Splitting equity is one of the first “real” decisions a founding team makes. It feels simple at first: two people, one idea, let’s be fair. But once one founder writes the code and the other founder does everything else, the word “fair” gets messy fast.

This is even more true in robotics, AI, and deep tech—because the technical work is not just “building a website.” It is years of skill, hard-to-copy know-how, and the kind of invention that can become real IP. That is why this topic matters so much early, before feelings harden and before the company has investors watching.

At Tran.vc, we see this play out the same way again and again. A technical founder wants a strong partner who can sell, recruit, talk to customers, and raise. A non-technical founder wants to be treated like a real co-founder, not “the helper.” Both are valid. The risk is not that you pick a “wrong” split on day one. The risk is that you pick a split without clear logic, and then you spend the next two years paying for it in tension, slow decisions, and silent resentment.

This article will help you avoid that.

Before we go further, one quick note: if you are building in robotics, AI, or deep tech, and you want to protect what you are inventing from day one, you can apply anytime at https://www.tran.vc/apply-now-form/. Tran.vc invests up to $50,000 in in-kind patent and IP services, so you build a moat early—without giving up control too soon.

Splitting Equity with a Non-Technical Co-Founder

The real reason this topic gets emotional

Equity is not just a number on a cap table. It is a signal of trust, respect, and long-term promise between two people taking a big risk together. That is why a small mismatch in expectations can feel personal, even when no one is trying to be unfair.

In deep tech, the pressure is higher because the technical work often is the product at the start. If one person can build the core system and the other person cannot, it can feel like the value is uneven. The non-technical founder may still be doing hard work, but it is harder to “see” in a demo.

The goal is not to remove emotion. The goal is to design a split that holds up under stress, so both founders can stay focused when the company gets hard—which it always does.

The biggest mistake: treating “50/50” as the default

Many teams pick 50/50 because it feels clean and friendly. It is also a fast way to avoid an uncomfortable talk. But “fast and clean” is not the same as “stable.”

A 50/50 split creates a hidden rule: both people have the same weight forever. If one founder ends up carrying the company for a year while the other struggles, the split can start to feel like a tax. If that feeling grows, decisions slow down and trust fades.

Sometimes 50/50 is right. But it should be the result of clear thinking, not the result of avoiding tension.

