If you are building a startup outside the United States, and a US investor shows interest, it can feel like a win and a warning at the same time.

A win, because US capital can unlock speed, trust, and reach.

A warning, because once US money enters the cap table, the “rules of the game” change in quiet but serious ways. Not always bad. Often helpful. But different.

This guide is here to make those changes easy to see before you sign anything. I am going to keep this simple, practical, and real. No fancy terms. No vague advice. Just what actually changes when a US investor invests in a non-US startup, and what you can do to stay in control while still getting the upside.

And if you want Tran.vc to help you build an IP base that US investors respect from day one—so you raise with leverage, not stress—you can apply anytime here: https://www.tran.vc/apply-now-form/

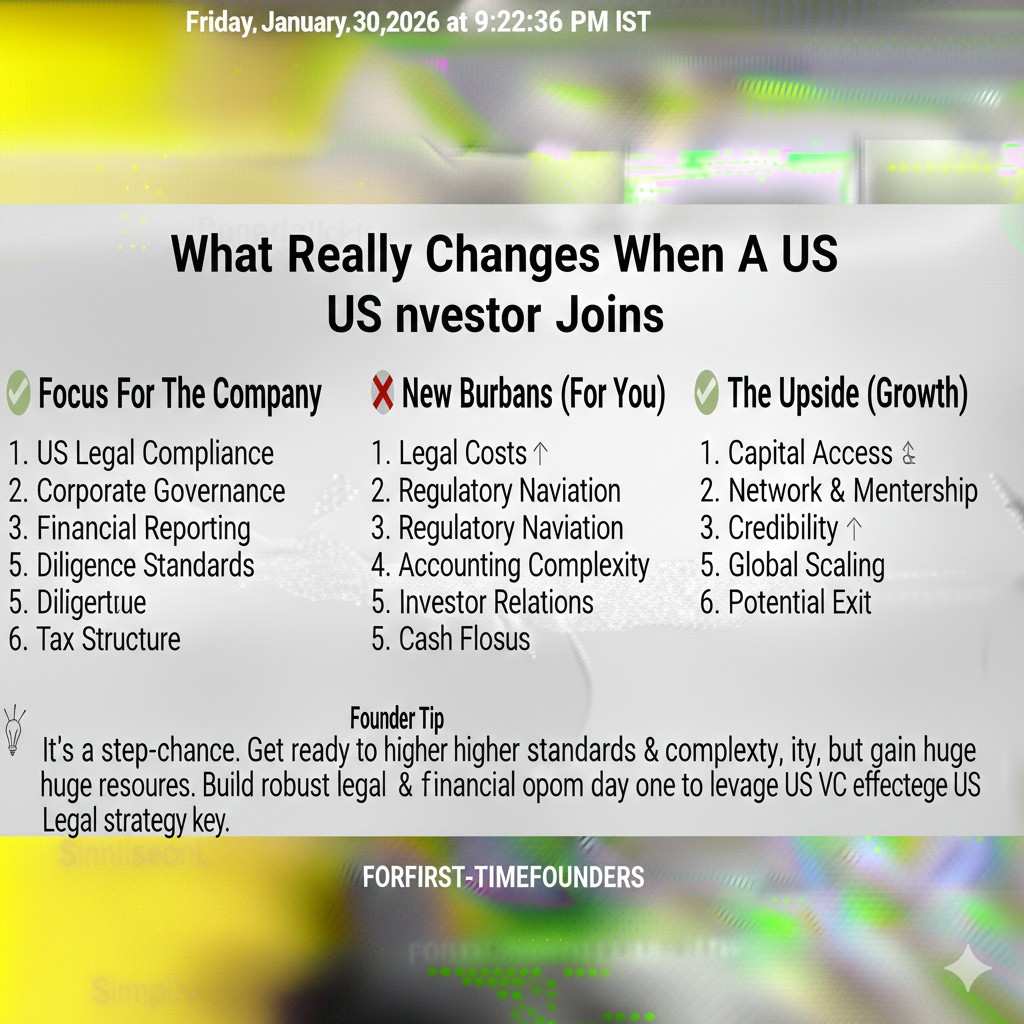

What really changes when a US investor joins

Most founders think the big change is the money. It is not.

The big change is that your company becomes “investable” under a US lens. That lens has its own habits. Its own fears. Its own legal and tax guardrails. And its own idea of what “clean” looks like.

A US investor will still care about your product, your traction, and your team. But they will also care deeply about structure. Not because they want to control you. Because they want to avoid surprises that can break a future round, block an exit, or trigger tax trouble.

