Protective provisions are the “rules” investors ask for when they put money into your startup.

They are not about being mean. They are about control and risk.

A VC is paid to avoid big losses. Even if they love your team, they still need guardrails. These guardrails show up in your term sheet as protective provisions. They decide what you can do without investor approval, what happens if things go sideways, and who gets a say when the stakes get high.

If you are a technical founder building AI, robotics, or deep tech, this matters even more. Your company may need longer timelines, bigger R&D bets, and more pivots. Protective provisions can either support that journey—or quietly box you in.

Tran.vc helps founders prepare for these conversations early, before you are signing papers under pressure. If you want support building leverage with a strong IP plan (and getting real patent work done, not just advice), you can apply anytime at https://www.tran.vc/apply-now-form/.

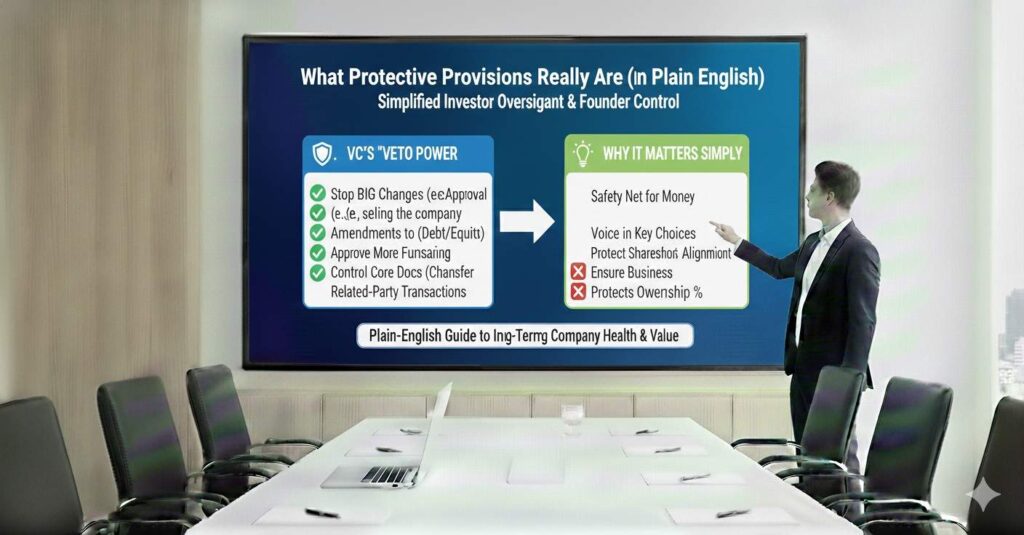

What protective provisions really are (in plain English)

A protective provision is a promise you make that says: “I won’t do certain major things unless the investors agree.”

It usually lives in the company’s charter or investor rights documents. In practice, it means some actions require a special vote. That special vote is often called a “class vote,” meaning the preferred stockholders (the investors) must approve, even if common stockholders (founders and employees) would vote yes.

Here is the key idea: protective provisions are not the same as “board control.”

Board control is about who sits at the table and votes on day-to-day company decisions. Protective provisions are about a short list of big, high-impact actions that investors want to block unless they sign off.

Think of it like this:

You are driving the car. The board is in the passenger seat and can grab the map, argue about the route, and tell you to slow down. Protective provisions are the brakes that can stop you from taking certain turns without their permission.

When founders get surprised, it is usually for two reasons.

First, they assume fundraising is only about price, like valuation. They treat the rest as “legal stuff.” That is where you get hurt. You can live with a slightly lower valuation. But a bad control term can follow you for years.

Second, they do not realize how easy it is to trigger these provisions. You might think, “We are not selling the company” or “We are not raising another round yet.” But protective provisions also cover things like changing your option pool, taking debt, licensing key IP, or even changing your business plan in a way investors consider “material.”

If you want to build with freedom, you must understand the triggers.

Why VCs ask for them

VCs ask for protective provisions because of three simple fears.

One: the company might take actions that reduce the value of their shares.

Two: the company might take actions that make it harder for them to get their money back.

Three: the founders might do something that benefits common shareholders at the expense of preferred shareholders.

