If you are building a tech startup, you will hear this phrase sooner than you expect: “You should do a Delaware flip.” It often shows up right after your first investor chat. Sometimes it comes from a lawyer. Sometimes it comes from another founder who already did it. And sometimes it comes from a spreadsheet-minded advisor who wants everything to look “standard.”

But a Delaware flip is not a badge. It is not a rite of passage. It is not always smart. It is a tool. Like any tool, it can build or break things depending on timing and fit.

This article is here to make the decision feel clear. Not “legalese” clear. Real-world clear.

A Delaware flip is usually when your current company (often formed outside the U.S., or formed in a U.S. state other than Delaware) becomes owned by a new Delaware corporation, with the founders’ shares moving up into that new Delaware parent. The Delaware company becomes the top company. Your old company becomes a subsidiary. People call it a “flip” because the ownership structure flips upward.

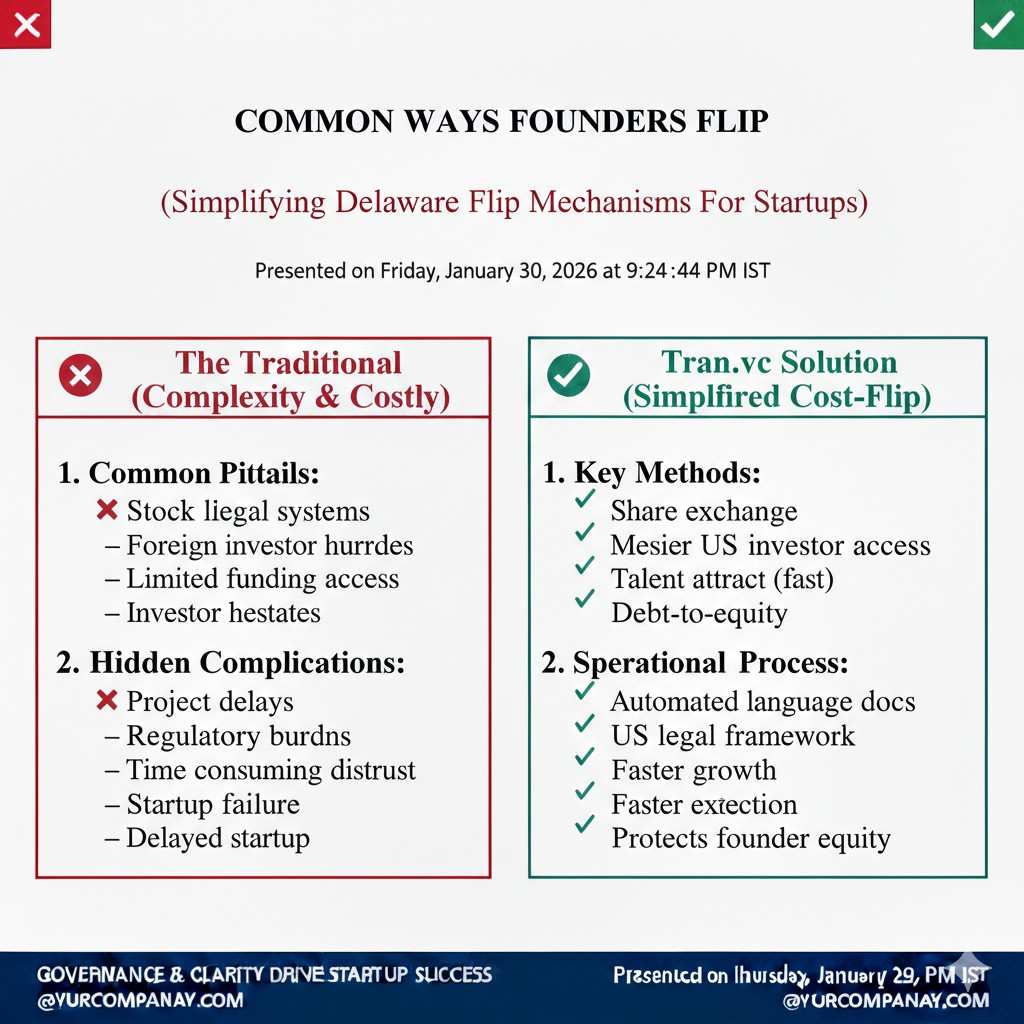

Founders do it for one main reason: fundraising. Many U.S. investors want to invest in a Delaware C-Corp. Delaware is familiar. The rules are known. Paperwork is predictable. They have seen it a thousand times. And when they are trying to move fast, predictable wins.