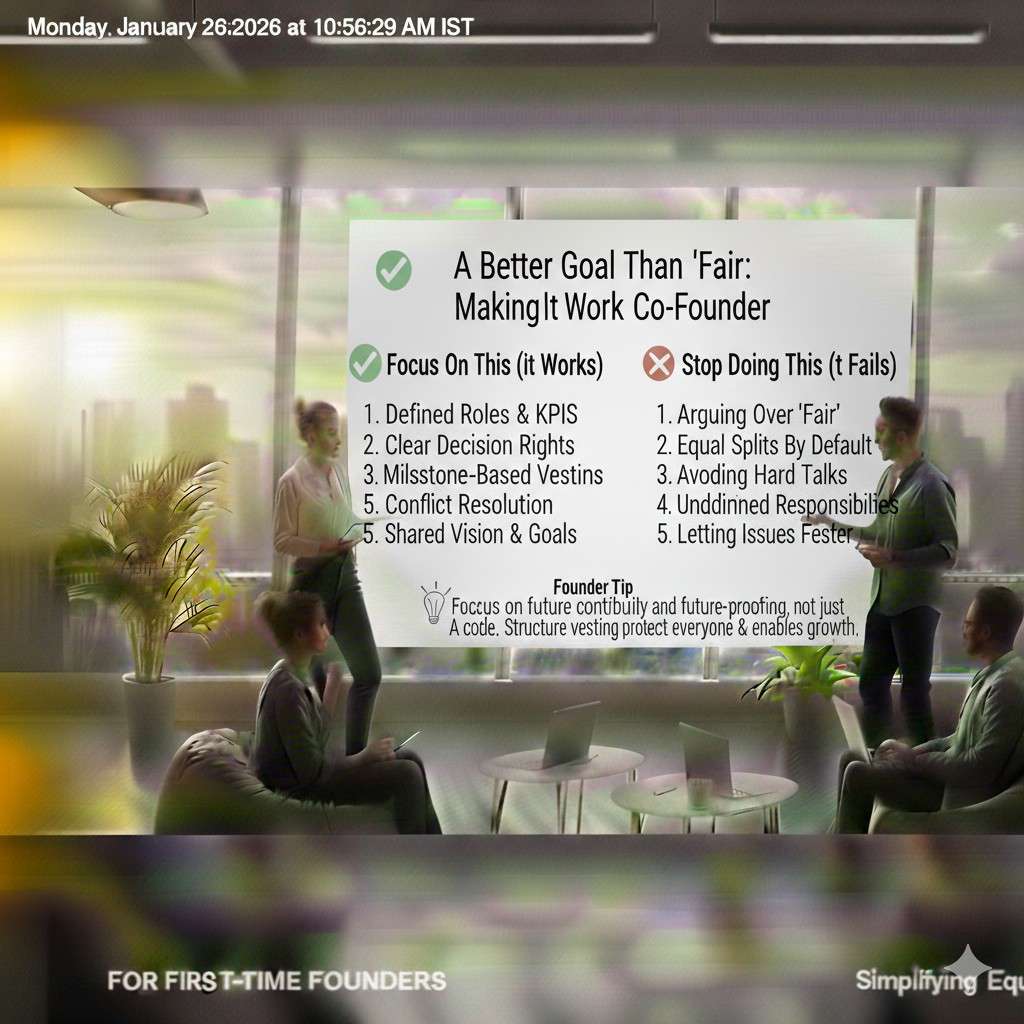

A better goal than “fair”: making it work

Early-stage startups do not need fairness in a perfect sense. They need a structure that keeps both founders committed, motivated, and honest. The company needs both of you to keep showing up when things go wrong, when money is tight, and when the first plan fails.

That is why the best equity splits are not moral judgments. They are practical agreements built on roles, risk, time, and impact. When the logic is clear, it becomes easier for both founders to accept the outcome.

If you are building robotics, AI, or deep tech, and your advantage comes from what you are inventing, you should protect it early. Tran.vc invests up to $50,000 in in-kind patent and IP services to help technical teams turn core ideas into defensible assets. You can apply anytime at https://www.tran.vc/apply-now-form/.

Start with one simple question: what company are you building?

Not all startups value the same work in the first 12 months

A non-technical co-founder can be priceless in some businesses and less critical in others. The difference is not about talent. It is about what the company must achieve first to survive.

If your first milestone is a working technical system that proves the core idea, then technical execution is the bottleneck. In many deep tech startups, without that proof, there is nothing to sell, nothing to test, and nothing credible to raise on.

If your first milestone is distribution—getting customers fast, landing partnerships, or closing revenue—then the bottleneck may be go-to-market. In some markets, speed of sales matters more than technical novelty at the start, even if the product becomes complex later.

Deep tech adds one more layer: defensibility

In robotics and AI, your edge is often in how you solve a hard problem. That can be your model design, your data pipeline, your control system, your hardware design, or a unique workflow that competitors cannot easily copy.

This is where IP becomes a real lever. Patents and IP strategy are not paperwork. They can turn fragile early advantage into a durable moat that holds value even when bigger teams show up.

If you want help building that moat early, Tran.vc’s model is built for this stage. Instead of just writing a check and stepping away, Tran.vc invests up to $50,000 in hands-on patent and IP services. Apply anytime at https://www.tran.vc/apply-now-form/.

Make a clear distinction: “co-founder” is a role, not a title

A non-technical co-founder is not the same as an early employee

This is where many technical founders get stuck. They meet someone great at talking, pitching, and networking, and they call them a co-founder. Then six months later they realize the person is acting more like a contractor who “helps” rather than an owner who carries weight.

A co-founder does not do tasks. A co-founder owns outcomes. They take responsibility for a major part of the company and they keep pushing even when there is no applause. If your non-technical partner is truly doing that, they may deserve meaningful equity.

If they are not owning outcomes, then the equity should reflect that. Titles can be friendly, but equity is expensive. It should be earned by responsibility and sustained effort.

