A funding round can feel like a fork in the road.

One path is fast: you grab a SAFE, keep building, and promise yourself you will “figure out the real round later.” The other path is slower: you set a price today, sign bigger papers, and lock the rules of the game.

Both paths can work. Both can also hurt you if you pick them at the wrong time, or if you sign terms you do not fully see yet.

This article is about the three most common early structures you will hear: SAFEs, notes, and priced rounds. We will keep it plain and real. No fancy talk. Just what founders need to know to make clean moves, keep control, and avoid traps.

And because Tran.vc works with deep tech, AI, and robotics teams, we will also talk about the part many founders miss: your IP. If your moat lives in code, models, motion control, sensors, chips, or data pipelines, your funding structure should not weaken your ability to protect it. It should help you build it.

If you want Tran.vc to help you turn your inventions into assets (with up to $50,000 in-kind patent and IP work), you can apply anytime here: https://www.tran.vc/apply-now-form/

The real goal of your first money

Let’s start with a truth that is easy to forget when you are tired and running on coffee.

Early money is not the finish line. It is not even “funding.” It is time.

Time to ship.

Time to learn.

Time to reach a clear next proof point.

If the money you raise does not buy you a clean sprint to the next proof point, you are taking dilution and risk for nothing.

So before we even touch SAFEs or notes, ask yourself one hard question:

What exact proof will make your next raise easier and more expensive (in a good way)?

For a deep tech founder, “proof” is often one of these:

A working demo that does not break.

A pilot that runs in the real world.

A repeatable unit that you can build again.

A key performance jump that is hard to copy.

A regulatory step cleared.

A paid contract, even if small.

Now add one more question that most founders skip:

What IP will be created during this sprint, and how will we protect it?

Because if you are building robotics or AI, you are almost always creating protectable inventions while you sprint. The structure of your money should give you room to file, not squeeze you into rushing or skipping it.

That is one reason Tran.vc exists: we invest as in-kind IP services so you can build defensible value while you build product. You can apply here when you are ready: https://www.tran.vc/apply-now-form/

The three structures in plain words

Here is the clean mental model.

A SAFE is a promise: “You give me money now. Later, when I raise a priced round, you convert into shares using a rule we agree on today.”

A note is a loan with a conversion feature: “You give me money now. I owe you back later, but usually it converts into shares when I raise a priced round.”

A priced round is what it sounds like: “We set a company value today, you buy shares today, and we all sign the full set of rules today.”

If you only remember one thing, remember this:

A SAFE is simple now, complex later.

A priced round is complex now, simple later.

Notes sit in the middle, but they come with one sharp knife: debt.

SAFEs: why founders love them, and where they bite

SAFEs became popular because they remove friction. A founder can close money in days, not months. That speed can save your company.

But speed has a cost. The cost shows up later when you have many SAFEs stacked on top of each other.

Let’s break SAFEs down in a way that matches real founder life.

What a SAFE is really doing

A SAFE does not set your company value today. It sets a rule for how value will be set later.

That rule usually comes in one of two forms:

A discount, like “20% off the next round price.”

A valuation cap, like “I convert as if the company was worth no more than $X.”

Sometimes it has both.

Most founders focus on the cap. They talk about it like it is the valuation. It is not. It is a ceiling for conversion math. It can feel like a valuation because it affects how many shares the SAFE investor gets later. But it is not the same thing as pricing the company today.

This matters because founders often stack SAFEs at rising caps. They think: “Great, my cap is going up, that means I am growing.” Sometimes that is true. But the math of conversion can still surprise you.

The hidden dilution problem

Here is the trap: dilution from SAFEs is not fully visible until the priced round happens.

That means you can wake up one day, right when you want to raise a big seed round, and realize you already sold more of the company than you thought.

This happens when:

You raised multiple SAFEs at different caps.

You raised on “most favored nation” terms and forgot what that can do.

You allowed a big discount and a low cap together.

You did not model conversion outcomes.

This is why serious founders run a simple cap table model early, even if they are pre-seed. Not a perfect model. Just enough to see the range of outcomes.