But here is the truth most people skip: a Delaware flip is not just paperwork. It touches your taxes, your IP, your employee equity, your contracts, your banking, and your long-term control. It can create hidden costs. It can also create a clean platform for scale if you do it at the right moment.

And because Tran.vc works with deep tech founders—robotics, AI, hard science—we see a unique twist: your IP is often your entire company. Your patents, your core algorithms, your training methods, your control systems, your sensor fusion, your edge inference stack, your data pipeline—this is what makes investors lean in. A flip that is done carelessly can muddle who owns what, where it was invented, and which entity can file and enforce patents. That is not a small issue. That is the company.

So we will walk through the decision in plain words:

- What a Delaware flip really is, and what it is not

- When it helps you raise money faster, hire faster, and scale cleaner

- When it hurts—through taxes, messy cap tables, IP confusion, and control drift

- How to time it, so you do not pay for “standard” before you need it

- The exact prep steps you can do now so the flip (if you do it) is simple, fast, and safe

One more thing: this is not legal advice. It is founder advice. The goal is to help you ask the right questions early, so your lawyer work is smaller, cheaper, and less stressful.

If you are a technical founder and you want to build a real moat early—before you chase a huge seed—Tran.vc can help. Tran.vc invests up to $50,000 in-kind in patent and IP services so you can protect what matters and raise with leverage. You can apply anytime here: https://www.tran.vc/apply-now-form/

The Delaware Flip: When It Helps and When It Hurts

Why this topic matters right now

A Delaware flip often feels like a “next step” you must take to be taken seriously. Many founders hear it early, sometimes before they even have a stable product.

That pressure can lead to rushed choices. And rushed choices around company structure can create years of clean-up work later. This is why it is worth slowing down for one hour and getting the logic straight.

If you build in robotics or AI, the risk is even higher. Your value is not only in revenue. It is in the technical edge you own and can defend. A flip done at the wrong time can blur IP ownership and weaken your story when investors finally lean in.

If you want help building an IP-backed foundation early, Tran.vc can step in with up to $50,000 in in-kind patent and IP services. You can apply anytime here: https://www.tran.vc/apply-now-form/

A simple promise for this guide

This guide will not talk in circles. It will not pretend every company must do the same thing.

Instead, it will help you decide based on your stage, your customers, your team location, and your next funding step. It will also help you avoid the most common traps that show up only after the flip is “done.”

A quick definition in plain words

A Delaware flip usually means you create a new company in Delaware, and that new company becomes the owner of your current company. Your old company still exists, but it becomes a subsidiary under the Delaware parent.

Founders and early holders swap their old shares for new shares in the Delaware parent. After that, investors typically invest into the Delaware parent, not the old company.

In many cases, the goal is simple. You want a structure that U.S. investors understand fast, with fewer exceptions and fewer delays.

What people get wrong at the start

Many founders think a flip is only a legal formality. They treat it like changing a profile photo, not changing the engine.

But a flip touches ownership, taxes, contracts, equity plans, bank accounts, and IP chain of title. If even one of those is handled in a sloppy way, it can create friction in diligence later.

Diligence is not only about finding problems. It is also about how quickly you can answer questions. A clean structure makes answers fast. A messy flip makes every answer slow, and slow can kill a round.

Where Tran.vc fits into this decision

Tran.vc works with technical founders who want to protect what they are building before they give away leverage. A flip decision is often tied to the same question: “What do we really own, and how do we prove it?”

When you build your patent strategy early, you reduce the risk that a restructure later will weaken your IP story. You also make it easier to move assets between entities if needed, because the paper trail is already clean.

If you want to build that kind of clarity early, you can apply anytime here: https://www.tran.vc/apply-now-form/

What a Delaware Flip Actually Is

The basic structure, without the jargon

Think of your company as a box that holds your team, your code, your contracts, and your IP. A Delaware flip means you put that box inside a bigger box.