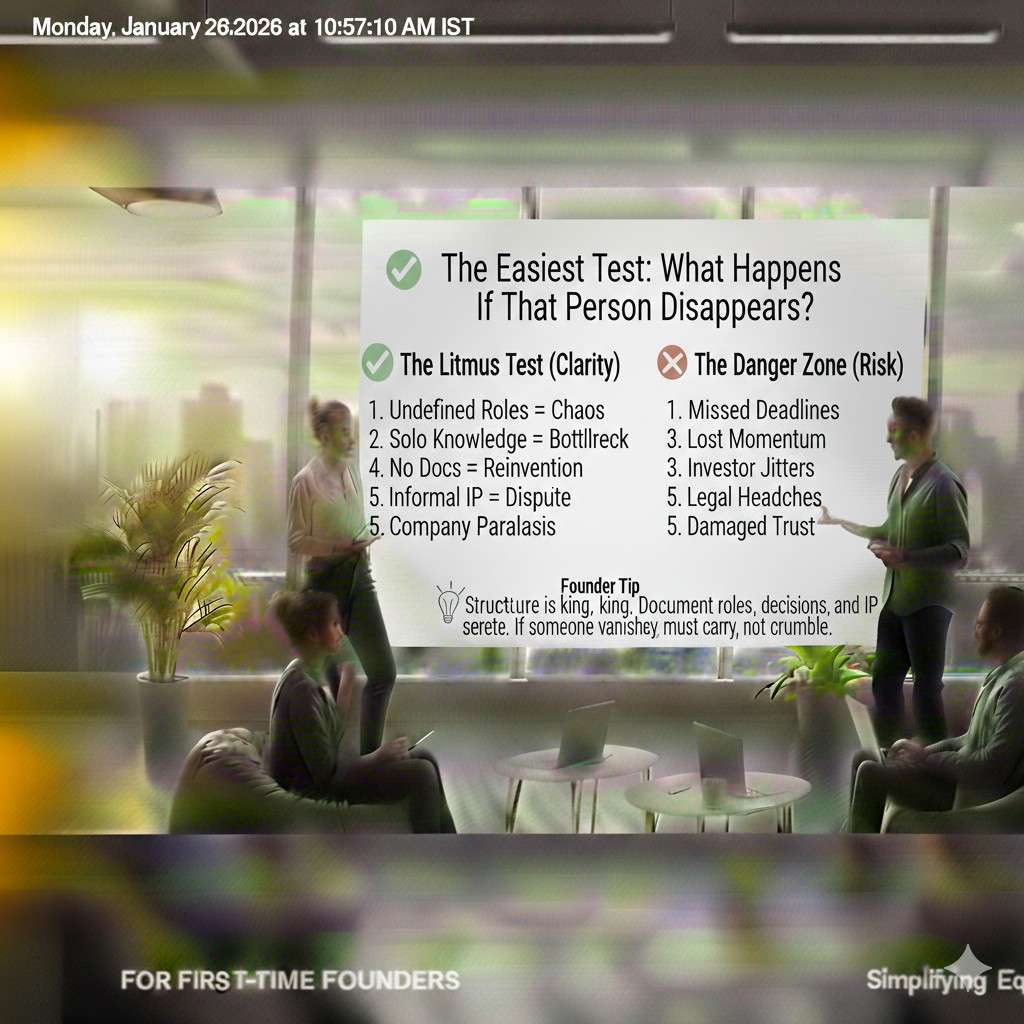

The easiest test: what happens if that person disappears?

Imagine each founder is gone for 60 days. What breaks first? What slows down badly? What becomes impossible?

If the technical founder disappears early, many deep tech startups stop breathing. The product does not move, the prototype does not improve, and key technical decisions stack up.

If the non-technical founder disappears early, the product may still advance, but customers may not be interviewed, pilots may not start, hires may not close, and fundraising may drag. The startup may still die, just more slowly.

This is not about who matters more as a person. It is about what the company needs now, and what it will need later.

Define the work in plain terms, not vague labels

Technical work is not just “writing code”

In deep tech, technical work often includes system design, architecture, model training, evaluation, integration, reliability, data work, deployment, testing, and security. It includes knowing what not to build, which saves months.

It can also include invention. If the technical founder is creating a new method, a new pipeline, a new hardware approach, or a new combination of known parts that creates a unique result, that may be patentable. That matters because it can become a real asset on the balance sheet of your company story.

This is one reason Tran.vc exists. Many teams build incredible inventions and never protect them early. Tran.vc helps you convert real technical advantage into IP, with up to $50,000 in in-kind patent and IP support. Apply anytime at https://www.tran.vc/apply-now-form/.