If you want help with this, Tran.vc does this kind of planning all the time, because it connects directly to how you protect your IP while you raise. Apply here: https://www.tran.vc/apply-now-form/

How SAFEs can scare off the next lead investor

A strong seed investor wants clarity. They want to know what they are buying, and what the company will look like after the round.

If your cap table has a pile of SAFEs with different caps, side letters, pro-rata promises, and unusual terms, a lead investor may slow down or walk away. Not because they dislike SAFEs, but because uncertainty creates risk.

A lead investor is signing up to own a large piece of the company. They want the rules clean.

This is why, if you are going to use SAFEs, you should keep them boring.

Boring terms are your friend.

What “boring” looks like in SAFE land

It looks like this:

One cap (or a tight range), not a ladder of ten caps.

One standard template, not custom edits for every check.

No strange side promises that create hidden rights.

A clear plan for when you stop using SAFEs.

The best SAFE strategy is not “raise forever on SAFEs.” The best SAFE strategy is “use SAFEs as a bridge to a real priced round, without creating a mess.”

When a SAFE is the right move

A SAFE is often a good fit when:

You are very early and still proving basics.

You need speed more than you need precision.

Your round is small enough that the dilution surprise is limited.

You expect a priced round in the near future.

“Near future” does not mean next month. It means you can see the path. You know what proof points you will hit, and you have a real shot at pricing in the next stage.

If you cannot see that path, a SAFE can turn into a habit. Habits are where companies get stuck.

Notes: the old tool that still matters

Convertible notes were common before SAFEs. They are still used, and sometimes they are the better tool.

The main difference is simple:

A note is debt. A SAFE is not.

Debt changes behavior. It adds pressure. Pressure can be useful, but it can also crush a young company.

Why investors ask for notes

Some investors like notes because notes can include:

An interest rate (even if small).

A maturity date (a deadline).

Clear rights if the company never raises a priced round.

From an investor view, notes can feel more protected.

From a founder view, that “protection” can become a constraint.

