Most founders think revenue is simple: you ship, you invoice, you get paid, you call it “revenue.”

Then one day, a buyer’s finance team asks for your revenue policy. Or an investor asks why your “revenue” is up but your cash is flat. Or your auditor says you cannot count half of what you booked. And suddenly, the story you tell about your business does not match what your numbers say.

This is why revenue recognition matters early. Not because you love accounting. Because it shapes how buyers trust you, how investors price you, how your team plans, and how clean your next round feels.

At Tran.vc, we spend a lot of time with technical founders building strong foundations. Patents and IP are one part of it. Clean revenue is another. Both make you harder to copy and easier to fund. If you want help building the kind of company that raises on better terms, you can apply anytime at https://www.tran.vc/apply-now-form/.

Now let’s get into the basics most founders miss—starting with the core idea that changes everything.

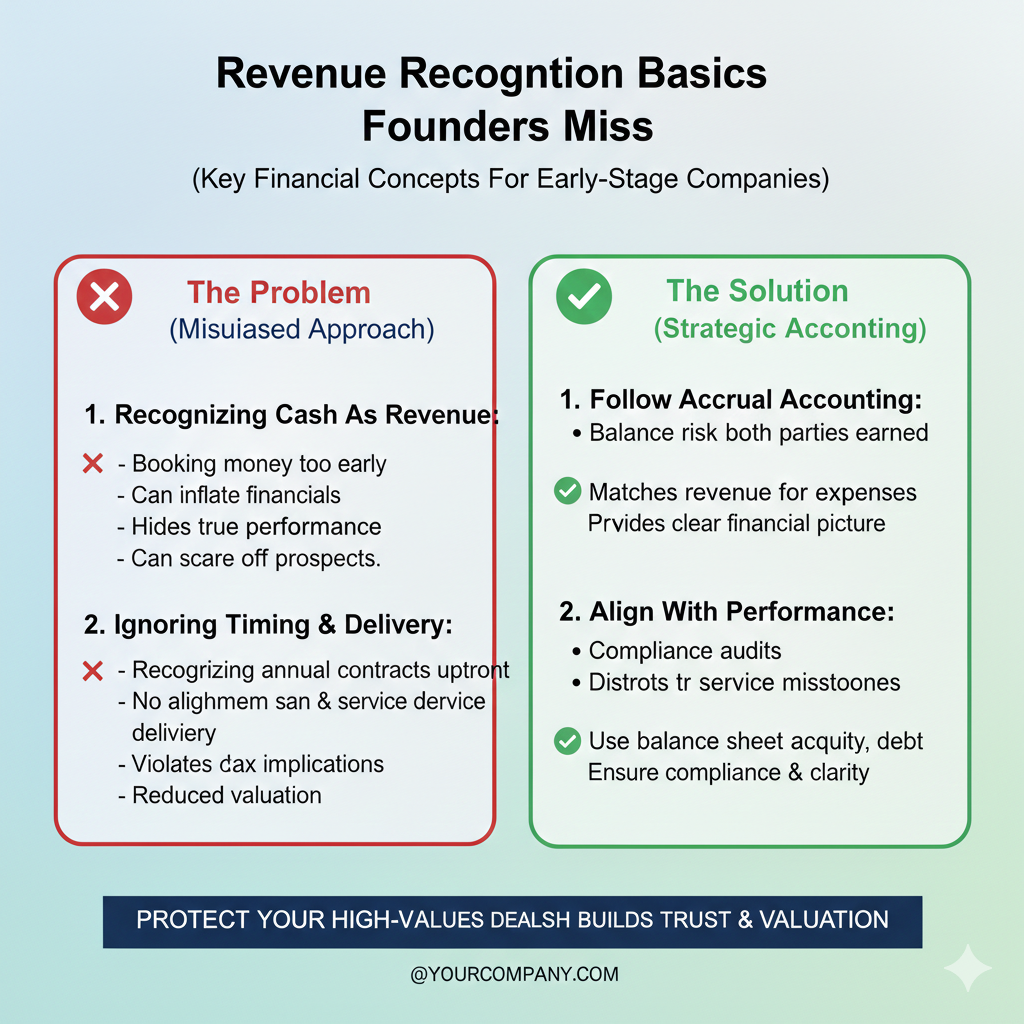

Revenue is not the invoice. It is the work.

An invoice is a request for payment. Revenue is what you earned by delivering what you promised.