The bigger box is a Delaware corporation, usually a Delaware C-Corp. Your original company becomes owned by it. The Delaware company becomes the “top” company that shows up in investor documents.

This structure is common when the original company was formed in another country, or in a place where U.S. investors feel less comfortable. It is also common when a company started as an LLC and later wants venture-style equity rules.

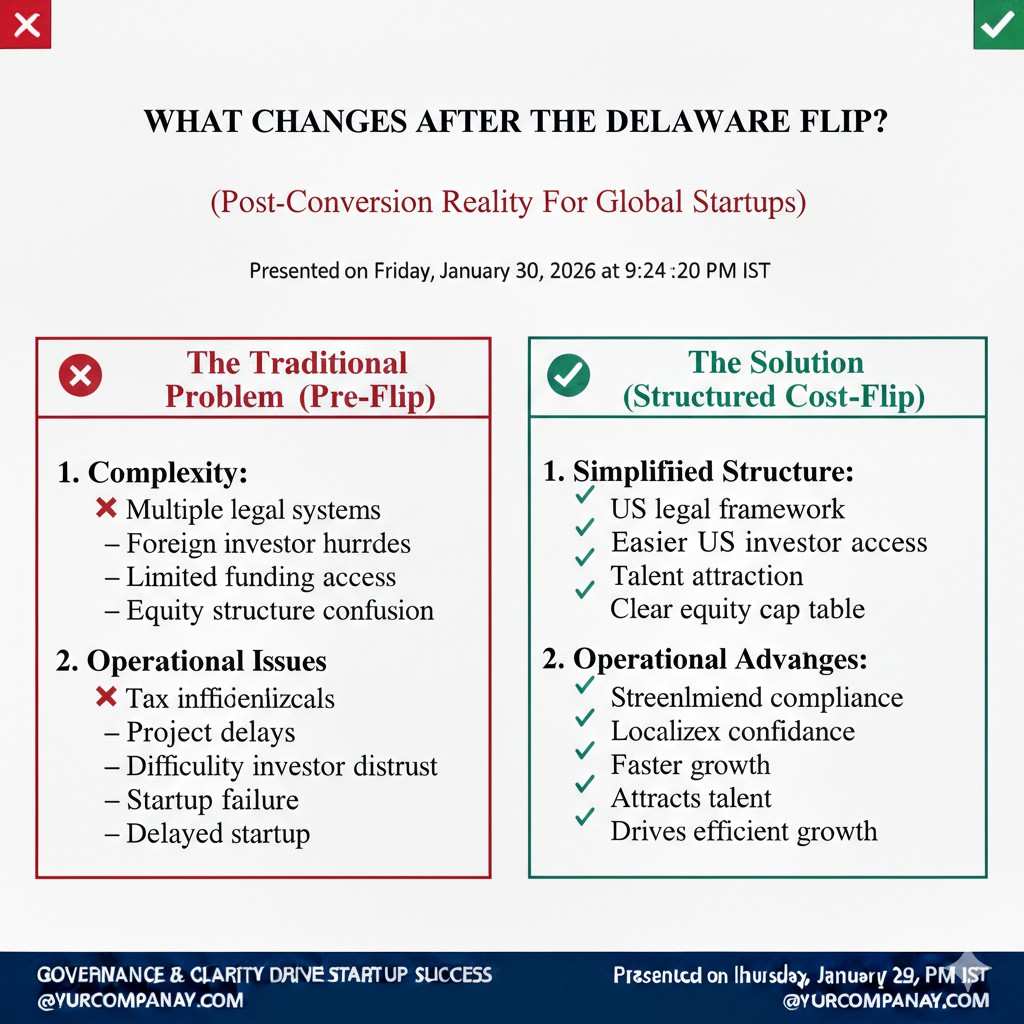

What changes after the flip

After the flip, new stock is usually issued by the Delaware parent. New option grants are usually granted from the Delaware parent. Investor money usually goes into the Delaware parent.

But the day-to-day work may still happen inside the old company, especially if your employees and operations are outside the U.S. That is normal. The parent owns the subsidiary, and the subsidiary runs much of the activity.

What matters is that ownership and governance now sit at the Delaware level. That can be helpful when you want clean investor rights and a standard cap table.

What does not magically change

A flip does not fix product risk. It does not create a moat. It does not make investors ignore weak traction.