That last one sounds harsh, but it is not personal. It is a structure problem.

Founders and employees hold common stock. Investors hold preferred stock. Preferred stock often has extra rights, like liquidation preference. Protective provisions exist to protect those extra rights.

Also, VCs are not investing their own money most of the time. They are investing money from limited partners, like endowments, funds, and family offices. They need to show discipline. If a portfolio company blows up because the VC “didn’t put basic protections in place,” it looks like bad judgment.

So the term sheet becomes a risk checklist.

But here is what founders should remember: VCs also use these provisions to manage behavior.

It is not only about preventing disasters. It is also about ensuring they have a seat at the table when the company makes a decision that could change the outcome of the investment.

This is why these provisions are most intense in moments like:

- when your runway is short,

- when the next round is uncertain,

- when you are exploring a sale,

- when you want to raise debt quickly,

- when your tech has become valuable and others want access.

If you know you will face those moments, you should structure the “rules” while everyone is still optimistic, not later when you are negotiating in a panic.

This is one reason Tran.vc focuses on early leverage through IP. Strong patents and a clear filing strategy make you harder to push around, because your company has assets that can’t be copied. When you have real defensibility, investors often become more flexible on control because the risk profile changes. If you want help building that leverage from day one, apply anytime at https://www.tran.vc/apply-now-form/.

The protective provisions you will see most often (and what they mean in real life)

Let’s walk through the common ones the way they actually show up in founder life, not legal theory.

1) Issuing new shares or changing the equity structure

Many term sheets say you cannot issue new shares of stock, or create a new class of stock, without investor approval.

Why they want it: if you can issue shares freely, you could dilute the preferred holders, or create a new senior class that gets paid before them.

How it plays out: this can affect more than future fundraising. It can affect option grants and refreshes, employee retention plans, and even small advisor grants.

Practical founder move: build a hiring plan that includes a realistic option pool early. If you wait and then need to increase the pool later, investors may use the approval step as leverage to renegotiate other terms. This is common. It is not always hostile. It is just negotiation.

Also, watch for language about “increase in authorized shares.” A company may need to increase the number of shares it is allowed to issue, even if no new financing is happening. That can be a trigger.

This is one place where founders get stuck unexpectedly: they think they are doing a normal option grant, but the company paperwork needs an authorized share increase, and suddenly the investor class vote is required.

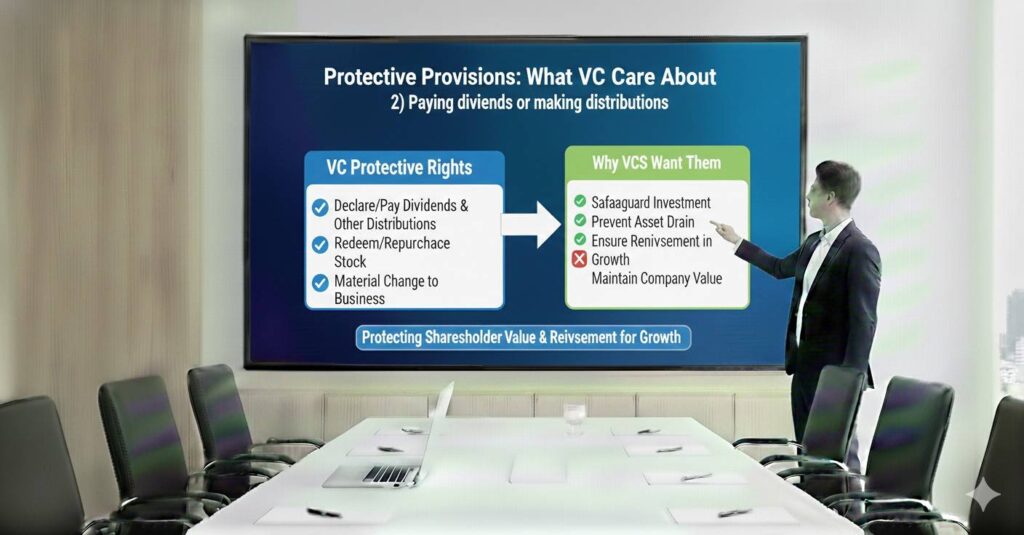

2) Paying dividends or making distributions

Early startups rarely pay dividends. Yet many protective provision sections mention dividends.