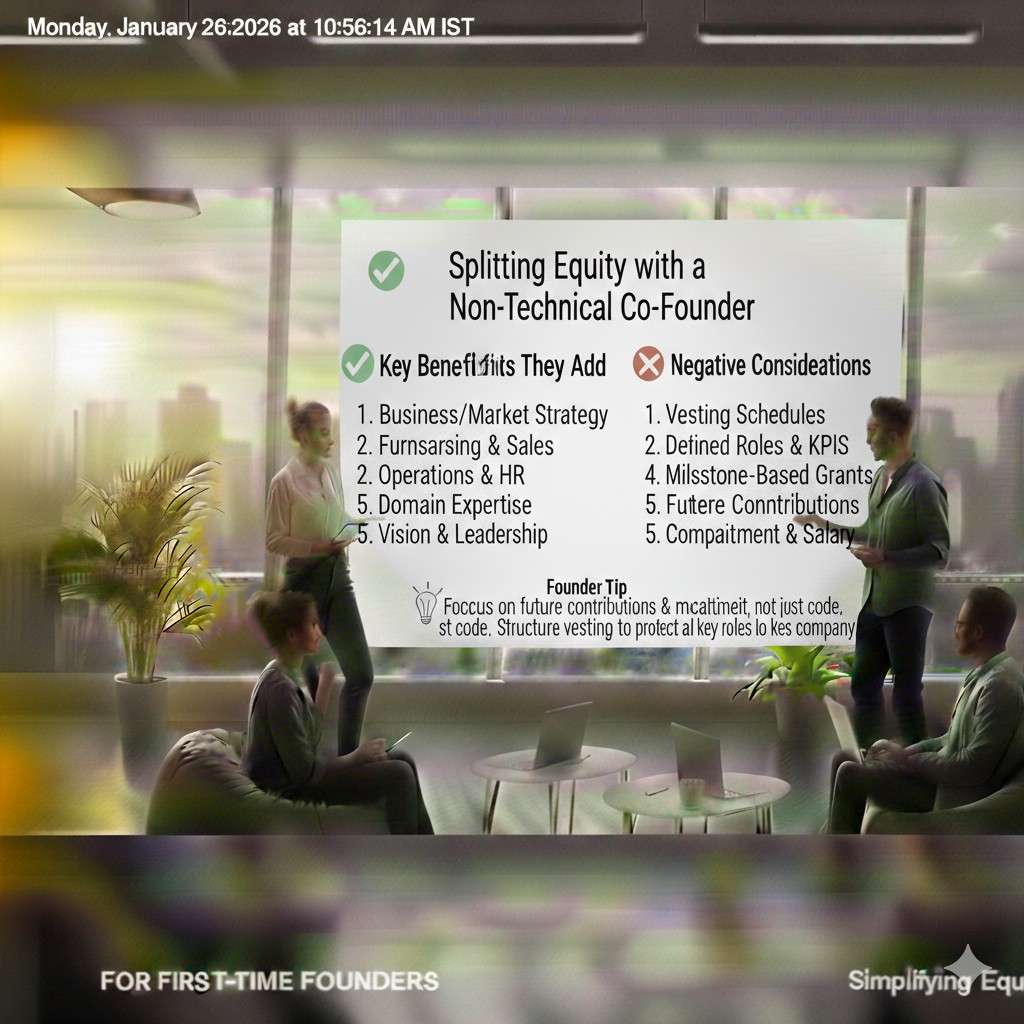

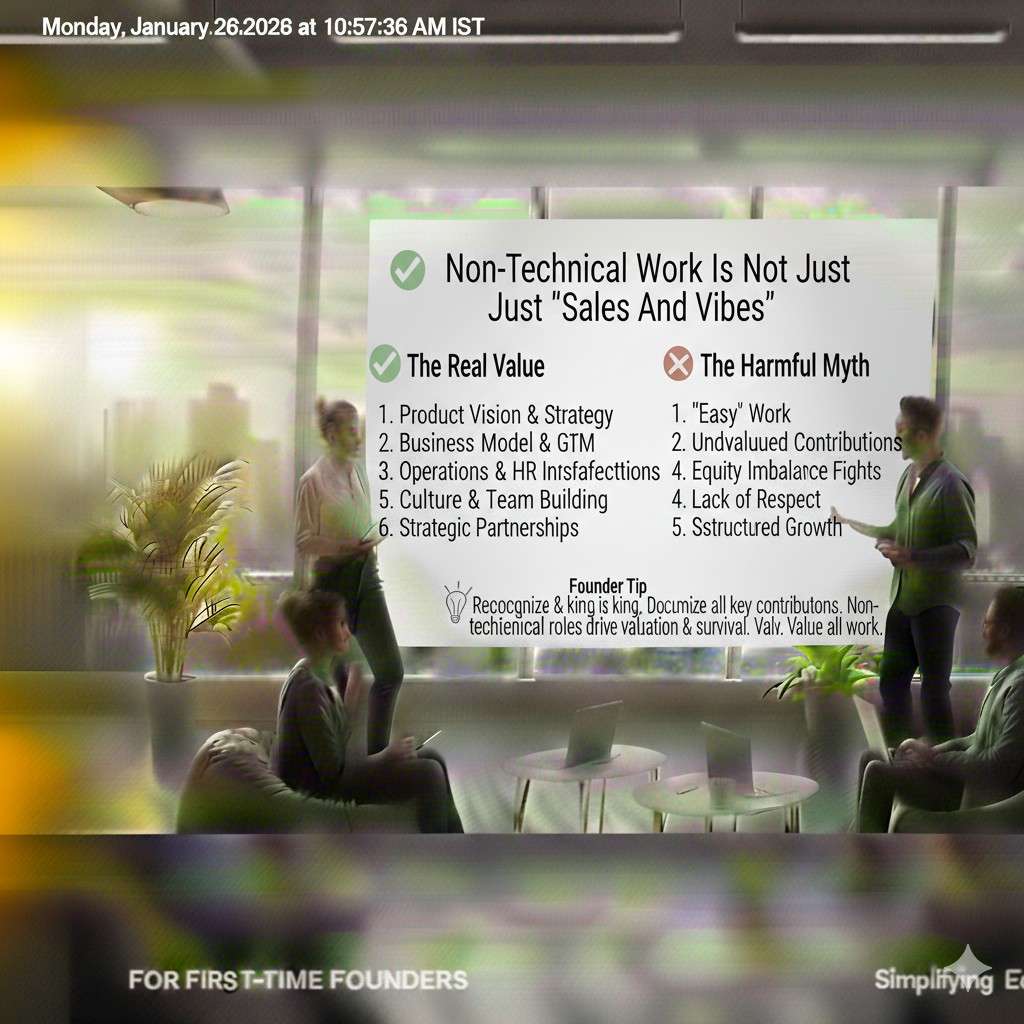

Non-technical work is not just “sales and vibes”

Strong non-technical founders do far more than pitch decks. They learn the market fast, they speak to customers weekly, and they write the message in a way that makes people lean in.

They build trust with early users and partners, which is hard and slow. They recruit talent, close advisors, manage investor updates, set up operations, and handle the messy work that keeps the team moving.

Most importantly, the best non-technical founders reduce risk. They reduce the risk of building the wrong thing. They reduce the risk of running out of money. They reduce the risk of being invisible.

Use a practical frame: equity equals risk plus responsibility plus time

Risk: who is giving up what, right now?

Risk is not just about how hard the work is. It is about what each person is putting on the line.

Is one founder quitting a high-paying job today while the other is staying employed for six months? Is one founder moving cities, taking visa risk, or burning personal savings? Is one founder taking on personal debt?

These details matter because they shape commitment. A founder taking bigger personal risk early may reasonably ask for more equity, especially if the other founder is not matching that risk at the same time.