That gap is where most early mistakes happen. A founder sees an invoice go out for $120,000 and thinks, “We made $120,000 this month.” But if that invoice covers a year of service, you did not “earn” a year of service in one month. You earned one month.

So what happens to the other eleven months? It sits in a bucket called deferred revenue. That bucket is not bad. In many cases, it is a sign you are selling well. But it is also a promise: you owe the customer future delivery.

If you ignore that promise and book everything as revenue now, your numbers look bigger today and weaker later. It also makes churn and refunds hit you harder, because you already claimed the revenue.

This is the first mindset shift: revenue follows delivery, not billing.

The second shift: “delivery” is not always obvious.

For software, delivery is not “we gave them a login.” Buyers pay for outcomes over time: access, uptime, support, updates, security, and sometimes success help. That is why most software revenue is recognized over time, not all at once.

But many founders mix things in one deal: setup, data work, custom changes, training, seats, usage, and a support plan. Some of that is “over time.” Some of that could be “at a point in time.” If you treat it all the same, you may be wrong in both directions. You might understate revenue and look smaller than you are. Or you might overstate revenue and create risk.

Your goal is not to game the system. Your goal is to match the story of value with the timing of value.

That is what revenue recognition tries to do.

Why this becomes a problem at the worst possible moment

Founders often delay this until they “have to.” The trouble is: the moment you “have to” is usually when you are in motion.

You are closing larger deals. You are signing your first big enterprise customer. You are negotiating with a strategic partner. You are raising. These are not calm moments.

And this is when someone asks questions like:

- Why is your gross margin so high this quarter?

- Why does your revenue jump when you sell multi-year contracts?

- Why do you call this “recurring” if you recognize it up front?

- If the customer can cancel, why do you count the whole thing now?

- Why is your cash balance strong but your P&L looks weak?

If you do not have clean answers, it makes you look less mature than you are. It can also slow deals because procurement and finance teams do not like surprises.

Clean revenue is a trust tool.

The simple framework behind most revenue rules

You do not need to memorize accounting text. You need a simple way to think.

When you sell anything, ask four plain questions:

- What did you promise?

- When does the customer get that value?

- How sure are you that you will get paid?

- Can the customer return, cancel, or demand a refund?

These questions map to the common “rules” buyers and investors expect you to follow.

In practice, this usually turns into a few core patterns founders should understand.

Pattern one: subscription access over time

If a customer pays $12,000 for 12 months of access, the clean approach is often to recognize $1,000 per month.

Even if they paid the full $12,000 on day one.

Even if you “delivered” the product by turning on the account.

Why? Because the value is the ongoing access. If you stop providing access in month 4, the customer has not gotten month 5–12.

What founders miss here is not the idea. It is the discipline.

They forget to set up their books so revenue is spread monthly. They also forget the second-order effect: if you pay a sales commission up front, you may want to spread that cost too, so your margins do not look weird. This is one reason mature companies track “contract assets” and “commission amortization.” You do not need to be fancy early, but you do need to know why your P&L can look distorted.

Pattern two: setup fees and onboarding

Many startups charge an onboarding fee. Sometimes it is real work. Sometimes it is a pricing trick to get more cash up front.

Revenue treatment depends on what it truly is.

If onboarding is required to get the customer live and it is a real service you deliver, you may recognize it as you perform that work. If you finish onboarding in two weeks, that portion might be recognized quickly.

But here is the trap: if onboarding is not separate in the customer’s mind—if it is just part of “getting the subscription working”—then finance teams often treat it as part of the overall subscription value. That can force you to spread the onboarding fee over the whole term.

Founders miss this because they think the line item name decides it. It does not. The substance decides it.

A clean way to handle this is to write clear statements of work, define what onboarding includes, define when it is “done,” and avoid promising ongoing services inside “onboarding” that really last all year.

You also want to be careful with language like “implementation includes ongoing optimization.” That sentence can quietly turn your “setup fee” into a year-long obligation.

Pattern three: usage-based charges

Usage-based revenue feels simple because it follows the meter. Customer uses more, customer pays more.

But founders still get tripped up.

The main risk is estimating usage before it happens. If you bill in advance for a usage bundle, you may not be able to count it as revenue until the usage occurs or the time period passes.

Also, if your contract has price breaks, credits, or true-ups, you need to ensure your billing system and your revenue logic match. Investors do not mind complexity. They mind confusion.