Why they want it: dividends are a way to move money out of the company. Investors do not want a founder team pulling cash out while the company is still risky and underfunded.

How it plays out: for almost every startup, it is mostly irrelevant until late-stage or profitability. But it matters in edge cases, like if you sell a product line, get a big settlement, or have a one-time cash event.

Practical founder move: do not stress about this one early, but note the broader idea: investors want to control “cash leaving the company” decisions.

3) Taking on debt above a threshold

Many term sheets say you cannot borrow money, guarantee loans, or take on debt above a certain amount without approval.

Why they want it: debt can kill a startup fast. It can also create a creditor who sits ahead of investors in a liquidation. If the company fails, debt holders often get paid first.

How it plays out: this one hits founders more now than it did years ago, because venture debt, revenue-based financing, and bank lines have become common tools to extend runway.

Practical founder move: before you sign anything, ask: what is the debt threshold, and does it cover leases, credit cards, and equipment financing? Robotics companies often need equipment. If your threshold is too low, you will need approvals for normal operational choices. That slows you down.

A good threshold is one that covers real needs without creating a free-for-all. If you are building hardware, this term deserves extra attention.

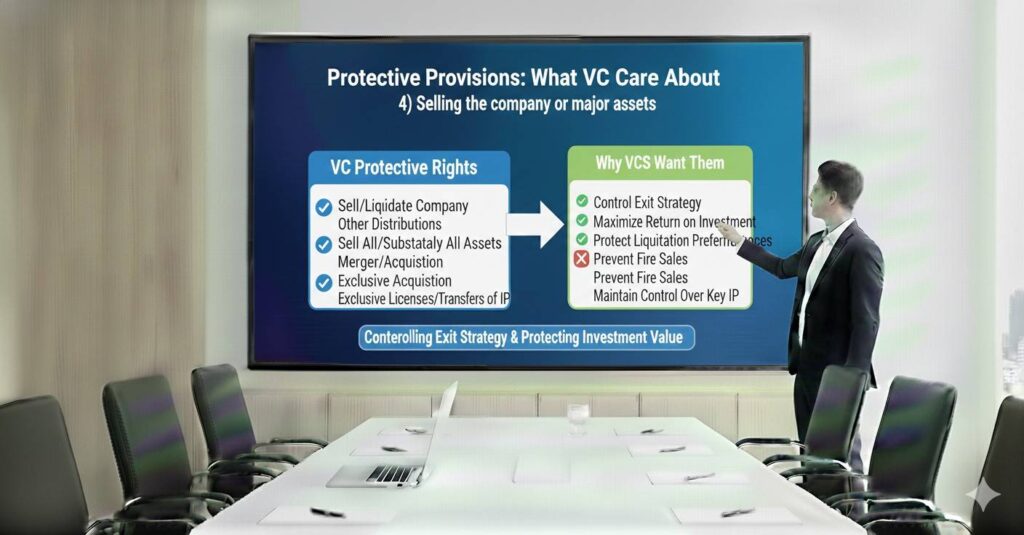

4) Selling the company or major assets

Most protective provisions require investor approval for a sale, merger, or the sale of “all or substantially all” assets.

Why they want it: this is the endgame decision. Investors want a veto if you try to sell too early or at a price that does not return enough.

How it plays out: you might want to take an early acquisition because it feels like a win, or because the market is tough. Investors may block it if they believe there is a path to a bigger outcome. Or they may push for a sale you do not want if it protects their downside.

Practical founder move: understand your investors’ fund size and incentives. A fund that needs very large outcomes may be less excited about a small exit. That is not “bad.” It is math. Align early.

Also, watch how liquidation preference interacts here. Even if the sale price is decent, the distribution might leave founders with little after preference stacks. Protective provisions can become a battle because people are fighting over who gets what.

This is where having strong IP can change the story. If you can credibly show that your patents create scarcity and increase strategic value, you can negotiate from strength. If you want Tran.vc to help you build that strength through real filings and strategy (up to $50,000 in in-kind IP services), apply anytime at https://www.tran.vc/apply-now-form/.