It also does not automatically clean up messy IP. If your IP ownership is unclear before the flip, the flip can make it worse by adding one more entity to the chain.

That is why founders should treat a flip as the last step in a clean-up process, not the first step in becoming “real.”

Common ways founders flip

Some flips are done by share exchange. Some are done by forming a new parent and moving assets. Some use a merger style approach. The right method depends on your country, your current entity type, and the tax outcome.

The key point for founders is not memorizing the method. The key point is understanding the consequences. If a method creates tax for founders, breaks contracts, or creates IP confusion, it is not the right method even if it is “common.”

Why Delaware, Specifically

The boring reason investors care

Investors like patterns because patterns reduce time. Delaware corporate law is widely used for venture-backed startups, and most U.S. investors know what they are getting with it.

They know how board control works. They know how preferred stock works. They know how option plans are typically written. They know how stockholder approvals tend to be handled.

That familiarity does not guarantee you will raise. It simply removes one reason for a “pause.” And pausing is where deals often die.

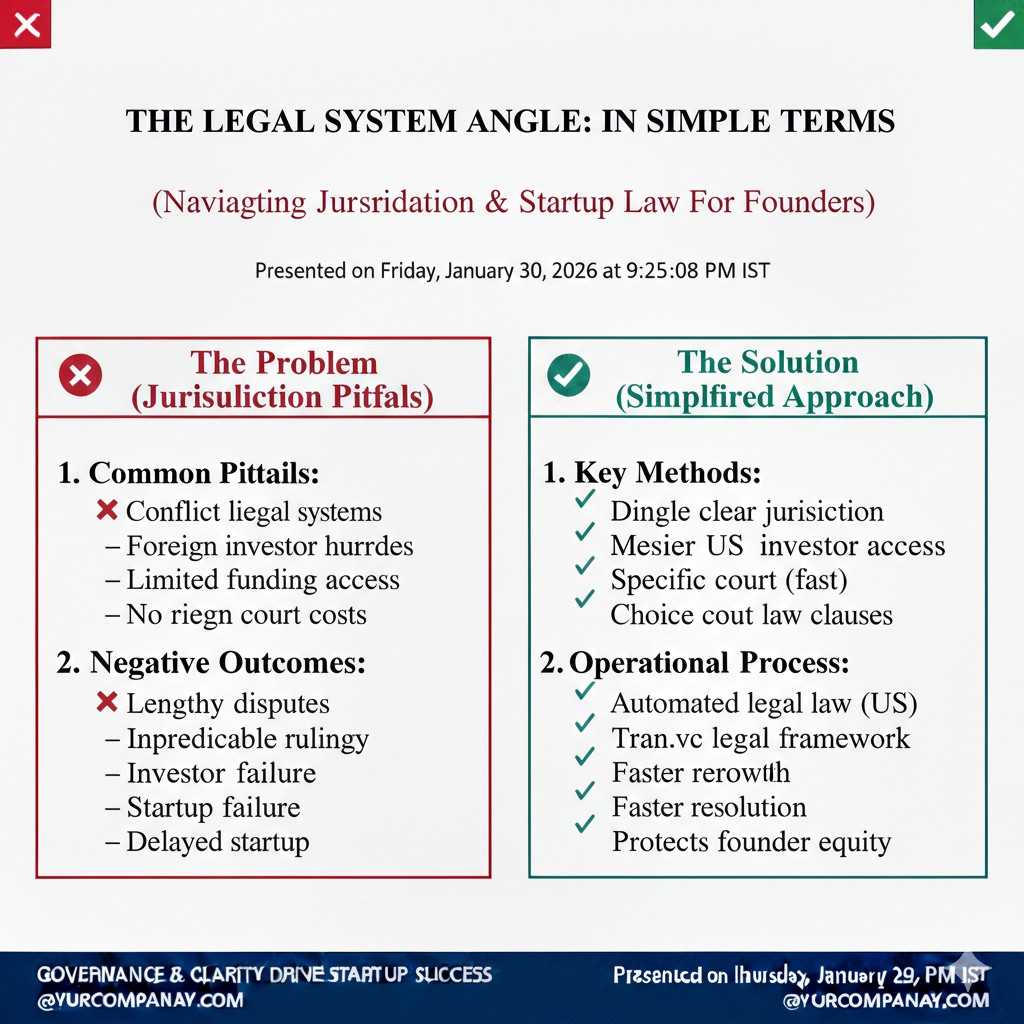

The legal system angle, in simple terms

Delaware has a well-known court system for business disputes. The outcomes are more predictable than in many other places.