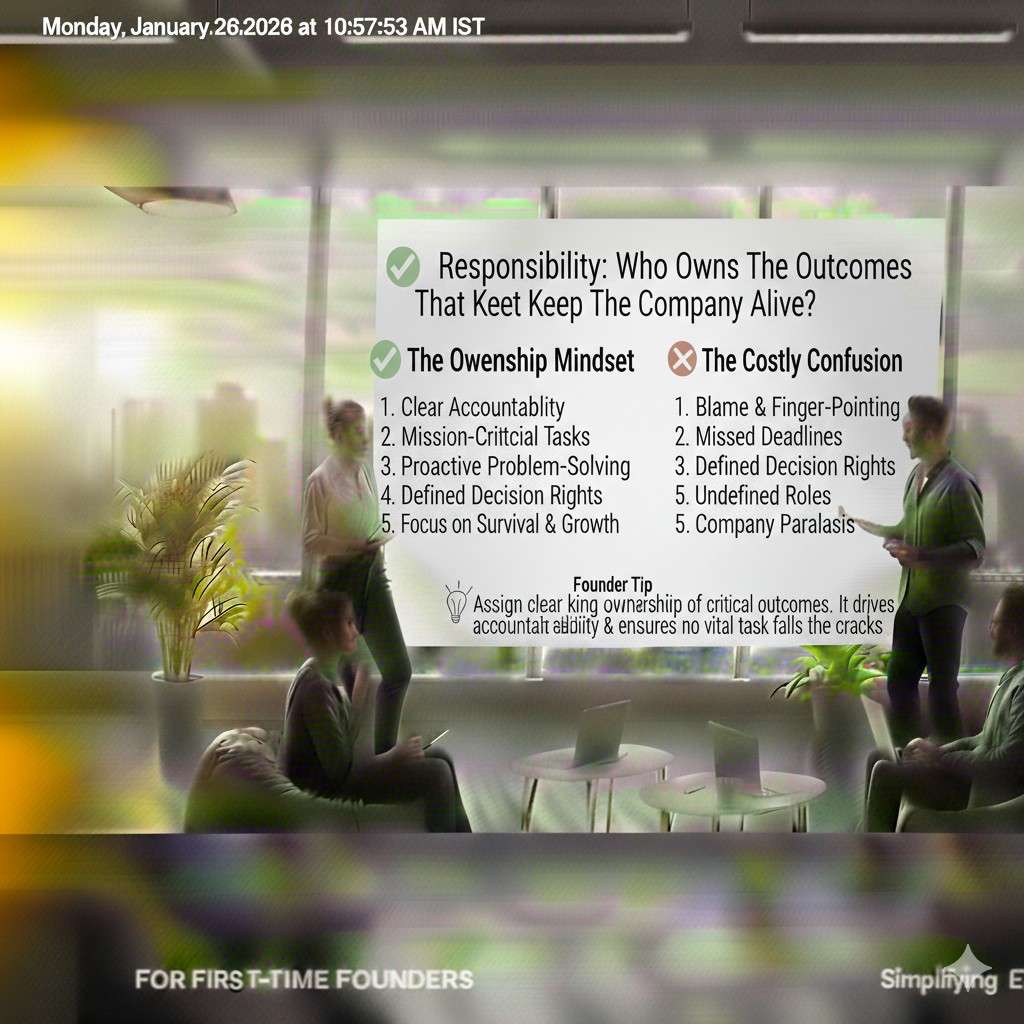

Responsibility: who owns the outcomes that keep the company alive?

Responsibility means the company fails if you do not deliver. In a deep tech startup, technical responsibility may include building a prototype, hitting performance targets, and making the system stable enough for a pilot.

Non-technical responsibility may include getting ten customer calls per week, turning those into a clear problem statement, landing a pilot, and creating a path to revenue. It may also include fundraising, but fundraising should not be treated like magic. It is a process, and it can be measured.

If both founders are truly responsible for survival outcomes, equity should reflect that. If one founder is mostly “support,” the equity should show that too.

Time: how many hours and how many years will each person commit?

Some partnerships fail because the time commitment was never stated. One founder expects full-time intensity, and the other thinks part-time is fine until funding arrives.

Equity should match real time input. If a non-technical founder is part-time, the split should not look like a full-time founder split. If they will become full-time later, you can design equity to increase when that happens, instead of guessing.