A tactical habit: every quarter, take five customer invoices and trace them back to the contract terms. Ask, “If I only read the contract, would the invoice make sense?” Then ask, “If I only read the invoice, would the revenue entry make sense?” If either answer is no, fix the system before it scales.

Pattern four: milestones and deliverables

Robotics, AI, and deep tech startups often sell projects: proof of concept, pilot, model tuning, integration, factory line tests, field trials, acceptance tests.

These deals are where revenue gets messy fast.

If the customer is paying for a result that happens at a point in time—like “acceptance of the prototype” or “system passes the test”—then revenue may be tied to that point. Until acceptance, you may not be able to count it, even if you worked for months.

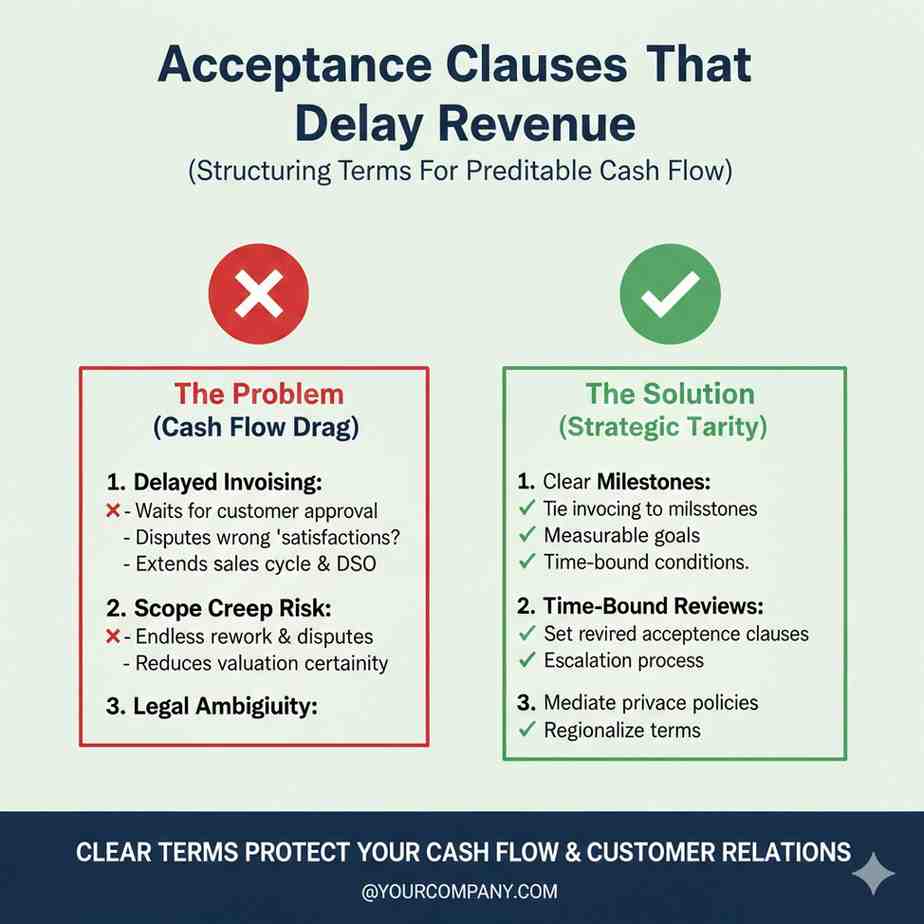

Founders miss the “acceptance clause” more than anything.

A buyer might say, “Payment due upon acceptance.” The founder hears, “We will get paid when it works.” But accounting hears, “You have not earned it until the customer accepts.”

If acceptance is subjective or open-ended, you can end up with revenue delays that make your company look lumpy, even when you are executing well.

This is not just accounting. It is contract strategy.

You can often improve this by defining acceptance clearly: objective tests, clear timelines, and what happens if the customer does not respond. You can also break large deliverables into smaller ones with their own acceptance.

This makes revenue smoother and reduces disputes. It also reduces “free work creep,” where the customer keeps asking for “just one more change” before acceptance.

How refund rights and cancellation terms quietly break your numbers

Many founders add a generous cancellation clause to close the deal. “Cancel anytime.” “30-day out.” “Refund if you’re not happy.”

That may be a good sales move. But it changes your revenue story.

If the customer can cancel and get money back, you may need to wait to recognize revenue, or you may need to set aside a reserve for expected refunds.

Even when you believe cancellations will be rare, a buyer’s finance team might push back if your policy does not reflect the contract.