Predictability is valuable when a company grows and has many owners, and when rules must be clear across years of changes. Investors are not hoping for lawsuits. They are hoping to avoid chaos if things ever get tense.

The paperwork and market practice angle

Many startup templates, financing documents, and equity tools are built around Delaware C-Corps. That lowers friction when you set up an option plan or close a priced round.

The more “standard” your setup is, the more time you can spend on product, customers, and hiring. That is the best reason to choose Delaware: fewer special cases.

When the Delaware Flip Helps

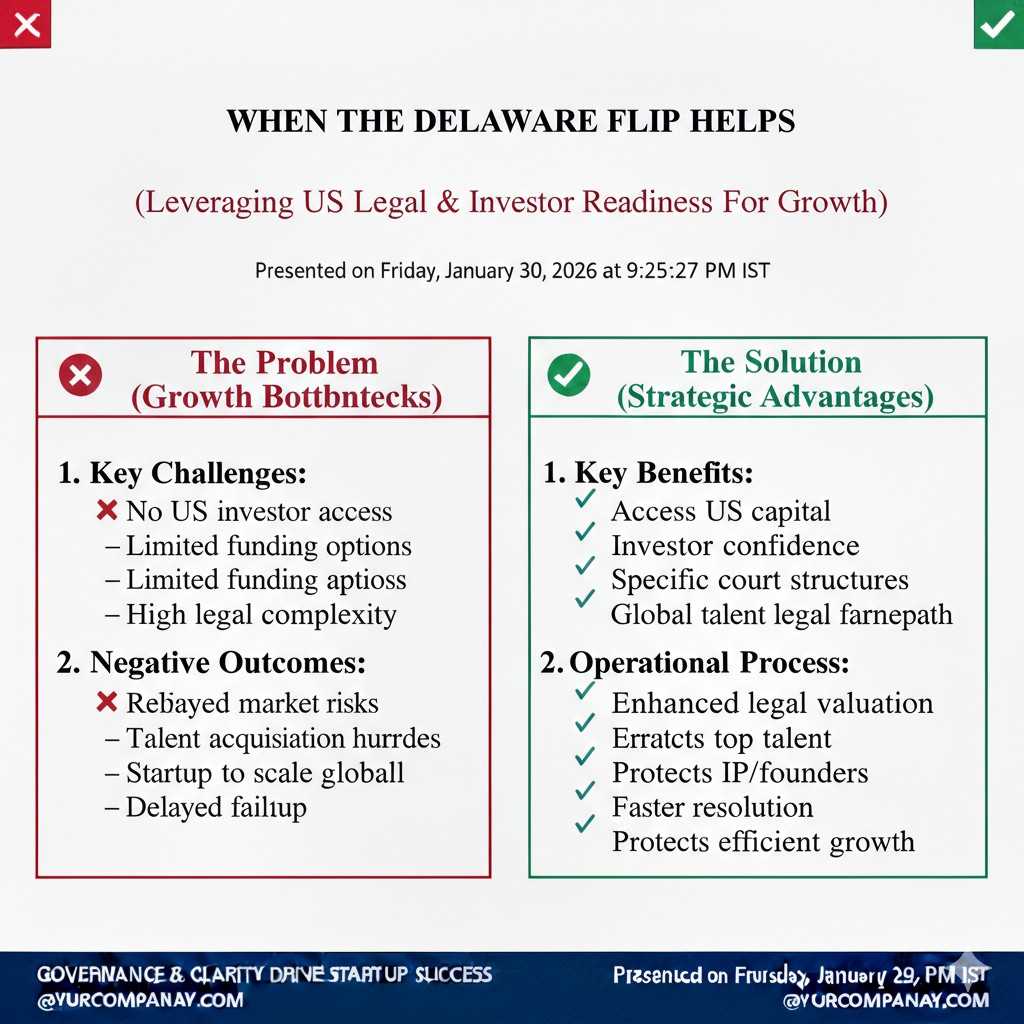

When your next round is led by U.S. investors

If a U.S. lead investor is ready to write a check but needs a Delaware C-Corp to do it, a flip can be the bridge that makes the round possible.