So the first shift is this: your company stops being only your local company. It becomes a cross-border asset that must fit into US deal systems.

That shows up in five main areas:

- where the company is formed and where it should be formed

- how shares, options, and founder ownership are recorded

- how IP is owned and how it moves across borders

- how money flows in and out, and what taxes might follow

- what reporting, compliance, and investor rights become normal

I will walk through each, but in a way you can act on.

1) Your company structure becomes a real topic, not a footnote

If you are incorporated outside the US, a US investor will quickly ask a simple question:

“Are you staying where you are, or are you flipping to the US?”

That word—“flip”—usually means setting up a US parent company (often Delaware) and making your current company a subsidiary under it, so the investor invests into the US parent.

This is common. But it is not always needed. And it is not always worth doing early. The right answer depends on your goals, your customers, your team location, and your future investor path.

Here is what changes in your day-to-day life the moment this question enters the chat:

You now have to think two steps ahead.

If you accept US money into a non-US entity, some US funds cannot do it at all because of their fund rules. Others can, but it may create tax or admin work they dislike. Some angels are flexible. Many institutions are not.

So the structure conversation is not about “what is best for you today.” It is about “what will not break the next round.”

This is why founders sometimes feel pushed into Delaware even if they are not ready. The investor is not being dramatic. They are protecting future deal flow.

But here is the part founders miss:

A Delaware company is not a magic badge. It can also create extra cost, extra filings, extra legal work, and extra mistakes if your team is not ready to run a cross-border setup.

So you want to handle it like a serious product decision: based on tradeoffs, not vibes.

A clean way to think about it is to ask:

Will US investors likely lead your next round too?

Will your main market be the US in the next 12–24 months?

Will you need US talent, US enterprise sales, or US partnerships soon?

Will your IP strategy benefit from US filings early?

If the answer to most of those is “yes,” a US parent can be a good move. If most are “no,” you may be able to delay, raise from angels, or take US money in a way that does not force a full flip right now.

But even if you delay, you must still plan for the flip. Because if you do it later in a rush, it gets messy. The messy version costs more, takes longer, and scares the next investor.

This is also where Tran.vc fits naturally. Because if your structure is going to change later, your IP decisions today must not create traps. You can apply anytime here: https://www.tran.vc/apply-now-form/