This is one reason enterprise deals have tight language around termination. Buyers want flexibility. Sellers want certainty. The contract becomes the source of truth for how stable your revenue really is.

A simple founder habit: before you sign any new “special terms,” ask one question: “If I had to explain this term to an investor using my financial statements, would it make my revenue look stronger or weaker?”

If the answer is weaker, either raise the price to match the risk or narrow the term.

The hidden founder mistake: mixing product revenue with services revenue

Technical founders often say, “We’re not a services company.” But early on, you might deliver a lot of service to make the product work.

That is normal. The mistake is hiding it.

When you bundle heavy services into a product contract, you may think you have high-margin software revenue. But if the effort is large, your true margin is lower. And if you price it wrong, you train the market that your product includes custom work for free.

From a revenue recognition view, services can also change timing. If part of the contract is service work that lasts months, you may need to recognize that portion over the service period.

This is why separating product and services in your quote can help even if the customer pays one total. It forces you to see what is really happening.

It also helps you protect your IP.

If you are doing custom model work, custom robotics integration, custom data pipelines, you are creating know-how. That know-how can become defensible assets if you treat it with care. Tran.vc helps founders turn technical work into IP assets that investors respect. If you are building in AI or robotics and want to lock in that advantage early, you can apply anytime at https://www.tran.vc/apply-now-form/.

A realistic “founder-grade” revenue system you can set up early

You do not need a big finance team to be clean. You need a few habits and a simple setup.

Start with your contract folder. Make sure every customer has one place where these items live:

- the signed agreement

- the order form or pricing page terms

- any statement of work

- any email that changes terms

- the invoice schedule

Then, for each contract, write a short note that answers:

What are we delivering, and over what time period?

That note becomes your revenue guide. It is also what you can hand to a bookkeeper or a fractional controller without long meetings.

Next, make your billing match your delivery as much as possible.

If you deliver monthly, bill monthly where you can. Annual prepay is great for cash, but it creates deferred revenue complexity. If you take annual prepay, be ready to track it properly. The solution is not to avoid annual deals. The solution is to design a clean workflow for them.

Finally, be consistent.

Most investors do not punish early-stage companies for being imperfect. They punish them for being sloppy or changing stories each quarter.

Consistency builds trust. Trust lowers perceived risk. Lower risk improves your terms.

This is the quiet advantage founders miss.

Revenue Recognition Basics Founders Miss

The gotcha scenarios that quietly break clean revenue

Founders usually run into trouble in the “in-between” deals. These are not pure subscriptions and not clean one-time projects. They are the deals you sign to win early logos, learn fast, and move upmarket.

The issue is not that these deals exist. The issue is that the contract terms often do not match how you talk about revenue in decks and updates. When those two stories drift apart, finance people notice fast.

In this section, we will walk through the situations that cause the most pain. You will see what typically goes wrong, why it matters, and what to change in your contracts and billing so your numbers stay honest and stable.

Free trials that turn into paid plans

Free trials feel harmless. You give access, they test, then they convert. But many founders build trials in a way that creates unclear start dates and unclear obligations.

If the trial includes “hands-on” help, data work, or custom setup, you are delivering real value before money starts. Then, when the customer pays later, it is tempting to treat the first paid invoice as clean revenue from day one.

A safer approach is to define the trial as a clear, limited period with clear limits. Make it obvious when the paid term begins, what is included in the paid term, and what was truly free. If you did real work during the trial, track it internally, because it affects how you price the paid plan.