5) Changing the charter or bylaws

You will often see language saying you cannot amend the charter, bylaws, or any document that affects the rights of preferred stock without investor approval.

Why they want it: your charter is where their rights live. Without this, you could legally change the rules after they invest.

How it plays out: it is reasonable. But the tricky part is how broad it can be. Sometimes it is written so that almost any meaningful governance change is blocked.

Practical founder move: ask for tight language that focuses on changes that “adversely affect” the preferred shares. That phrase matters. Broad language can make routine housekeeping feel like a political process.

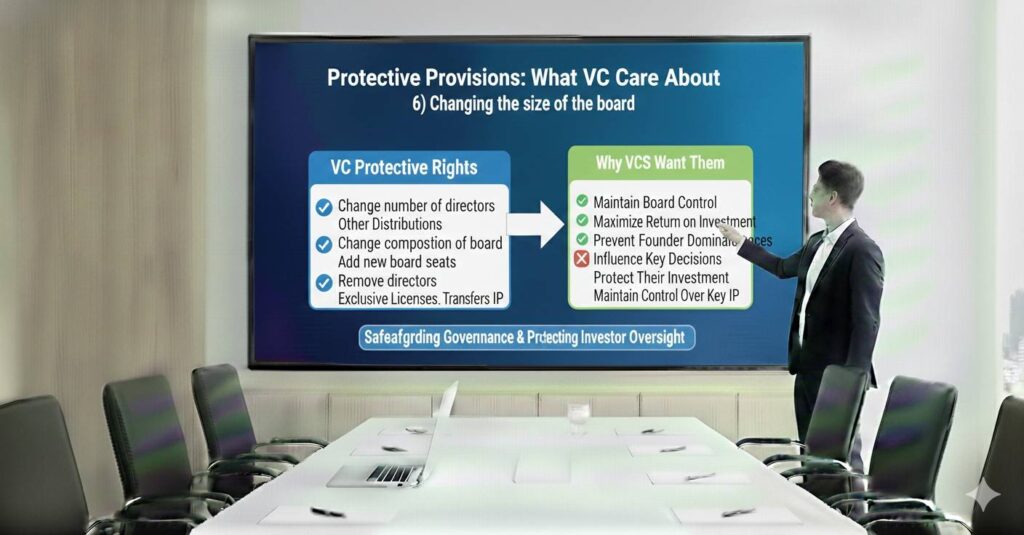

6) Changing the size of the board

Some deals require investor approval to expand or shrink the board.

Why they want it: board composition is power. If you can add seats, you could dilute investor influence. If you can remove seats, you could eliminate oversight.

How it plays out: if your board is small, one seat is a big shift. In early rounds, a single board seat can decide votes.

Practical founder move: decide what board you want at Series A before you get there. It sounds early, but it prevents you from making “temporary” choices that become hard to unwind.

If you are pre-seed or seed, a common good pattern is a three-person board where founders hold two seats early, then transition later as the company grows. But the details matter, and protective provisions can lock you into something you did not mean.

7) Liquidating or winding down the company

Investors often want a say if you decide to dissolve the company.

Why they want it: dissolution ends the story. If they think the company still has a chance, they want to block an early shutdown.

How it plays out: this can create tension if founders are burned out and investors still want you to push. It can also matter if the company is exploring an asset sale or IP sale as part of winding down.

Practical founder move: document your decision-making and make sure you have clean IP ownership and assignment from day one. If things ever go poorly, messy IP turns a hard situation into a disaster. Tran.vc’s model is built around making the IP foundation clean early, before stress hits. Apply anytime at https://www.tran.vc/apply-now-form/.