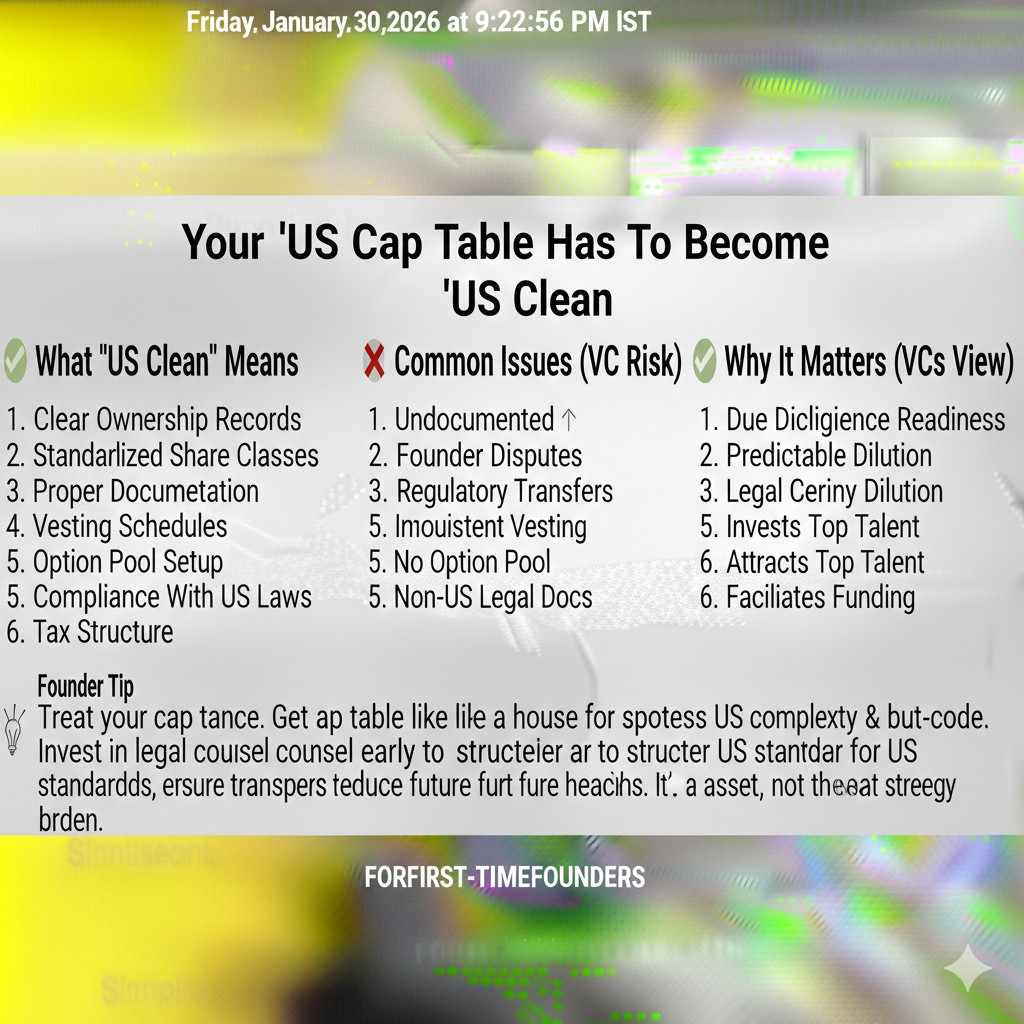

2) Your cap table has to become “US clean”

Every country has its own way of tracking ownership. Some are strict and simple. Some are paper-heavy. Some rely on informal agreements early.

US investors, especially those who have done many deals, expect a cap table that answers basic questions fast:

Who owns what today?

What did each person pay?

When did they buy?

Are there side deals?

Are there promises for shares that are not documented?

Are options granted, and if so, under what plan?

If any of those answers are unclear, the deal slows down.

This is not because investors love paperwork. It is because unclear ownership can explode later. A co-founder disagreement. An early contractor claiming equity. A “handshake” advisor grant. A missing assignment agreement. These things can turn a future round into a legal fight.

When US money is involved, investors will push harder to make the cap table boring. “Boring” is a compliment in financing.

So what changes?

You cannot treat early equity like a friendly side agreement anymore. You have to treat it like a legal asset.

A few common cross-border issues show up here:

Founder shares that are not properly issued.

Some founders “agree” they own 50/50, but the company never issued shares correctly. When a US investor asks for proof, things get awkward.

Vesting is missing or informal.

In many places, vesting is less common early. In the US, it is almost assumed. If there is no vesting and a founder leaves, your cap table can get stuck forever.

Contractor equity promises.

A contractor might believe they own part of the company because of a chat message or a short email. US investors will not accept this risk.

Local option plan issues.

Option rules differ by country. What is standard in one place can be painful in another. A US investor does not want your option plan to create tax harm for employees.

The practical move here is not to panic. It is to do a “cap table cleanup” before the US investor is deep in diligence.

That cleanup usually includes:

- making sure shares were issued correctly

- making sure every founder and early contributor signed invention and IP assignment agreements

- documenting advisory grants properly

- putting vesting in place (even if it is not perfect, it must be real)

- creating a clear option plan framework for future hires

I am keeping this short on purpose. Later in the article, I can walk through what “cap table cleanup” looks like in real steps, without turning it into a checklist wall.

For now, remember: US investors want ownership clarity more than they want a fancy pitch.

And they will often judge founder maturity based on how quickly you can produce clean answers.

3) IP becomes the main question, not a side question

If you are building in robotics, AI, or deep tech, and you bring a US investor in, the IP talk gets louder.

A lot louder.

Here is why: cross-border companies create IP risk. Not because you did anything wrong, but because IP can end up owned by the wrong entity or the wrong person by accident.

US investors worry about three things:

First, who owns the core invention.

Second, where that IP sits (which company holds it).

Third, whether it is protected in the places that matter.

This is where many non-US startups lose leverage.

They build something real. They have an advantage. But they did not lock it into IP early. Or they filed late. Or they filed in the wrong name. Or a contractor wrote key code without signing proper assignments.

Then a US investor asks, “Can you show me your IP chain of title?”

And the founder says, “Our engineer made it, but it’s ours.”

That is not an answer.

A US investor does not want to “believe” you own it. They want proof.

This is also why Tran.vc exists in its current model. Because early-stage founders do not need more advice. They need real IP work done—strategy, filings, and clean ownership—before the big money rounds.

Tran.vc invests up to $50,000 in-kind in patent and IP services. That means you get the work product without giving up control early or burning cash that should go to building.

If you want that kind of support, you can apply here: https://www.tran.vc/apply-now-form/

Now, back to what changes.

When a US investor comes in, they often push for:

- a clear invention assignment from every person who touched core tech

- IP owned by the right entity (often the parent that will raise money)

- patent strategy that matches your market and threat model

- proof you are not infringing obvious third-party IP, especially in the US market

- clarity on open-source use, because license mistakes can create ugly surprises

For AI startups, one more topic gets serious: data rights.