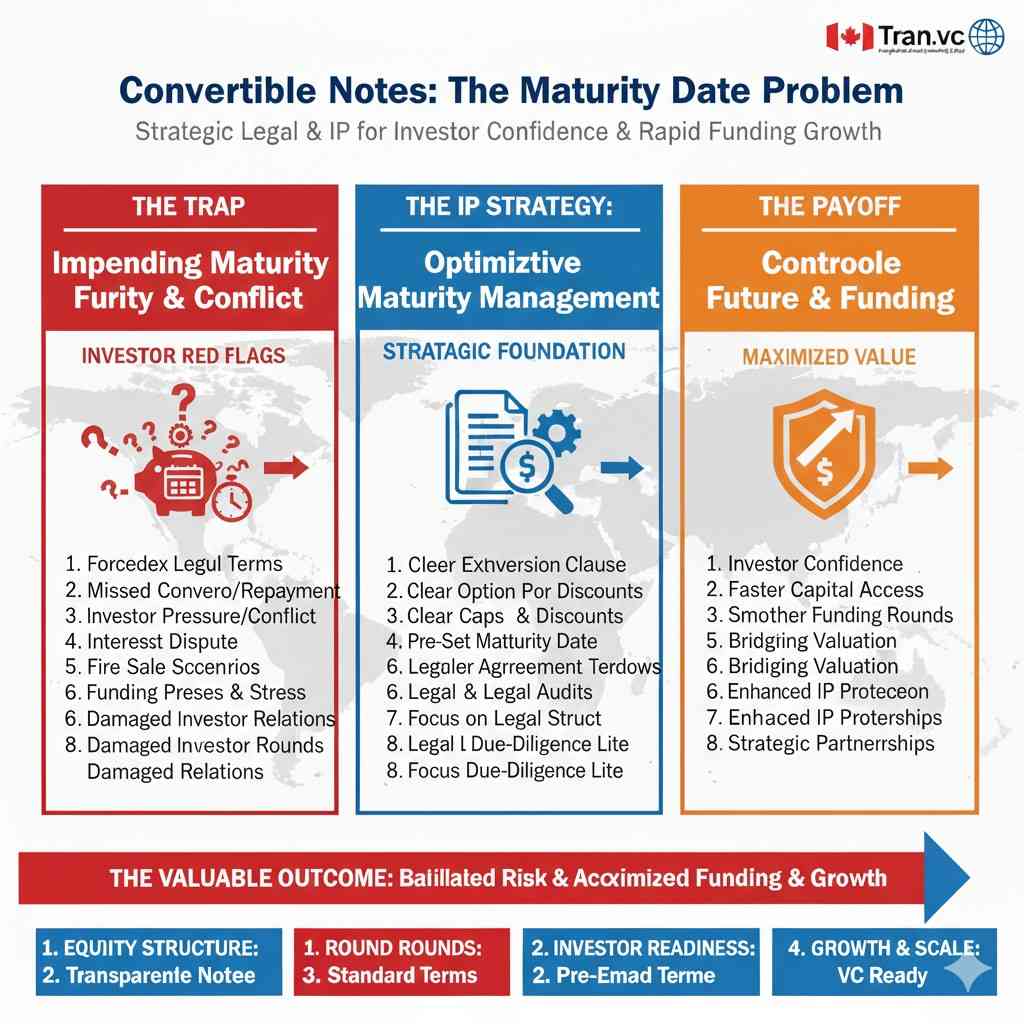

The maturity date issue

A maturity date sounds harmless when it is two years away.

But startups run on surprises. Two years can vanish fast.

If you hit the maturity date without a priced round, you may face:

Pressure to repay (usually impossible).

Pressure to convert on terms that favor the investor.

Pressure during a time you least need it.

Some notes are written in a founder-friendly way, where maturity triggers a discussion, not a hammer. Others are written like a bank loan in disguise.

So if you use notes, treat the maturity date as real. Do not assume you can “extend it later.” You might not have leverage later.

When notes can be a smart choice

Notes can be useful when:

The investor will not do a SAFE, period.

You want a forcing function so the company does not drift.

You are close to a priced round and want a short bridge.

The terms are simple, and the maturity is not designed to trap you.

A note should feel like a bridge, not a cage.

Priced rounds: the moment you set the rules

A priced round is the cleanest structure long term because it sets the company value now, sells shares now, and creates a clear cap table now.

It is also heavier. It takes time, legal work, and negotiation.

Founders often avoid priced rounds because they think they are “too early.” Sometimes they are right. But sometimes they are just afraid of pricing.

Pricing is not scary if you treat it correctly.

What pricing really means

Pricing is simply saying: “This is the value today, based on today’s risk.”

It is not a trophy. It is not your identity. It is a tool.

A priced round forces you to answer hard questions:

Who owns what?

How much control do founders keep?

What rights do investors get?

What happens if things go wrong?

In deep tech, these questions also touch IP:

Who owns inventions made during the company’s life?

What happens if a founder leaves?

What happens if you used open source in risky ways?

What happens if a contractor wrote key code?

What happens if university work is involved?

A priced round is often the first time investors look at these issues closely. That can be painful if you ignored them. Or it can be smooth if you handled them early.

Tran.vc’s whole model is built around helping founders handle them early. Apply anytime: https://www.tran.vc/apply-now-form/

When priced rounds are worth it

A priced round is often worth it when:

You have strong proof and can defend a price.

You are raising a larger seed round.

You want one lead investor who sets terms.

You want to stop stacking convertibles.

You need a clean structure for future rounds.

If you are building robotics or AI with real technical edges, pricing earlier than you think can sometimes help you. Why? Because you can lock in value before you scale the team and dilute yourself through more bridges.

But you need the right setup, and you need to protect the inventions being created. If you raise a priced round and your IP is messy, you can lose leverage fast.

The “path” most founders actually take

In real life, many companies follow a path like this:

A small pre-seed on SAFEs.

A bigger seed as a priced round.

Then Series A priced round.

That is a normal path. The danger is not the path itself. The danger is drifting.

Drifting looks like:

SAFE after SAFE after SAFE, with no plan to price.

Notes with short maturity dates that keep rolling.

Raising money without building the proof needed to price higher.

Ignoring IP until a lead investor asks for it.

To structure the path well, you need to connect funding structure to your proof plan.

Your proof plan is the engine. Your funding structure is the fuel tank.

If the tank is leaky, you will stall right when you should be accelerating.