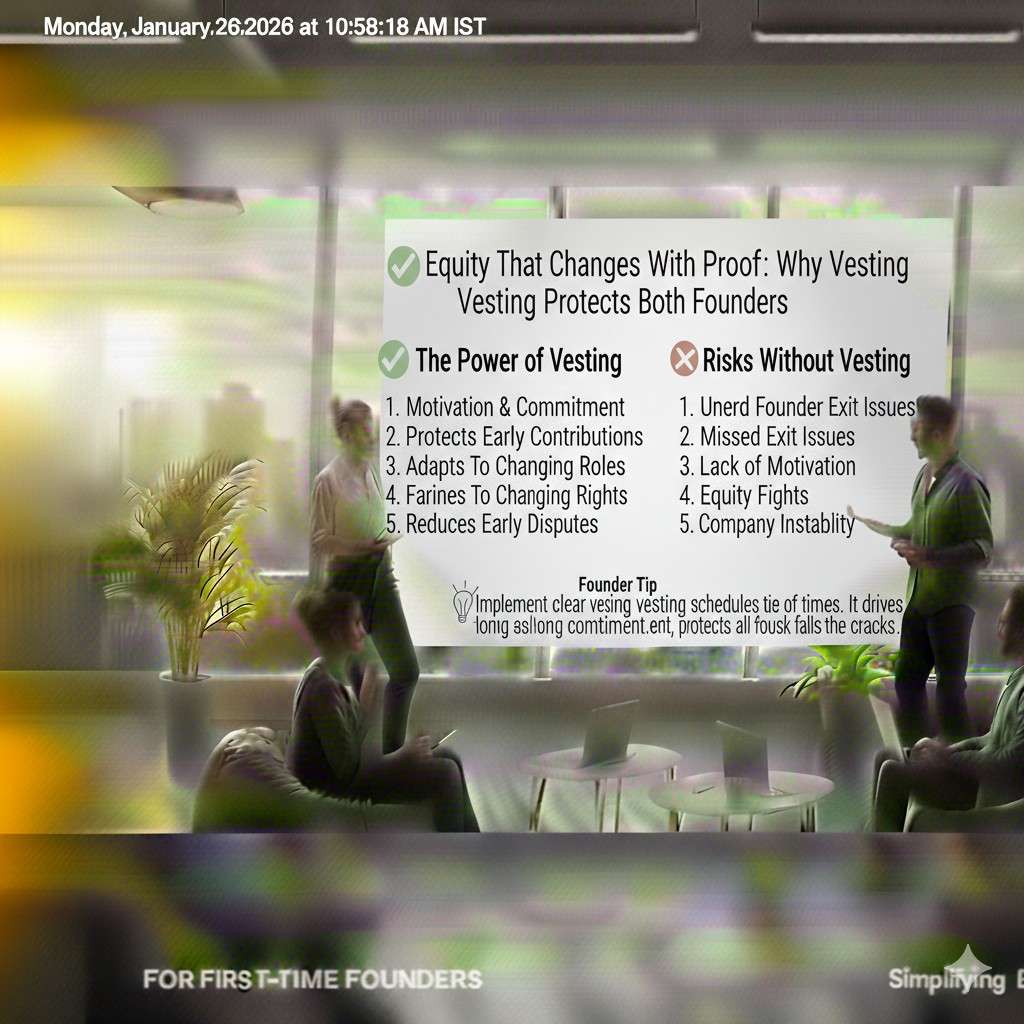

Equity that changes with proof: why vesting protects both founders

Vesting is not distrust, it is basic safety

Vesting is a way to make sure equity is earned over time. It protects the company if someone leaves early. It also protects the remaining founder from carrying the company while still “paying” the other person in ownership.

Most founder equity is set up with vesting. It is normal. If someone refuses vesting, it is a warning sign. Not because they are bad, but because they may not understand what a real founder agreement looks like.

The non-technical co-founder should expect the same standard

A common mistake is giving the technical founder vesting but giving the non-technical founder immediate ownership, or the reverse. Both should be treated with the same structure, unless there is a very special reason.

If your non-technical co-founder is truly a co-founder, they should be comfortable earning equity through real work over time. A strong founder does not fear vesting because they plan to stay and build.

We’re now in the first section and moving toward the next major part, where I’ll get very tactical about common split patterns, what to do when one founder brings the idea, how to value customer traction vs product work, and how to handle “future promises” without blowing up trust.

Common equity split patterns that actually hold up

Why “equal effort” is not the same as “equal equity”

Two founders can work just as hard and still not bring the same type of leverage at the same time. Early on, leverage is about what removes the biggest risk first. In many robotics and AI startups, the biggest early risk is simple: can this thing work at all, in the real world, at a level that customers will pay for?

When the technical founder is the one turning uncertainty into proof, the company’s survival often depends on that work more than anything else. That does not mean the non-technical founder is less important. It means timing matters. The value of non-technical work can explode later, once there is something to sell and validate.

So instead of trying to measure “effort,” measure what risk each person is killing, and when. That mindset makes the split less emotional because it is tied to the company’s needs, not ego.

The “technical-heavy early” split

This is the most common pattern in deep tech when the product does not exist yet. The technical founder gets more equity because they are building the core system, making foundational decisions, and often inventing new methods along the way.

The non-technical founder still gets meaningful equity, but not equal, because the company can often survive longer without go-to-market than it can survive without the ability to ship a working prototype. The non-technical founder’s equity can also be designed to grow later when traction milestones are met, instead of guessing upfront.

This pattern tends to work well when the non-technical founder is strong, but the startup is not ready for aggressive selling yet. It also reduces the risk that the technical founder feels trapped doing the hardest early work while “splitting the prize” evenly.

The “equal founders” split

This can work when both founders are truly all-in, both own make-or-break outcomes, and both have a track record of execution. It also works when the non-technical founder brings something hard to replace right away, like deep domain access, a strong customer channel, or a clear path to paid pilots.

In these cases, the non-technical founder is not just “the pitch person.” They are the person who can get the company into real environments, with real users, fast. If that access is rare and immediate, equal equity may be reasonable.

The key is to be honest about whether that access is real, repeatable, and close in time. Promises of “I can introduce you to people” are not the same as a signed pilot or a committed buyer.

The “prove it then split it” structure

Some teams do not choose a final split on day one. They set a temporary split and commit to revisiting it after a short period, usually when there is proof of execution.

This can be useful when you have a new partnership and limited trust so far. It can also prevent long debates that block building. But it only works if you write down what “proof” means, and you set a date to decide.

Without a clear checkpoint, this structure becomes a slow-motion conflict. The technical founder keeps building, the non-technical founder keeps “working on strategy,” and nothing ever triggers a final agreement. If you use this approach, keep it tight and concrete.