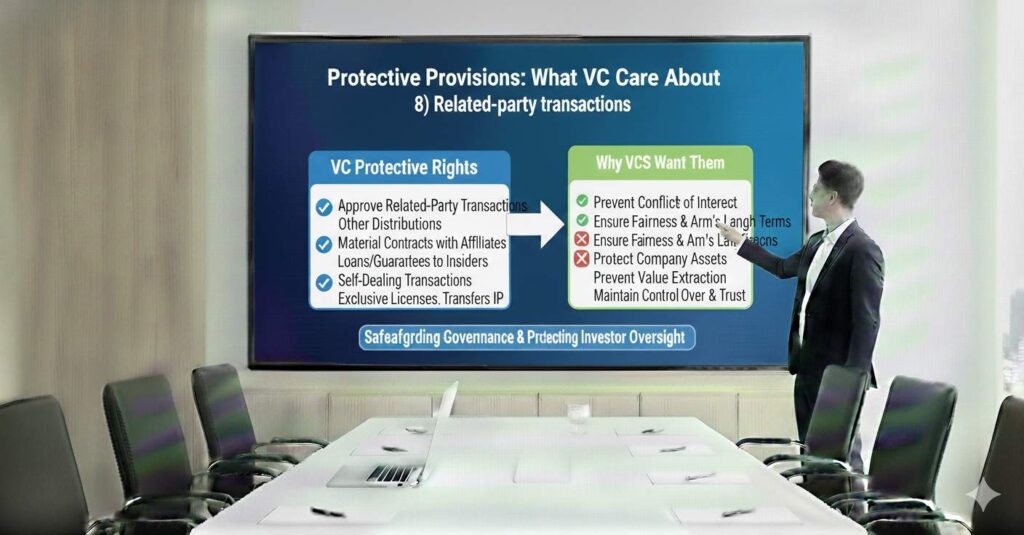

8) Related-party transactions

Many protective provisions require approval for transactions between the company and founders, or between the company and an entity a founder controls.

Why they want it: because self-dealing is real. It can be intentional, or accidental. Investors want a check.

How it plays out: it can cover things like a founder-owned consulting entity doing work for the company, or renting space from a founder, or paying a founder for IP.

Practical founder move: keep it simple. Avoid these deals unless truly needed. If needed, disclose early and get formal approval. It is not only about fairness. It is about clean due diligence for the next round.

The part founders miss: protective provisions can shape your roadmap

Founders often read these provisions like they are rare events. But they can shape your day-to-day strategy because they change what you can do quickly.

If you need investor approval to take debt, you might avoid debt even when it is smart.

If you need investor approval to license IP, you might hesitate to do partnerships.

If you need investor approval to adjust the option pool, you might delay hires.

This is why you should treat protective provisions as operating constraints, not legal trivia.

The goal is not to “win” by stripping all protections. You will not. VCs will not invest without basic rights.

The goal is to avoid terms that turn normal founder actions into permission requests.

This is also why it helps to build leverage before you raise. Leverage can be traction, revenue, demand, or a strong technical moat that investors respect. In deep tech, that moat is often patents and clear IP positioning. When your IP story is sharp, it is easier to push back on heavy control because you are less replaceable.

Tran.vc exists for exactly that stage: helping technical founders build an IP-backed foundation while you still have negotiating power. If you want to explore that path, apply anytime at https://www.tran.vc/apply-now-form/.