If your model is trained on data you do not have rights to use for commercial purposes, US investors will get nervous fast. Not because they want to slow you down. Because lawsuits and platform bans are real threats.

For robotics, investors will ask about:

- patent coverage on key mechanical designs, sensing methods, and control systems

- whether your designs are easy to copy once seen

- whether your supply chain partners have signed agreements that protect your designs

- whether your manufacturing steps leak your secret sauce

These questions sound heavy, but they are manageable if you start early.

The key shift is this:

Before US money, many founders treat IP like “we will handle it later.”

After US money, IP becomes part of your fundraising story and your deal safety.

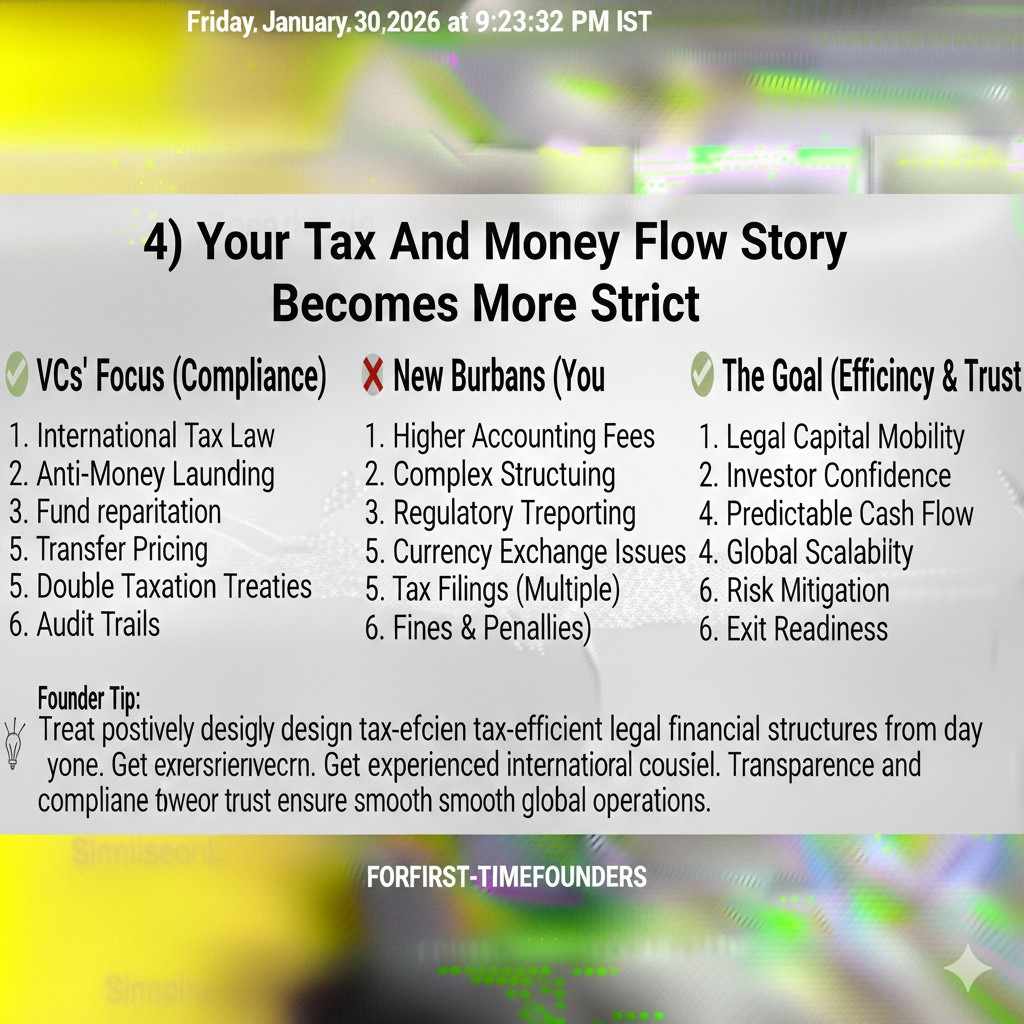

4) Your tax and money flow story becomes more strict

The next big change is how money moves.

A US investor will care about things like:

- how they wire money in

- what entity they are investing into

- whether there are withholding taxes

- whether there are “bad” tax outcomes for the investor because of your structure

- whether your company can pay them back in an exit without extra friction

This is where founders get surprised, because the investor may start talking about tax forms, reporting, and rules that feel unrelated to building the product.