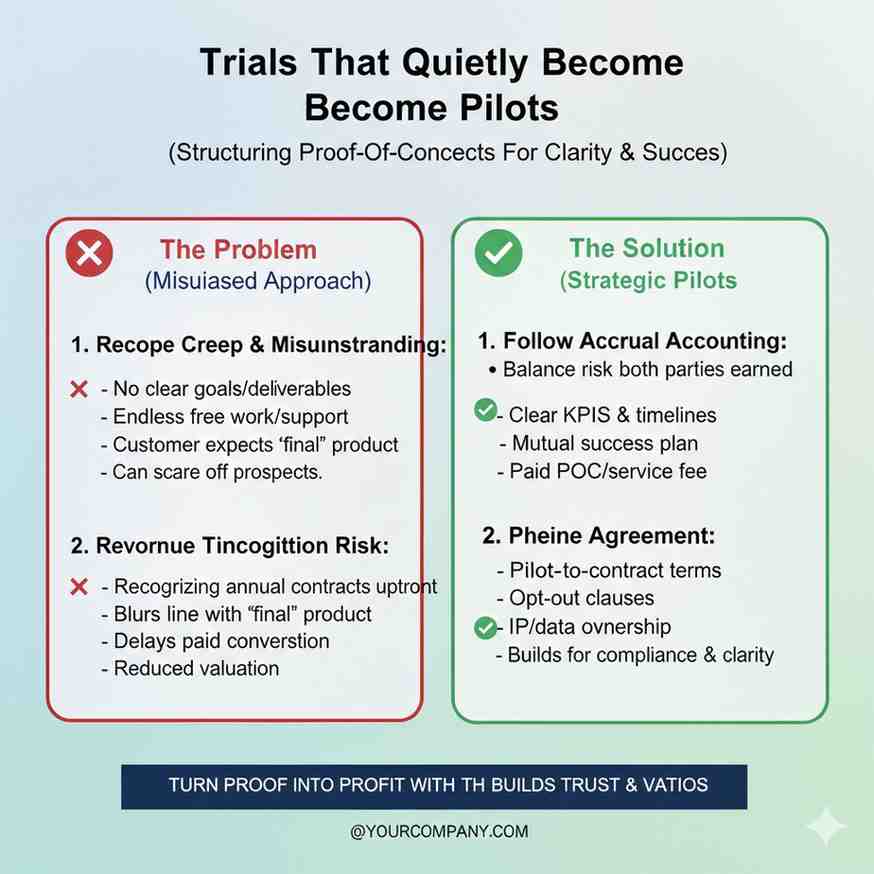

Trials that quietly become pilots

A trial is usually product access with light help. A pilot is usually a project with real effort and defined success goals. Many startups use the word “trial” while behaving like a “pilot,” and that is where revenue stories get messy.

If you promise outcomes like “we will hit this accuracy” or “we will deploy to this site,” you are no longer offering a casual test. You are committing to deliverables that may need acceptance or sign-off.

When you treat a pilot like a simple subscription, you risk booking revenue too early. You also risk training your team to do deep custom work without pricing it as such. The clean fix is simple: call it what it is, define what “done” means, and price it like a real engagement.

The “pilot fee” that is really a discount coupon

Some founders charge a pilot fee and promise it will “credit toward production.” That sounds friendly to the buyer, but it can complicate revenue timing and create confusion.

From the buyer’s view, they paid money now and expect a benefit later. From your view, you may have delivered pilot work now but also owe them future discounts. That future discount is an obligation.

If you want to do this, keep the language precise. Make the credit terms clear, time-bound, and tied to specific future purchases. Internally, track it as a real commitment, because it can affect how revenue and pricing are understood later.

Start dates that do not match invoice dates

A very common early-stage pattern is “invoice now, start later.” You might do this because procurement takes time, or because the buyer wants to spend budget before the quarter ends.

Cash comes in early, which feels great. But you did not start delivering yet. That means the invoice is not revenue yet, even if your bank account is smiling.

This is one of the easiest places for founders to misstate revenue. The practical fix is to record it as deferred revenue and then recognize it as the service period actually runs. It also helps to write contracts with clear start dates and clear service periods, so no one has to guess later.

Mid-term upgrades that make revenue look like a spike

Customers upgrade. They add seats. They move from a pilot to production. They buy extra modules. These are good problems, but the accounting can look strange if you do not structure the change well.

If a customer pays a large upgrade fee mid-year, it is tempting to count that whole upgrade immediately. But if the upgrade provides value over the remaining term, recognition often follows time, not the moment of payment.

A strong habit is to document every upgrade with a short order form that states what changes, when it starts, and how long it lasts. This prevents messy back-and-forth and makes revenue entries match the commercial reality.

Downgrades and pauses that you treat like churn

Some customers do not churn. They pause. They reduce usage. They shift scope. If your contract allows these moves, revenue stability becomes more sensitive to customer behavior.

Founders sometimes call a pause “temporary churn” and keep the revenue story as if the customer is still fully active. That can create a mismatch between product use, invoices, and recognized revenue.

The clean approach is to design pause terms deliberately. If you allow pauses, decide what happens to the contract term, what happens to fees, and what happens to support. When the contract logic is clear, your revenue logic stays clean.

“Cancel anytime” that creates refund risk

Founders often offer flexible cancellation to close a deal fast. The buyer likes it. The founder hopes it will not be used. But accounting treats cancel rights as real, not hopeful.