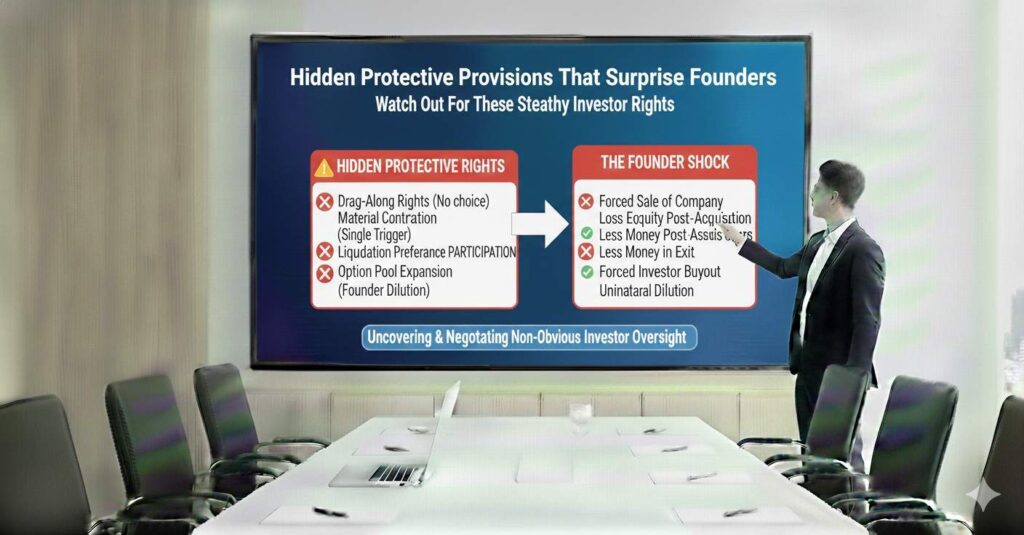

Hidden protective provisions that surprise founders

“Material adverse” and other vague words

Some protective provisions look normal until you read one key phrase. Words like “material,” “substantially,” or “adverse” can quietly widen the investor veto.

In real life, this means a founder may think, “This is a small change,” while an investor thinks, “This changes the risk.” When the document is vague, the person with more power in the moment often decides what the word means. That is why you want tighter language.

A practical way to handle this is to push for wording that ties approval to clear outcomes, like changes that “adversely affect the rights of the preferred stock.” That phrase narrows the scope. It still protects investors, but it avoids turning every meaningful decision into a debate.

If you are early and you do not have strong leverage, you may not be able to rewrite everything. But you can often narrow the most dangerous vague lines, especially when you explain you need speed to execute.

Approval rights that hide inside “consent” clauses

Sometimes the protective provisions section looks short, but the approval rights pop up elsewhere. You might see “consent required” in investor rights, voting agreements, side letters, or even board consents.

This is where founders get hit later. You think you agreed to ten approval items, but you actually agreed to twenty-five, spread across documents. The term sheet summary may not list them all, but the final papers will.

A tactical habit is to ask your lawyer for a single combined list of all actions requiring preferred approval. Not a vague summary. A real checklist pulled from every document. If your counsel cannot give you that in writing, push harder.

Protective provisions that become weapons in hard times

Most investors do not use these rights day to day. The trouble starts when the company is low on cash, the round is delayed, or the product needs a pivot.

At that point, investor approval rights can turn into bargaining chips. A founder asks for consent to do something urgent, like taking a bridge note or expanding the option pool. An investor might say yes, but only if other terms change too.

This is not always evil. It is often how investors manage their own risk when things get uncertain. But it can feel like pressure if you are negotiating with a short runway. The best defense is planning early, before you are cornered.

This is also why an IP moat matters. If your company owns defensible patents and has a clear story about why competitors cannot copy you, investors see more upside and less downside. That often makes them less likely to tighten the screws when times get tough. If you want support building that leverage, you can apply anytime at https://www.tran.vc/apply-now-form/.

How protective provisions change by funding stage

Pre-seed: simple terms, but the tone gets set

At pre-seed, the documents may be lighter, especially if you raise on SAFEs or simple notes. Many founders assume this means there are no control terms. But control can still show up through side letters, pro rata arrangements, and governance promises tied to the priced round.

Even when the paperwork is light, the tone you set with early backers matters. If your earliest investors expect veto power over many choices, that expectation can carry into the seed and Series A.

If you are raising a pre-seed priced round, you may see a standard set of protective provisions even this early. The risk is not that the provisions exist. The risk is that they are written too broadly because nobody expects conflict yet.

The tactical move in pre-seed is to keep the list focused on true “company life and death” actions. You want flexibility to hire, adjust your plan, and build. You also want to avoid any clause that blocks normal IP and product decisions.

Seed: protective provisions become more detailed

Seed investors often ask for a fuller set of veto rights because the check is bigger and the company is still fragile. This is where you will see more explicit debt limits, option pool controls, and restrictions around selling assets.

Seed is also where founder mistakes are common because the term sheet feels “standard.” It is standard in the sense that many deals use similar categories. It is not standard in how broad each category is.

A seed protective provision can be written in a founder-friendly way, or in a way that makes the company slow. The difference is usually a few lines of text. That is why reading closely matters.

If you are a deep tech founder, seed is also when IP becomes a negotiation lever. When you can point to filed patents, clear ownership, and a forward plan, you change the investor’s view of risk. That can help you keep decision speed. If you want Tran.vc’s help building that IP foundation, apply anytime at https://www.tran.vc/apply-now-form/.