But it matters. A lot.

Some structures cause US investors to have extra reporting duties every year. Some structures can create tax exposure they do not want. Some structures can limit what they can own.

And this is one reason US investors often prefer a US parent.

The moment you bring in US money, you must expect:

- more questions from lawyers

- more need for clean financial records

- more pressure to separate company funds from personal spending

- more demand for clear contracts for revenue, contractors, and suppliers

If you are early, you might not have strong finance ops yet. That is fine. But you should not pretend. Instead, you set up basic hygiene quickly.

Simple hygiene wins trust:

You keep clean books.

You keep contracts signed.

You keep founder expenses documented.

You keep payroll and contractor payments clear.

And you do not move money between entities casually, because cross-border transfers can create tax issues.

Even if you are tiny, your systems must look like they can grow.

That is what US investors pay for: the ability to scale without chaos.

5) Investor rights and “US style” expectations become normal

US investors often invest using standard documents and standard rights. Even angels tend to follow common patterns.

What changes for you is not only what you sign, but what becomes “normal” in your relationship with investors.

US investors tend to expect:

- regular updates

- clear reporting on spend, runway, and hiring

- a professional approach to governance (board, approvals, consents)

- the ability to protect their downside in a bad case

- strong clarity around future fundraising rules

This does not mean they will run your company. Many are founder-friendly.

But it does mean you must operate like a company that can pass diligence again and again.

And that is actually a good thing, because repeatable diligence is how you raise faster later.

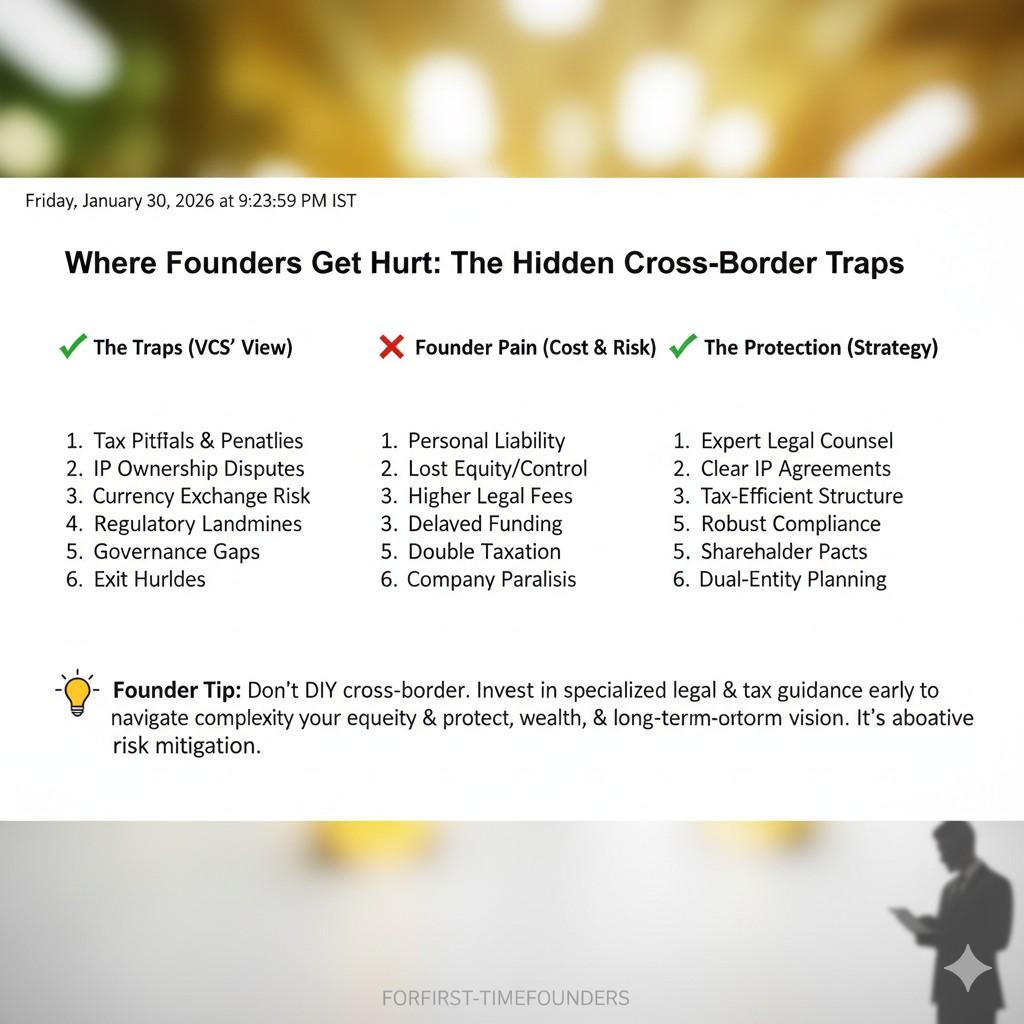

Where founders get hurt: the hidden cross-border traps

Now let us talk about the parts that cause pain. Not theory. Real traps.