In that case, the flip is not theoretical. It is part of getting the funding across the line. If the lead is strong and the terms are fair, it can be worth doing the flip to remove the final structural objection.

The mistake is doing it earlier than needed. The goal is to flip when it unlocks a real outcome, not when it unlocks a feeling.

When your cap table needs venture-style clarity

Some structures are fine when it is only founders. But when you add employees, advisors, and multiple investors, the structure must support clean rules around equity, voting, and rights.

A Delaware C-Corp can make those rules simpler to manage, especially if you are planning preferred stock rounds. It can also make it easier to grant options in a way that future investors recognize.

Clarity is not about looking fancy. It is about preventing confusion that later turns into conflict.

When you are building a U.S. hiring and sales engine

If you plan to hire a U.S. team, open U.S. banking, and sell to U.S. enterprise buyers, a Delaware parent can fit that story.

Many large customers want clean vendor onboarding, clear contracting, and a stable legal home. A Delaware entity can reduce friction in procurement, insurance, and payment setup.

This is not always required, but it can help if the U.S. becomes your center of gravity.

When the Delaware Flip Hurts

When you do it too early, before value is clear

Early flips often create cost without creating leverage. You pay legal fees, tax planning fees, and time costs. Then you still have the same product risk and the same customer uncertainty.

Worse, you may lock yourself into a structure that makes later choices harder. For example, if you later realize your market is not U.S.-centered, you may carry U.S. overhead without a matching benefit.

A flip should support a strategy that is already forming. It should not be the strategy.

When the tax impact lands on founders

Some flips can trigger taxes for founders depending on where you live, where the company is formed, and how the transaction is structured.

Founders often assume “startups do this all the time, so it must be tax-free.” That is a dangerous assumption. A common path is not always a safe path in every country.

If a flip creates a personal tax bill you cannot afford, it can harm the company in a very direct way. It can also create stress that distracts you from building.

When IP ownership becomes unclear

In deep tech, the most painful flips are the ones that make IP chain of title fuzzy. If inventions were created under one entity, assigned late, or not assigned at all, a flip can add another layer of uncertainty.

Investors do not need your IP to be perfect. They need it to be clear. They want to see that the company owns what it claims to own, and that the right entity can file patents and enforce them.

This is exactly why Tran.vc focuses so much on early IP hygiene. It makes later structure changes safer because the ownership trail is already clean. If you want support here, apply anytime: https://www.tran.vc/apply-now-form/

When contracts and approvals get messy

Some customer contracts and partner deals have clauses that restrict assignment or changes in control. A flip can trigger those clauses.

This is often missed. Founders flip, then later learn they needed a customer’s consent, or they accidentally breached a clause. The risk is not always a lawsuit. The risk can be lost trust or delayed deals.

The fix is usually possible, but it is never fun, and it can show up right in the middle of a fundraise.

How to Decide Without Guessing

Start from your next concrete milestone

A flip is most justified when it unlocks something real within the next few months. That “something” is usually a funding event, a major customer contract, or a major hiring plan in the U.S.

If you cannot name the milestone, then the flip is probably a “maybe later” item. This does not mean you ignore it. It means you prepare for it without doing it yet.

Preparation can be as simple as cleaning IP assignments, tightening your cap table records, and making sure key contracts are in order.

Use the “cost of delay” test

Ask one simple question: if you do not flip now, what do you lose?

If the honest answer is “nothing, except we might look less standard,” then you are paying for a feeling, not a result. If the honest answer is “we lose a signed term sheet,” then the flip may be worth it.

This test keeps you grounded. It also helps you avoid doing things because someone on the internet said you should.

Align the flip with IP strategy

For robotics and AI startups, you should treat entity structure and IP structure as connected.

If your patent filings are planned and your assignments are clean, a flip can be done with less risk. If your IP is scattered across people, contractors, and old entities, a flip can turn that scatter into a diligence nightmare.

Tran.vc’s approach is to help you build the IP foundation early, so your company structure choices later are easier and safer. Apply anytime here: https://www.tran.vc/apply-now-form/