If the customer can cancel and get money back, you may need to recognize revenue more cautiously. In some cases, you may need to record expected refunds as a reserve, even if you believe the risk is low.

The practical takeaway is not “never offer flexibility.” The takeaway is to price for flexibility and define the rules tightly. Short notice periods, clear termination clauses, and limited refund windows make revenue more reliable and easier to defend.

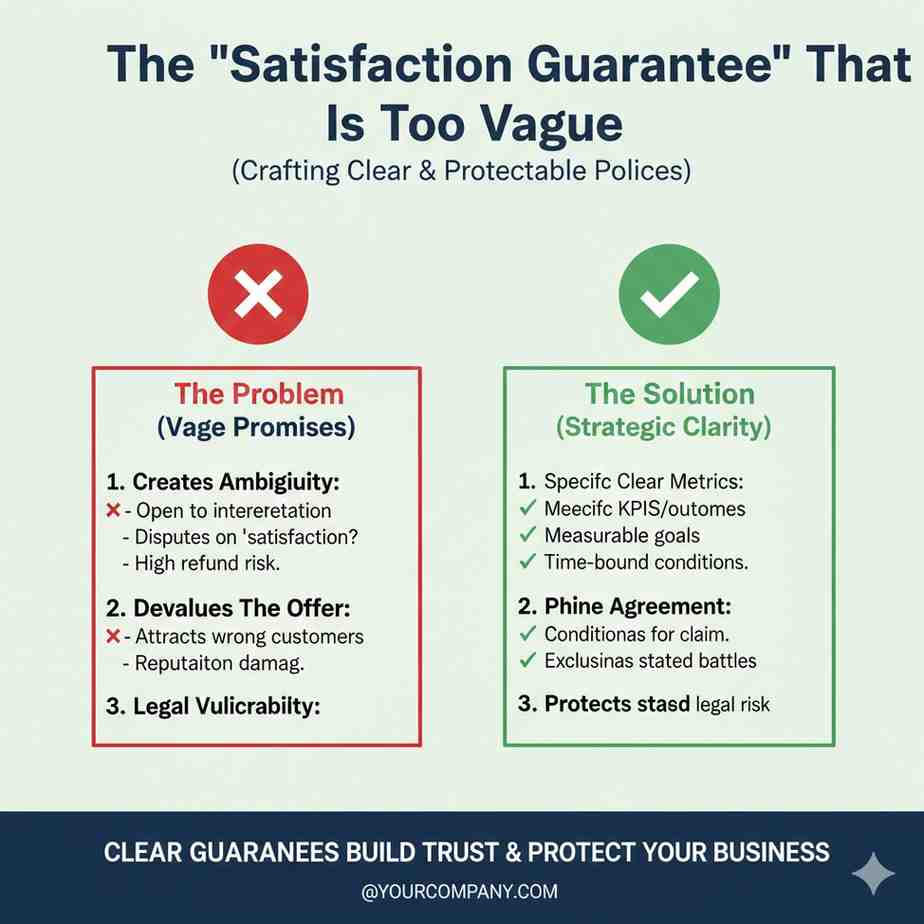

The “satisfaction guarantee” that is too vague

A satisfaction guarantee can be a strong sales tool. It can also be a revenue landmine if it is subjective.

If the contract says “refund if not satisfied,” you may have created an open door that a buyer can use for reasons unrelated to performance. When terms are subjective, revenue confidence drops.

If you want to offer guarantees, make them objective. Tie them to measurable service levels or specific deliverables. Define what the customer must do to qualify. This keeps your promise fair and keeps your revenue story clean.

Contract terms that control your revenue story

Why the contract is the real source of truth

Your revenue recognition is not based on what you meant. It is based on what the contract says. Even if you are early, buyers and investors will treat the signed terms as the reality.

This is why revenue recognition is not only an accounting topic. It is a product, sales, and legal topic. One vague clause can change the timing of revenue for an entire deal.

A founder who understands this can negotiate smarter. You do not need to “fight” buyers. You need to write terms that protect both sides and reduce confusion.

Acceptance clauses that delay revenue

Acceptance is one of the biggest traps in robotics and deep tech deals. Buyers like acceptance because it reduces their risk. Founders accept it because they want the deal.

The problem starts when acceptance is not defined. If acceptance depends on “customer approval,” and approval can be delayed for internal reasons, your revenue may be delayed even if you did great work.