One trap is doing a flip too late.

If you wait until a priced round to flip, and you have many shareholders, advisors, and small grants, the legal work can become a long mess. Each person must sign documents. Some people are slow. Some are unresponsive. Some are upset. And suddenly your financing timeline is at risk.

Another trap is moving IP without thinking.

A founder may move IP to a US entity in a hurry to satisfy an investor, without checking local rules, local taxes, or whether that move creates problems with government grants, local R&D credits, or existing contracts.

Another trap is misaligned option plans.

If you hire in multiple countries, your equity plan must fit each place. If you copy-paste a US option plan into a country where it triggers ugly taxes for employees, you might lose great hires. Or create employee anger later when taxes hit.

Another trap is confusing “US investor interest” with “US market readiness.”

Sometimes founders chase US investors before they are ready to sell in the US, support US customers, or compete in US legal realities. US money is powerful, but it also raises the bar.

This is why your planning must match your real stage. Not your dream stage.

A simple way to prepare before you even talk to US investors

Here is the good news: you do not need to be perfect. You just need to be prepared.

If you are a non-US startup and you want US investors later, you can do a few things now that create outsized leverage:

You make ownership boring and provable.

You make IP clean, assigned, and protected

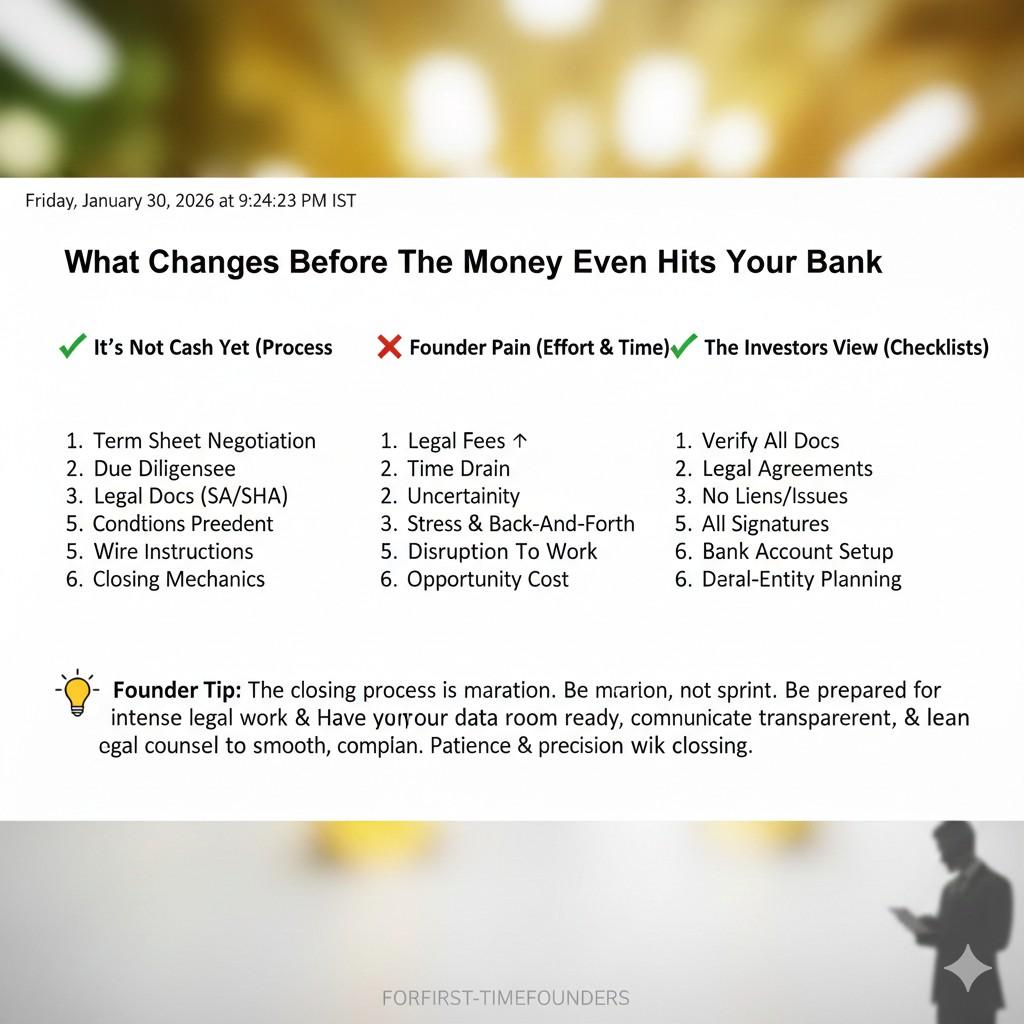

What Changes Before the Money Even Hits Your Bank

How investor behavior shifts early

Long before funds are wired, the tone of conversations changes once a US investor is involved. Questions become more precise and less forgiving. Investors start testing how you think, not just what you have built.

They pay close attention to how you answer basic questions. Clear answers signal maturity. Vague answers signal future risk. This is not about intelligence. It is about readiness.

Why diligence starts earlier than expected

US investors often begin light diligence even at the first serious conversation. They want to know if it is safe to keep talking. This means your structure, ownership, and IP story matter sooner than founders expect.

Founders who prepare early control the pace. Founders who wait often feel rushed and defensive. That difference alone can shape deal terms.

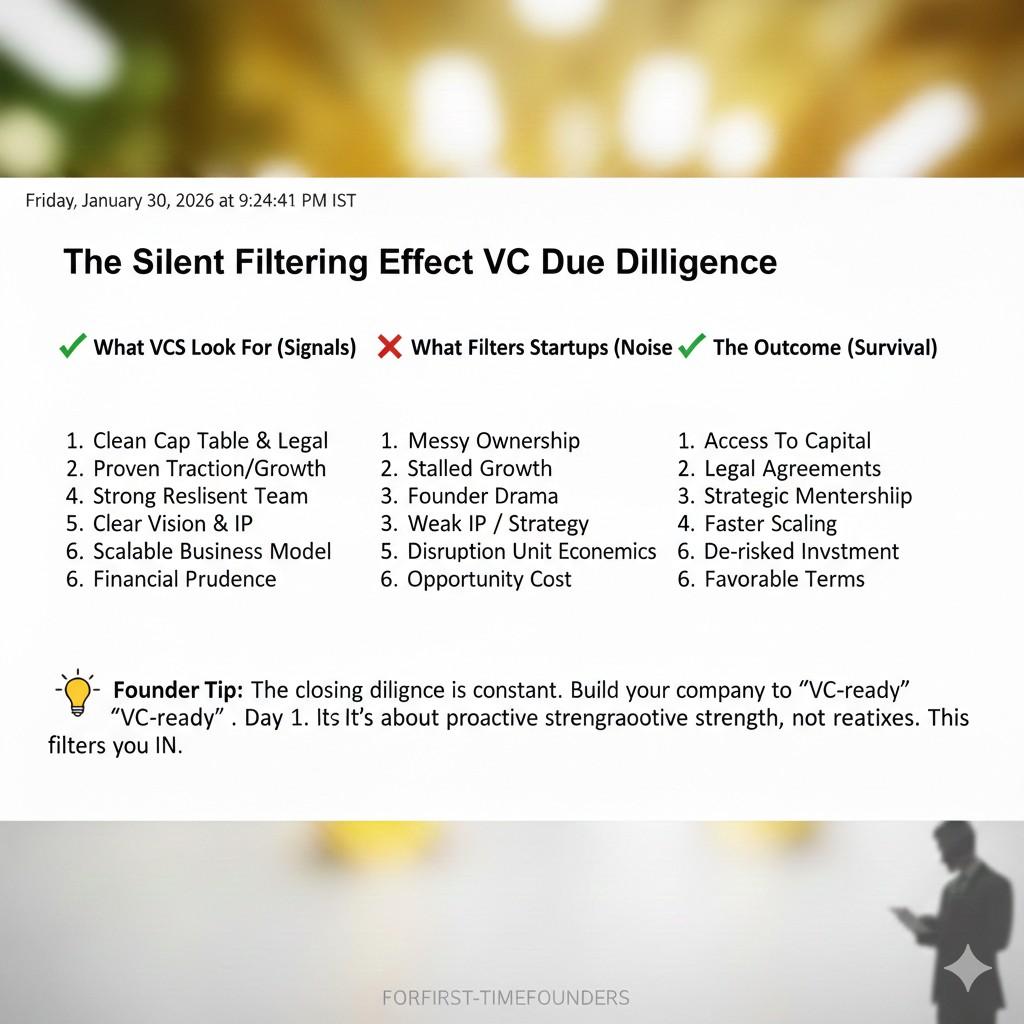

The silent filtering effect

Many US investors quietly filter deals before making offers. If your setup looks hard to fix, they may pass without explanation. Not because your product is weak, but because the cleanup cost feels too high.