When one founder brings the idea

Ideas do not earn equity by themselves

This can be a sensitive topic, but it is better to say it plainly. Most startup ideas are not unique. Even in deep tech, multiple smart teams can arrive at similar concepts. What is rare is execution, and what is very rare is execution plus defensibility.

Equity should be paid for building, not for thinking. If one founder says, “It was my idea, so I deserve more,” the right response is calm and simple: the company will be valued by what we ship, what we learn, and what we protect.

If the “idea person” is also doing heavy work to turn it into reality, then they are not just an idea person. They are a builder in their own way. But the idea alone is not a reason to tilt the split.

Domain knowledge can matter, but only if it changes outcomes

There is a real case where non-technical input can be worth a lot early: deep domain knowledge that prevents wasted building. If your non-technical co-founder has spent years inside the industry you are selling into, they may save you from building the wrong thing.

They may also be able to get high-quality customer calls quickly, because people trust them. That can sharply reduce market risk, which is one of the two biggest risks in any startup.

But again, the test is outcomes. Are they producing clear insights, paid pilots, or strong commitments? Or are they mainly offering opinions and broad claims? Reward the outcomes, not the story.

How to value “customer work” versus “product work”

Customer work must be visible, not vague

Technical work is easy to see because there is a repo, a prototype, and a measurable output. Non-technical work often becomes vague because it happens in calls, meetings, and messages.

That is why non-technical founders must learn to make their work visible without turning it into theater. They should document what they learn from customers, show patterns, and turn those patterns into decisions that change what the team builds.

If all the customer work leads to no changes, no clear roadmap, and no measurable progress toward revenue, it becomes hard to justify equal equity. Not because the calls were useless, but because the loop is not closing.

A simple way to judge go-to-market value

In early-stage deep tech, go-to-market value usually shows up in four forms: clarity, proof, pull, and cash.

Clarity means you now know exactly who the customer is, what problem hurts, and what they would pay for. Proof means the customer is willing to test your solution in their environment. Pull means the customer is asking for the product, not just politely listening. Cash means they pay, even if it is small.

A strong non-technical co-founder should be driving you from fog to clarity, then from clarity to proof, then from proof to pull, then to cash. If that progression is happening, equity can be defended with confidence.

Fundraising as a contribution: what counts and what does not

Fundraising is not a substitute for building

Many non-technical founders believe they can “raise the round” and that alone should earn them equal equity. In reality, in robotics and AI, fundraising is usually easier when there is technical proof and a story backed by defensible IP.

Investors want evidence. They want to know the tech works, the market is real, and the advantage is protected. That is why early IP strategy can matter so much. It gives investors a reason to believe your lead is real, not temporary.

Tran.vc is built around that idea. Instead of telling founders to wait until later to protect their inventions, Tran.vc helps you build IP early through up to $50,000 in in-kind patent and IP services. If you want to build with leverage, you can apply anytime at https://www.tran.vc/apply-now-form/.

What “good fundraising work” looks like early

Good fundraising work is not just taking meetings. It is preparing the company to be fundable. That includes tightening the narrative, building a list of the right investors, running a clean process, and collecting signals from the market.

It also includes managing the company so the technical team is not constantly distracted. A strong non-technical founder can protect focus by handling updates, scheduling, follow-ups, and investor questions.

But even then, fundraising should not be the only pillar holding up their equity claim. If fundraising is the plan before product proof, the startup can drift into a cycle where the story gets rehearsed more than the product gets built.

The “future promises” trap

Promising future work is not the same as doing current work

One of the most common equity conflicts happens when a non-technical co-founder says, “Once we have a prototype, I will be able to sell it easily.” That may be true. But it is not happening today.

If you give full equity today based on work that might happen later, you are paying in advance. Sometimes that works, but it is risky. The better approach is to connect extra equity to future milestones.

This is not punishment. It is alignment. It says: we believe you will do this, and when you do it, you earn more ownership.

How to make future equity feel respectful

Many founders fear milestone-based equity because it can feel like one founder is judging the other. The way to avoid that is to design milestones together, and make them about the company, not the person.

For example, instead of “you must sell,” the milestone can be “the company must secure two paid pilots.” The non-technical founder may lead that effort, but it is framed as a shared company win.

When milestones are written well, they reduce fighting because both founders can see what success looks like. It becomes less about opinions and more about results.

We’re now past another major chunk. Next, I can cover the most practical part: how to have the conversation without damaging trust, what to put in writing, how to handle vesting and cliffs in plain terms, and how to deal with tricky cases like part-time founders, uneven cash contribution, and founder couples.