A cleaner pattern is to define acceptance tests, timelines, and what happens if the customer does not respond. Many agreements can include “deemed acceptance” after a set number of days. That small clause can prevent months of stuck revenue.

Change requests that expand obligations

Early customers often ask for changes. Some of those changes are fair. Some are scope creep. If your contract does not separate the core deliverable from optional changes, it becomes hard to know what you truly owe.

This matters for revenue because unclear scope means unclear delivery. Unclear delivery means you cannot confidently say you “earned” the fee.

The best fix is to treat changes as changes. Document them. Price them when needed. Tie them to a new timeline. This is not about being rigid. It is about preventing your revenue from becoming a fog.

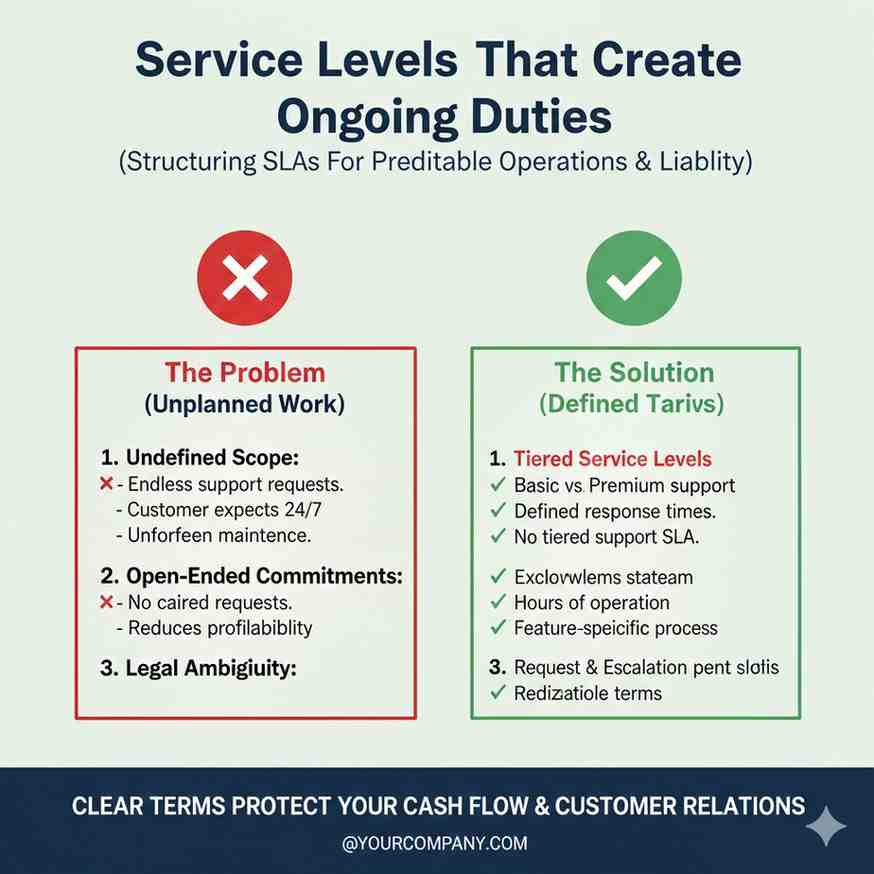

Service levels that create ongoing duties

Many founders copy service level language without thinking. They promise response times, uptime, and support coverage that their team cannot consistently deliver.

If you promise a service level, you have a duty to provide it. That duty often means the revenue should be recognized over time, because the value is provided over time.

If you are early, keep service levels realistic. Offer what you can deliver with confidence. This also reduces refund risk and keeps customers happier.

Payment terms that do not mean revenue terms

Payment terms tell you when cash arrives. They do not tell you when revenue is earned.

A customer might pay upfront for a year. That is still a year of delivery. The cash is yours, but the obligation remains.

This is important because founders often treat upfront payment as proof of product-market fit. It can be. But you still need to track the promise you owe. Investors look at deferred revenue because it shows future commitments and future confidence.

The role of renewals in clean revenue

Renewals are not only a sales event. They are also a test of whether your revenue is truly recurring.

If you book a large upfront amount and call it recurring, but renewals are weak, you are not building a stable base. You are building spikes. Spikes make planning hard and make fundraising riskier.

Clean revenue recognition forces you to see the business as it is. That truth can feel uncomfortable. It can also guide better decisions sooner.