A quick word on Tran.vc and why IP changes the funding math

Most people treat patents like a “later” item. In deep tech, “later” is often too late.

If your company’s value is tied to:

A new control method,

A new training pipeline,

A new sensor fusion approach,

A new edge inference trick,

A new robot mechanism,

A new hardware-software loop,

…then you are creating protectable inventions early.

When you protect them early, you can often raise with more leverage. You are not just selling a dream. You are building assets.

Tran.vc invests up to $50,000 in-kind in patent and IP work so founders can do this without burning scarce cash. If you want to see if you fit, apply here: https://www.tran.vc/apply-now-form/

SAFEs: fast now, messy later if you are not careful

What a SAFE really is

A SAFE is not a loan and it is not stock today. It is a simple promise that says, “You invest now, and you get shares later when we do a priced round.” That is why founders like it. The company can take money without having to fight over valuation right away.

The key detail is that a SAFE delays the hard part. It pushes the real pricing conversation into the future. That can be healthy when you are still proving basics, but it can also create a pile of unknowns that shows up all at once when you try to raise your seed round.

The two knobs that control almost everything

Most SAFEs have a discount, a valuation cap, or both. A discount means the SAFE converts at a cheaper price than the new investors pay. A cap means the SAFE converts as if the company’s value is no higher than a set number, even if the priced round values the company higher.

Founders often talk about the cap like it is their valuation. It is not. The cap is a conversion rule, not a public price. Still, it has real impact because it changes how many shares the SAFE investor receives later. If you stack SAFEs at low caps, you may be giving away more ownership than you think.

Why SAFEs can feel easy but cost you later

A SAFE makes it simple to close money in days instead of months. That speed can matter when you are hiring, building, or racing a competitor. But speed also means you might skip the work of modeling dilution and future outcomes.

The problem is that SAFE dilution stays hidden until conversion. When the seed lead investor asks, “How much of the company is already spoken for?” you may not like the answer. Even worse, you may not have a clean way to fix it without upsetting early backers.

The common SAFE trap in real fundraising

A lot of founders raise a SAFE, then raise another one, then another. Each time, the cap creeps up a bit and everyone feels good. But under the hood, you are creating a conversion stack with different rules and different prices, and that can turn into a cap table puzzle.

Seed investors do not fear SAFEs. They fear confusion. If your conversion math is unclear, it slows down the round. If it looks unfair to new money, it can reduce your leverage. If it looks unfair to earlier money, it can create drama right when you need focus.

How to keep a SAFE round clean

If you are going to use SAFEs, keep the terms boring and consistent. Aim for one template and one main set of terms so the conversion math stays understandable. Avoid side promises that quietly grant extra rights, because those are the things that surface during diligence and create delays.

A SAFE works best when it is a bridge with a clear end point. The “end point” is not a date on the calendar. It is a proof point that makes a priced round realistic. If you cannot name that proof point, you might be starting a SAFE habit instead of running a SAFE strategy.

When a SAFE is usually the right tool

A SAFE is often a strong fit when you are early and speed matters more than precision. It can also make sense when the check sizes are small and you expect to price the next round after a clear product or traction milestone. For deep tech teams, it can be useful while you validate feasibility and show a demo that works outside the lab.

If your invention is your edge, this is also the phase where IP planning matters. The safest SAFE strategy is the one that leaves you enough room to file and protect what you are creating, not one that forces you to rush or ignore it. If you want Tran.vc’s help building that IP foundation with up to $50,000 of in-kind patent work, you can apply here: https://www.tran.vc/apply-now-form/

Notes: familiar structure, real pressure

How a note differs from a SAFE

A convertible note looks similar to a SAFE on the surface because it also converts into shares later. The difference is that a note is debt. It is a loan to the company that usually converts when you raise a priced round, but it still carries loan features.

Those features may include interest and a maturity date. Even if everyone expects conversion, the presence of debt changes the tone. It adds a timeline and, in some cases, gives the investor leverage if things take longer than planned.

Why the maturity date matters more than it seems

The maturity date is the moment the note technically comes due. If you hit that date without a priced round, you are forced into a decision point. That decision point might be friendly, but it might not be. It depends on the terms and on the relationship.