This is why preparation is leverage. You may never see the deals you lost because of structure issues, but they do happen.

Company Structure Becomes a Strategic Asset

Staying local versus going US-first

Once a US investor is involved, your company’s location is no longer just a legal fact. It becomes a strategy question. Each option sends a signal about where you are going.

Staying local can show focus and cost control. Going US-first can show ambition and scale. Neither is wrong, but each must match your real plan.

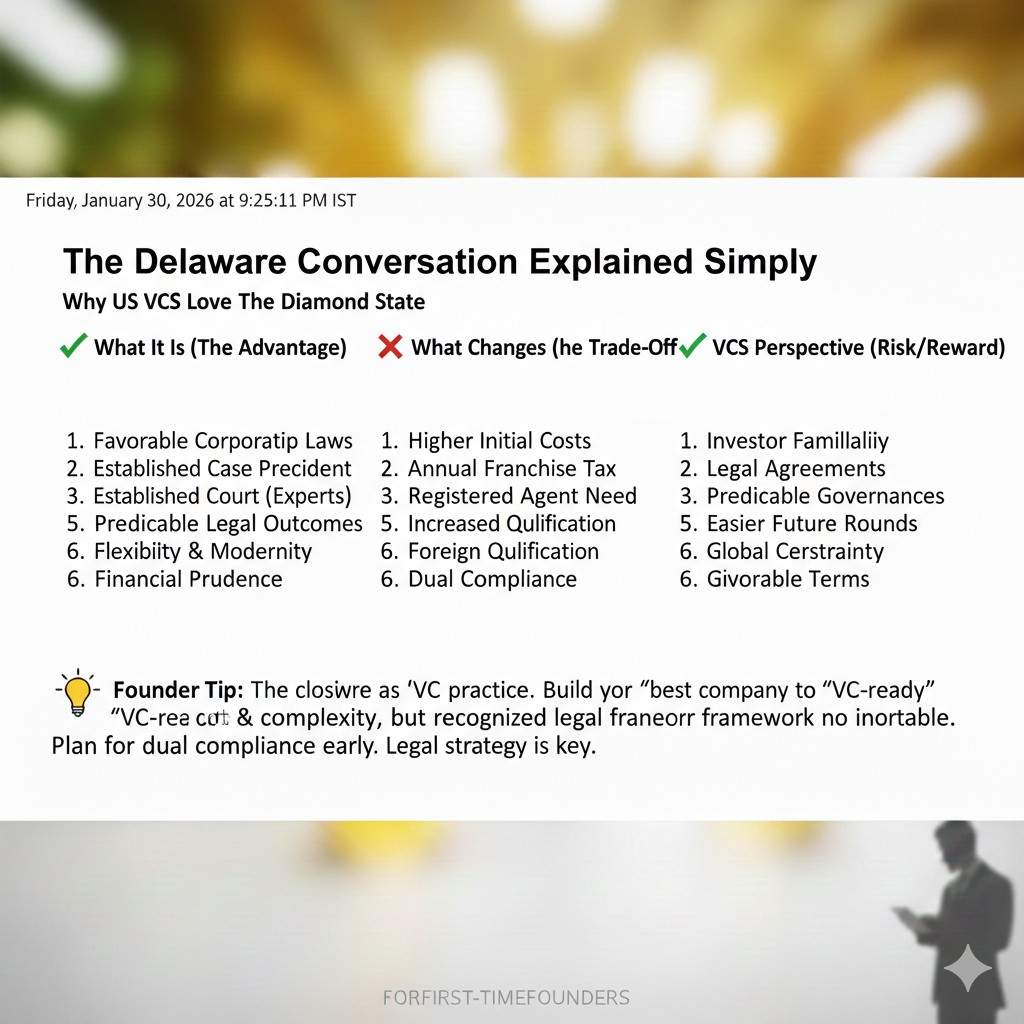

The Delaware conversation explained simply

Delaware is popular because US investors understand it well. The rules are familiar, the courts are predictable, and future investors feel comfortable.

That comfort can reduce friction later. But it also adds responsibility. A Delaware company must be maintained carefully, especially when paired with non-US teams.

Timing matters more than the decision itself

Founders often ask if they should flip now or later. The better question is whether they are ready to operate two companies cleanly.

Flipping too early wastes money. Flipping too late risks deals. The right time is when your growth path clearly points toward US capital and customers.