Bundles that confuse founders the most

Hardware plus software in one deal

Robotics startups often sell hardware and software together. Sometimes the hardware is a one-time sale and the software is ongoing. Sometimes the hardware includes future service obligations. Sometimes the buyer expects replacement parts and field support.

If you treat the entire deal as “product revenue,” you lose the real picture. The hardware may be delivered at once, but the software and support are delivered over time.

The clean approach is to separate the pieces in your mind and often in your quote. Even if you present one total price, you should internally allocate value across hardware, software, and services so your revenue timing matches what you actually deliver.

Professional services inside a “software” package

Many AI companies do data labeling, data cleaning, model tuning, and integration work to get to value. This work is often essential, but it is still work.

If you hide it inside subscription pricing, you can end up with margins that look great on paper and terrible in real life. You also risk creating a model where every new customer requires heavy manual effort.

From a revenue recognition view, heavy services may need to be recognized as performed, not as a pure subscription. From a business view, separating it helps you see what must be automated and what can be standardized.

Training and enablement that looks small but adds up

Training often feels like a tiny add-on. In enterprise settings, training can be repeated, customized, and demanded by many teams.

If training is promised as “included,” and it happens across months, it becomes a real obligation. If you do not plan for it, you get surprise work that hurts delivery and customer happiness.

A cleaner pattern is to define training clearly. Specify how many sessions, the format, and the time window. This protects your team and keeps the delivery period easier to define.

Multi-year deals with front-loaded discounts

Many startups offer a discount for multi-year commitments. That can be smart. But it can also create confusion about what you earned in each year.

If you bill all upfront, you will likely recognize over time. But founders also need to watch how they talk about “ARR” and “run rate.” A discounted multi-year deal may not reflect future pricing power.

A strong habit is to track the full list price value and the discounted value separately. This helps you see whether you are truly increasing value or simply pulling cash forward with discounts.

Resellers and channel partners

Selling through a reseller can speed up distribution. It can also complicate revenue because you are no longer selling directly to the end user.

The key questions become: who is your customer, who has the right to return, and who controls the end user relationship? If the reseller can return product or cancel easily, your revenue may be less certain.

Even if you are early, treat reseller deals with care. Get clear on refund rights and end user terms. These deals are often where founders overstate certainty.

The founder-grade operating system for clean revenue

A simple way to document each deal

You do not need a huge finance stack. You need a repeatable method. For every signed deal, write a short internal note that answers: what are we delivering, and when is it delivered?

If the delivery is over time, note the period. If there are milestones, note what triggers each milestone. If there is acceptance, note what acceptance means.

This note becomes your map. It helps your bookkeeper. It helps your future auditor. It helps you explain your numbers with calm confidence.

How to align sales, legal, and finance

Early teams often let sales “do what it takes.” That is normal at the start. But after a point, special terms create more pain than they are worth.

Set a simple rule: any term that changes cancellation rights, refund rights, acceptance, or start dates must be reviewed by someone who understands revenue impact. That can be a fractional controller, a startup-focused CPA, or an experienced advisor.

This is not about slowing sales. It is about avoiding deals that look great in cash but dangerous in reporting.

How to speak about revenue without misleading anyone

Founders sometimes speak in shortcuts: “We closed $300k this month.” That might mean bookings, or billed amounts, or collected cash, or recognized revenue. If the listener assumes the wrong one, trust erodes.

Pick clear words and stick to them. When you say “revenue,” mean recognized revenue. When you mean signed value, say “contracted.” When you mean cash collected, say “cash received.”

This clarity makes investors relax. It also makes internal planning more accurate.

Why clean revenue helps you raise on better terms

Investors do not only invest in growth. They invest in reliability. Reliable numbers reduce fear. Reduced fear improves your leverage.

Clean revenue recognition does not make you bigger. It makes you believable. In fundraising, belief often matters as much as size.

This is similar to IP. Strong patents and clean revenue both signal that you build with care. Tran.vc helps technical founders lock in both kinds of strength early. If you are building in AI, robotics, or deep tech and want a strong foundation, you can apply anytime at https://www.tran.vc/apply-now-form/.

A practical weekly and monthly habit set

If you want this to stay simple, do not overbuild. Build small habits.

Each week, scan new deals for odd terms: delayed start, acceptance, cancel anytime, refund language, heavy services bundled inside software. Each month, reconcile what was invoiced with what should be recognized.

When you do this from the start, you avoid the painful moment where you need to restate numbers. You also avoid the emotional stress of not trusting your own dashboard.