Many founders assume they can simply extend maturity. Sometimes you can. Sometimes the investor says no. If you are not in a strong position at that time, a maturity date can become a stress event that distracts you from product and customers.

When notes can still be a smart move

Notes can work well as short bridges when you are close to a priced round and you want a simple tool with familiar investor expectations. They can also work when an investor will not do a SAFE and insists on debt-like structure.

The key is to treat notes with respect. You want terms that do not turn the maturity date into a weapon. You also want to avoid complex repayment triggers that create panic if your timeline shifts, which is common in robotics and other hard tech.

What to watch for in note terms

Interest is rarely the main issue. The bigger issue is what happens at maturity and what the investor can demand. Some notes include conversion options that heavily favor the investor if you do not raise in time, which can silently set a low effective price.

If you use notes, you should model the “bad case” outcome, not just the happy path. You do not need a perfect model, but you do need to see what happens if the priced round takes longer. That small exercise protects you from signing a deal that only works if life goes perfectly.

Priced rounds: heavier work, cleaner future

What “priced” actually means

A priced round sets the value of the company today and sells shares today. This makes the ownership picture clear right away. It also locks in the main investor rights, the governance structure, and the rules for future rounds.

It is more work than a SAFE because it requires deeper legal documents and more negotiation. But it can also reduce future friction because you do not have a conversion stack hanging over the cap table.

Why priced rounds can improve your leverage

When you price a round, you stop postponing the valuation conversation. If you have strong proof, pricing can help you capture the value you already created. It can also make the next raise smoother because investors see a clean, standard structure.

For deep tech, a priced round often forces the company to get serious about things investors care about, like IP ownership, contractor assignments, open-source risk, and founder vesting. These topics can feel annoying, but solving them early often makes fundraising faster later.

When priced rounds are worth the effort

Priced rounds are often worth it when you are raising a larger seed and you expect a lead investor. They also make sense when you are done with “feasibility” and you can defend a valuation based on real progress. If you already have pilots, paid contracts, or a working system that is hard to copy, a priced round may be the clean next step.

They are also useful when you want to stop stacking SAFEs. If your cap table is getting crowded with convertibles, pricing can be a reset that gives everyone clarity and gives you a stable base to build from.

The real cost of avoiding pricing for too long

Avoiding pricing can feel safe, but it can also reduce your options. If you raise many SAFEs and then try to price later, the conversion math may force you into a structure that new investors dislike. In some cases, founders end up accepting worse terms in the priced round just to manage the SAFE stack.

A priced round is not always the answer, but it is often the moment you regain control of the narrative. It lets you say, “Here is what the company is worth now, and here is the plan to grow it.”

The path: choosing the right structure for your stage

The clean way to decide without guesswork

The best way to choose between a SAFE, a note, and a priced round is to start with your next proof point. Your structure should buy you enough time and focus to hit that proof point without creating a messy future.

If you are still proving that the tech works, a SAFE can be the simplest tool. If you are close to pricing and you need a short bridge, a note might fit, but only if the maturity risk is truly manageable. If you have proof and you want to raise a meaningful seed, pricing often makes fundraising smoother and puts you back on solid ground.

How your proof point changes what “good terms” look like

If your next proof point is a working demo or first pilot, speed matters. You do not want to spend months on legal work. In that case, a SAFE with clean, standard terms is often enough. But you still want to be honest about dilution and stop-loss points, so you do not wake up later with surprise ownership loss.

If your next proof point is scale, like deploying multiple pilots or building a manufacturing path, you may need a stronger investor partner and larger checks. That is where priced rounds often shine, because they bring a lead investor into the open with clear commitments and clear expectations.

Why IP should sit inside the structure choice

In robotics and AI, your value is often the part people cannot easily copy. That might be a novel control loop, a training method, a data pipeline, or a system design that took months to refine. If you leave that unprotected, you may be forced to raise on weaker terms because you cannot prove defensibility.

Tran.vc’s approach is built around fixing this early. Instead of just adding cash, we invest up to $50,000 in-kind in patent and IP work so you can turn technical progress into durable assets. If you are building in deep tech, AI, or robotics and want to raise with more leverage, you can apply here: https://www.tran.vc/apply-now-form/