ownership clearly.

When you walk into a seed round with real IP assets, your story changes. Investors are not just funding potential. They are funding protected innovation.

This is where pre-seed strategy connects directly to long-term ownership. The instrument you choose works best when paired with strong intellectual property.

How Tran.vc Supports Founders at This Stage

At Tran.vc, we invest up to $50,000 in in-kind patent and IP services. That means real patent strategy, filings, and guidance from experienced professionals.

We work alongside founders before the big institutional round. We help structure IP in a way that strengthens valuation and protects ownership.

Instead of pushing you to raise fast, we focus on helping you raise strong. We believe leverage comes from protected assets, not hype.

If you are preparing for a pre-seed round and want to build real defensibility from day one, you can apply anytime at https://www.tran.vc/apply-now-form/